Market Overview

| Study Period | 2020 - 2031 |

|---|---|

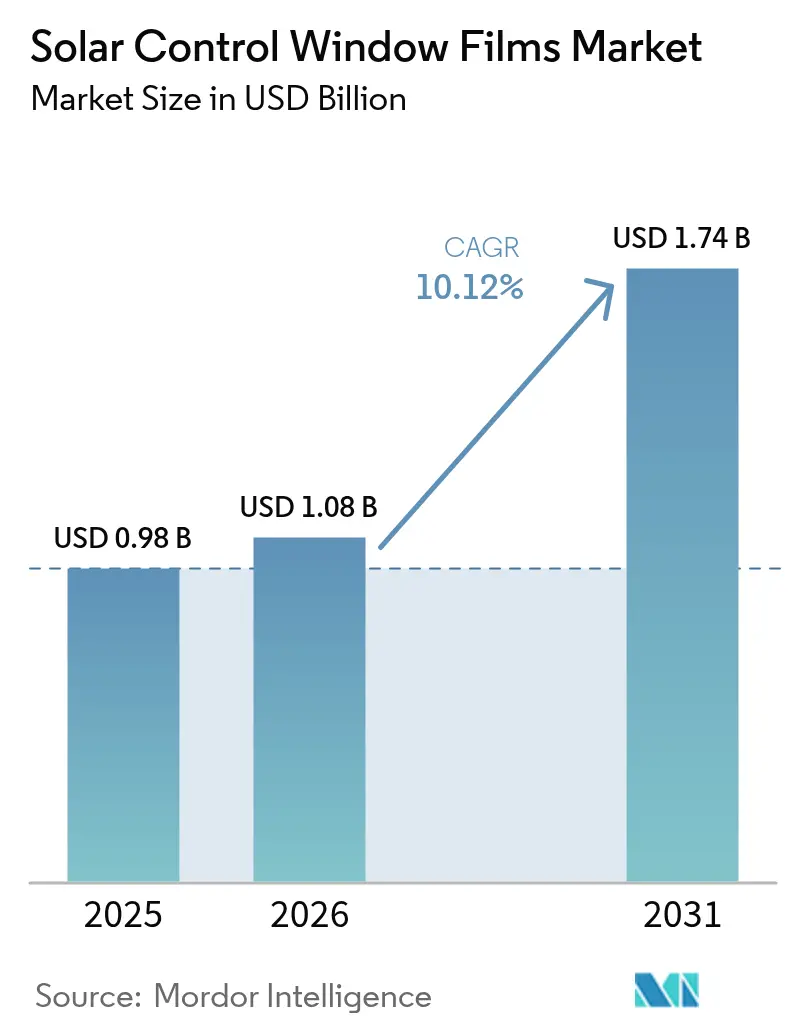

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Control Window Films Market Analysis by Mordor Intelligence

The Solar Control Window Films Market size was valued at USD 0.98 billion in 2025 and estimated to grow from USD 1.08 billion in 2026 to reach USD 1.74 billion by 2031, at a CAGR of 10.12% during the forecast period (2026-2031).International decarbonization rules, rising utility costs, and proven payback periods below three years keep demand resilient. Vacuum-coated reflective products dominate current specifications because they combine high infrared rejection with neutral aesthetics, while ceramic–metallic hybrids push performance thresholds in climates with extreme temperature swings. Asia Pacific construction booms, EU net-zero mandates, and US fiscal incentives all converge to keep volumes expanding even when raw-material costs fluctuate. These forces collectively reinforce the solar control window films market as a pivotal lever in the wider energy-efficiency value.

Key Report Takeaways

- By film type, vacuum-coated reflective variants commanded 42.35% of the solar control window films market share in 2025, and the category is advancing at a 10.44% CAGR through 2031.

- By absorber type, ceramic technology led with 45.60% revenue share in 2025; metallic absorbers post the quickest pace at 10.42% CAGR through 2031.

- By the installation stage, new-build projects accounted for 84.20% of the solar control window films market size in 2025 and continue at a 10.41% CAGR.

- By end-user industry, construction held 54.10% of 2025 revenue, while automotive applications are forecast to expand at 11.03% CAGR to 2031.

- By geography, Asia Pacific dominated with 44.40% of 2025 revenue and remains the fastest region at 10.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Solar Control Window Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Emphasis on Reducing Carbon Footprints | +2.8% | Global, with the strongest impact in the EU and North America | Medium term (2-4 years) |

| Net-Zero Building Codes in Europe Driving Low-E Film Adoption | +2.1% | Europe core, spill-over to APAC and North America | Long term (≥ 4 years) |

| Upsurge in the Asia-Pacific Construction Industry | +3.2% | APAC core, with secondary effects in MEA | Short term (≤ 2 years) |

| Awareness of UV Protection and Health Concerns | +1.5% | Global, with premium market concentration in developed economies | Medium term (2-4 years) |

| Rapid E-Commerce Warehouse Construction Requiring Day-Lighting Control in APAC | +1.8% | APAC core, emerging in Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Emphasis on Reducing Carbon Footprints

Corporate climate pledges elevate the solar control window films market because films shave 5–15% cooling loads and qualify for science-based emission targets. Peak-demand trimming aligns neatly with grid-resilience objectives in hot regions. Real-estate investment trusts also treat glazing upgrades as accretive to asset value rather than as deferred maintenance. As renewable penetration accelerates, demand-side solutions such as films gain prestige for stabilizing load profiles. This positioning solidifies procurement budgets even during capex slowdowns.

Net-Zero Building Codes in Europe Driving Low-E Film Adoption

- The EU’s recast Energy Performance of Buildings Directive compels member states to renovate 3% of public-sector floor area annually and to meet zero-emission standards by 2050. Retro-orientated targets elevate window films by boosting thermal performance without costly frame replacement. Multinationals now replicate the same envelope standards in Asia and North America, exporting European benchmarks worldwide. Lifecycle-carbon clauses also favor thin-film retrofits over high-embodied-carbon glazing swaps. Consequently, suppliers see longer order visibility in public tenders.

Upsurge in the Asia-Pacific Construction Industry

- Urbanization trajectories in China, India, and Southeast Asia accelerate completions in Tier-2 metro corridors where cooling degree-days are rising fastest. National codes referencing ASHRAE 90.1 analogues now mandate solar-heat-gain limits, ensuring that specifications include high-performance glazing. Developers prize vacuum-coated constructions because they meet performance thresholds at modest added cost. The result is a compounding feedback loop: expanding stock magnifies baseline demand while tighter codes raise per-building film intensity.

Awareness of UV Protection and Health Concerns

- Corporate tenants link indoor-environment quality with retention and productivity gains, so they specify films that block 99% of UV yet maintain daylight. WELL and LEED frameworks grant credits when UV transmission is kept below 2%, letting owners monetise health benefits. Premium rents in knowledge hubs justify incremental capex as employers compete for talent. Insurers also discount premiums for buildings demonstrating reduced UV-induced interior degradation, underscoring a multi-pronged ROI case.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution Risk from Dynamic Smart Glazing in Premium Commercial Towers | -1.8% | Global, concentrated in premium commercial segments | Long term (≥ 4 years) |

| Warranty-Linked Liability for Delamination in Hot-Humid Climates | -1.2% | APAC and MEA tropical regions, Gulf states | Medium term (2-4 years) |

| Volatile Polyester and Nano-Ceramic Raw Material Prices | -2.1% | Global, with supply chain concentration in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Substitution Risk from Dynamic Smart Glazing in Premium Commercial Towers

- Electrochromic and thermochromic units dynamically tint glass, providing glare mitigation that static films cannot match. As manufacturing costs fall, façade consultants increasingly specify these systems for double-skin or unitized curtain walls in prestige projects. Although price premiums remain 3–5 times film installations, long-term energy simulations often favor dynamic controls. Film suppliers respond by sharpening mid-market pitches and expanding retrofit channels where smart glass paybacks extend beyond 12 years.

Warranty-Linked Liability for Delamination in Hot-Humid Climates

- High vapor pressure and relentless UV in tropical latitudes erode adhesives, causing edge lift and optical haze. Large-surface failures spawn multi-tenant claims that can dwarf product revenue, challenging insurer appetite. Premium adhesive chemistries lengthen warranty coverage in Asia Pacific high-rise portfolios, yet price-sensitive owners still gravitate to low-cost films with limited guarantees. Liability risk, therefore, caps penetration in equatorial coastal cities until installer training and specification diligence improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Vacuum-Coated Dominance Drives Performance Premium

Vacuum-coated reflective products captured 42.35% of 2025 revenue, and their 10.44% CAGR keeps the solar control window films market size for this segment well ahead of dyed and clear alternatives. Architects value the micro-thin metallic stack that selectively reflects near-infrared while admitting visible light.

Film manufacturers now deploy sputter chambers using silver, indium, and nickel alloys that achieve emissivity below 0.20. In mass-housing retrofits, dyed polyester films still appeal for initial affordability, yet energy-code tightening steadily redirects volume to reflective constructions.

By Absorber Type: Ceramic Leadership Faces Metallic Challenge

Ceramic absorbers held 45.60% of 2025 revenue, reflecting their color stability, high melting point, and negligible radio-frequency interference. Automotive OEMs favor nano-ceramic layers because they avoid signal attenuation for telematics antennas. The solar control window films market share advantage may narrow, however, as refined metallic nanoparticle dispersions cut manufacturing costs and restore conductivity benefits for defogger grids.

Metallic-only films are marching at 10.42% CAGR, aided by sputter stack refinements that curb iridescence. Hybrid architectures now deposit alumina or silica atop silver seed layers, creating composite optical stacks that combine low reflectance with steep infrared rejection. Such progress blurs historic boundaries and pushes the category toward function-specific formulations, glare suppression, anti-graffiti, or photovoltaic overlay.

By Installation Stage: New-Build Concentration Creates Retrofit Opportunity

New-build integration represented 84.20% of 2025 revenue and grew in step with site-based glazing packages, yet retrofit demand remains a trillion-square-foot opportunity. Construction managers like specifying films during curtain-wall fabrication because factory conditions guarantee adhesion, optical clarity, and quality-assurance traceability.

The retrofit channel also benefits from government fiscal stimuli. Asian municipalities grant additional floor-area ratios to owners performing green refurbishments, effectively monetizing energy savings through leasable space bonuses. These carrots rapidly reshape investment calculus in favor of aftermarket films.

By End-User Industry: Construction Stability Versus Automotive Acceleration

The construction sector secured 54.10% of the 2025 volume, giving the overall solar control window films market a firm baseline demand. Office towers, hospitals, and schools specify films for operational-carbon compliance, while new suburban housing selects tinting for privacy and glare control.

Nevertheless, automotive glazing is the fast lane, clocking 11.03% CAGR through 2031 as battery-electric platforms expose cabin-heat resilience as a range determinant. OEM engineering groups now model the impact of 3 °C cabin reduction on kWh draw and integrate low-e films into sunroofs and side windows accordingly. Complementary demand surfaces in distribution warehouses, data centers, and sports arenas, each with unique optical and thermal needs. Warehouse operators in Southeast Asia install films to balance daylight with heat-load thresholds, protecting temperature-controlled zones from refrigeration spikes.

Geography Analysis

Asia Pacific commanded 44.40% of 2025 revenues and is expanding at a 10.55% CAGR, ensuring it remains the gravitational center of the solar control window films market. China’s Green Building Evaluation Standard GB/T 50378 and India’s Eco-Niwas mandate solar-heat-gain coefficients that accelerate high-selectivity film uptake.

Retrofit incentives anchor North America. The Inflation Reduction Act’s enhanced tax deduction accelerates envelope upgrades across federal and private portfolios, and California’s Title 24 revisions elevate exterior-shade coefficient thresholds that thin films meet without altering façade appearance.

Europe maintains mature penetration yet enjoys a second wave of demand tied to the 2030 “Fit-for-55” climate package.

Value Chain Analysis

The value chain starts with upstream petrochemical and specialty-material inputs, including PET base films, pressure-sensitive or curing adhesives, release liners, and performance layers for vacuum sputtering. These performance layers can use dyes, UV absorbers, and metallic or ceramic targets, depending on the required optical and infrared performance. Core manufacturing steps generally include PET film conversion, coating or dyeing, vacuum metallization or sputtering for reflective stacks, lamination of multi-layer constructions, and then slitting and rewinding into master or finished rolls. Larger branded manufacturers such as 3M, Eastman, and Saint-Gobain typically manage proprietary formulations and performance testing before supplying master rolls to regional converting, distribution, and authorized dealer networks.

On the downstream side, channel execution, including surface preparation, application technique, edge sealing, and curing conditions, has a direct bearing on optical quality and durability. This makes professional installer networks a key link for warranty outcomes, particularly in hot-humid climates where delamination risk is higher. Distribution is usually a mix of direct-to-project sales for commercial construction and a fragmented installer and dealer base for retrofit and automotive channels, which can also limit spec-compliant performance consistency. As public and commercial buyers increase documentation requirements, EPD-backed environmental reporting and certified performance data are being incorporated into procurement, tightening coordination among manufacturers, converters, and installation partners.

Competitive Landscape

Competition remains moderately fragmented. Strategic moves center on sustainability, branding, and circular design. Toray’s PICASUS series extends into advanced-mobility windshields with nano-layer stacks thinner than one micron, targeting the booming electric-vehicle glass segment. These differentiated strategies defend margins as commodity entrants undercut on price in mass-retrofit bids.

Solar Control Window Films Industry Leaders

3M

Avery Dennison Corporation

Eastman Chemical Company

Saint-Gobain

Garware Hi-Tech Films

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Retrofit-focused energy codes and compliance pathways create whitespace for films positioned as measurable envelope upgrades, especially where façade changes are constrained. In the United States, California Energy Commission enforcement of Title 24 (Part 6) recognizes NFRC-certified solar control window film as a compliant retrofit measure for existing building envelopes (2025 Energy Code enforced in 2026). This supports suppliers that can provide certified ratings, documentation packages, and trained installation capacity. Compliance-led pull also favors performance-based selling tools, including EPDs and ROI calculators, as commercial procurement increasingly requests verifiable energy and comfort outcomes rather than tint-only specifications.

Product and capacity actions by named suppliers point to two near-term opportunity areas: climate-specific architectural offerings and regionalized manufacturing. Avery Dennison expanded its architectural portfolio in India with the June 2026 launch of the Clima Architectural Window Film series, targeting commercial and residential cooling-load reduction with multiple sub-series. On the supply side, ORAFOL Europe began industrial-scale production of spectrally selective solar protection films at its Hall 10 facility in Oranienburg, Germany (June 2025), supporting shorter lead times and more local supply for European projects. Sustainability-driven differentiation is also entering mainstream specifications, including LINTEC's July 2025 release of a solar radiation control film using 100% recycled PET resin facestock, which aligns product selection with corporate decarbonization and reporting needs.

Recent Industry Developments

- July 2026: Avery Dennison Graphics Solutions introduced a new and improved XTRM PRO solar control window film line, adding an anti-fading protection layer and a more UV-durable coating for exterior-use applications. The update strengthens the company's ability to serve harsher exposure conditions where warranty performance and longevity drive specification decisions.

- June 2026: Avery Dennison launched the Clima Architectural Window Film series in India, including Clima Vista, Clima Fusion DR, Clima Sterling DR, and Clima Ceramic variants for commercial and residential buildings. The India-focused rollout broadens access to segmented solar-control performance options and supports faster channel penetration in a high-volume construction and retrofit market.

- November 2024: Eastman announced an investment to upgrade and expand extrusion capabilities for its Saflex PVB interlayer product lines at its Ghent, Belgium site, with completion targeted for 2026. The project increases regional capacity for specialized interlayers used in glazing systems, reinforcing supply availability for solar and safety performance requirements across automotive and architectural applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market includes revenue from solar control window films applied to glazing to reduce solar heat gain, UV transmission, and glare in buildings and transport uses. We count film material supplied for installation in new builds and retrofits across the major regions where these films are sold.

Scope exclusions: We exclude electrochromic smart glass, onsite liquid coatings, and decorative or privacy films that do not have a tested solar control performance rating.

Segmentation Overview

- By Film Type

- Clear (Non-reflective)

- Dyed (Non-reflective)

- Vacuum-Coated (Reflective)

- High Performance Films

- Other Film Types

- By Absorber Type

- Organic

- Inorganic / Ceramic

- Metallic

- By Installation Stage

- New-Build

- Retrofit

- By End-user Industry

- Construction

- Automotive

- Marine

- Design

- Other End-user Industry

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- Spain

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

To start the model, we pull a clean view of demand conditions and the policy signals that make solar control films relevant. Public sources, such as the International Energy Agency for buildings energy trends, the US Department of Energy for efficiency references, and the US Energy Information Administration for cooling related indicators, are used to anchor the direction and timing of demand.

We then cross-check application exposure using construction and transport activity series, supported by sources such as the US Census Bureau construction data, Eurostat construction statistics, and UN Comtrade for trade flows of film and related polymer materials as supporting context. Company filings, investor presentations, association websites, and reputable press are reviewed to understand product positioning, channel structure, and typical end user requirements. Where useful, a paid subscription covering company financials and another covering patent databases are used to sanity check supplier scale and technology change, and the sources listed here are illustrative rather than exhaustive.

Primary Interviews and Surveys

Primary work focuses on confirming what is sold as solar control film in practice, and how price and mix shift by application. We speak with manufacturers, converters, installers, distributors, and large end users across Americas, EMEA, and APAC so assumptions on retrofit share, film type mix, and average selling price movement align with replacement cycles and buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 20% | Managers: 41% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool that reconstructs film consumption from glazing exposure and adoption, followed by checks against supply side signals. The starting logic ties addressable window area in construction and the serviced vehicle parc to a penetration rate for solar control films, which is then converted to value using an ASP ladder by film type and use case.

Key inputs that shape the totals include retrofit versus new build split, installer throughput and seasonality in hotter climates, film type mix (vacuum coated, clear, dyed, high performance), absorber material mix, and typical replacement timing by application. When data gaps appear, we use bounded assumptions agreed in interviews, and then stress test them against trade movement direction, construction activity, and observed price bands from channel checks.

Forecasting is done using scenario analysis supported by simple multivariate regression, where drivers such as construction starts, cooling degree day intensity, electricity price direction, and energy efficiency policy momentum are varied within realistic ranges. Bottom-up approximations, including sampled ASP times estimated volume for select countries and channel roll-ups from installer networks, are used to adjust the final totals so the outcome stays repeatable and easy to audit.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals, and then reviewed for outliers before sign-off. We compare implied film volumes and ASP movement with what installers report, with what distributors see in ordering patterns, and with construction and transport indicators so the final number does not rely on a single data stream.

Variance checks are run at region and application levels, and unusual jumps trigger a re-check of assumptions and, when needed, follow-up conversations with interviewees. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, sharp polymer price shifts, or demand shocks. Before delivery, an analyst completes a fresh data pass so clients receive the latest updated view.

Mordor Intelligence's Solar Control Window Films Market Estimate Compared With Other Published Estimates

It is common to see different market values for solar control window films because publishers do not always count the same product set or the same selling point in the value chain. Differences also come from how retrofit demand is treated, how film performance categories are grouped, and how aggressively pricing is assumed to move over time.

A key gap driver is scope, where some figures blend wider window film categories or add adjacent solutions like smart glazing, which expands the counted revenue pool. Another driver is the valuation method, since some methods lean on broad polymer film trade values or installed project values, while our model keeps value tied to film sales on rolls with an explicit mix and ASP ladder, after separating decorative-only and untested films from solar control performance rated products, for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.98 B (2025) | |

| Industry Publisher A | USD 1.70 B (2025) | Likely counts a broader window film basket and may include adjacent categories beyond solar control window films, which inflates the value base and can shift regional weighting. |

| Global Publisher B | USD 0.95 B (2025) | Likely uses a narrower scope or a different value point, and the lower path suggests conservative ASP progression and slower retrofit uptake assumptions in early years. |

The table shows that the spread is mainly explained by what gets counted as solar control film, and whether the value reflects film material sales or a wider installed solution view. By keeping the steps visible, from addressable glazing exposure to penetration, mix, and pricing, the final estimate stays traceable to practical demand indicators and can be updated cleanly when new signals appear.

Key Questions Answered in the Report

What is the current value of the solar control window films market?

The market stood at USD 1.08 billion in 2026 and is projected to reach USD 1.74 billion by 2031 at a 10.12% CAGR.

Which region leads demand for solar control window films?

Asia Pacific accounts for 44.40% of global revenue and posts the highest growth at 10.55% CAGR through 2031.

Why are vacuum-coated reflective films gaining popularity?

They offer high infrared rejection with neutral appearance, holding 42.35% market share and expanding at 10.44% CAGR.

How do government incentives influence adoption?

Measures such as the US Inflation Reduction Act’s USD 5.00-per-sq ft deduction and EU net-zero mandates directly raise retrofit and new-build demand.

What restrains wider adoption in tropical climates?

Elevated humidity accelerates adhesive failure, causing delamination that results in costly warranty claims.

Page last updated on: