Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

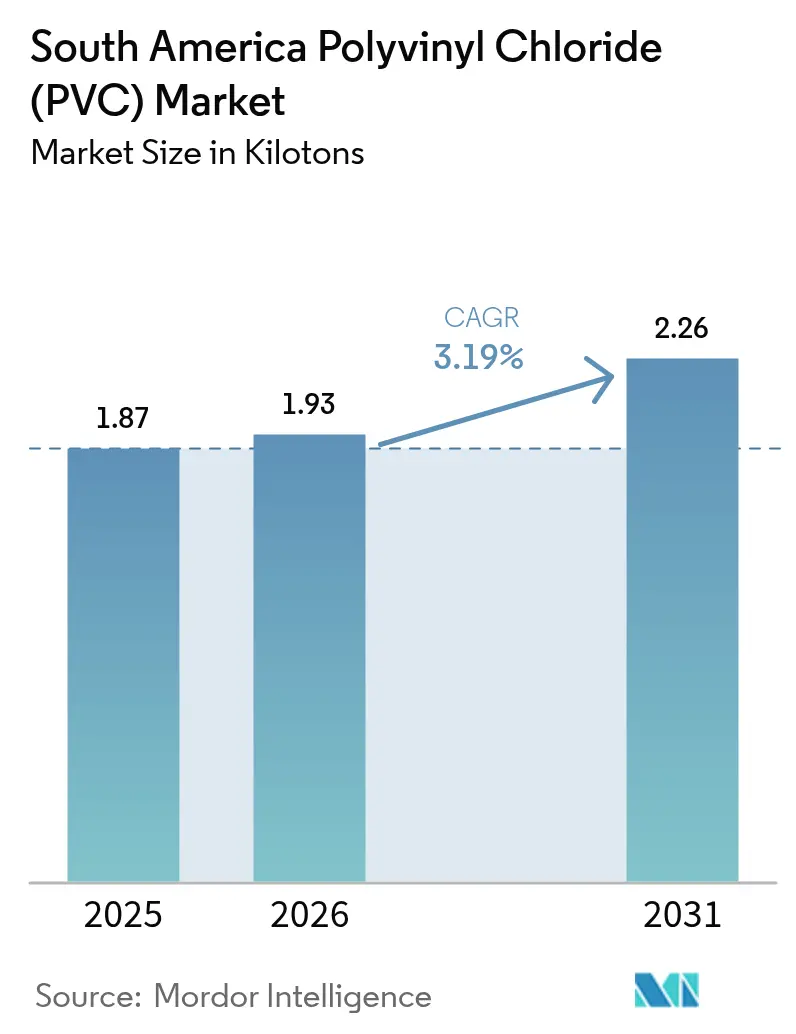

| Base Year Market Size (2025) | 1.87 kilotons |

| Market Volume (2026) | 1.93 kilotons |

| Market Volume (2031) | 2.26 kilotons |

| Growth Rate (2026 - 2031) | 3.19% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Polyvinyl Chloride (PVC) Market Analysis by Mordor Intelligence

The South America Polyvinyl Chloride Market size in 2026 is estimated at 1.93 kilotons, growing from 2025 value of 1.87 kilotons with 2031 projections showing 2.26 kilotons, growing at 3.19% CAGR over 2026-2031. Robust public-sector spending on water and sanitation networks, accelerated urbanization, and sustained manufacturing output underpin this expansion. Brazil’s 2020 Sanitation Legal Framework compels universal water access and near-complete sewage coverage by 2033, pushing utilities toward high-performance PVC piping that commands roughly three-fifths of conveyance capex. Integrated feedstock ecosystems in Brazil and Argentina translate into lower vinyl chain costs, granting incumbents a price buffer against import parity pressures. Meanwhile, sustainability imperatives steer compounders toward calcium-zinc stabilizers and renewable plasticizers that cut product carbon footprints up to 80% while safeguarding material performance.

Key Report Takeaways

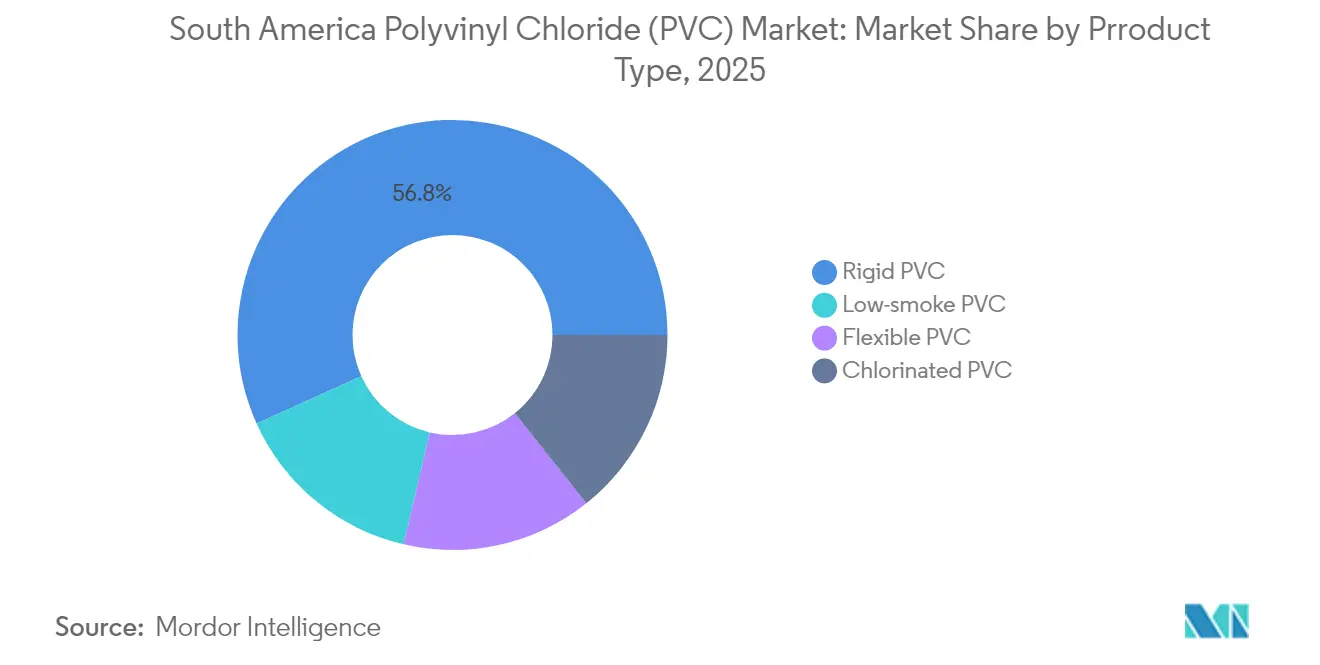

- By product type, Rigid PVC held a 56.75% share of the South America polyvinyl chloride market in 2025; Low-smoke PVC is forecast to grow at a 3.8% CAGR through 2031.

- By stabilizer type, Calcium-based systems commanded 40.78% of the South America polyvinyl chloride market share in 2025, while Tin/Organotin stabilizers are projected to post the quickest 3.55% CAGR to 2031.

- By application, Pipes and Fittings captured 45.89% of the South America polyvinyl chloride market size in 2025, whereas Wires and Cables are projected to expand at a 3.6% CAGR over 2026–2031.

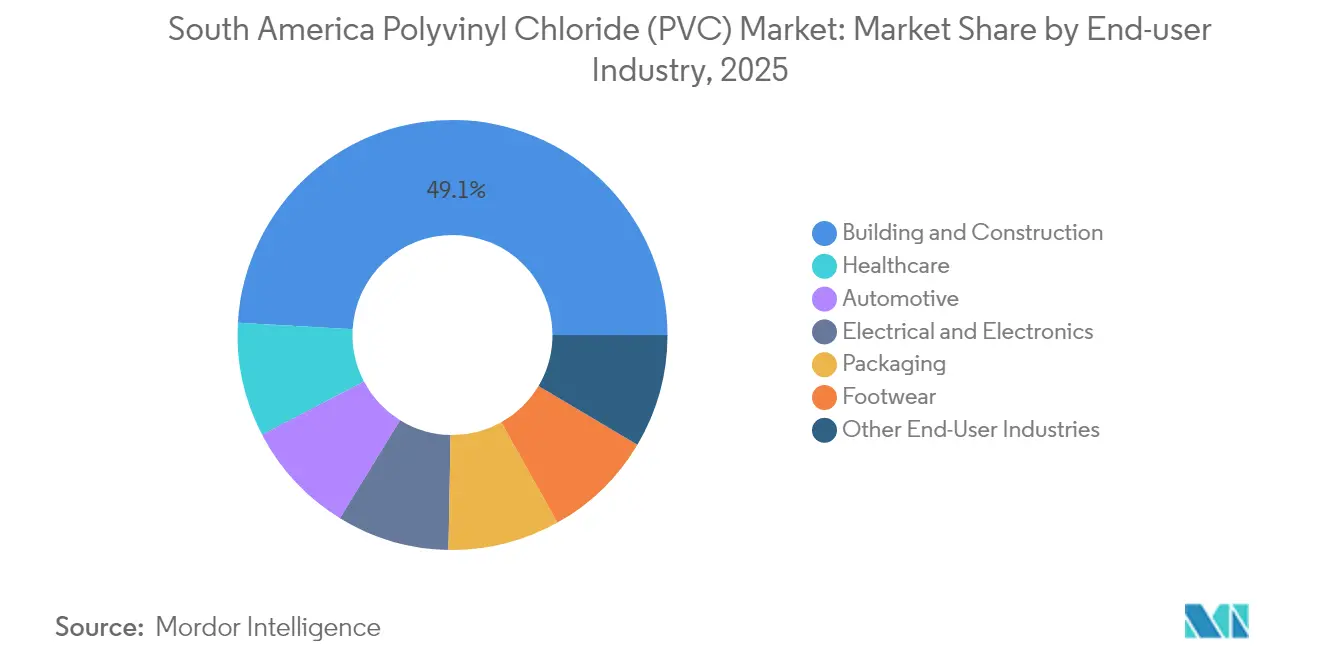

- By end-user industry, Building and Construction accounted for 49.10% of the South America polyvinyl chloride market in 2025; Healthcare is advancing at a 3.95% CAGR to 2031.

- By geography, Brazil controlled 52.85% of regional volume in 2025, while Colombia is on track for the fastest 3.45% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Polyvinyl Chloride (PVC) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-led surge in pipe and fittings demand | +0.8% | Brazil, Colombia, Peru, Argentina spillover | Medium term (2-4 years) |

| Rising lightweighting in South American automotive production | +0.3% | Brazil, Argentina | Short term (≤ 2 years) |

| Expansion of PVC-based medical disposables | +0.4% | Regional with Brazil concentration | Medium term (2-4 years) |

| Lead-pipe replacement schemes in Brazil and Peru | +0.5% | Brazil, Peru | Long term (≥ 4 years) |

| Domestic chlorine-vinyl integration lowering feedstock costs | +0.6% | Brazil, Argentina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction-led Surge in Pipe and Fittings Demand

Annual spending of BRL 27.6 billion is required through 2035 to bridge water-service gaps affecting 100 million Brazilians without sewage collection and 35 million lacking treated water[1]Organisation for Economic Co-operation and Development, “Driving Performance at Brazil's National Agency for Water and Basic Sanitation,” oecd.org. The 2020 Sanitation Legal Framework obliges 90% urban sewage coverage by 2033, prompting utilities to phase out corroded metal lines in favor of PVC systems that deliver 50-year lifespans and four-to-one disease-prevention paybacks for every real invested. Colombia’s potable-water concessions, Peru’s mine-water programs, and an IDB Invest-backed USD 135 million Maranhão project underscore region-wide momentum for standardized PVC infrastructure. Faster installation, lower maintenance, and corrosion resistance consolidate PVC’s value proposition across distribution, collection, and treatment networks.

Rising Lightweighting in South American Automotive Production

Vehicles assembled in Brazil and Argentina increasingly embed specialty PVC compounds in dashboards, wire harnesses, and under-hood seals to cut mass, improve flame resistance, and enhance cabin acoustics. Brazil’s automotive sector, equal to 25% of industrial GDP, is pursuing higher local content under programs that reward efficiency-driven materials adoption. Domestic compounders have introduced high-flow, low-fogging PVC grades that satisfy electric-vehicle thermal-management standards while aligning with region-specific cost and logistics realities. Preferential trade rules in MERCOSUR ease cross-border component circulation, encouraging harmonized specifications that elevate PVC demand in wiring and interiors.

Expansion of PVC-based Medical Disposables

National payers are boosting outlays on single-use devices to reduce hospital-acquired infections, a shift reinforced by Brazil’s ANVISA 2024-2025 priority list calling for tighter reprocessing guidance. The South America polyvinyl chloride market benefits as intravenous tubing, blood bags, and respiratory components leverage PVC’s clarity, kink resistance, and steam-sterilization compatibility. Colombia and Peru are channeling public funds into hospital upgrades that favor domestically made, standards-compliant PVC articles. Producers responding with non-phthalate, biocompatible plasticizer systems gain access to tenders linked to multilateral lenders that require conformance with international quality benchmarks.

Domestic Chlorine-vinyl Integration Lowering Feedstock Costs

Braskem’s integration from ethylene through PVC, aided by a USD 100 million debottlenecking plan to raise polymer capacity by 139,000 tons across three Brazilian states, limits exposure to global freight volatility and cushions processors against import parity prices. Unipar Carbocloro’s 82% nameplate utilization underscores operational leverage realized through in-house chlor-alkali assets. During logistics disruptions, local producers enjoyed freight savings of USD 180–200 per ton relative to landed imports, enabling competitive exports and stable domestic supply

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity perception and tightening EHS regulations | -0.4% | Brazil, Colombia | Medium term (2-4 years) |

| Phthalate-free mandates in toys and childcare products | -0.2% | Brazil, Argentina | Short term (≤ 2 years) |

| Volatile electricity tariffs inflating electrolysis OPEX | -0.3% | Brazil, Argentina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Toxicity Perception and Tightening EHS Regulations

Broader adoption of lifecycle assessments and mandatory disclosure frameworks elevates compliance costs for small-to-mid-size PVC converters. MERCOSUR food-contact rules and ANVISA medical-device dossiers now demand granular additive traceability, pushing producers to invest in digital material-passport systems. Advocacy groups spotlight chlorine processes and additive residues, steering institutional buyers toward eco-labels. Counter-measures include renewable plasticizers such as Pevalen Pro 100 that slash product CO₂ footprints by 80% and bolster circular-economy credentials.

Volatile Electricity Tariffs Inflating Electrolysis OPEX

Chlor-alkali energy costs in Brazil and Argentina can swing 30% within a quarter, distorting vinyl-chain margins and discouraging small chlor-alkali entrants. Integrated players mitigate volatility through captive power or long-term renewable PPAs, yet merchant converters see pass-through lags that squeeze spreads. Recent energy-integration models show potential 28.54% heating and 5.91% cooling utility cuts for large-scale plants when advanced heat-recovery networks are employed, offering a roadmap to more stable economics[2]Antonio Mendivil-Arrieta et al., “Energy Integration and WEP Technical Evaluation of a Large-Scale PVC Production Process,” mdpi.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid PVC Dominates Infrastructure Applications

Rigid PVC accounted for 56.75% of regional volume in 2025 as potable-water projects and building profiles prioritized its durability and pressure rating. The South America polyvinyl chloride market size tied to rigid formulations is forecast to progress in tandem with Brazil’s annual BRL 27.6 billion water-security outlays, securing a dependable base load for resin demand. Low-smoke PVC, though representing a smaller tonnage, will clock a 3.8% CAGR on the back of tighter fire-safety rules in high-rise commercial construction.

Flexible PVC applications span automotive sheathing and healthcare tubing, benefitting from cold-temperature flexibility and clarity. Chlorinated PVC appeals to industrial conveying and hot-water piping segments, adding premium margin streams. Clear rigid grades, essential for pharmaceutical inspection windows and food-processing sight-glasses, grow steadily as GMP investments materialize. Collectively, the product mix evolution ensures the South America polyvinyl chloride market remains diversified while anchored in core infrastructure.

By Stabilizer Type: Calcium-based Systems Lead Environmental Transition

Calcium-zinc packages secured 40.78% of stabilizer tonnage in 2025, aided by cost parity with legacy lead compounds and straightforward drop-in processing. Tin/Organotin alternatives, although higher priced, will outpace the broader South America polyvinyl chloride market at 3.55% CAGR because of superior heat-ageing resistance demanded in wire jacketing and medical devices. Lead stabilizers are retreating under phased bans, whereas barium-zinc liquids serve niche extrusions needing elevated gloss.

Market shifts favor additive suppliers that can pair performance claims with life-cycle data sets recognized by regulators. Integrated resin makers bundling stabilizers, lubricants, and color concentrates into single invoices are meeting converter demand for simplified procurement and robust technical troubleshooting.

By Application: Pipes and Fittings Anchor Market Growth

Pipes and Fittings captured 45.89% of South America polyvinyl chloride market share in 2025 and retain the highest absolute volume expansion through 2031 as utility-scale water schemes are rolled out in Brazil, Colombia, and Peru. Wires and Cables—propelled by grid digitalization and data-center interconnect upgrades—register the quickest 3.6% CAGR, supported by PVC’s dielectric strength and flame-retardant performance.

Films and Sheets serve greenhouse roofing and shrink-sleeve labels, whereas Bottles absorb beverage and pharmaceutical rinses where chemical inertness is critical. Profiles, Hoses, and Tubing supply a variety of sectors, from irrigation to industrial ventilation, ensuring breadth in demand drivers.

By End-User Industry: Building and Construction Drives Regional Demand

49.10% of PVC resins in 2025 ended in Building and Construction, underscoring PVC’s entrenched status in window frames, conduit, and roofing membranes. Automotive customers represent the second-largest draw, leveraging PVC for door-seal noise abatement and interior feel. Healthcare is the fastest mover at 3.95% CAGR as clinics specify sterile single-use PVC sets co-developed with multinational device firms. Electrical and Electronics applications ride on renewable-energy rollouts, while Packaging and Footwear sustain baseline demand through consumer staples and lifestyle wear.

Geography Analysis

Brazil supplied 52.85% of regional demand in 2025, fortified by integrated ethylene-to-PVC chains and a policy mix that favors domestic producers through tariff protection. Automotive OEM clusters in São Paulo and Minas Gerais adopt lightweight PVC parts to meet fleetwide efficiency stipulations, and ANVISA’s stricter medical regulations galvanize investments in cleanroom extrusion for blood-bag film.

Colombia will lead growth at 3.45% CAGR through 2031 as its 5G build-out and potable-water concessions amplify demand for wire insulation and pressure pipe. Argentina’s macroeconomic volatility tempers short-run prospects, yet energy integration projects and automotive exports anchor a stable consumption base. Chile’s copper mines sustain specialty hose and liner demand, whereas Peru couples mining-driven infrastructure with urban pipeline replacement schemes that deploy PVC for both potable and effluent networks. Smaller economies—Ecuador, Uruguay, and Paraguay—consume resin for agriculture and light construction, adding incremental tonnage through regional distributors.

Regulatory Landscape

PVC in South America operates under a mix of product-safety rules, particularly for packaging and medical uses, and trade defenses that affect resin and additive choices. In the MERCOSUR bloc, food-contact plastics are governed through technical regulations built around positive lists of authorized substances (monomers, polymers, and additives), with national regulators transposing these resolutions into domestic rules.

Brazil is a key compliance anchor for the region because ANVISA administers food-contact plastics requirements and incorporates MERCOSUR updates into Brazilian regulation, including RDC No. 961/2025 (effective February 2025, transposing GMC Resolution 28/2024) and RDC No. 979/2025 (published June 2025, incorporating MERCOSUR Resolution 2/2025). On the trade side, Brazil increased the anti-dumping tariff on U.S. suspension-grade PVC to 43.7% in May 2025, reinforcing domestic producers' positioning against import pressure while converters manage documentation demands for additive traceability under tightening EHS scrutiny.

Value Chain Analysis

The regional PVC value chain runs from hydrocarbon and salt-based inputs to integrated chlor-alkali, EDC/VCM, and polymerization assets concentrated in Brazil and Argentina, then through compounders and converters into construction materials, cables, automotive parts, and medical disposables. Integrated producers such as Braskem and Unipar Carbocloro link chlorine (from electrolysis) with downstream vinyls and PVC, supporting higher supply stability for large-volume pipe and profile extrusion as well as specialty grades.

Downstream, a large share of consumption flows into construction and infrastructure, which raises the role of local pipe and fittings manufacturers and distributors. Trade acts as a balancing lever: Brazil recorded 712,000 tons of PVC production in 2024 (down 3.6% year over year) while imports rose to 554,000 tons (up 37.5%), intensifying price competition and increasing the importance of anti-dumping actions and logistics. Cross-border dynamics are pronounced between Brazil and Argentina, with Brazil accounting for 54% of Argentina's PVC imports by value in 2024 and acting as the destination for 74% of Argentina's PVC exports, keeping MERCOSUR movement and port-to-plant logistics central to regional availability and working-capital management.

Competitive Landscape

The market is consolidated in nature. Integrated petrochemical majors lead resin output, with Braskem, Unipar Carbocloro, and Orbia holding a major share. Process-efficiency upgrades, such as advanced heat-recovery retrofits documented to shave 28.54% of heating loads, are diffusing among top-tier producers and will likely cascade to mid-size converters through shared-savings contracts. On the downstream side, compounders specializing in non-phthalate plasticizers and calcium-zinc stabilizers secure OEM approvals from medical and automotive clients, opening sticky revenue streams. Anti-dumping measures isolate domestic supply from volatile spot imports, encouraging long-term offtake agreements between resin makers and pipe extruders.

South America Polyvinyl Chloride (PVC) Industry Leaders

Braskem

Formosa Plastics Corporation

Orbia

Unipar Carbocloro

Westlake Vinnolit GmbH& Co.KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on upgrading the regional product mix and improving cost resilience in electro-intensive parts of the chain. In Brazil, the sanitation investment push tied to the 2020 Sanitation Legal Framework (coverage targets through 2033) supports a standardized pull for pressure pipe and fittings, underpinning demand for consistent rigid PVC supply and converter capacity aligned with public procurement requirements. On the compliance side, ANVISA's 2025 updates to food-contact positive lists (RDC 961/2025 and RDC 979/2025) create room for additive systems and formulations that can simplify regulatory dossiers and traceability in packaging and healthcare applications.

Producers are also working on differentiated grades and operational flexibility. Unipar's emulsion PVC expansion at Santo Andre, with the 6,000 tons per year project conclusion referenced for April 2026, reflects a shift toward higher-value PVC that competes less directly with commodity imports. Modernization steps such as transitioning electrolysis technology at Cubatao support energy-efficiency and sustainability positioning for chlor-alkali-linked PVC production. These moves align with converter interest in non-phthalate plasticizers and calcium-zinc stabilizers for medical and consumer applications, where buyer specifications and compliance documentation are tightening across the region.

Recent Industry Developments

- July 2026: Unipar Carbocloro confirmed its Camacari, Brazil facility is operating with 100% renewable energy sourced from the Tucano Wind Farm, reinforcing its energy-cost and decarbonization strategy for chlorine and PVC-linked operations. The company also referenced a second expansion phase planned for the second half of 2026 focused on chlorine purification, which supports higher-value product flexibility and supply reliability for downstream customers.

- May 2026: Brazil reported Q1 2026 recurring EBITDA of BRL 1 billion, with results supported by improved international resin spreads in its Brazil and South America segment. The update highlighted how spread recovery and operational execution can quickly change cash generation capacity for integrated resin producers that supply regional PVC converters.

- May 2025: Brazil raised its anti-dumping tariff on U.S. suspension-grade PVC from 8.2% to 43.7% following petitions from domestic producers. The measure changed import economics for commodity PVC, influencing procurement strategies for pipe, profile, and cable converters across South America.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the demand and supply of polyvinyl chloride (PVC) within South America, measured in physical volume, across the main uses where PVC is processed into finished and semi-finished goods.

Scope exclusions: The sizing excludes PVC demand outside South America and does not convert the market into a value estimate in USD.

Segmentation Overview

- By Product Type

- Rigid PVC

- Clear Rigid PVC

- Non-Clear Rigid PVC

- Flexible PVC

- Clear Flexible PVC

- Non-Clear Flexible PVC

- Low-smoke PVC

- Chlorinated PVC

- Rigid PVC

- By Stabilizer Type

- Calcium-based (Ca-Zn)

- Lead-based (Pb)

- Tin / Organotin (Sn)

- Barium-based and Liquid Mixed Metals

- By Application

- Pipes and Fittings

- Films and Sheets

- Wires and Cables

- Bottles

- Profiles, Hoses and Tubing

- Other Applications

- By End-User Industry

- Building and Construction

- Automotive

- Electrical and Electronics

- Packaging

- Footwear

- Healthcare

- Other End-User Industry

- By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and to build an initial demand picture for PVC in South America before assumptions were tested. We used public sources such as national statistics offices in key countries, UN Comtrade trade tables, World Bank macro indicators, and industrial production and construction activity series published by central banks and ministries.

To make sure the PVC story lines up with what can be observed in the real economy, company annual reports, investor presentations, association websites, and credible regional business press were reviewed for capacity changes, maintenance shutdowns, and downstream consumption signals, especially in construction products. In parallel, a paid subscription for company financials and another paid source for import and export shipment-level data were used selectively to cross-check volumes and identify timing shifts. The desk sources listed here are illustrative only, and many other public references were used for data collection, clarification, and cross-verification.

Primary Interviews and Surveys

Primary work was used to validate PVC volume flows, application mix, and the practical price and availability dynamics that are not fully visible in public data. We spoke with a mix of resin producers, compounders, converters, distributors, and large end users, and coverage was balanced across the main South American demand centers so that country-level differences did not get averaged out.

These conversations helped confirm operating rate expectations, substitution patterns versus other plastics, and how construction and infrastructure activity translates into actual PVC consumption. The interview takeaways were then used to tune the final model assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 17% | APAC: 41% |

| Mid tier: 56% | Functional/Unit leaders: 41% | EMEA: 34% |

| Smaller Players: 19% | Managers: 42% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using both top-down and bottom-up logic, with the core structure anchored on a demand pool reconstructed from regional consumption signals and then reconciled with supply availability. In practice, the top-down view was shaped by country-level indicators tied to PVC usage and then adjusted for trade inflows and outflows so the regional PVC balance made sense.

Key inputs that guided the model included PVC consumption by major application group, with construction-linked uses treated as the most sensitive, construction output and housing activity trends, infrastructure spending direction, manufacturing activity for relevant conversion categories, and import and export movement timing. For reasonableness checks, we used selective bottom-up approximations, such as sampled volume-by-application builds and supplier and channel checks on utilization and availability. Where data gaps existed, we used conservative ranges that were validated again in follow-up calls.

Forecasts were prepared using scenario analysis, where baseline demand is linked to the expected pace of construction and industrial activity, and then tested against expert views on operating rates, trade behavior, and substitution. Where the outlook was uncertain, assumptions were kept simple and traceable, and sensitivity was reviewed so a single input did not dominate the outcome.

Data Validation & Update Cycle

Outputs were checked through multiple steps so the final volumes align with independent signals and do not drift due to one optimistic or conservative input. Analysts compare the final consumption trajectory with trade patterns, macro indicators, and known capacity and operating rate developments, and then review variances that fall outside expected ranges before sign-off.

If a major mismatch appears, follow-up outreach is triggered with industry participants to re-check the underlying assumption and the timing of changes. Reports are refreshed annually, and interim updates are completed when material events occur, such as plant outages, new capacity starts, or policy changes impacting construction demand. Before delivery, a final review pass is performed to ensure the latest information is reflected consistently across sizing, narrative, and charts.

Mordor Intelligence's South America Polyvinyl Chloride Pvc Market Size Measured Against Other Published Estimates

It is normal to see different PVC market sizes for South America because publishers do not always measure the same thing, and they can also use different base years and conversion steps. The differences usually come from geography coverage, whether the number is a value or a volume, and how trade and downstream usage are treated.

The table shows a wide spread mainly because some sources publish the PVC market in USD value for 2024, while the baseline here is reported as volume for 2025 to 2026, and under Mordor Intelligence's scope the market is sized in kilotons based on regional PVC consumption rather than pricing-led revenue expansion.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.87 M (2025) | |

| Regional Consultancy A | USD 4.70 B (2024) | Reports the market in USD value and can lift totals when price assumptions, currency timing, and revenue attribution across applications are set differently from a pure volume approach. |

| Industry Publisher B | USD 2.25 B (2024) | Uses a broader LATAM framing rather than South America only, and its type-level split can miss trade and conversion adjustments that change the effective demand pool. |

Taken together, the comparison points to three repeatable drivers of variance, which are unit of measure, geographic boundary, and how trade and downstream conversion are reconciled. By keeping the steps tied to observable consumption indicators and then cross-checking them with supply and trade signals, the estimate stays transparent and easier to replicate year to year.

Key Questions Answered in the Report

How large is PVC demand in South America today?

Regional consumption reached 1.93 kilotons in 2026 and is projected to hit 2.26 kilotons by 2031, equivalent to a 3.19% CAGR.

Which country drives most PVC usage in South America?

Brazil held 52.85% of total volume in 2025, powered by integrated resin capacity and sizable water-infrastructure projects.

What application segment uses the most PVC?

Pipes and Fittings commanded 45.89% of demand in 2025 thanks to ongoing water and sewage network upgrades.

Which PVC product shows the fastest growth?

Low-smoke PVC will expand at 3.8% CAGR through 2031 as stricter building-code fire requirements gain traction.

What is propelling healthcare PVC demand?

Hospital expansions and ANVISA's sterility rules are boosting single-use PVC medical devices, driving a 3.95% CAGR in healthcare usage.

Page last updated on: