Polyvinyl Alcohol (PVA) Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

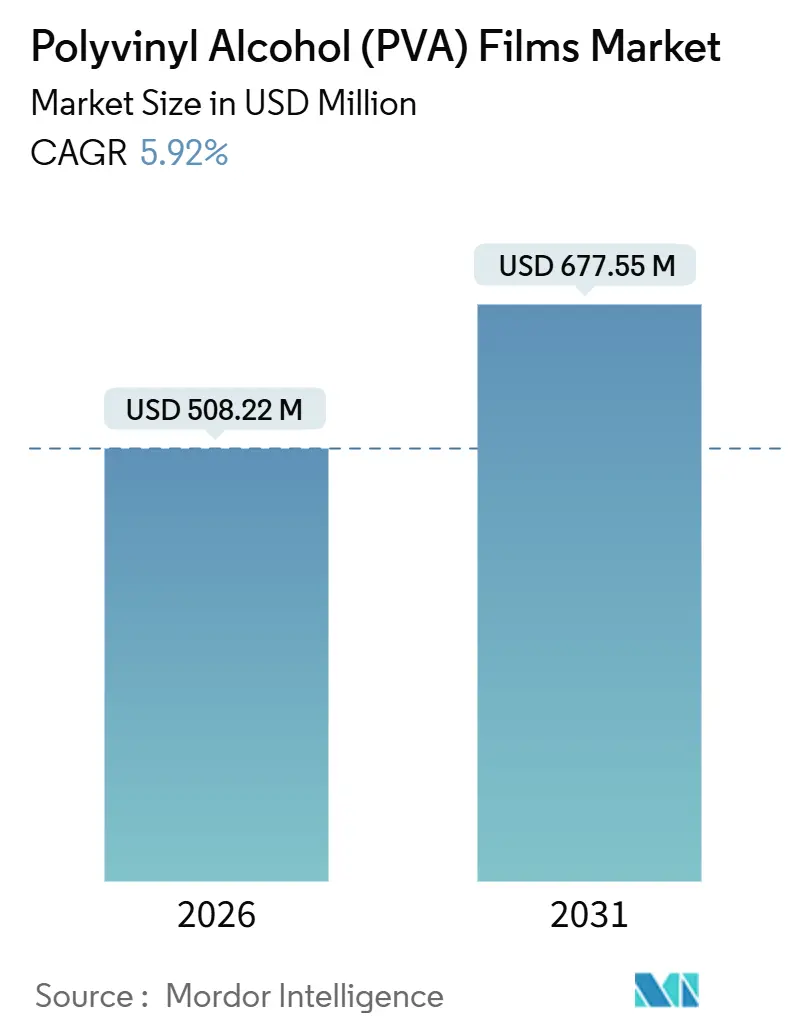

| Market Size (2026) | USD 508.22 Million |

| Market Size (2031) | USD 677.55 Million |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyvinyl Alcohol (PVA) Films Market Analysis by Mordor Intelligence

The Polyvinyl Alcohol Films Market size is estimated at USD 508.22 million in 2026, and is expected to reach USD 677.55 million by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). Growth flows from three converging trends, namely cold-water detergent pods, display-grade polarizer investment, and government-backed substitution of polyethylene mulch with water-soluble agro-packs. North America leads today on the strength of pod adoption and optical film output, yet Asia-Pacific is on a faster 6.88% track as China and India enforce plastic-reduction rules that explicitly credit water-soluble packaging. Competitive strategies revolve around vertical integration into vinyl-acetate-monomer feedstock, bio-based grades that trim Scope 3 emissions, and high-throughput casting lines that shorten order lead times. Producers that balance cost control with functional upgrades are positioned to capture procurement that now embeds dissolvability, carbon intensity, and traceability metrics side by side.

Key Report Takeaways

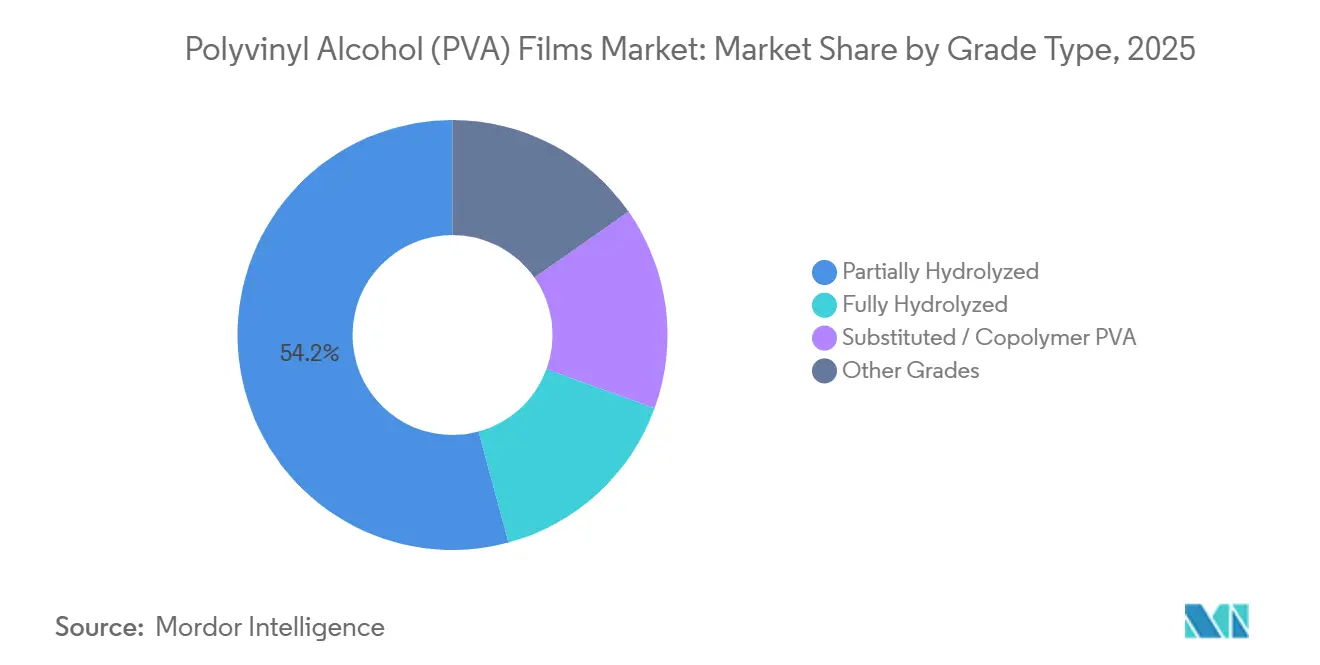

- By grade type, partially hydrolyzed films led with 54.19% revenue share in 2025; substituted/copolymer grades are forecast to expand at a 6.50% CAGR through 2031.

- By application, unit-dose detergent packaging accounted for a 43.65% share of the Polyvinyl Alcohol films market size in 2025, while healthcare films are advancing at a 7.21% CAGR to 2031.

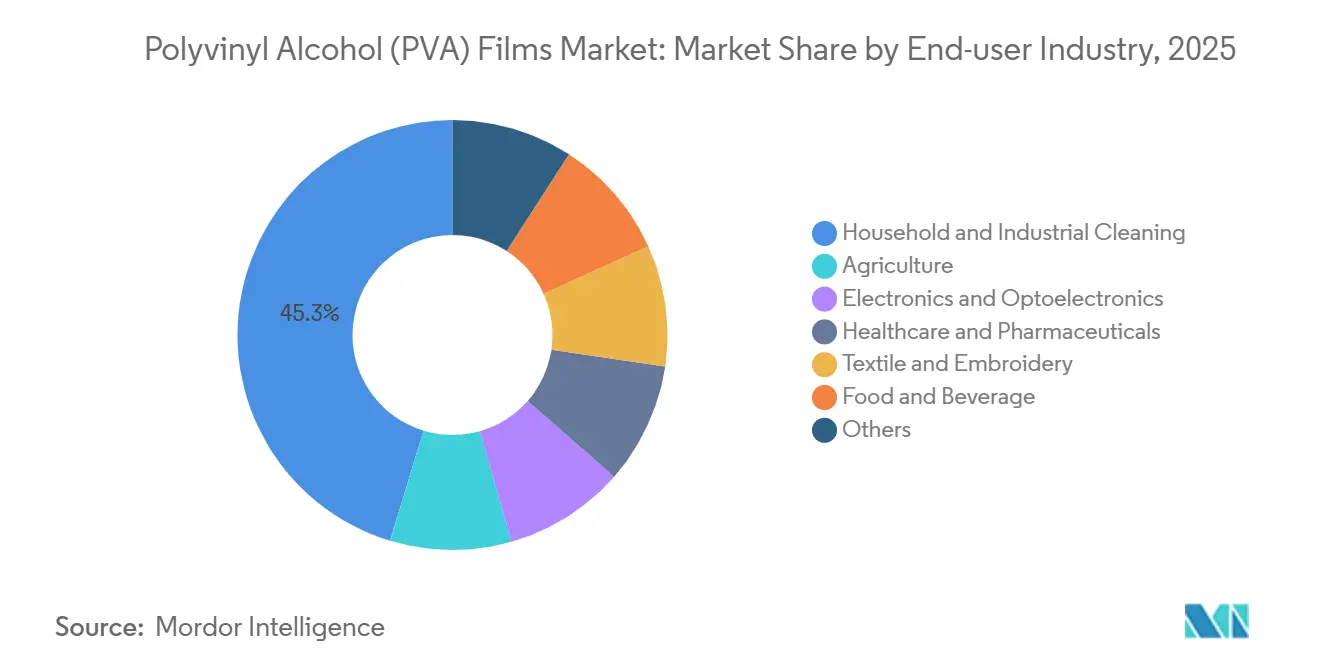

- By end-user industry, household and industrial cleaning commanded 45.29% of the Polyvinyl Alcohol films market share in 2025; healthcare and pharmaceuticals are expected to post the highest projected CAGR at 7.89% through 2031.

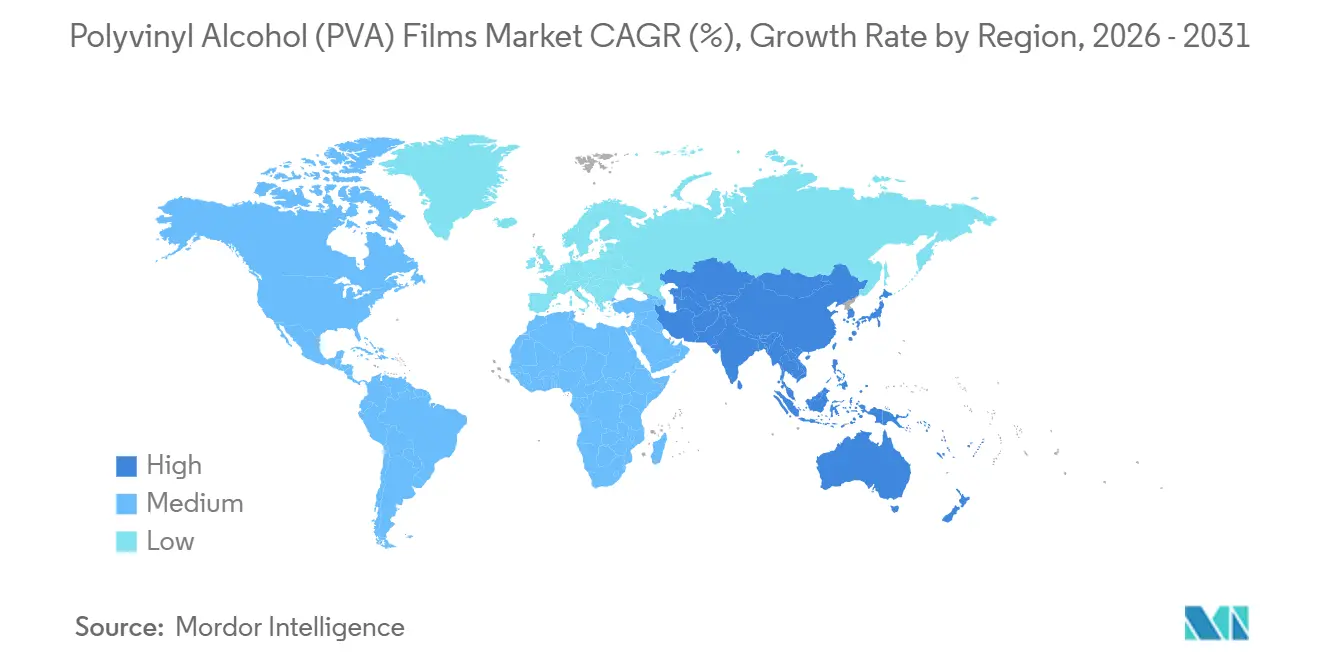

- By geography, North America held 35.87% of revenue in 2025; Asia-Pacific is projected to grow fastest at a 6.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyvinyl Alcohol (PVA) Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cold-water-soluble detergent pods across North America and Europe | +1.2% | North America & Western Europe | Medium term (2-4 years) |

| Asia-Pacific plastic-ban directives accelerating water-soluble agro-packs | +1.5% | APAC core (China, India, Southeast Asia), spill-over to South America | Long term (≥ 4 years) |

| Expanded optical-grade polarizer production for OLED and mini-LED displays | +1.0% | Global, concentrated in East Asia (Japan, South Korea, China) | Medium term (2-4 years) |

| Growing demand for unit-dose detergent packaging in emerging economies | +0.9% | South America (Brazil), South Asia (India), Southeast Asia | Long term (≥ 4 years) |

| Circular textile sizing lines adopting PVA films for temporary yarn coating | +0.4% | Global, early adoption in Europe and East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Cold-Water-Soluble Detergent Pods Across North America and Europe

Pods that dissolve completely below 15°C meet energy-saving wash cycles that represented more than 60% of loads in both regions during 2025. Formulators aligned PVA hydrolysis between 87% and 92% to meet the stricter residue-free benchmarks embedded in EN 13432, prompting a surge in film call-offs from detergent plants that switched pod throughput to over 1,000 units per minute. Market revenue for water-soluble laundry pods climbed to USD 333.7 million in 2025 and is projected to top USD 1.23 billion by 2034. The high-growth pod segment, therefore, underpins the largest absolute volume gain expected in the polyvinyl alcohol films market over the outlook period.

Asia-Pacific Plastic-Ban Directives Accelerating Water-Soluble Agro-Packs

China’s Agricultural Film Management Measures require recovery or certified biodegradation, moving pesticide formulators away from polyethylene sachets toward unit-dose PVA film packs that dissolve in spray tanks. Enforcement intensified after April 2023 when three ministries launched joint inspections during peak planting seasons [1]Chinese State Council, “Notice on Strengthening Agricultural Film Management,” GOV.CN. India’s pesticide-waste rules echo this stance, disallowing reuse of emptied containers for any food contact. Together, these policies explain why Asia-Pacific is the fastest advancing geography in the polyvinyl alcohol films market.

Expanded Optical-Grade Polarizer Production for OLED and Mini-LED Displays

Nitto Denko, LG Chem, and Sumitomo Chemical added new lines through 2025 to meet rising OLED smartphone and automotive demand. Every OLED panel embeds two PVA polarizers that account for around 10-12% of the material bill. The global polarizer sector is forecast to expand from USD 15.2 billion in 2024 to USD 22.8 billion by 2030, anchoring a stable offtake for fully hydrolyzed optical films.

Growing Demand for Unit-Dose Detergent Packaging in Emerging Economies

Urban consumers in India, Brazil, and Southeast Asia adopt pods for dosing accuracy and spill avoidance in compact dwellings. Retail distribution widened when e-commerce platforms listed local multi-packs in 2024. National plastic-waste statutes that reward water-soluble content amplify this pull, reinforcing the growth of the polyvinyl alcohol films market in rapidly industrializing nations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in vinyl-acetate-monomer (VAM) pricing | -0.8% | Global, acute in regions dependent on imported VAM (Latin America, Middle East) | Short term (≤ 2 years) |

| Higher cost and limited heat-resistance versus PE/PET films | -0.6% | Global, most pronounced in tropical climates and high-temperature packaging applications | Medium term (2-4 years) |

| Availability of substitutes such as HPMC and PLA bio-films | -0.5% | North America & Europe (pharmaceutical, food packaging); emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Vinyl-Acetate-Monomer Pricing

Spot VAM rose by USD 100 per ton in 2025 after ethylene and acetic acid rallied, handing integrated producers such as Kuraray and Mitsubishi Chemical a clear margin hedge. Independent converters in Latin America documented 200-300 basis-point margin erosion because imported VAM was rerouted to China’s adhesives sector during the spike. Long-term contracts and direct investment in captive VAM units remain the only credible buffer[2]ICIS, “Global VAM Market Report 2025,” ICIS.COM.

Higher Cost and Limited Heat Resistance Versus PE and PET Films

PVA films carry a 40-80% premium over polyethylene and a 20-60% premium over PET. A glass-transition window of 58-85°C restricts usage in hot-fill or tropical environments where ambient moisture accelerates tensile decay. Ethylene-copolymer grades uplift heat resistance yet partly sacrifice rapid solubility, limiting cross-over into mainstream food pouches. The cost-performance gap, therefore, caps the potential addressable share for the polyvinyl alcohol films market in price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade Type - Partial Hydrolysis Balances Dissolution and Durability

Partially hydrolyzed films supplied 54.19% of the polyvinyl alcohol films market in 2025 and are forecast to remain the dominant revenue stream through 2031 because the 87-92% hydrolysis window delivers quick dissolution and robust tensile strength. These grades dissolve in 30-90 seconds at 20°C, enabling high-speed pod fillers that run beyond 1,000 units per minute. Fully hydrolyzed films, with hydrolysis above 98%, excel as optical polarizers where oxygen barrier values below 0.02 cc m² day align with long back-plane service life, yet they break down too rapidly in cold water for detergent use. Copolymer grades that graft ethylene improve hot-seal strength and moisture resistance, growing at 6.50% to 2031 by serving laundry bags and embroidery backing where delayed dissolution is desired. Specialty low-viscosity and high-viscosity grades cater to textile sizing and adhesive tapes, posting stable but modest expansion.

Polyvinyl alcohol films market share at the grade level illustrates the versatility premium of partial hydrolysis. Polyva upgraded casting speed by 60% when it refined hydrolysis to 90% alongside in-line film tempering, cutting brittleness events by 30% and lifting plant utilization to 85%. Mitsubishi Chemical continues to lift fully hydrolyzed capacity, targeting 154 million m² per year by fiscal 2027 in response to television panel enlargement, thereby securing its foothold despite slower growth relative to pods.

By Application - Healthcare Films Outpace Legacy Detergent Segment

Unit-dose detergent packaging delivered 43.65% of application revenue in 2025, cementing pods as the anchor of the polyvinyl alcohol films market. However, healthcare films chart a 7.21% CAGR owing to regulatory imperatives that prioritize infection control and worker safety. Hospitals deploy water-soluble laundry bags that dissolve at 70°C, eliminating manual handling of biohazard linens. Polarizer layers rank second by value because OLED and mini-LED screens pack two high-purity PVA sheets per panel, and annual OLED output is forecast to reach 1.2 billion displays by 2027. Embroidery and textile sizing hold steady shares, helped by apparel exports from Vietnam, Bangladesh, and Turkey that rely on wash-away backing.

The polyvinyl alcohol films market size for healthcare films is projected to climb from USD 83 million in 2026 to USD 125 million by 2031, illustrating the pivot underway in high-margin regulated niches. Kuraray’s MonoSol brand earned USP Class VI credentials, unlocking oral disinfectant sachets that dissolve directly in the mouth, and already ships multi-layer peelable films to OTC producers in the United States. Food and beverage packers evaluate edible PVA composites blended with gelatin for oxygen-sensitive convenience meals, signaling another diversification avenue.

By End-User Industry - Pharmaceuticals Disrupt Cleaning Dominance

Household and industrial cleaning preserved the largest 45.29% slice of the polyvinyl alcohol films market in 2025 as pods entrenched themselves in North American and European cupboards. Yet healthcare and pharmaceuticals will deliver the fastest 7.89% growth to 2031, powered by hospital infection-control protocols and single-use disinfectant dosing. Agriculture shifts toward water-soluble pesticide sachets as China and India harden film recollection laws. Electronics and optoelectronics, home to polarizers, track a healthy 6.5% rate on OLED and mini-LED adoption. Textile and embroidery consume stable volumes, while food packaging and cosmetic masks form niche but strategic footholds.

Hospitals in the United States referenced FDA guidance issued in 2024 that favors unit-dose disinfectant packaging, translating to double-digit PVA film bookings among laundry service contractors. In China, Anhui Wanwei runs a bio-based PVA project aimed at 20,000 t per annum, specifically targeting agricultural sachets that comply with the national recovery mandate. Japanese and South Korean polarizer champions together supply more than 70% of the OLED market, and investments in thinner high-transmittance PVA films suggest continued material share protection even as LCD panel units plateau.

Geography Analysis

North America commanded 35.87% revenue in 2025 through high pod penetration and polarizer exports to Mexico based display assemblers. Asia-Pacific, however, gathers velocity at a 6.88% CAGR given China’s agro-film recovery laws and India’s widening retail network that sells pods in tier-two cities. Europe advances 5.5% as circular textile sizing plants spring up in Italy, Germany, and Turkey under the European Green Deal. South America grows at 5.2% with Brazil’s detergent shift, and the Middle East & Africa hit 4.8% where agricultural sachets are early in the adoption curve.

China’s pod consumption climbed about 30% in 2023, prompting Anhui Wanwei to fast-track a bio-PVA line that will secure both domestic and export orders. Japan’s Kuraray and Mitsubishi Chemical dominate optical film exports, with the latter adding a 27 million m² annual line at Ogaki by H2 2027. India leverages pesticide-waste rules that forbid container reuse, driving volume-secure demand for water-soluble sachets. South Korea’s Sumitomo Chemical raised polarizer capacity by 25% in 2025 to ride mini-LED momentum. North America sees incremental upside from healthcare films rather than laundry pods, whose penetration already exceeds 40% of households.

Regulatory Landscape

Regulation of PVA films is shaped by food-contact clearances, chemical-substance compliance, and emerging packaging and microplastics rules that scrutinize solubility and degradation behavior. In the United States, FDA food-contact use for polyvinyl alcohol film is governed under 21 CFR 177.1670, and manufacturers also use the Food Contact Notification (FCN) system for specific formulations, with FCNs being company-specific and non-transferable. In the European Union, REACH (Regulation (EC) No 1907/2006) treats polymers such as PVA differently from monomers, shifting compliance attention to upstream registration and supply chain documentation for monomers and additives.

Policy pressure on plastics is also pushing test-method and standards alignment for water-soluble packaging. The EU microplastics restriction under Commission Regulation (EU) 2023/2055 increases the need for documented solubility and wastewater-treatment compatibility, especially for products positioned as water-soluble alternatives to conventional plastics. In China, the QB/T 5786-2022 industry standard sets requirements and test methods for PVA films for packaging, supporting procurement specifications for unit-dose detergents and agrochemicals and improving cross-supplier comparability in domestic supply chains.

Value Chain Analysis

The value chain starts with petrochemical inputs, notably ethylene and acetic acid, which are used to produce vinyl acetate monomer (VAM), followed by polymerization to polyvinyl acetate and saponification (hydrolysis) to polyvinyl alcohol (PVA) resin. Upstream risk concentrates around cost and availability because VAM pricing is energy-linked, and the report context highlights 2025 spot VAM increases that favored integrated producers with captive feedstock positions. Downstream performance in cold-water pod films, high-purity optical polarizers, and delayed-dissolution bags is then driven by resin selection and hydrolysis control across partially hydrolyzed, fully hydrolyzed, and copolymer grades.

Midstream conversion is led by film-making through solution casting, which is common for high-clarity and tight-thickness control, and in some formats through extrusion-based approaches. After casting or extrusion, the process typically includes slitting and winding, then application-specific converting such as printing, lamination, and unit-dose pack forming. Solution casting is capital intensive due to multi-zone drying ovens and tight humidity control, which supports scale advantages for established producers. Downstream channels include direct supply to multinational detergent, healthcare, and display-material customers, plus distributor-led routes for smaller agrochemical and embroidery converters, where logistics must account for moisture protection during storage and transport given PVA films' sensitivity to humidity and temperature.

Competitive Landscape

The Polyvinyl Alcohol Films market is moderately concentrated. Smaller converters serve detergent, agrochemical, and embroidery niches where agility and local compliance trump scale. Chinese challengers Polyva and Anhui Wanwei commercialize plant-derived PVA that replaces up to 45% fossil feedstock, carving a route into European Scope 3 procurement. Technology moves emphasize faster casting, controlled hydrolysis, and multi-functional layering that merges corrosion inhibition or electrostatic discharge protection with water solubility.

Polyvinyl Alcohol (PVA) Films Industry Leaders

Kuraray Co., Ltd.

Mitsubishi Chemical Group Corporation

Aicello Corporation

SEKISUI CHEMICAL CO., LTD.

Ecopol

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace is emerging in compliance-ready, water-soluble packaging formats designed for the tightening EU packaging and microplastics scrutiny, where buyers increasingly ask for documented biodegradation behavior and wastewater-treatment compatibility alongside functional specifications. The EU Packaging and Packaging Waste Regulation entering into force in February 2025, with provisions applicable from 12 August 2026, creates a timing anchor for brands and converters to qualify materials and rework packaging portfolios, which supports demand for films positioned as water-soluble alternatives in unit-dose formats. This is most visible in detergent and agrochemical unit-dose packs, where cold-water dissolution performance and residue control are already embedded in specifications, and where the report context ties demand to plastic-reduction enforcement in China and India.

Investment and certification programs on the supply side also create competitive room for differentiated film offerings. In June 2025, Kuraray announced an expansion of optical-use poval film capacity at its Saijo Plant in Japan, adding 38 million square meters per year and reinforcing pull from OLED and mini-LED polarizer structures that incorporate PVA layers. In China, Ningxia Shuangying New Material Technology announced in March 2026 the start of construction for a 100,000-ton per year PVA capacity project in Ningxia, with trial production planned by November 2026, which signals continued localization and scale-up of PVA raw-material supply for film converters. The opportunity set is therefore shifting toward suppliers that combine reliable resin access and throughput with verifiable sustainability credentials, plus application-tailored performance in high-humidity packaging, healthcare containment, and optical-grade film cleanliness.

Recent Industry Developments

- March 2026: Kuraray announced a global price revision for its PVOH resin products. The revision affects film producers and converters whose costs track resin benchmarks, reinforcing the advantage of procurement strategies that lock in supply or leverage integrated feedstock positions.

- June 2025: Kuraray announced an expansion of optical-use poval film production capacity at its Saijo Plant in Japan, adding 38 million square meters per year with completion targeted for December 2027. This investment supports higher-value optical polarizer demand and increases the availability of high-purity film feedstock for display-material supply chains.

- October 2024: Mitsubishi Chemical Group announced an expansion of OPL Film (optical PVOH film) capacity at its Central Japan, Ogaki (Kanda) Plant in Gifu, adding 27 million square meters per year and lifting total capacity to 154 million square meters annually, with operations scheduled for the second half of FY2027. The project strengthens supply assurance for polarizer-grade PVA films used in OLED and mini-LED panels and raises competitive pressure on optical-grade incumbents.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue earned from selling polyvinyl alcohol (PVA) films that are designed to dissolve in water or provide functional barrier performance in end-use film applications.

Scope exclusions: It excludes upstream PVA resin-only valuation and film structures where PVA is a minor layer rather than the main functional film component.

Segmentation Overview

- By Grade Type

- Fully Hydrolyzed

- Partially Hydrolyzed

- Substituted / Copolymer PVA

- Other Grades

- By Application

- Unit-Dose Packaging

- Detergents

- Agrochemicals

- Disinfectants

- Other Unit Dose Packaging

- Laundry Bags

- Embroidery

- Polarizing Panels

- Other Applications(Medical and Healthcare,Food and Beverage Packaging)

- Unit-Dose Packaging

- By End-user Industry

- Household and Industrial Cleaning

- Agriculture

- Electronics and Optoelectronics

- Healthcare and Pharmaceuticals

- Textile and Embroidery

- Food and Beverage

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the model and to put reasonable limits around demand by application and region. We relied on public sources such as the US International Trade Commission, UN Comtrade, the US Census Bureau, Eurostat, and the Japan Customs portal to understand trade direction, unit trends, and pricing signals for film-related categories.

To avoid guessing on the industry side, we also reviewed annual reports, investor decks, and sustainability reports of film and specialty chemical producers, along with packaging and detergents association websites and peer-reviewed polymer journals that discuss water solubility and film performance needs. Select paid subscriptions were used only for company financials and patent databases, mainly to confirm product focus areas and to time new grade launches. The sources listed here are illustrative, and many other public and paid references were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets counted as PVA film revenue and how volumes move across unit-dose packaging, laundry bags, and specialty optical uses. We spoke with a mix of film producers, compounders, converters, and downstream buyers across APAC, EMEA, and the Americas, then used these inputs to tighten average selling price assumptions, grade splits (fully vs partially hydrolyzed), and realistic adoption rates by end-user industry.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 40% |

| Mid tier: 47% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 14% | Managers: 50% | Americas: 24% |

Market-Sizing & Forecasting

The main build used a top-down and bottom-up approach. Production and trade signals were used first to reconstruct a realistic addressable demand pool for PVA films by region and application, and then the totals were tested through selective supplier and channel checks. In practice, we started from visible demand anchors such as unit-dose detergent and cleaning packs, then added other film uses after confirming what share of those applications is actually served by PVA films.

A few practical inputs were treated as key levers in the model, including adoption rates of water-soluble pods in household and industrial cleaning, mix shifts between fully and partially hydrolyzed grades, regional price differences tied to resin costs, and the penetration of healthcare film uses where growth can be faster. We also tracked polarizer-related demand behavior, but kept it tightly defined to avoid mixing it with non-film PVA uses. Where bottom-up detail was not available for smaller geographies, we used proxy splits based on trade patterns and converter feedback, and then sanity checked results against capacity additions and reported utilization comments.

For forecasting, scenario analysis was used, with a base case reflecting what most interviewees expect for new unit-dose formats and for substitution into dissolvable packaging. Key assumptions such as price progression, application mix, and regional growth were refreshed so the forecast stays realistic when raw material costs and regulatory pressure change.

Data Validation & Update Cycle

Before sign-off, model outputs were checked against independent signals, including import and export movements, reported expansion projects, and the relative share of cleaning and healthcare demand implied by downstream indicators. When an outlier showed up, we traced the driver back to one assumption at a time, and we re-contacted sources if the variance could not be explained with public data.

A second analyst review was done to confirm definitions, conversions, and that no double counting was introduced when moving from applications to regions. Reports are refreshed annually, and interim adjustments are made when a material event occurs, such as a major capacity start-up, a policy change affecting packaging, or a sharp input-cost shift. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Polyvinyl Alcohol Pva Films Market Sizing Compared With Other Published Estimates

Published market sizes for PVA films can vary even when they use similar growth rates. One reason is that the boundary of what counts as a PVA film sale is handled differently across reports. Differences also come from base-year choice, regional coverage, and how prices are converted and carried forward.

In this study, the biggest gap drivers are whether estimates include upstream PVA resin value, whether they count film structures where PVA is only a thin layer, and how they treat optical uses versus water-soluble packaging demand. By tracking grade mix and application-led volume drivers, and then refreshing price assumptions with annual checks, Mordor Intelligence keeps the total tied to film revenue actually sold into defined end uses, instead of expanding the number through adjacent polymer or resin scopes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.51 B (2026) | |

| Industry Publisher A | USD 0.41 B (2025) | Uses an earlier base year and a longer horizon, and its segment map can pull in broader end uses and grade buckets, which can shift the counted revenue pool for films. |

| Industry Publisher B | USD 0.45 B (2024) | Anchors the model to a different base year and may apply a wider packaging definition and price series, which can move the market value even if volumes are similar. |

The spread across sources is mainly explained by scope edges and by how price and mix are handled at the starting year. When definitions stay tight to film revenue and the same demand anchors are checked each year, the resulting market size becomes easier to trace, update, and reuse in planning.

Key Questions Answered in the Report

What is the current value of the polyvinyl alcohol films market?

The global market stands at USD 508.22 million in 2026 and is forecast to reach USD 677.55 million by 2031.

Which region will grow fastest through 2031?

Asia-Pacific leads with a 6.88% CAGR, supported by strict plastic reduction mandates in China and India.

Why are partially hydrolyzed grades dominant?

Their 87-92% hydrolysis brings quick dissolution and robust tensile strength, fitting detergent pods and agro-packs.

How are hospitals using polyvinyl alcohol films?

Healthcare facilities deploy water-soluble laundry bags and single-dose disinfectant sachets that dissolve on contact, cutting infection-transfer risk.

What limits broader adoption of PVA films?

Higher price versus PE and PET and a glass-transition temperature below 85°C restrict usage in hot-fill or tropical packaging.

Page last updated on: