Cling Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

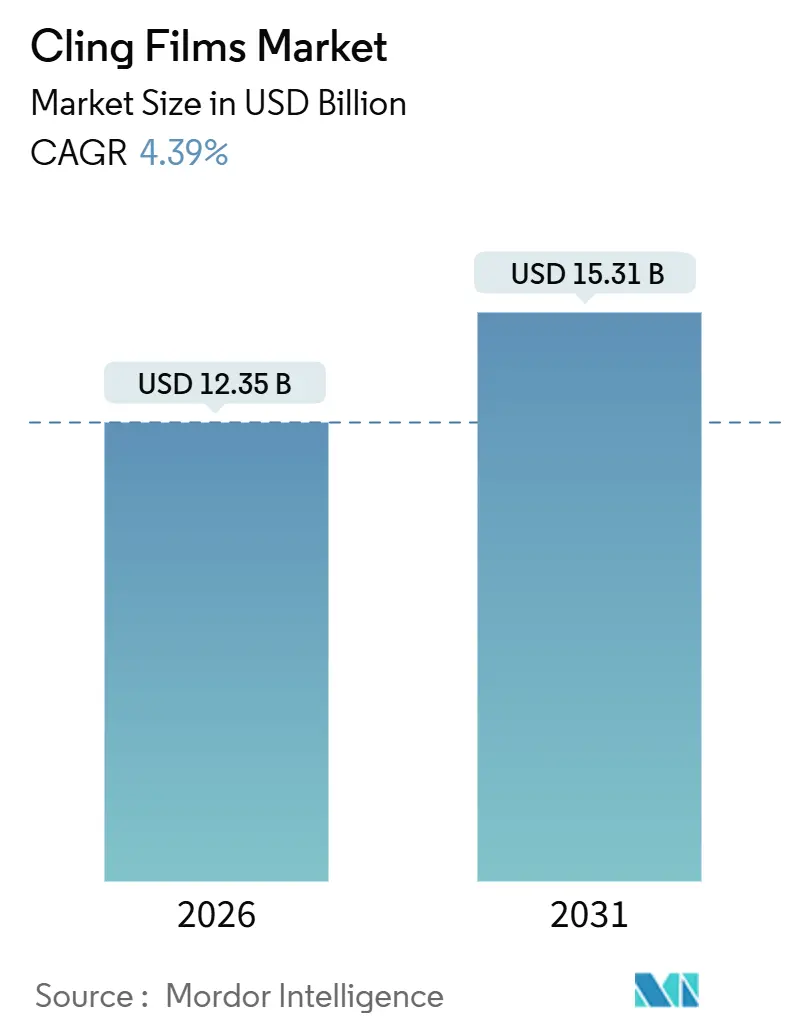

| Market Size (2026) | USD 12.35 Billion |

| Market Size (2031) | USD 15.31 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

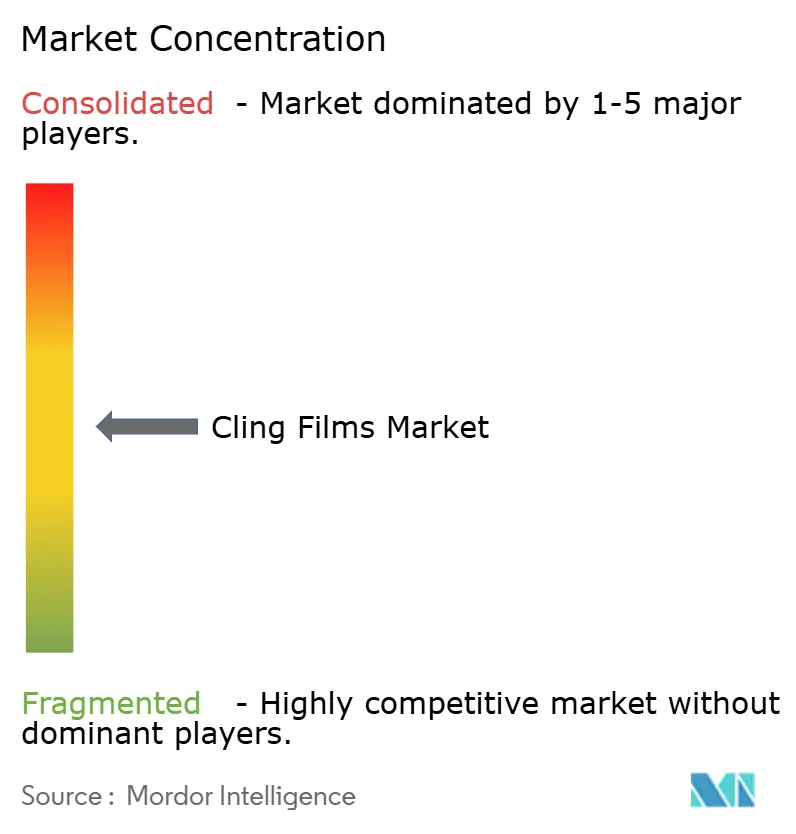

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cling Films Market Analysis by Mordor Intelligence

The Cling Films Market size is estimated at USD 12.35 billion in 2026, and is expected to reach USD 15.31 billion by 2031, at a CAGR of 4.39% during the forecast period (2026-2031). Strong demand from e-commerce grocery channels, healthcare sterile-packaging mandates, and regulatory pressure on single-use plastics are converging to keep volume growth steady despite price volatility. Polyethylene grades, especially bio-based PE, are winning share because they comply with Extended Producer Responsibility rules in Europe and several North American states, while cast-film technology is capturing most new capacity as automation spreads across food retail and fulfillment centers. Food processors remain the dominant buyers, yet hospital procurement teams are raising specifications that only high-clarity, corona-treated films can meet, signaling a sustainable premium segment. Competitive dynamics show moderate concentration; the top five suppliers control around 40% of installed output, but regional converters still find space in high-barrier and ultra-thin niches.

Key Report Takeaways

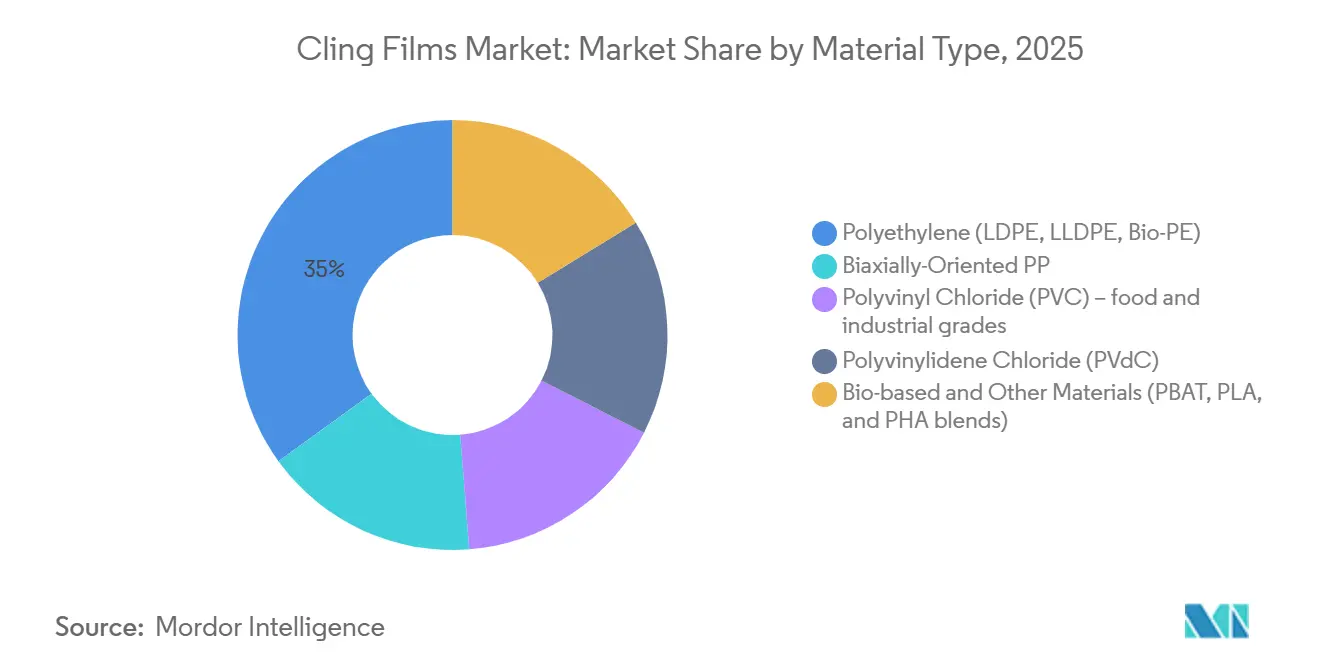

- By material type, polyethylene held 34.98% of 2025 revenue and is forecast to post a 5.08% CAGR through 2031.

- By form, cast films accounted for 75.67% of the 2025 volume and are on track for a 4.49% CAGR to 2031.

- By end-user industry, food applications captured 44.98% of 2025 demand and lead with a 4.78% outlook to 2031.

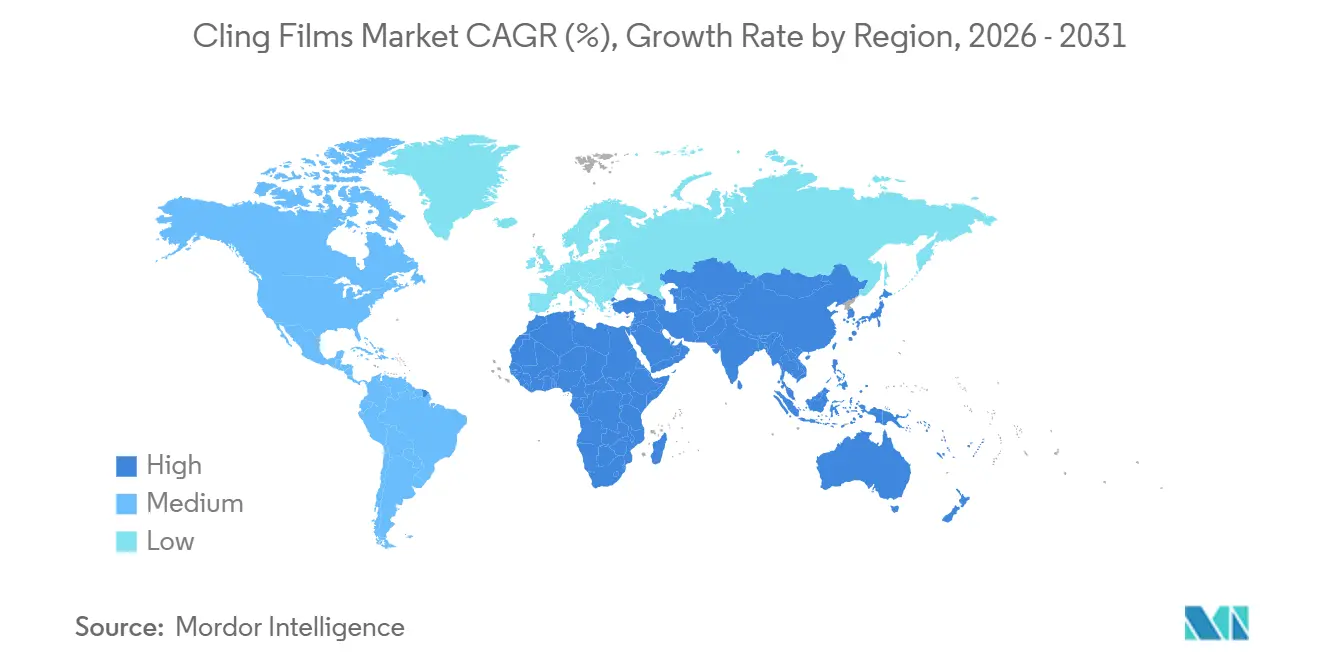

- By geography, Europe led with 34.36% of 2025 revenue, while Asia-Pacific is the fastest-growing region at 4.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cling Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing food industry and packaged-food penetration | +1.2% | Global, with concentration in Asia-Pacific urban centers and North American meal-kit hubs | Medium term (2-4 years) |

| Expanding healthcare packaging demand | +0.8% | North America and Europe, spillover to Middle East private hospital networks | Long term (≥ 4 years) |

| Rapid supermarket roll-out in emerging economies | +1.0% | Asia-Pacific core (China, India, ASEAN), early gains in Middle East and Africa | Short term (≤ 2 years) |

| Integration of antimicrobial and barrier nanocoatings | +0.7% | Global, led by North America and European premium segments | Medium term (2-4 years) |

| Surge in online grocery and meal-kit delivery | +0.9% | North America, Western Europe, urban Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Food Industry and Packaged-Food Penetration

China’s supermarket density rose from 1.2 stores per 10,000 residents in 2020 to an estimated 2.1 in 2025, lifting demand for transparent oxygen-barrier wraps that protect produce during multi-day cold-chain transit. Leading meat processors trimmed LLDPE gauges from 12 µm to 9 µm after inline tension control, cut wrinkling, and saved 18-22% resin per pack. North American bakery chains are shifting from wax paper to micro-perforated films that vent 300-500 g/m²/day of moisture vapor, curbing mold in artisan bread displays. Meal-kit providers favor phthalate-free LDPE films certified under FDA 21 CFR 177.1520 to secure seven-day refrigerated shelf life.[1]U.S. Food and Drug Administration, “21 CFR 177.1520: Olefin Polymers,” fda.gov Together, these trends reposition cling wrap from a commodity to a branding tool, especially for premium organic labels where clarity signals freshness.

Expanding Healthcare Packaging Demand

Updated Association for the Advancement of Medical Instrumentation guidance sets peel-strength windows between 200 and 400 g-force per 25 mm, a range consistently met only by cast films treated to 42-46 dynes/cm.[2]Association for the Advancement of Medical Instrumentation, “TIR 109 Guidance on Peel Strength,” aami.org Device makers are switching from paper-plastic pouches to all-plastic wraps to minimize fiber particulate in cleanrooms. PVdC-coated cling films cut oxygen ingress to below 1 cm³/m²/day, extending the shelf life of moisture-sensitive APIs by up to 40% in cold-chain transit. The European Medicines Agency’s 2025 tamper-evidence rule for parenteral drugs is accelerating demand for heat-sealable wraps with holographic features. Aging populations and rising surgical volumes in Gulf states strengthen long-term volume visibility for ISO 15378-qualified producers.

Rapid Supermarket Roll-Out in Emerging Economies

India commissioned roughly 1,200 new supermarkets and hypermarkets in 2025, a 14% year-on-year leap that forces produce suppliers to adopt cling-wrapped trays meeting standardized display requirements. Vietnam’s organized retail share climbed to 35% in 2025, up from 28% two years earlier, prompting Southeast Asian converters to import European cast-film lines sized for 300 mm rolls compatible with automatic wrapping stations. Saudi Arabia’s Vision 2030 cold-chain hubs need films that keep seals intact at ambient temperatures above 45°C. As wet markets cede ground to air-conditioned stores, demand pivots to anti-fog films that preserve visibility on chilled shelves, creating a technological hurdle for smaller domestic producers.

Integration of Antimicrobial and Barrier Nanocoatings

Silver-ion films extend microbial thresholds in fresh meat by three to five days under USDA standards, curbing spoilage below 10⁵ CFU/g. Zinc-oxide wraps applied to dairy products achieve a 99.7% Listeria reduction after 72 h at refrigeration temperatures. Nanoclay-dispersion structures push oxygen transmission below 5 cm³/m²/day, allowing salad processors to eliminate nitrogen flushing and cut packaging costs by around 13%. EFSA cleared titanium-dioxide nanoparticles for food-contact use in 2024, yet some member states keep interim bans pending migration data, tilting the advantage toward multinational converters with robust regulatory teams. Players that scale nanocoatings at >300 m/min line speed stand to capture premium slots in high-margin fresh-food supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low resistance to extreme temperatures | -0.5% | Global, acute in frozen-food and industrial cold-chain applications | Medium term (2-4 years) |

| Tightening global single-use-plastic regulation | -0.9% | Europe and North America core, spillover to Asia-Pacific coastal cities | Long term (≥ 4 years) |

| Consumer shift to reusable silicone and beeswax wraps | -0.3% | North America and Western Europe premium organic segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Resistance to Extreme Temperatures

Standard LDPE and LLDPE films turn brittle below –18°C, causing seal failure rates above 8% on frozen-seafood pallets compared with under 2% for stretch hoods. High-temperature use is limited because films soften above 60°C, excluding hot-fill soups and sauces that make up a USD 8 billion flexible-packaging niche. Metallocene-PE grades stay tough to –30°C but cost 25-35% more than commodity LDPE, restricting uptake to pharmaceutical cargoes. Flex-modifying additives such as polyisobutylene can migrate to food-contact surfaces, complicating FDA and EFSA extraction tests, so converters face trade-offs between performance and compliance.

Tightening Global Single-Use-Plastic Regulation and Consumer Shift to Reusables

The EU Single-Use Plastics Directive requires 30% recycled content in food-contact films by 2030. France and Germany now impose fees of EUR 0.08-0.12 per kg on non-recyclable films, lifting PVdC costs by 20% and accelerating the pivot to mono-material PE. California’s SB 54 mandates 65% recyclability or compostability in single-use plastic packaging by 2032, pushing producers toward PBAT or PLA blends. A Deloitte survey showed 42% of the United States households tried silicone wraps in 2025, up from 28% in 2023, underscoring perception risks even though these reusables still hold below 2% share in food-wrap volume. The result is a bifurcated landscape where commodity petro-PE endures a margin squeeze while compostable grades command price premiums but require heavy capital upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bio-PE Fuels Polyethylene Leadership

Polyethylene accounted for 34.98% of 2025 revenue and is expected to expand at a 5.08% CAGR, adding significant weight to the cling films market size through 2031. Bio-PE derived from sugarcane ethanol slots directly into existing extrusion lines, avoids phthalates, and satisfies European recycled-content mandates, making it the fastest-adopted resin among large food brands. LDPE remains favored for hand-wrap because its inherent cling eliminates supplemental tackifiers, while LLDPE’s 40-50 MPa tensile strength cuts breaks on high-speed flow-wrap equipment. PVC is shrinking in Europe owing to dioxin and phthalate concerns, but PVdC-coated film still owns a thin yet defensible niche in vacuum-packed meat exports that need oxygen transmission under 2 cm³/m²/day.

Compostable polymers continue to widen choice yet remain a small slice of the cling film market. PBAT-PLA blends certified under EN 13432 are gaining listings with municipal organics programs, while PHA grades tout marine biodegradability but sell at a 3-4× premium to fossil PE. BOPP addresses twist-wrap candy niches where stiffness matters over cling. Overall, material selection is sorting into three tiers: commodity PE for cost-sensitive packs, bio-PE for mainstream sustainability programs, and fully compostable blends for jurisdictions that subsidize separate collection, a hierarchy that should keep polyethylene dominant in cling films industry revenues for most of the decade.

By Form: Cast Films Strengthen Automation Advantage

Cast films claimed 75.67% of 2025 volume and are forecast at a 4.49% CAGR, adding incremental tonnage that will reinforce their 2031 cling films market share lead. Gauge uniformity within ±3% is essential for robotic pick-and-place systems populating grocery fulfillment hubs, and chill-roll quenching yields haze below 5%, critical for premium meat displays. Inline corona treatment integrates label-ready surfaces at full line speed, avoiding offline passes that inflate cost for blown-film competitors.

Blown films still serve hand-wrap food-service outlets that value puncture resistance and higher natural cling, yet their share is stable rather than growing. Multilayer blown towers outfitted with real-time thickness gauging cost upward of USD 5 million each, so many regional converters delay upgrades, eroding their relative quality proposition. Automation’s rise across meal-kit assembly and supermarket deli counters thus cements cast extrusion as the workhorse technology anchoring the future cling films market.

By End-User Industry: Food Holds the Largest Share

Food uses absorbed 44.98% of the 2025 demand and are pacing a 4.78% trajectory, bolstering the cling films market size in absolute terms. Fresh-produce packers choose ultra-clear wraps that limit moisture loss and exhibit anti-fog properties for chilled displays. Meat processors deploy 8-µm films embedded with oxygen scavengers to gain 4-6 days extra shelf life, directly lowering shrink. Dairy makers favor micro-perforated wraps that vent carbon dioxide from ripening cheese without admitting oxygen, keeping mold counts low.

Healthcare packaging shows the steepest percentage growth, albeit off a smaller base, as hospitals enforce ISO 11607 sterile-barrier requirements. Pharmaceutical blisters are gradually migrating from foil to transparent PVdC-coated films that still block moisture yet aid tablet identification. Industrial unitization and consumer goods are mature but vulnerable to substitution from stretch hoods and shrink sleeves. Overall, fresh food and healthcare will dictate material development, with oxygen barrier, seal integrity, and migration-free additives topping converter R&D agendas in the cling films industry.

Geography Analysis

Europe led with 34.36% revenue in 2025, underpinned by decades-old flexible-packaging infrastructure, strict Framework Regulation (EC) No 1935/2004, and consumer penchant for pre-packed produce. Germany and the United Kingdom post the highest per-capita consumption, yet volume headwinds are arising as retailers experiment with reusable silicone wraps in deli counters. France’s 2024 EPR fees of EUR 0.10 per kg on non-recyclable films have accelerated bio-based adoption, while Italy’s focus on antimicrobial coatings for export mozzarella and prosciutto offers a differentiated edge. Nordic pilots of flexible-film deposit schemes signal future circular-economy shifts, though current recycling streams still sideline flexible PE.

Asia-Pacific is the fastest-growing region, clocking a 4.73% CAGR that will gradually close the gap with Europe in the overall cling films market size. China doubled supermarket density between 2020 and 2025, a shift requiring barrier wraps capable of surviving multi-day domestic cold chains. India’s addition of 1,200 supermarkets in 2025 spurs uptake of cling-wrapped trays and drives new cast-line installs. Japan refines technology leadership with 6-µm metallocene-PE films, and South Korea’s 20% recycled-content rule for 2027 compels investment in advanced sorting capacity. ASEAN markets, buoyed by Japanese and Korean convenience-store investments, import European machinery to standardize roll widths for automated deli stations.

In North America, the United States’ growth is tied to online grocery and meal-kit firms that demand portion-controlled, automation-ready wraps. Canada’s patchwork provincial EPR rules complicate nationwide launches, yet bilingual packs remain a stable niche. Mexico attracts near-shoring cast-film projects valued at more than USD 50 million over 2024-2025, securing supply into US produce corridors. Brazil heads South America, but cold-chain gaps outside major metros cap upside, while Saudi Arabia’s heat-resistant film requirements and South Africa’s split between organized and informal retail shape early-stage opportunities across the Middle East and Africa. Collectively, regional dynamics keep the cling films market in a multi-polar growth mode, with Asia-Pacific delivering volume, Europe pushing regulation, and North America innovating technology.

Competitive Landscape

The Cling Films market is moderately concentrated. Amcor’s 2024 bio-PE joint venture with Braskem is locked in 50,000 t/y resin supply, enabling renewable-content claims that resonate with supermarket house brands. Sealed Air and Reynolds have installed machine-vision gauge-inspection systems that cut scrap below 2%, safeguarding margins on large e-commerce contracts. Mondi’s work with BASF on PBAT-PLA blends illustrates how compostable films are migrating from pilot to commercial scale pending EN 13432 certification. Backward integration into bio-resins and strategic alliances with nanotechnology firms dominate the forward strategy. Several majors explore vertical moves into recycling, eyeing food-grade rPE to meet 2030 recycled-content mandates.

Cling Films Industry Leaders

Amcor plc

Sigma Plastics Group

Jindal Poly Films Limited

Reynolds Consumer Products

NAN YA PLASTICS CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023: Berry Global Group Inc. launched a next-generation version of its proven stretch hood film with a minimum of 30% recycled plastic content. This will help the company to support businesses in achieving sustainability objectives as well as meeting the requirements of current and forthcoming United Kingdom and European plastics packaging legislation.

- January 2023: Amcor plc announced the introduction of its new PrimeSeal and DairySeal Recycle-Ready Thermoforming Films for meat and dairy, which provide outstanding packaging performance and enhanced packaging circularity. The novel packaging is heat resistant up to 90 °C and is made with low Ethylene-Vinyl Alcohol Copolymer (EVOH) content without reducing the shelf-life of perishable items. It is appropriate for fresh and processed meat and fish, as well as hard cheese.

Global Cling Films Market Report Scope

Cling film (plastic wrap, food wrap, or saran wrap) is a thin, transparent plastic film that adheres to surfaces and to itself and is used for packaging food items. They protect food from insects and microbial contamination, keep it fresh, and minimize the risk of food wastage by increasing its shelf life. Besides food applications, it is used for packaging in healthcare, consumer goods, industrial, and other applications.

The cling films market is segmented by material type (Polyethylene, Biaxially Oriented Polypropylene, Polyvinyl Chloride (PVC), Polyvinylidene Chloride (PVDC), and Other Material Types), form (Cast Cling Film and Blow Cling Film), end-user industry (Food, Healthcare, Consumer Goods, Industrial, and Other End-user Industries), and geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers market size and forecasts in terms of revenue (USD) for all the above segments.

| Polyethylene (LDPE, LLDPE, Bio-PE) |

| Biaxially-Oriented PP |

| Polyvinyl Chloride (PVC) – food & industrial grades |

| Polyvinylidene Chloride (PVdC) |

| Bio-based & Other Materials (PBAT, PLA, PHA blends) |

| Cast Cling Film |

| Blown Cling Film |

| Food |

| Healthcare |

| Consumer Goods |

| Industrial |

| Other End-user Industries |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| Material Type | Polyethylene (LDPE, LLDPE, Bio-PE) | |

| Biaxially-Oriented PP | ||

| Polyvinyl Chloride (PVC) – food & industrial grades | ||

| Polyvinylidene Chloride (PVdC) | ||

| Bio-based & Other Materials (PBAT, PLA, PHA blends) | ||

| Form | Cast Cling Film | |

| Blown Cling Film | ||

| End-user Industry | Food | |

| Healthcare | ||

| Consumer Goods | ||

| Industrial | ||

| Other End-user Industries | ||

| Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global cling films market size?

What is the current global cling films market size?

How fast is the cling films market expected to grow?

How fast is the cling films market expected to grow?

Which material leads sales within cling wrap?

Which material leads sales within cling wrap?

Which end-use segment drives most demand?

Which end-use segment drives most demand?

Page last updated on: