Polyvinylidene Difluoride (PVDF) Membrane Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

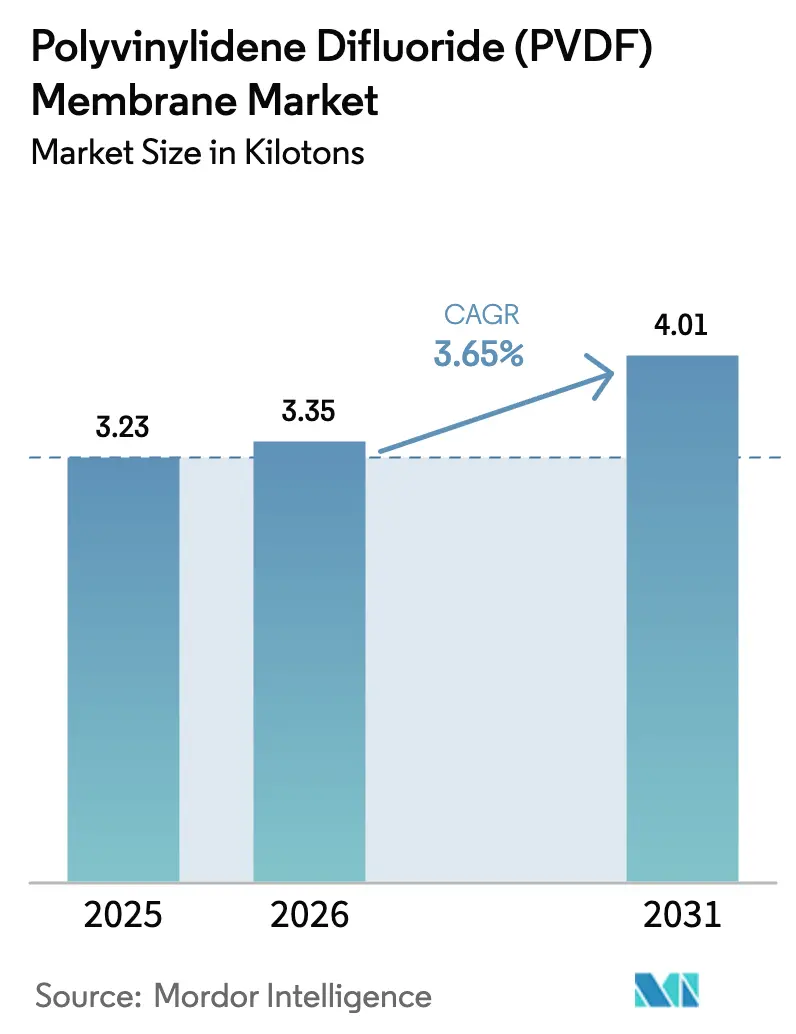

| Market Volume (2026) | 3.35 kilotons |

| Market Volume (2031) | 4.01 kilotons |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyvinylidene Difluoride (PVDF) Membrane Market Analysis by Mordor Intelligence

The Polyvinylidene Difluoride Membrane Market size is expected to increase from 3.23 kilotons in 2025 to 3.35 kilotons in 2026 and reach 4.01 kilotons by 2031, growing at a CAGR of 3.65% over 2026-2031. This steady headline growth belies a major shift in end-use patterns as biopharmaceutical plants replace batch filters with continuous, single-use tangential-flow systems that demand higher flux, lower protein binding, and traceable serialization. Hydrophilic grades dominate because they shorten validation time, while nanofiltration modules are scaling fastest as virus-clearance rules tighten. Consolidated supply, rapid capital expenditure by leading brands, and regional manufacturing strategies are shaping competitive behavior. Meanwhile, Asia-Pacific policy pressure on pharmaceutical wastewater and India’s contract-manufacturing boom continue to anchor volume growth.

Key Report Takeaways

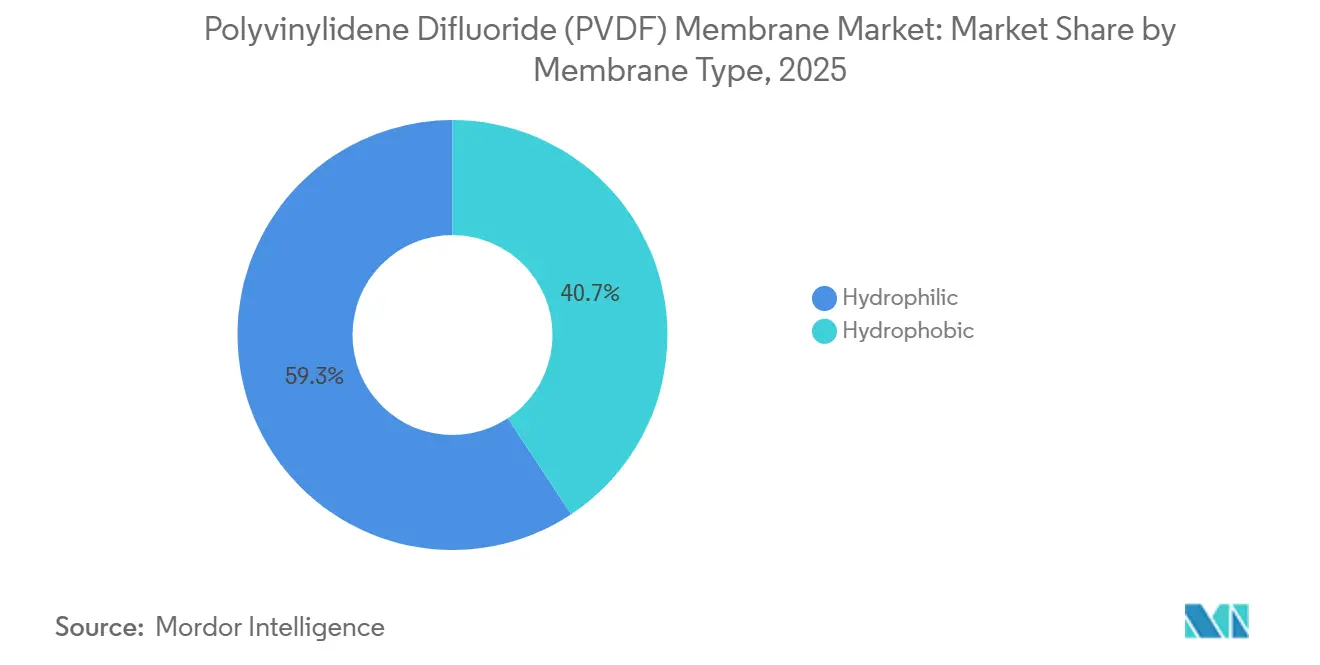

- By membrane type, hydrophilic variants held 59.32% PVDF membrane market share in 2025 and are set to expand at a 3.61% CAGR through 2031.

- By technology, nanofiltration recorded the highest projected growth at a 4.27% CAGR to 2031, while microfiltration retained 41.75% of the PVDF membrane market size in 2025.

- By application, filtration led with 38.36% of the PVDF membrane market size in 2025 and is forecast to grow at a 4.96% CAGR to 2031.

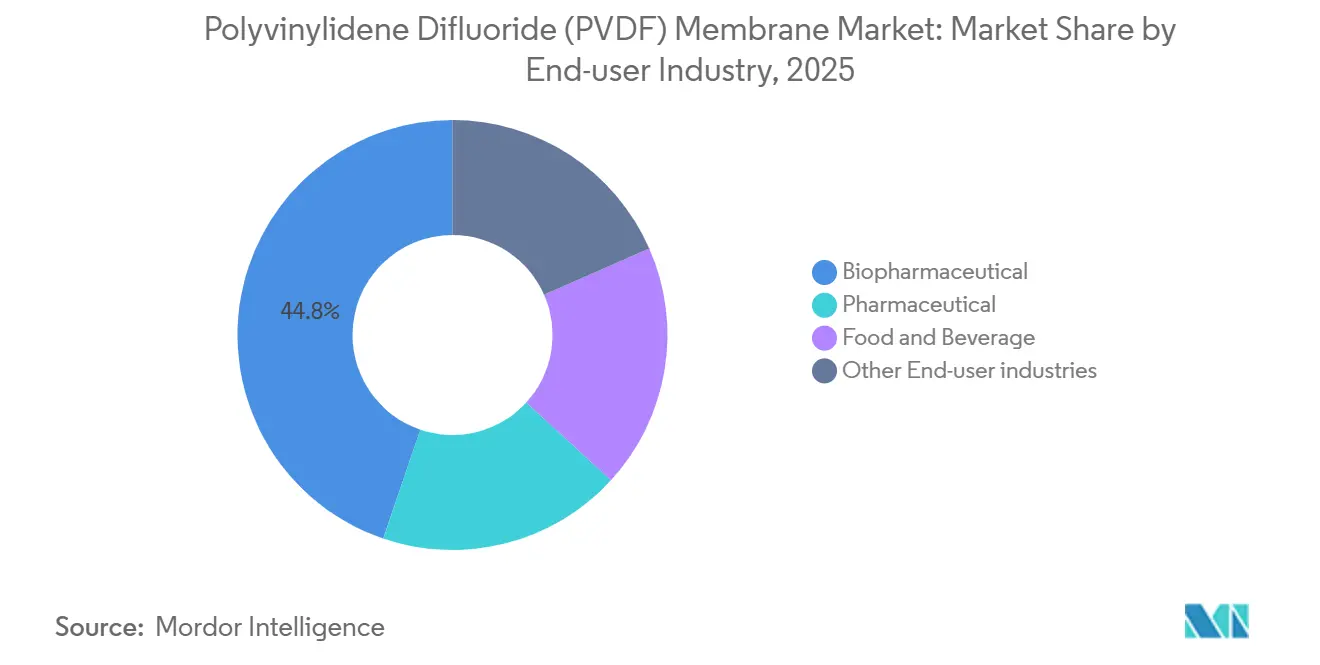

- By end-user industry, biopharmaceutical producers captured 44.78% PVDF membrane market share in 2025, and this segment is advancing at a 4.77% CAGR through 2031.

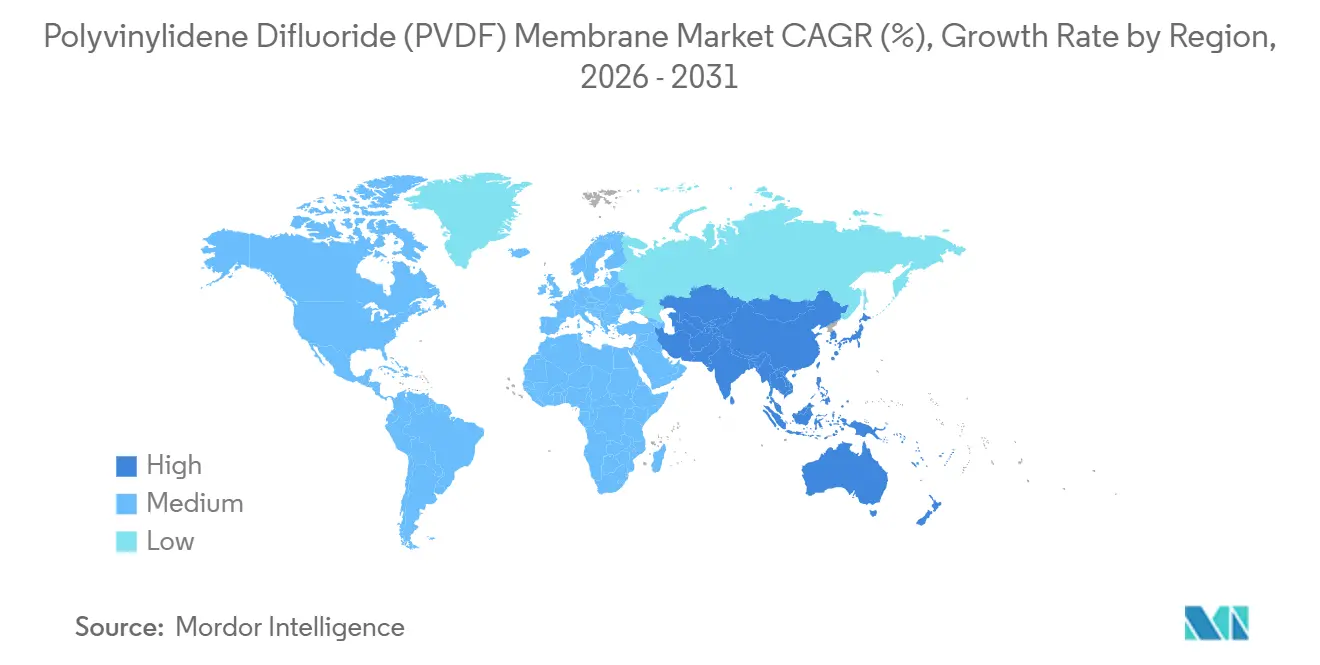

- By geography, Asia-Pacific commanded 56.39% of the 2025 volume and is expanding at a 4.85% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyvinylidene Difluoride (PVDF) Membrane Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of bioprocessing demand | +1.0% | Global, with APAC and North America leading capacity additions | Medium term (2-4 years) |

| Rising utilization in medical and diagnostic devices | +0.5% | North America and EU, driven by point-of-care diagnostics and Western blotting | Short term (≤ 2 years) |

| Growing demand for wastewater treatment applications | +0.4% | APAC core (China, India), spill-over to Middle East | Long term (≥ 4 years) |

| Continuous expansion of biotechnology and pharma sector | +0.9% | Global, concentrated in Boston, San Francisco, Hyderabad, Bengaluru clusters | Medium term (2-4 years) |

| Emergence of single-use TFF modules integrating PVDF | +0.7% | North America and EU, with adoption spreading to APAC CDMOs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Bioprocessing Demand

Single-use tangential-flow cassettes now arrive pre-irradiated and serialized, eliminating on-site integrity testing and reducing campaign turnaround from days to hours. Biocon Biologics invested approximately USD 1.2 billion in a new Bengaluru biosimilar manufacturing plant between 2022 and 2025 that embeds advanced continuous harvest and purification processes, tripling membrane consumption per kilogram of drug substance compared with legacy lines[1]Pharmaceutical Technology Team, “India CDMO Market Outlook,” pharmaceutical-technology.com. Cell- and gene-therapy developers require residual host-cell DNA below 10 nanograms per dose, steering them toward 0.2-micrometer hydrophilic PVDF that balances sterile retention and flux. Capacity additions remain lengthy; Asahi Kasei broke ground in July 2026 on its fourth Planova virus-removal filter plant that will open in 2030, underscoring structural supply tightness[2]Asahi Kasei, “Planova Fourth Plant Announcement,” asahi-kasei.com. Both brand owners and CDMOs lock in multi-year supply contracts, reinforcing volume visibility and underpinning the PVDF membrane market outlook. The resulting demand pull lifts average plant utilization rates above 85%, supporting premium pricing.

Rising Utilization in Medical and Diagnostic Devices

PVDF remains the benchmark blotting media. Bio-Rad’s Sequi-Blot range binds 170–200 µg/cm² of protein, outperforming nitrocellulose while tolerating multiple stripping cycles for antibody reprobing. Decentralized testing heightens this advantage because point-of-care kits must withstand ambient storage and deliver results within 15 minutes. Merck installed a second membrane line in Cork in 2025 aimed at lateral-flow assays for dengue, malaria, and COVID-19 detection. Pore-size bifurcation persists: 0.2 µm sheets enable low-molecular-weight protein sequencing, while 0.45 µm variants support general immunoblotting. The net effect is a broader installed base of diagnostic platforms that consume replacement rolls annually, keeping the PVDF membrane market on a predictable reorder cycle.

Growing Demand for Wastewater Treatment Applications

China’s pharmaceutical wastewater rules cap biochemical oxygen demand at 50 mg/L and chemical oxygen demand at 100 mg/L, levels that conventional activated sludge cannot achieve. PVDF hollow-fiber membrane bioreactors now polish effluent at 2,000 m³/day scales, with operating costs ranging from USD 0.168 to USD 1.39 per cubic meter depending on influent strength. Hangzhou Qiushi supplies many of these installations, leveraging in-house resin casting to control pore uniformity. Outside China, Toray opened a reverse-osmosis plant in Saudi Arabia in November 2025, pairing PVDF microfiltration pretreatment with polyamide RO to cut fouling and prolong membrane life. Municipal adoption lags industrial uptake because budgets favor low upfront outlay, but tightening nutrient limits mean utilities increasingly view membrane bioreactors as the only one-step solution for nitrification, denitrification, and pathogen removal. This shift supports a multi-year tailwind for the PVDF membrane market.

Continuous Expansion of Biotechnology and Pharma Sector

India’s CDMO market rose to USD 8.2 billion in 2024 and should hit USD 20.8 billion by 2030 at 16.8% CAGR, driven by 30–40% cost advantages versus Western facilities. Laurus Labs injected USD 150 million into a Visakhapatnam API plant in 2023, and Piramal Pharma committed USD 100 million to an Ahmedabad fill-finish site in 2024, each built around single-use filtration trains. These hubs shorten the path from lab feasibility to GMP production, locking in local demand for hydrophilic membranes. Large-molecule biologics consume 10–20 m² of membrane per kilogram of product, dwarfing the 1–2 m² requirement for small-molecule sterile filtration, which tilts volume growth toward bioprocessing. Global CDMOs now position membrane technical-service staff on-site in Hyderabad and Bengaluru, fueling rapid knowledge transfer and boosting the PVDF membrane market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of PVDF membranes | -0.5% | Global, most acute in price-sensitive food-and-beverage and municipal water segments | Short term (≤ 2 years) |

| Membrane fouling in high-fat food and beverage streams | -0.2% | North America and EU dairy and beverage processing; APAC emerging | Medium term (2-4 years) |

| ESG scrutiny on fluorinated-polymer disposal | -0.4% | EU and North America, with regulatory pathways under ECHA and EPA PFAS frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of PVDF Membranes

PVDF resin sells for USD 8–12/kg, double polysulfone, and triple cellulose acetate, pricing many municipal and dairy projects out of the market. Arkema expanded Calvert City PVDF capacity by 15% in 2024 but targeted batteries and semiconductors rather than filtration, showing that resin producers prioritize higher-margin outlets. Biopharma buyers absorb the premium because membrane costs stay below 1% of drug-substance value, yet dairy processors running on 5–8% margins cannot justify PVDF when polysulfone delivers 80% of the flux at half the cost. This price gap limits penetration into commodity applications and clips upside potential for the PVDF membrane market in price-sensitive segments.

Membrane Fouling in High-Fat Food and Beverage Streams

Casein-whey separation operates at 10–100 L/h-m², but fat globules adsorb onto hydrophilic PVDF, forcing caustic cleaning every 4–6 hours and cutting service life from 18 months to 12 months. Ceramic alternatives such as Pall’s Membralox GP-IC achieve three-year life and 95% flux recovery, though at USD 1,500–2,000/m² installed versus USD 300–500 for PVDF. The capital-versus-operating cost trade-off pushes dairy processors to optimize around total lifecycle value rather than material choice alone. Seasonal juice clarification favors disposable PVDF cartridges that avoid off-season storage, yet the cleaning burden in continuous dairy lines remains a headwind for the PVDF membrane market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Membrane Type: Hydrophilic Dominance Reflects Bioprocessing Shift

Hydrophilic variants held 59.32% PVDF membrane market share in 2025 and are forecast to grow at a 3.61% CAGR, outperforming hydrophobic formats that serve air and solvent filtration. Merck’s Durapore line delivers 170–200 µg/cm² binding capacity, enabling multiplex antibody reuse without methanol pre-wetting. Hydrophobic PVDF remains critical for venting and solvent applications where moisture repellence prevents pore blockage. Surface-modification research explores zwitterionic peptide grafting and titanium-dioxide nanocomposites that preserve flux without PFAS processing aids, addressing ESG concerns. A 2024 Membranes study reported 40–60% higher pure-water flux on graphene-oxide-enhanced PVDF, although long-term caustic stability is unproven. Amphiphilic copolymers that toggle wettability by pH may blur the hydrophilic-hydrophobic divide, yet validation cycles mean current segmentation will persist through the forecast period. The continued shift toward biologics keeps hydrophilic grades central to the PVDF membrane market.

By Technology: Nanofiltration Gains as Virus Clearance Tightens

Microfiltration accounted for 41.75% of the PVDF membrane market size in 2025, anchored by sterile filtration at 0.2 µm. Nanofiltration, however, is expanding at a 4.27% CAGR because 20-nm cutoffs remove viruses while passing monoclonal antibodies above 150 kDa. Asahi Kasei’s Planova range, though cellulose-based, demonstrates the pull of virus-removal membranes and validates demand for PVDF analogs that tolerate caustic cleaning. Ultrafiltration occupies the middle ground for protein concentration, while niche technologies such as membrane distillation remain below 5% of volume. PVDF’s chemical resistance opens doors for caustic-cleaned nanofiltration skids in continuous bioreactors, where solvent compatibility eclipses the lower cost of polyamide. Integrated membrane cascades reduce chromatography steps and speed virus clearance validation, reinforcing the growth trajectory of nanofiltration inside the PVDF membrane market.

By Application: Filtration Leads, Purification Gains Traction

Filtration held 38.36% PVDF membrane market share in 2025 and is growing at 4.96% CAGR thanks to injectable-drug regulations that mandate sterile-grade barriers. Blotting consumes smaller areas but commands premium pricing in research and diagnostics. Separation covers dairy fractionation and yeast recovery, while purification targets trace contaminant removal, such as endotoxins and host-cell proteins. Merck’s EUR 150 million Blarney facility bundles TFF devices and virus-filtration modules, blurring application lines but reinforcing membrane demand. Continuous manufacturing multiplies membrane usage because processes filter continuously rather than per batch. Depth-filter competition persists, yet tangential-flow ultrafiltration recovers 95–98% of product, improving yields and favoring PVDF adoption. Collectively, these forces keep filtration at the core of the PVDF membrane market while purification posts the fastest step-change in technical specifications.

By End-User Industry: Biopharmaceutical Sector Anchors Demand

Biopharmaceutical plants consumed 44.78% of PVDF volume in 2025 and will grow at a 4.77% CAGR, driven by monoclonal antibody, cell-therapy, and gene-therapy pipelines that require sterile barriers at multiple points. Pharmaceutical small-molecule operations rely on PVDF for parenteral solutions and HPLC solvent filtration, while food and beverage processors weigh PVDF against ceramic and polysulfone on lifecycle cost. India’s CDMO surge, centered in Hyderabad and Bengaluru, is redirecting global procurement flows and deepening supplier technical-service footprints. Water and wastewater applications grow steadily as discharge standards tighten, although ESG scrutiny tempers municipal enthusiasm. Electronics fabs use PVDF pretreatment to protect ultrapure polyamide RO elements, a niche but high-margin end market. The biopharmaceutical pull remains decisive in shaping production planning across the PVDF membrane market.

Geography Analysis

Asia-Pacific held 56.39% of the PVDF membrane market share in 2025 and is expanding at a 4.85% CAGR through 2031, propelled by China’s wastewater mandates, India’s CDMO boom, and Japan’s precision membrane exports. China’s 2,000 m³/day PVDF MBRs for pharmaceutical effluent underscore regulatory enforcement, while Hangzhou Qiushi supplies local modules with short lead times. India’s contract manufacturing jumped to USD 8.2 billion in 2024, targeting USD 20.8 billion by 2030, pulling membranes into new single-use bioreactors. Toray’s November 2025 Saudi RO plant serves Gulf desalination projects, with PVDF pretreatment cutting fouling. South Korea’s biotech corridor benefits from domestic PVDF production at Hyundae Micro and LG Chem, tightening supply loops for Samsung Biologics.

North America’s PVDF membrane market growth is supported by Danaher’s USD 1.6 billion capacity expansion across Pensacola, Fajardo, and a South Korean line serving U.S. demand. Government initiatives such as BARDA reinforce on-shore vaccine supply, sustaining order visibility. Europe follows with region-for-region manufacturing; Merck’s EUR 440 million Cork hub produces filtration devices for the EMEA market, and Sartorius’ Yauco investment serves the Americas. The 6.5-year PFAS derogation shapes municipal uptake, nudging utilities toward PVDF alternatives yet leaving industrial users largely unaffected.

South America and Middle East and Africa are witnessing rising demand for PVDF membranes. Saudi desalination and Brazilian sanitation privatization drive orders for PVDF-based MBRs that treat high-salinity or nutrient-rich feedwater. South African mining and petrochemical firms adopt closed-loop ultrafiltration-RO systems to stretch water supply, with PVDF pretreatment extending RO life from three to five years. While smaller in tonnage, these regions offer high unit margins that attract specialist suppliers in the PVDF membrane market.

Competitive Landscape

The Polyvinylidene Difluoride (PVDF) market is moderately fragmented. Qualifying a new membrane for GMP production requires 12–18 months of validation, cementing customer stickiness. Danaher’s USD 1.6 billion spend since 2019, Merck’s EUR 440 million Cork expansion, and Sartorius’ EUR 410 million outlays in 2024 illustrate scale investment that few challengers can match. Patent activity emphasizes PFAS-free surface treatments and sensor-embedded cassettes, opening white space that nimble innovators can pursue. GVS filed DMSO-phase-inversion process patents to narrow pore distribution, while academic work on graphene oxide shows flux gains yet awaits industrial proof. Niche specialists such as Cobetter and Membrane Solutions target food-and-beverage and wastewater segments where lower regulatory scrutiny allows quick iteration. ECHA’s PFAS proposal steers some municipal buyers toward ceramic or polyethersulfone, creating headroom for non-fluoropolymer entrants. The combined dynamics underscore a PVDF membrane market in which scale, validation data, and ESG compliance define long-term positioning.

Polyvinylidene Difluoride (PVDF) Membrane Industry Leaders

Arkema

Merck

Pall Corporation (Danaher Corporation)

Asahi Kasei Corporation

Cytiva (Danaher Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Danaher’s Cytiva division began production at a new South Korean filtration line, cutting lead times from 12 weeks to 6 weeks for single-use TFF cassettes.

- November 2025: Toray opened a reverse-osmosis membrane facility in Dammam, Saudi Arabia, targeting Gulf desalination and industrial reuse projects.

- September 2025: Merck inaugurated a EUR 150 million climate-neutral filtration plant in Blarney, Ireland, producing TFF and virus-filtration modules.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the polyvinylidene difluoride (PVDF) membrane market as the worldwide demand for finished flat-sheet or hollow-fiber membranes made wholly from PVDF resin and supplied in rolls, cassettes, cartridges, or modules for filtration, purification, separation, and blotting across biopharmaceutical, industrial water, food, electronics, and laboratory settings. Mordor Intelligence counts both hydrophilic and hydrophobic grades at original sale and at subsequent replacement.

Scope exclusion: We exclude PVDF resin consumed in battery binders, coatings, pipes, or composite membranes where PVDF represents less than half of the active layer.

Segmentation Overview

- By Membrane Type

- Hydrophobic

- Hydrophilic

- By Technology

- Microfiltration

- Ultrafiltration

- Nanofiltration

- Other Technologies

- By Application

- Filtration

- Blotting

- Separation

- Purification

- Other Applications

- By End-user Industry

- Biopharmaceutical

- Pharmaceutical

- Food and Beverage

- Other End-user industries

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with membrane OEM process engineers, Asian contract water-treatment operators, procurement leads at US biopharma plants, and European distributors. These interviews validated preliminary numbers, filled pricing and replacement-cycle gaps, and refined adoption curves inferred from secondary data.

Desk Research

We began with UN Comtrade shipment codes, United States International Trade Commission tariff tables, and Japan Chemical Fibers Association production yearbooks to map physical flows. Patent family searches on Questel, quarterly filings to the US SEC and Tokyo Stock Exchange, and regulatory notices from the European Chemicals Agency on PFAS informed supply shifts and potential demand restraints. Technical depth came from peer-reviewed work in the Journal of Membrane Science, while Dow Jones Factiva, company press releases, and investor decks clarified pricing and capacity moves. This list is illustrative; many additional public and paid sources underpinned our desk work.

Market-Sizing & Forecasting

A top-down build starts with installed membrane area across water, bioprocessing, and food verticals reconstructed from production and trade records. It then converts it into volume through standard packing densities. Select bottom-up checks, supplier shipment roll-ups and sampled ASP × square-meter calculations, reconcile totals. Key model inputs include membrane replacement interval, average surface per unit of treated fluid, new bioreactor capacity additions, municipal reuse project announcements, and PFAS-phase-out timelines. Multivariate regression blended with scenario analysis projects these drivers to 2030, and gaps in bottom-up estimates are bridged using utilization factors confirmed in primary interviews.

Data Validation & Update Cycle

Outputs undergo triple-layer analyst review, where anomalies are tested against bioprocessing CAPEX trends and quarterly shipment disclosures. Models refresh annually, with interim updates for material events, so clients always receive the latest baseline.

Why Mordor's PVDF Membrane Baseline Stays Trustworthy

Published figures often diverge because providers pick different product mixes, years, and pricing paths.

Our disciplined scope, dynamic price curves, and yearly refresh narrow those gaps for clearer decision making.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 3.23 million tons (2025) | Mordor Intelligence | - |

| USD 779 million (2022) | Global Consultancy A | Narrow end-use scope, constant ASP, older base year |

| USD 724.53 million (2024) | Research Firm B | Omits blotting demand, fixed replacement rate |

These comparisons show that our balanced, variable-driven framework delivers a transparent, reproducible baseline that decision makers can trust.

Key Questions Answered in the Report

What CAGR is forecast for the PVDF membrane market from 2026 to 2031?

The market is projected to grow at a 3.65% CAGR, reaching 4.01 kilotons by 2031.

Which membrane type currently leads global volume?

Hydrophilic PVDF holds 59.32% of 2025 demand due to its low protein binding and rapid wet-out properties.

Why is nanofiltration the fastest-growing technology category?

Stricter virus-clearance rules push process engineers to adopt 20-nm membranes that remove pathogens while letting large biologics pass, driving a 4.27% CAGR.

Which region commands the largest share of PVDF membrane demand?

Asia-Pacific accounts for 56.39% of the 2025 volume, supported by strong pharmaceutical wastewater and CDMO growth.

Page last updated on: