Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The North America Solar Control Window Films Market Report is Segmented by Film Type (Clear, Dyed, Vacuum-Coated, High Performance Films, Other Film Types), Absorber Type (Organic, Inorganic/Ceramic, Metallic), End-User Industry (Construction, Automotive, Marine, Design, Other End-User Industry), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

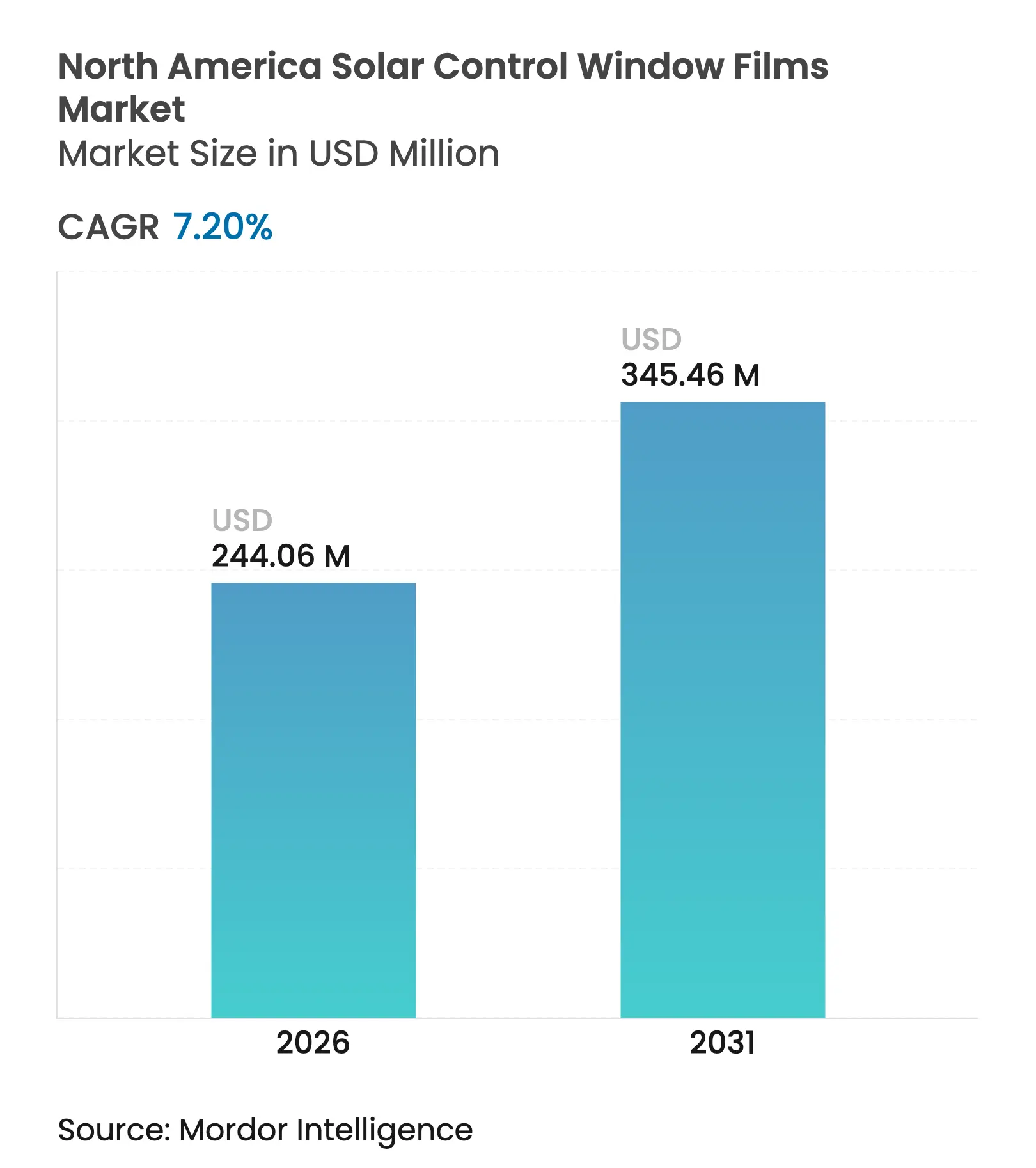

| Market Size (2026) | USD 244.06 Million |

| Market Size (2031) | USD 345.46 Million |

| Growth Rate (2026 - 2031) | 7.20 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The North America Solar Control Window Films Market size market is expected to grow from USD 227.67 million in 2025 to USD 244.06 million in 2026 and is forecast to reach USD 345.46 million by 2031 at 7.20% CAGR over 2026-2031. Growth is supported by tighter building‐energy codes, federal and state tax incentives, and expanded use of solar control films by original-equipment automotive manufacturers seeking to reduce air-conditioning loads in electric vehicles. Heightened public awareness of ultraviolet exposure risks, particularly in the Sun Belt, adds a health-protection dimension to purchasing decisions. Corporate ESG retrofits across commercial real estate demonstrate clear operating-expense savings by upgrading existing façades rather than replacing glazing systems outright. Meanwhile, dynamic supply-chain integration under USMCA allows North American producers to serve automotive and construction markets efficiently, reinforcing regional demand resilience.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent building-energy codes & tax incentives Stringent building-energy codes & tax incentives | +1.80% | United States & Canada, with state-level variations | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.80% | Geographic Relevance:United States & Canada, with state-level variations | Impact Timeline:Medium term (2-4 years) |

Rising OEM adoption in automotive to cut A/C load Rising OEM adoption in automotive to cut A/C load | +1.20% | United States & Mexico manufacturing corridors | Short term (≤ 2 years) | |||

Heightened UV-exposure & skin-cancer awareness Heightened UV-exposure & skin-cancer awareness | +1.50% | North America, particularly sun-belt states | Long term (≥ 4 years) | |||

Corporate ESG retrofits of existing glass façades Corporate ESG retrofits of existing glass façades | +0.90% | Major metropolitan areas across North America | Medium term (2-4 years) | |||

Hybrid-work home-office upgrades for glare control Hybrid-work home-office upgrades for glare control | +0.70% | Suburban residential markets, United States & Canada | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Building-Energy Codes & Tax Incentives

The 2024 International Energy Conservation Code lowered allowable air leakage for fixed fenestration from 0.40 cfm/ft² to 0.35 cfm/ft², pushing building owners toward cost-effective retrofit solutions such as high-performance films. Concurrently, the Inflation Reduction Act enables homeowners to claim a 30% credit—capped at USD 600—for qualified film purchases, while commercial properties leverage Section 179D deductions to offset installation costs[1]U.S. Congress, “Energy Efficient Commercial Buildings Deduction,” uscode.house.gov . California Title 24 and New York City Local Law 97 strengthen state-level demand, creating compliance drivers that bypass full window replacement cycles in favor of film retrofits.

Rising OEM Adoption in Automotive to Cut A/C Load

Automakers integrate solar control layers during lamination, lowering cabin heat gain by roughly 20% and extending electric-vehicle range. Pilkington’s Galaxsee glazing blocks 65% of solar heat and more than 95% of UV radiation, setting baseline specifications for factory adoption. USMCA simplifies cross-border sourcing, and Mexico’s USD 37 billion component-import market provides scale for regional glass and film producers. Demand is particularly strong in electric vehicles, where every reduction in A/C load extends battery range and reduces warranty costs related to thermal degradation.

Heightened UV-Exposure & Skin-Cancer Awareness

Public health campaigns linking indoor UV exposure to skin-cancer prevalence encourage adoption of films that block 99% of UV-A and UV-B radiation. Peer-reviewed studies confirm window films’ preventive efficacy, strengthening consumer confidence and driving purchases in healthcare, education, and residential environments[2]PubMed, “Use of UV-Protective Window Films in Skin Cancer Prevention,” pubmed.ncbi.nlm.nih.gov . Product launches such as Solar Gard’s Ultragard UV series combine compliance with legal tint limits and occupant protection, harmonizing safety and regulatory requirements.

Corporate ESG Retrofits of Existing Glass Façades

Large enterprises prioritize glazing upgrades to meet decarbonization targets without capital-intensive façade replacements. Digital Realty retrofitted 1.3 million ft² of data-center space while moving toward net-zero goals, underscoring the economic viability of film solutions in energy-intensive facilities. Oxford Properties also cites film retrofits within its pathway to carbon neutrality by 2050. Financial penalties under municipal carbon laws, especially in New York City, accelerate payback periods for film installations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Smart-glass substitution threat Smart-glass substitution threat | -1.10% | Major metropolitan areas with high-end construction | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.10% | Geographic Relevance:Major metropolitan areas with high-end construction | Impact Timeline:Long term (≥ 4 years) |

Durability & discoloration issues on IGUs Durability & discoloration issues on IGUs | -0.80% | Northern climates with extreme temperature variations | Medium term (2-4 years) | |||

Growing prevalence of low-E coated glazing Growing prevalence of low-E coated glazing | -0.60% | New construction markets across North America | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Smart-Glass Substitution Threat

Electrochromic windows achieve 17–23% building-energy savings through dynamic light and heat control, outperforming static films in optimized management systems[3]Sustainability Journal, “Energy-Saving Potential of Electrochromic Windows,” doi.org . Integration with IoT enables automated tint adjustment, adding functionality beyond the reach of conventional films. Manufacturing scale efficiencies are gradually narrowing cost gaps, bringing smart glass into mainstream commercial budgets. Although high capital costs still limit penetration, accelerating R&D suggests a competitive threat in premium construction segments over the next decade.

Durability & Discoloration Issues on IGUs

Insulated glass units often fail through sealant degradation and moisture ingress, creating fogging and discoloration that can be incorrectly attributed to aftermarket films. Field research shows polyisobutylene seals are particularly vulnerable to temperature fluctuations. When failures occur, warranty disputes reduce consumer confidence in film solutions and elevate replacement costs. Updated guidelines from the National Glass Association recommend modern seal configurations to mitigate risk, but retrofit installers must still manage customer expectations on long-term IGU performance.

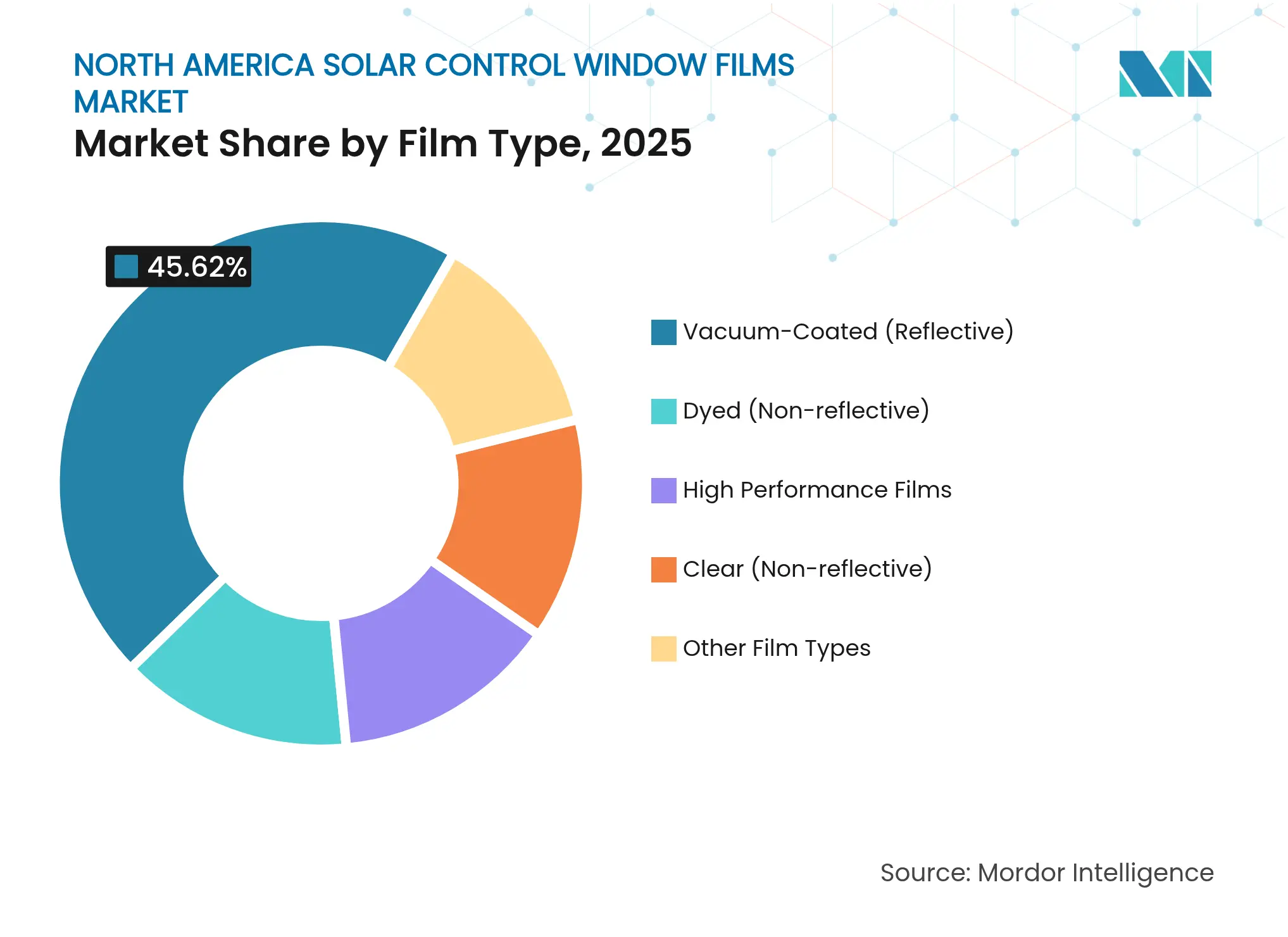

By Film Type: Reflective Performance Outweighs Aesthetic Trade-Offs

Vacuum-coated reflective films led the North America Solar Control Window Films market with a 45.62% share in 2025, thanks to sputter-deposited metallic layers that cut infrared gain without compromising visible light. These products routinely deliver Solar Heat Gain Coefficient values below 0.30, helping commercial towers meet energy codes in climate zones with high cooling loads. Demand is sustained by facility managers prioritizing operating-expense savings over exterior uniformity concerns. Dyed non-reflective products, however, are catching up by offering neutral aesthetics at lower price points and enjoying a 7.83% CAGR through 2031, propelled by suburban homeowners claiming federal tax credits. Clear non-reflective variants serve hospitals and schools that require daylighting compliance while still blocking ultraviolet exposure. High-performance hybrid films occupy a smaller revenue niche but showcase the direction of future product development through advanced ceramic layering that maintains clarity and durability over multidecade lifetimes.

Laboratory advances highlight the segment’s innovation curve. The University of Notre Dame reported quantum-optimized coatings capable of reducing cooling energy by one-third while preserving outward views, signaling potential step-change improvements in film efficacy. Manufacturers such as Eastman deploy proprietary infrared-blocking ceramic coatings combined with pressure-sensitive adhesives to raise the thermal rejection bar further. Organic-based decorative films retain relevance in interior design, yet face mounting competition from integrated low-E glass that arrives pre-tinted from the factory. Still, the retrofit appeal of films—quick installation and minimal tenant disruption—keeps the North America Solar Control Window Films market firmly in play, even as technically superior yet costlier smart glass solutions vie for future specification.

Note: Segment shares of all individual segments available upon report purchase

By Absorber Type: Ceramic Dominance Faces Organic Innovation

Inorganic ceramic absorbers held 49.86% of the North America Solar Control Window Films market size in 2025 due to exceptional thermal stability and near-zero signal interference, a critical consideration for 5G-ready office complexes. Commercial buyers value ceramics for their decades-long service life and consistent solar performance, while the segment also benefits from falling unit costs as sputter-coating equipment scales. Organic absorbers are growing at an 8.07% CAGR, reflecting improvements in polymer resilience that counteract historical discoloration concerns. Production flexibility allows organic systems to be cast in vibrant colors, meeting architectural themes without adding metallic sheen.

Metallic absorbers remain a high-performance option but face constraints where electromagnetic compatibility or visual reflectivity is unacceptable. Novel concepts such as molecular solar thermal storage (MOST) systems—thin-film layers that absorb sunlight and later release low-grade heat—hint at disruptive absorber technologies on the horizon. Research into flexible photochromic films that autonomously adjust tint in response to UV intensity illustrates the sector’s evolving capabilities. For now, ceramic absorbers remain the benchmark for premium performance, yet the pipeline of organic and hybrid innovations ensures intensifying competition within the North America Solar Control Window Films market.

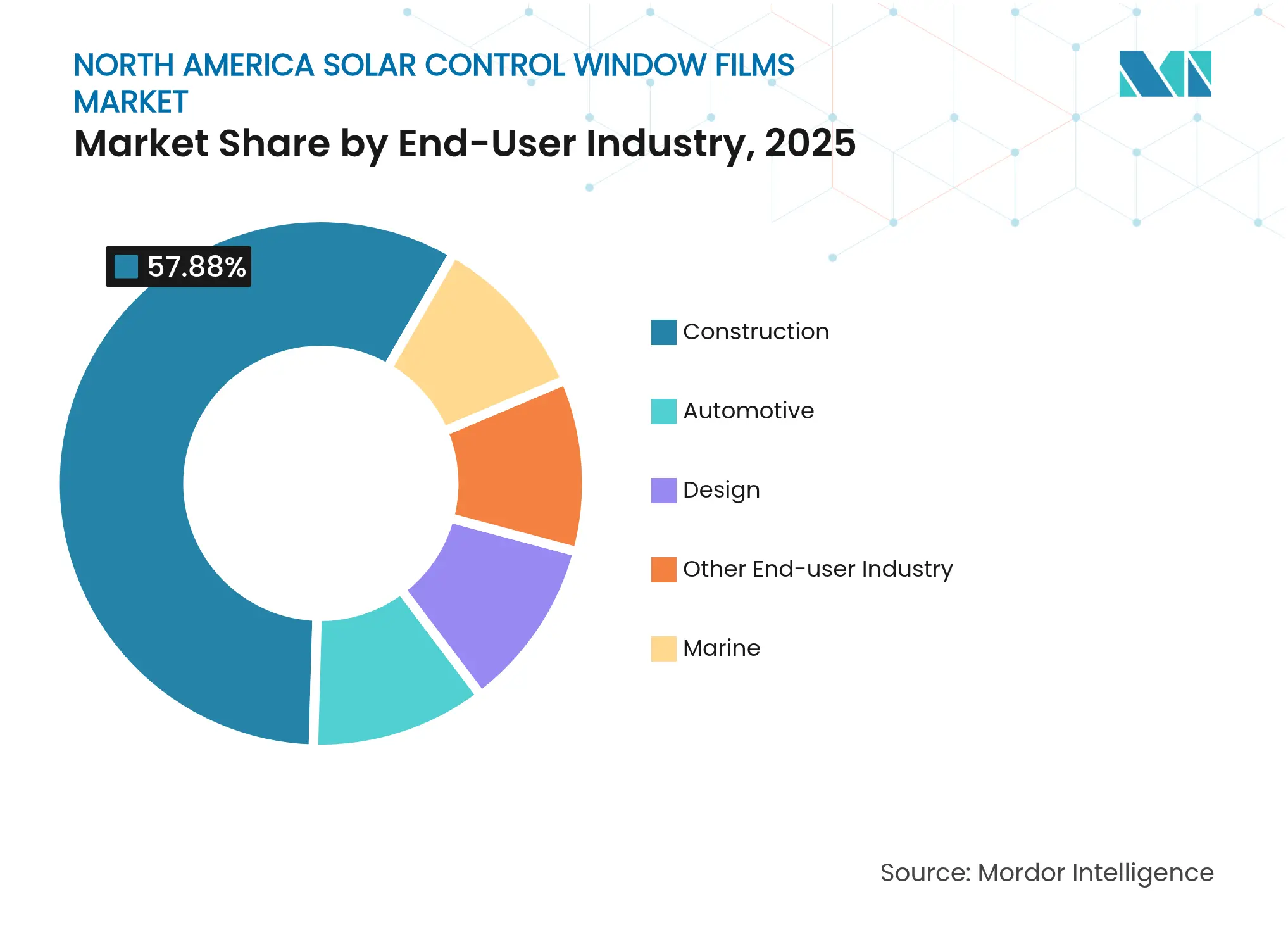

By End-User Industry: Construction Maturity Meets Automotive Acceleration

Construction applications constituted 57.88% of the North America Solar Control Window Films market size in 2025, reflecting the long-established role of films in energy retrofits for office towers, retail centers, and institutional buildings. Corporate ESG frameworks and local building-performance mandates drive continuous demand, particularly in cities where full façade replacements disrupt leasing schedules and require large capital outlays. Educational districts and healthcare systems adopt films to meet glare and UV criteria while preserving daylighting, bolstered by documented productivity and wellness gains.

Automotive adoption is the fastest-growing at 8.22% CAGR, propelled by EV platform design requirements that prioritize cabin thermal control to conserve battery capacity. OEM integration yields film layers laminated within glass, delivering factory-level clarity and durability while minimizing aftermarket variability. USMCA regional supply chains shorten lead times for American, Canadian, and Mexican assembly plants. Marine and specialty vehicle markets, though smaller, rely on films for safety and visibility under high-glare conditions. Design-oriented applications—retail storefronts, hospitality, and interior partitions—expand as architects employ films for branding or privacy without the cost of custom glass fabrication. Regulatory momentum, including Texas’s incorporation of protective window films into school safety standards, continues to create new verticals for adoption.

Note: Segment shares of all individual segments available upon report purchase

The United States captured 75.30% of North America Solar Control Window Films market share in 2025 and is projected to grow at a 7.55% CAGR to 2031, buoyed by federal tax credits, state-specific energy codes, and municipal carbon-reduction ordinances. Title 24 in California compels builders to meet stringent Solar Heat Gain Coefficient targets, while New York City’s Local Law 97 imposes increasing fines on inefficient buildings, both conditions that favor film retrofits over glass replacement. OEM glass suppliers located across the Midwest benefit from existing logistics corridors that support rapid deployment to automotive assembly lines.

Canada represents a sizeable yet underpenetrated component of the North America Solar Control Window Films market, aided by federal and provincial climate actions that mirror U.S. policy incentives. The extensive 3M-authorized dealer network spanning more than 60 outlets provides national coverage, enabling large multi-site retrofits for commercial real-estate portfolios. Budget allocations for public-sector infrastructure modernization further support uptake in schools and hospitals, particularly in provinces applying carbon-pricing mechanisms that raise utility costs.

Mexico’s role is primarily supply-chain-driven, anchored by its robust automotive manufacturing sector and increasing adoption of LEED-compliant building practices in urban centers. Manufacturing plants in states such as Nuevo León integrate solar control films into vehicle glass destined for U.S. dealerships, illustrating seamless regional procurement. Cross-border trade under USMCA has expanded intra-regional shipments by 50% since 2020, fostering cost efficiencies that ripple through the North America Solar Control Window Films market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

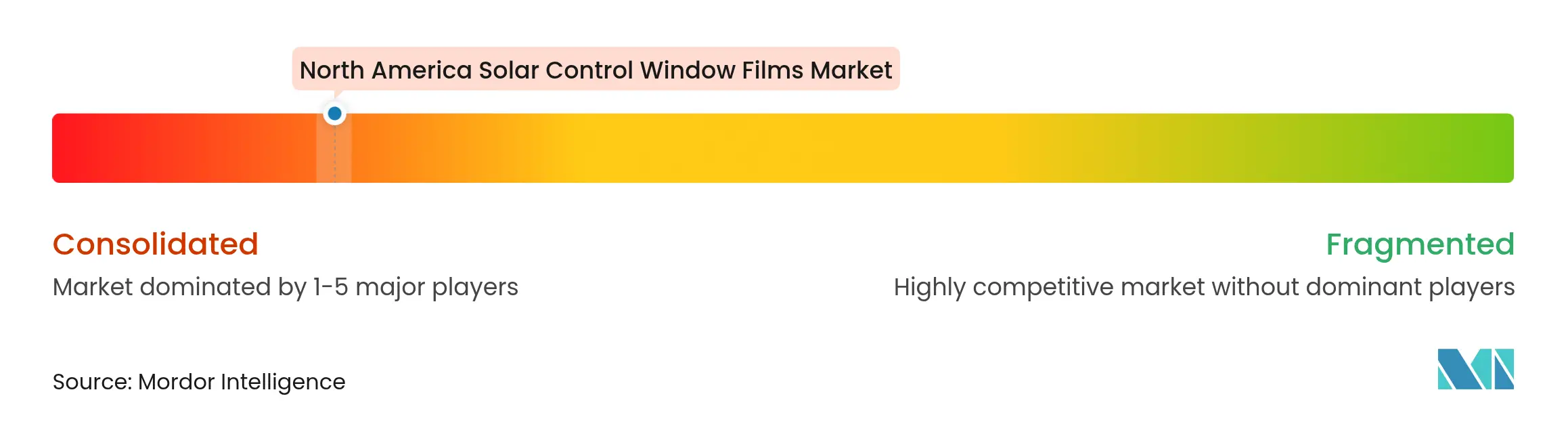

Market Concentration

The North America Solar Control Window Films market is highly consolidated, with 3M, Eastman Chemical, and Saint-Gobain occupying leadership positions based on patent portfolios, vertically integrated manufacturing, and dealer networks. 3M’s heritage as the original window-film inventor underpins significant brand equity, while its U.S. and Canadian production footprint ensures short order-to-delivery cycles. Eastman continues to diversify its Saflex product family, backed by recent investments in European interlayer capacity that will ultimately supplement North American supply. Saint-Gobain leverages global fabrication know-how to integrate film technology within broader façade systems, positioning itself for the transition toward dynamic glazing.

Strategic moves center on R&D and channel expansion rather than price competition. PPG Industries directs significant R&D outlays toward low-carbon coating chemistries that complement energy-saving glazing solutions, reinforcing its USD 18.2 billion coatings business with sustainability credentials. OEM partnerships in the automotive sector represent the most dynamic battleground, as film suppliers vie to embed their solutions into laminated glass at the factory level, effectively locking in multiyear production volumes. Passive-film specialists also explore cooperation agreements with smart-glass developers to maintain relevance as electrochromic technologies mature.

New entrants focus on niche functionalities—such as anti-viral coatings or embedded photovoltaic layers—but face high certification and warranty hurdles in the regulated North American construction environment. M&A activity remains selective, targeting small specialty formulators or regional distributors to accelerate geographic penetration. Overall, product differentiation around optical clarity, durability, and warranty support defines competitive advantage more than headline pricing, insulating established leaders from aggressive commoditization.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The North America solar control window films market report include

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.