Polyvinyl Butyral (PVB) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 5.69 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

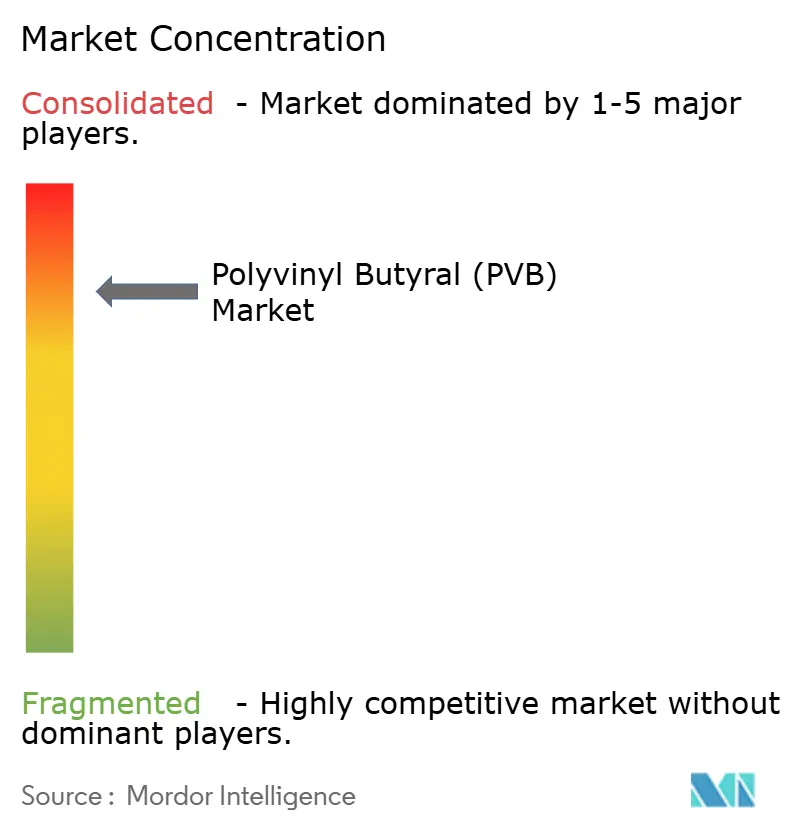

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyvinyl Butyral (PVB) Market Analysis by Mordor Intelligence

The Polyvinyl Butyral Market size was valued at USD 4.06 billion in 2025 and estimated to grow from USD 4.29 billion in 2026 to reach USD 5.69 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). Tailwinds include the material’s near-universal acceptance for laminated safety glass, rising electric-vehicle (EV) penetration that prioritizes cabin acoustics, and accelerating solar-photovoltaic investments that seek long-life encapsulants. Adhesive films dominate demand because regulatory bodies—from U.S. highway authorities to Asia-Pacific building inspectors, require proven interlayer performance. Meanwhile, producers are scaling European and Asian capacity, signaling confidence that the polyvinyl butyral market will absorb additional output without eroding margins. Barriers to entry remain formidable thanks to intensive capital requirements, established automotive qualification cycles, and long-standing customer relationships favoring incumbent suppliers.

Key Report Takeaways

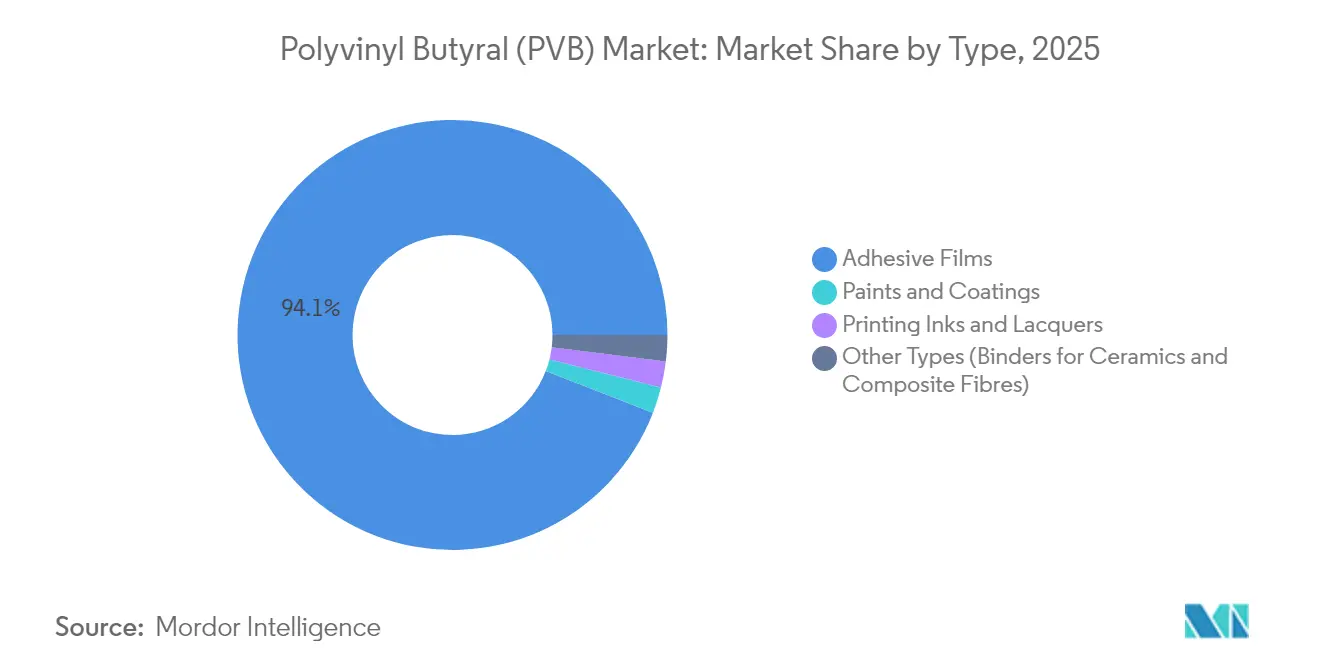

- By type, adhesive films captured 94.12% of polyvinyl butyral market share in 2025, while the segment is projected to expand at a 6.05% CAGR through 2031.

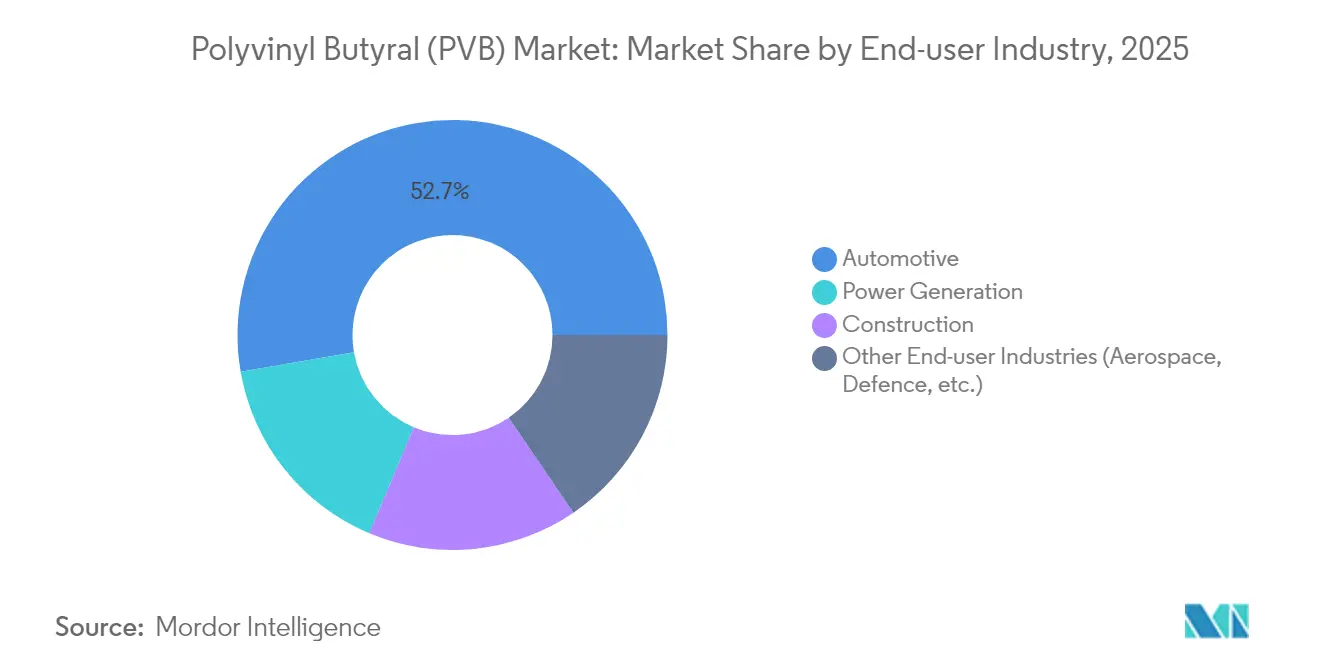

- By end-user industry, automotive glazing accounted for 52.74% share of the polyvinyl butyral market size in 2025; power generation applications are advancing at an 7.95% CAGR through 2031.

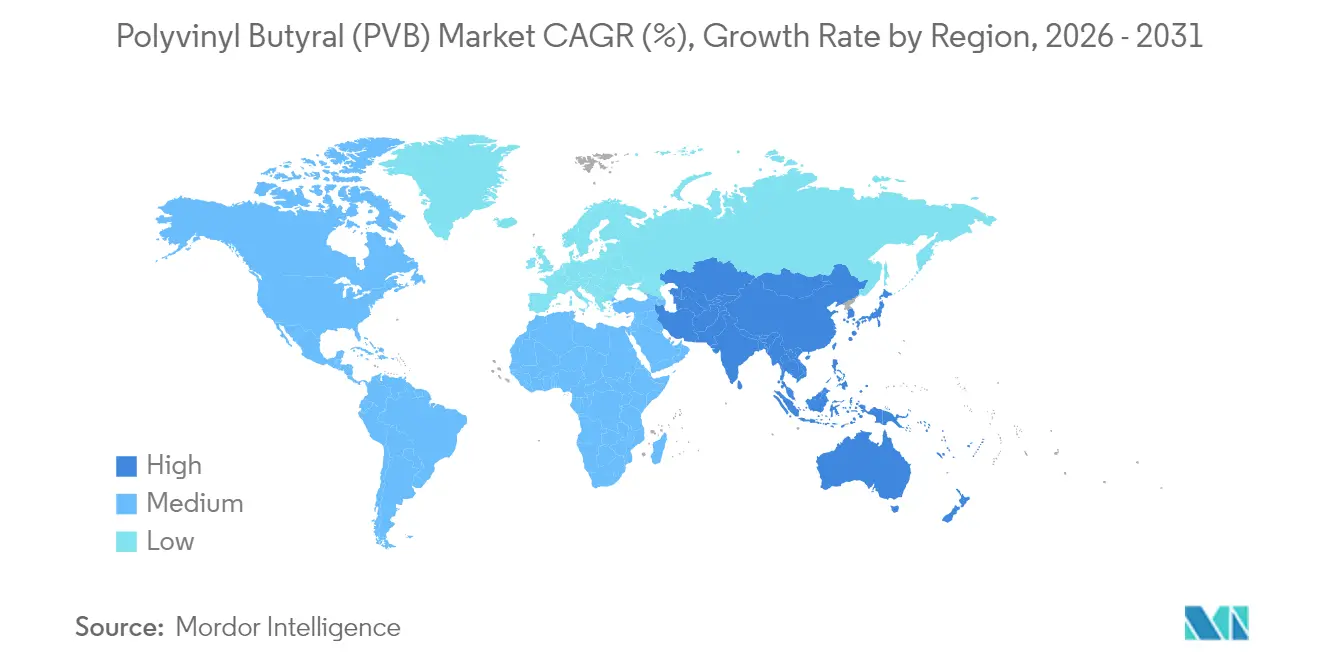

- By geography, Asia-Pacific led with 50.83% share of the polyvinyl butyral market in 2025 and is forecast to maintain the fastest regional CAGR at 6.11% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyvinyl Butyral (PVB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction and Infrastructure Boom | +1.5% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Laminated-Glass Penetration in Automotive | +1.2% | Global, led by Asia-Pacific automotive hubs | Short term (≤ 2 years) |

| Mandatory Safety Glazing Regulations | +0.8% | North America and EU, expanding to emerging markets | Long term (≥ 4 years) |

| Solar-PV Build-Out using PVB Encapsulants | +0.6% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| EV-Driven Demand for Acoustic Interlayers | +0.4% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction and Infrastructure Boom

Glazing, curtain walls, and point-supported facades are increasingly specified across several U.S. states and in Hong Kong. The Pennsylvania Building Code 2018 stipulates the use of laminated glass in high-occupancy zones, locking in baseline demand [1]Pennsylvania Department of Labor and Industry, “Uniform Construction Code,” dli.pa.gov. Parallel mandates in Hong Kong’s Code of Practice for the Structural Use of Glass are raising PVB penetration in dense Asian cities. As urban skylines densify and architects favor larger glazed surfaces, these rules translate into multi-year, non-deferrable orders that buttress the polyvinyl butyral market. Developers also value PVB’s acoustic benefits in transit-oriented projects, where interlayers can cut external noise by 3-7 dB without adding weight. Collectively, these factors underpin a sustained construction-led tailwind through the decade.

Laminated-Glass Penetration in Automotive

Automotive original-equipment manufacturers (OEMs) extend laminated glass beyond windshields to include side, roof, and rear lights, enhancing occupant safety and reducing cabin noise. Eastman’s Saflex Horizon interlayer targets head-up-display clarity while meeting dynamic impact tests. Electric vehicles amplify this need because drivetrain silence accentuates wind and road noise; acoustic PVB grades deliver up to 6 dB attenuation, improving perceived quality. OEM adoption timelines are short, the average model refresh cycle is three to four years, supporting near-term volume growth. The addition of glass area in panoramic roof designs further increases square-meter demand per vehicle, raising unit consumption even if global auto output grows modestly.

Mandatory Safety Glazing Regulations

Regulators worldwide reference U.S. Federal Motor Vehicle Safety Standard No. 205 and the ANSI/SAE Z26.1-1996 tests, effectively hard-coding PVB into passenger-car windshields. European lawmakers are extending recycling targets under the revised End-of-Life Vehicles Directive, favoring laminated assemblies because PVB facilitates higher recovery rates. OEMs face lengthy validation cycles to switch interlayer chemistries, so rule tightening cements incumbent PVB volumes. Similar trajectories are emerging in Brazil and India, where draft automotive-glass regulations are mirroring North American specifications, thereby broadening the regulatory safety net for the polyvinyl butyral market.

Solar-PV Build-Out using PVB Encapsulants

Thin-film module makers increasingly replace ethylene-vinyl acetate (EVA) with PVB encapsulants that provide superior UV resistance and glass adhesion. National Renewable Energy Laboratory testing shows PVB retains >95% transmittance after 2,000 hours of damp-heat exposure, outperforming EVA by more than 10 percentage points. DuPont’s PV5200 series leverages these properties, and the company anticipates more than 25% annual sales growth for its PVB sheets, as global solar installations are expected to surpass 400 GW by 2025. New float-glass lines dedicated to photovoltaic glass in the United States and Europe create synchronized upstream pull for encapsulants, diversifying revenue streams for PVB producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product Substitutes (EVA, SGP, Ionoplast) | -0.7% | Global, higher impact in cost-sensitive markets | Medium term (2-4 years) |

| Intensifying PVB Recycling | -0.5% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Volatile Butyraldehyde Feedstock Supply | -0.3% | Global, concentrated in Asia-Pacific production hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Product Substitutes (EVA, SGP, Ionoplast)

Cost-sensitive construction and automotive tiers increasingly weigh EVA and ionoplast interlayers against PVB. Research published in Materials shows EVA meeting the requisite impact performance while simplifying storage logistics due to lower moisture pick-up. Kuraray’s SentryGlas ionoplast, which is five times stronger than conventional PVB, is displacing PVB in structural facades despite its premium pricing. Although substitution remains marginal in regulated windshield applications, price-pressured segments could erode PVB volumes, particularly in emerging markets prioritizing upfront cost over long-term durability.

Intensifying PVB Recycling in Developed Regions

Tarkett’s French facility recycles 20,000 tons of post-consumer PVB annually, blending 24–33% recycled content into premium flooring. Mature markets are promoting circular-economy credentials, spurring architects and automakers to specify recycled polymers where optical clarity is non-critical. Ultrasound-aided separation technologies demonstrated by academic consortia preserve molecular weight, enabling recyclate use in coatings and sealants. The rising supply of recycled PVB may dampen the growth of virgin-resin demand, especially in Europe, where legislators are seeking to mandate quotas for secondary raw materials in building products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Adhesive Films Dominate Through Safety Applications

Adhesive films accounted for 94.12% of polyvinyl butyral market share in 2025, reflecting their central role in laminated-glass safety systems across automotive and architectural sectors. The adhesive-film polyvinyl butyral market size is projected to reach USD 5.43 billion by 2031, advancing at a 6.05% CAGR alongside global construction upcycles. Strict windshield standards, city-center noise ordinances, and growth in panoramic roofs collectively lock adhesive films into multi-year OEM programs. Producers differentiate through specialty grades, structural, UV-blocking, and bird-friendly variants, withhich command premiums of 8-12 % over commodity resin.

Innovation centers on resin rheology, enabling thinner interlayers without sacrificing impact performance, thereby reducing vehicle weight and glazing costs. Eastman’s Saflex Structural series raises laminate strength by 30%, enabling frameless balustrades and reducing metal hardware in facades. Optical-grade PVB films for heads-up displays are an emerging niche, with Kuraray expanding Japanese capacity to serve LCD and augmented-reality windshields. Such specialization supports a resilient revenue outlook for adhesive films even as volumes mature.

Paints, coatings, printing inks, and niche applications collectively held 5.88% share in 2025, valued at USD 0.24 billion. While small, these segments provide margin buffers; PVB’s hydroxyl functionality delivers excellent pigment dispersion and adhesion to metal substrates, commanding higher price points per kilogram. Researchers are blending PVB with nanocellulose to create solvent-free binders for 3-D-printed composites, hinting at incremental demand pockets beyond legacy markets. Overall, non-film uses are forecast to grow at 4.03% CAGR, trailing the headline polyvinyl butyral market but preserving niche profitability.

By End-user Industry: Automotive Leadership Faces Power Generation Challenge

Automotive glazing accounted for 52.74% of the polyvinyl butyral market volume in 2025 and is projected to post a steady 5.62% CAGR through 2031, driven by mandatory windshield standards in over 100 jurisdictions. Added glass area per vehicle, spurred by larger infotainment displays and roof-light expansions, elevates square-meter consumption, partially offsetting a moderate slowdown in global unit production. Acoustic grades, priced roughly 15% above standard films, are gaining market share as OEMs compete on NVH (noise, vibration, harshness) metrics in battery-electric models.

Power generation, chiefly photovoltaic modules, contributed only 15.94% of 2025 consumption yet is on track for the fastest 7.95% CAGR, lifting its share to 17.72% by 2031. The power-generation polyvinyl butyral market size for encapsulants is projected to reach USD 1.02 billion by 2031, driven by the growth of large-format thin-film solar projects and the increasing adoption of bifacial glass-glass panels. DuPont’s PV5200 sheets demonstrated 40-year service life potential in accelerated-aging tests, appealing to utility-scale developers seeking lower levelized cost of electricity.

Construction represented 15.83% of 2025 demand, especially in Asia, where skyscraper cladding and balcony balustrades proliferate. Retrofitting programs in Europe and North America stimulate replacement demand, with some cities mandating acoustic-graded interlayers along transit corridors. Aerospace, defense, and specialty optics round out the “other” category, relying on PVB for impact-resistant transparencies in rotorcraft and armored vehicles.

Geography Analysis

Asia-Pacific held 50.83% of polyvinyl butyral market share in 2025, underpinned by integrated petrochemicals, glass finishing, and automotive assembly clusters in China, Japan, and South Korea. Regional volume is forecast to grow at 6.11% CAGR through 2031, solidifying its lead as EV production hubs scale. Government incentives, such as China’s NEV credits and Japan’s green-building subsidies, accelerate demand for acoustic and low-VOC interlayers. Nonetheless, feedstock tightness from olefin-cracker curtailments occasionally disrupts supply, highlighting the need for inventory buffers and multi-sourcing strategies.

North America accounted for 19.08% of 2025 demand. Growth centers on the rehabilitation of aging infrastructure and the elevated adoption of laminated side windows in premium vehicles. The region’s construction codes consistently require 0.76 mm PVB interlayers in overhead glazing, ensuring baseline volumes. Eastman’s Ghent capacity expansion enables nearby supply to U.S. and Mexican OEMs, mitigating trans-Atlantic shipping costs and CO₂ footprints. Circular-economy programs, such as glass-laminate recycling hubs in Ohio—are piloting closed-loop feedstock streams that could temper virgin PVB growth after 2028.

Europe captured 16.46% share in 2025 and exhibits mature but technologically sophisticated demand. Tight carbon regulations spur architects to select higher-performing acoustic and solar-control interlayers that lower operational energy use. Kuraray and Everlam collaborate with EU glassmakers on bird-safe and post-tensioned laminate innovations, aligning with biodiversity directives. Extended-producer-responsibility schemes under discussion in Germany may require PVB producers to finance collection and recycling of end-of-life windshields, influencing cost structures after 2027.

Latin America, the Middle East, and Africa collectively represented 13.63% of global volume in 2025. Market development hinges on new float-glass investments in the Gulf and expanded automotive production in Brazil. Currency volatility and import duties remain hurdles, but multilateral infrastructure funding is boosting demand for laminated glass in airports and stadiums, creating incremental volumes for the polyvinyl butyral market.

Competitive Landscape

The polyvinyl butyral market is highly concentrated, with Eastman, Kuraray, and Sekisui accounting for an estimated 80-85% of global capacity, thereby sustaining an oligopolistic environment. These leaders operate backward-integrated value chains that encompass aldehyde derivatization and extrusion, granting cost and supply security advantages. Capital intensity, exceeding USD 150 million for a greenfield 50,000 t/y plant, deters new entrants. Long-term qualification protocols with OEMs, often spanning two model cycles, further entrench incumbents.

Players seek growth via high-margin niches and geographic proximity. Eastman’s 2024 Belgium revamp expands Saflex production for European acoustic and HUD applications, leveraging shorter lead times for German OEMs. Kuraray’s 2025 optical-film expansion in Japan taps booming LCD cover-glass and augmented-reality windshield demand. Sekisui targets Southeast Asia with Thailand capacity slated for 2026, capturing EV-related growth while diversifying outside its domestic base.

Strategic moves extend to sustainability. Everlam and Garland Glass co-develop solvent-free PVB recycling compatible with architectural films, aiming to integrate 40% recycled content by 2030. Patent filings show momentum in deep eutectic-solvent catalysis for butyral synthesis, offering 15% energy savings versus conventional acid catalysis. Smaller regional actors such as Qingdao Jiahua, Huakai, and Kingboard Special Resins, compete on localized supply and price flexibility, but lack the R&D heft to challenge premium niches currently controlled by the top three.

Polyvinyl Butyral (PVB) Industry Leaders

Chang Chun Group

Eastman Chemical Company

Sekisui Chemical Co., Ltd.

Kuraray Co., Ltd.

Kingboard (Fogang) Special Resins Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Eastman Chemical Company announced an investment to upgrade and expand its polyvinyl butyral (PVB) interlayer extrusion capabilities at its Ghent, Belgium facility. This expansion addresses the increasing demand from automotive and architectural markets. The project will enhance the supply capabilities for Saflex PVB products, with completion expected by 2026.

- July 2024: Sekisui Chemical announced an 8 billion yen investment to expand its PVB interlayer production capacity at its Rayong, Thailand facility. The new production line, scheduled to be operational in the second half of 2026, will focus on high-performance products for head-up displays and increase capacity by 7 million units annually.

Global Polyvinyl Butyral (PVB) Market Report Scope

Polyvinyl butyral (PVB) is a clear, colorless, amorphous thermoplastic material that can be produced by reacting polyvinyl alcohol and butyraldehyde. It is mainly used in fabricating various laminated glass products for the automotive, construction, and photovoltaic end-user sectors, owing to its optical clarity and strong adhesive nature. The polyvinyl butyral (PVB) market is segmented by type, end-user industry, and geography. By type, the market is segmented into adhesive films, paints and coatings, printing inks and lacquers, and other types (binders for ceramics and composite fibers). By end-user industry, the market is segmented into automotive, construction, power generation, and other end-user industries (aerospace, defense). The report also covers the market size and forecasts for the polyvinyl butyral (PVB) market in 15 countries across the major regions. For each segment, the market sizing and forecast have been done on the basis of revenue (USD million).

| Adhesive Films |

| Paints and Coatings |

| Printing Inks and Lacquers |

| Other Types (Binders for Ceramics and Composite Fibres) |

| Automotive |

| Construction |

| Power Generation |

| Other End-user Industries (Aerospace, Defence, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Adhesive Films | |

| Paints and Coatings | ||

| Printing Inks and Lacquers | ||

| Other Types (Binders for Ceramics and Composite Fibres) | ||

| By End-user Industry | Automotive | |

| Construction | ||

| Power Generation | ||

| Other End-user Industries (Aerospace, Defence, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the polyvinyl butyral market?

The polyvinyl butyral market size reached USD 4.29 billion in 2026 and is forecast to climb to USD 5.69 billion by 2031 at a 5.78% CAGR.

Which segment holds the largest polyvinyl butyral market share?

Adhesive films dominate with 94.12% share in 2025, largely driven by laminated safety-glass applications.

Why is Asia-Pacific the leading region for polyvinyl butyral demand?

Integrated automotive and construction supply chains in China, Japan, and South Korea give Asia-Pacific 50.83% global share and the highest regional CAGR of 6.11% through 2031.

How are electric vehicles influencing polyvinyl butyral consumption?

EVs amplify demand for acoustic PVB interlayers that cut cabin noise by up to 6 dB, prompting capacity expansions in Thailand and Japan targeted at this niche.

What challenges could slow polyvinyl butyral market growth?

Feedstock volatility, rising recycling rates that offset virgin demand, and competition from substitutes such as EVA and ionoplast materials could temper the market’s CAGR by up to 1.5 percentage points.

Page last updated on: