Polypill Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.18 Billion |

| Market Size (2031) | USD 38.82 Billion |

| Growth Rate (2026 - 2031) | 2.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

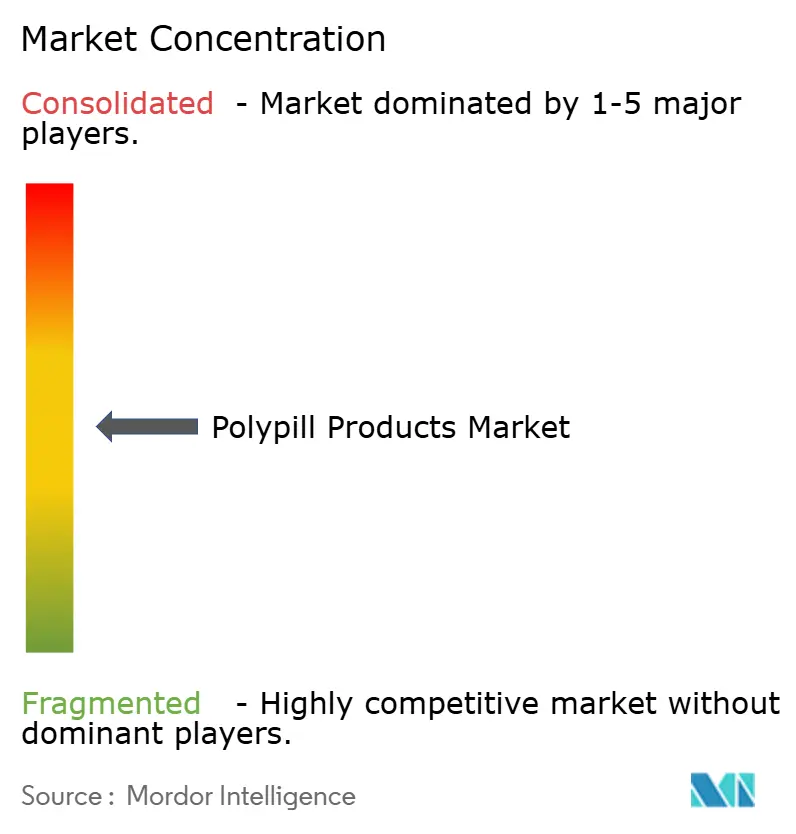

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polypill Products Market Analysis by Mordor Intelligence

The Polypill Products Market size is expected to increase from USD 33.41 billion in 2025 to USD 34.18 billion in 2026 and reach USD 38.82 billion by 2031, growing at a CAGR of 2.58% over 2026-2031.

Established single-parameter formulations still dominate hospital formularies in North America and Europe, yet the polypill products market is steadily tilting toward multi-parameter combinations that simplify cardiometabolic therapy in low- and middle-income countries. Rapid drug-price deflation under China’s volume-based procurement, preferential reimbursement for fixed-dose combinations in Japan and South Korea, and FDA fast-tracking of the triple-therapy Widaplik in 2025 highlight the policy momentum that is pulling adherence-oriented therapies into mainstream use. Modular 3D-printing pilots now running in fewer than five hospitals have already cut pharmacist compounding time by 55%, signaling early disruption to centralized manufacturing economics.

Key Report Takeaways

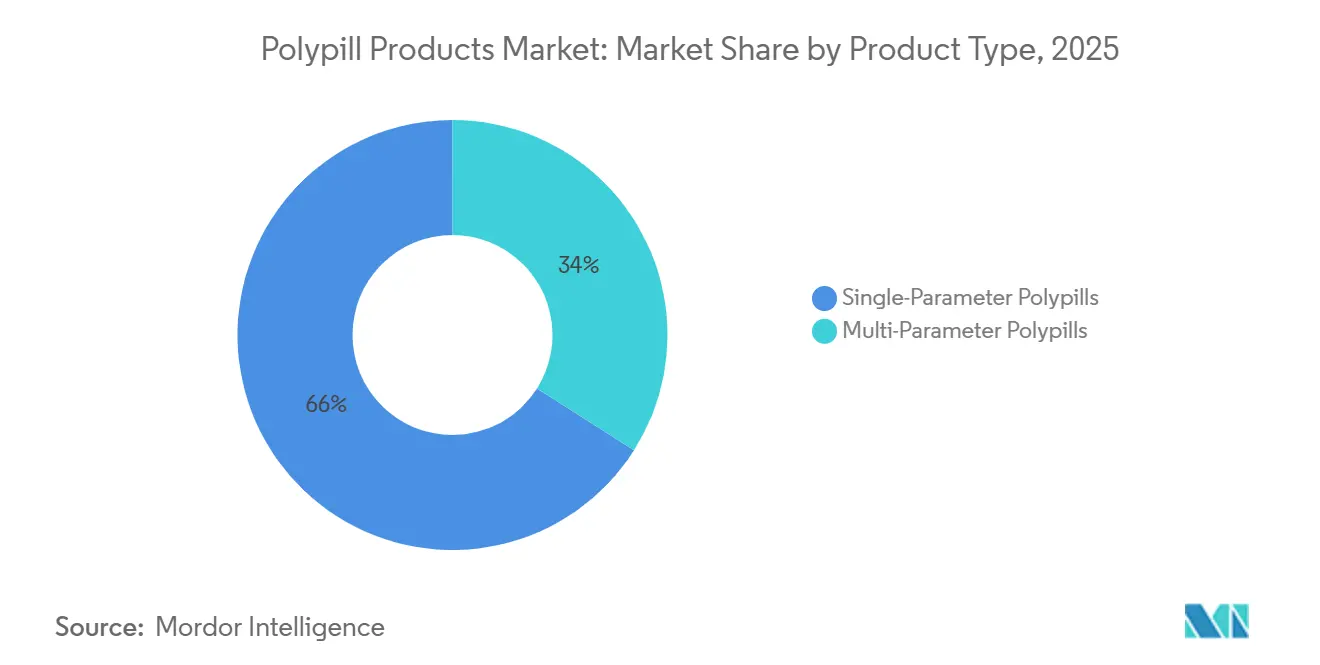

- By product type, single-parameter polypills held 66.02% of the polypill products market share in 2025, while multi-parameter formulations are forecast to expand at a 3.06% CAGR through 2031.

- By application, cardiovascular disease prevention accounted for 51.27% of the polypill products market in 2025, and diabetes-linked CV risk reduction is projected to grow at a 4.63% CAGR through 2031.

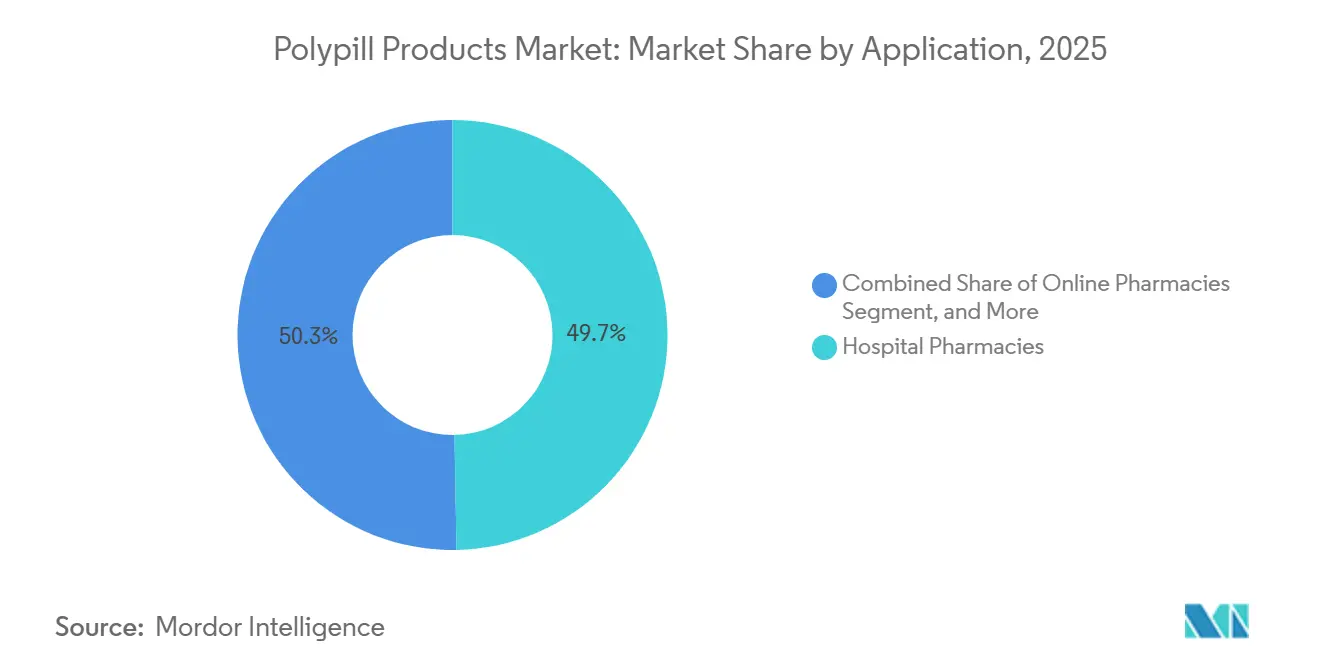

- By distribution channel, hospital pharmacies led with 49.72% revenue share in 2025; online pharmacies are projected to grow at a 5.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polypill Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular & metabolic diseases | +0.8% | Global, with highest burden in South Asia, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Improved adherence & pill-burden reduction with FDCs | +0.6% | Global, particularly LMIC settings with fragmented healthcare access | Medium term (2-4 years) |

| Inclusion of key FDCs in WHO EML & clinical guidelines | +0.5% | LMIC procurement systems, spill-over to middle-income Asia Pacific | Medium term (2-4 years) |

| Aging population driving cost-effective polypharmacy | +0.4% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| 3-D printing enables personalized, on-demand polypills | +0.2% | Academic medical centers in UK, US, select EU hubs | Long term (≥ 4 years) |

| LMIC public-procurement schemes boosting bulk uptake | +0.7% | China, India, Brazil, Indonesia, national programs in Sub-Saharan Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular & Metabolic Diseases

Cardiovascular disease and type 2 diabetes now co-occur in roughly 30% of patients in high-burden regions, creating demand for once-daily tablets that target multiple risk factors at once. Meta-analyses published in 2025 reported 22%–29% reductions in major adverse cardiovascular events among polypill users versus usual care.[1]JAMA Cardiology, “Cost-Effectiveness of Polypill-Based Primary Prevention,” jamanetwork.com The World Health Organization’s 2025 Model List of Essential Medicines endorsed GLP-1 receptor agonists for patients with diabetes and co-morbid cardiovascular or kidney disease, a move that strengthens the case for cardiometabolic fixed-dose combinations. Regulators on both sides of the Atlantic now recognize adherence improvement as a patient-centered endpoint, compressing review timelines when superior persistence is documented. Cost-utility models peg the incremental cost per QALY of a primary-prevention polypill at USD 8,560, well beneath OECD willingness-to-pay thresholds.

Improved Adherence & Pill-Burden Reduction with FDCs

One-year persistence on multi-pill cardiovascular regimens often drops below 60%, yet randomized trials such as SECURE logged 86% adherence in the polypill arm and a 24% cut in cardiovascular events. Sanofi’s Global Health Unit has distributed low-cost combinations to more than 586,000 patients across 40 countries, often pairing drug delivery with SMS reminders that increase refill rates by 15%–20% relative to retail benchmarks. Online pharmacies in India bundle subscriptions with teleconsultations that auto-titrate therapy after remote blood-pressure uploads, reinforcing persistence gains. The European Medicines Agency guideline on combination products explicitly treats real-world adherence evidence as a valid registration endpoint. As digital adherence tools spread, the polypill products market can capture value by reducing hospitalizations and productivity losses.

Inclusion of Key FDCs in WHO EML & Clinical Guidelines

The WHO added three cardiovascular polypill templates to its 23rd Model List of Essential Medicines in 2023, prompting procurement shifts in more than 50 LMICs whose formularies mirror the list. India’s 2024 public procurement order reserves government tenders for firms enrolled in the Production-Linked Incentive scheme, effectively steering demand toward domestic manufacturers such as Cipla and Sun Pharma. China’s 11th wave of volume-based procurement in 2025 covered 55 drugs and slashed prices by up to 90%, obligating public hospitals to secure 60% of their volume from winning bidders.[2]National Healthcare Security Administration, “National Volume-Based Procurement,” nhsa.gov.cn Local trials such as PolyPars in Iran demonstrate 50% reductions in event rates with a USD 0.10 per day regimen, strengthening health-economic arguments in resource-constrained settings. Prequalification and GMP audits remain gatekeepers for LMIC tenders, pushing generic suppliers to maintain baseline quality.

Aging Population Driving Cost-Effective Polypharmacy

Japan, where 29% of residents are 65 or older, now records polypharmacy in more than 40% of seniors, sparking reimbursement incentives for fixed-dose combinations that simplify dosing. South Korea’s national insurer cut patient co-payments for approved cardiovascular polypills by 20% in 2024, boosting prescriptions by 12% within 6 months. The CNIC-Polypill, available in six dose permutations, offers the titration flexibility clinicians need to personalize geriatric therapy while sustaining adherence gains. Health-technology assessors in Germany and the United Kingdom now assign monetary value to persistence-driven QALY gains, justifying higher unit prices for fixed-dose combinations that supplant multi-pill regimens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity for multi-API approvals | -0.5% | Global, with heightened scrutiny in EU and US | Medium term (2-4 years) |

| Limited dosing flexibility reduces clinician uptake | -0.4% | North America, Europe, academic medical centers | Medium term (2-4 years) |

| Patent-price & reimbursement pressures | -0.3% | OECD countries, middle-income Asia Pacific | Short term (≤ 2 years) |

| Stability challenges in hot/humid supply chains | -0.2% | Tropical Zone IVb climates (Sub-Saharan Africa, Southeast Asia, Latin America) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity for Multi-API Approvals

Sponsors must run separate bioequivalence studies for every strength permutation, multiplying time and cost for a six-strength product like the CNIC-Polypill. Zone IVb climate testing, mandatory for tropical markets, forces moisture-barrier packaging when acid-labile APIs such as ramipril degrade above 30 °C and 75% humidity. The FDA cleared Widaplik only after an 18-month accelerated-stability program and a 500-patient bioequivalence trial, delaying the launch by roughly 2 years. Patent linkage in the U.S. and Canada enables innovators to stack multiple formulation and method patents, extending market exclusivity. Global harmonization lags: ICH Q1A(R2) does not cover multi-API interactions, so each authority negotiates bespoke protocols, elongating timelines.

Limited Dosing Flexibility Reduces Clinician Uptake

A fixed ramipril 5 mg, amlodipine 5 mg, atorvastatin 20 mg tablet cannot serve a patient needing 10 mg of ramipril and only 2.5 mg of amlodipine, nudging clinicians back to multi-pill regimens or partial adherence. The SMART cohort logged only 30% uptake of a diabetic polypill among vascular-disease patients because renal dosing and glycemic control required individualized titration. Metformin doses vary fourfold across patients and often require twice-daily intake, complicating synchronization with once-daily cardiovascular agents. Just five hospitals worldwide have validated 3D printing lines that could solve this flexibility gap, and each printer costs roughly USD 150,000. Reimbursement frameworks in Germany and France penalize off-label dose splitting, further discouraging polypill prescriptions outside narrow indication windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Parameter Formulations Gain Traction

Multi-parameter tablets are forecast to expand at a 3.06% CAGR, outpacing the overall polypill products market. The CNIC-Polypill, sold in six dose permutations, demonstrates how multilayer tablet technology sidesteps API incompatibility, delivering about 7% extra LDL-cholesterol reduction when atorvastatin and ramipril are co-administered. Single-parameter tablets accounted for 66.02% of 2025 revenue because they cleared regulatory hurdles early and aligned with existing hospital protocols. Still, SECURE’s 24% MACE reduction and PolyIran-Liver’s 9.3 mg/dL fasting glucose drop provide clinical ammunition for triple- and quadruple-component products. George Medicines’ FDA-cleared Widaplik signals mainstream acceptance of three-drug hypertension therapy, while Ferrer’s Trinomia is scaling across Europe. Formulation advances—coated pellet cores, multilayer compression, and hot-melt extrusion—lower historical barriers that once limited API counts.

Competitive intensity will rise once Chinese and Indian generics replicate early movers under local production mandates, likely shaving 20%–30% from branded prices. Innovators, therefore, lean on differentiated evidence and dose-flexibility kits to defend price premiums.

By Application: Diabetes-Linked CV Risk Reduction Accelerates

Diabetes-linked cardiovascular therapy is growing at 4.63% almost double the headline CAGR, as guidelines now treat type 2 diabetes as a coronary-risk equivalent. WHO’s 2025 move to list GLP-1 receptor agonists foreshadows multi-API tablets that marry glycemic control with lipid- and blood-pressure-lowering agents. Yet integrating metformin remains challenging because doses range from 500 mg to 2,000 mg and often require twice-daily dosing, which clashes with once-daily cardiovascular regimens. Trials such as PolyPars show 50% reductions in event rates in mixed cardiometabolic populations, and cost-per-QALY analyses sit far below usual local thresholds.

Cardiovascular prevention still accounted for 51.27% of the polypill products market in 2025. As hospital protocols integrate mixed-pathology risk scores, analysts expect diabetes-centric combinations to add almost USD 2 billion to incremental revenue by 2031. The polypill products market share of cardiometabolic hybrids could therefore surpass 20% within the forecast window, provided developers solve metformin’s dose-frequency hurdle and secure payer acceptance for pricey GLP-1 components.

By Distribution Channel: Online Pharmacies Leverage Digital Integration

Hospital pharmacies accounted for 49.72% of 2025 revenue because public tenders in China and India require them to source centrally contracted volumes at steep discounts. Retail chains rank second but face stiff competition as online platforms expand 24-hour delivery across urban clusters. India’s PharmEasy and 1mg now embed auto-refill, teleconsultation, and SMS adherence nudges into subscription packages, pushing refill rates 15%–20% above brick-and-mortar norms. China’s dual-track system channels low-priced generics to public hospitals while letting private hospitals and e-pharmacies target affluent segments with branded polypills at 30%–50% premiums.

The online channel is forecast to grow at a 5.18% CAGR by 2031. Regulatory clarity on e-prescriptions and cold-chain compliance remains a gating factor in Southeast Asia and Latin America, but demand for doorstep delivery is surging among urban millennials managing hereditary dyslipidemia. If digital adherence dashboards continue to cut early discontinuation, insurers may steer chronic-disease members toward e-pharmacy subscriptions, raising the polypill products market share of online outlets beyond 20% in the next five years.

Geography Analysis

North America generated 41.36% of 2025 revenue, buoyed by high hypertension prevalence, widespread insurance coverage, and early regulatory approval of triple-component tablets such as Widaplik. Patent linkage rules slow generic erosion, allowing innovators to maintain double-digit margins. Canada follows similar intellectual-property pathways, while Mexico has only recently added polypills to its essential medicines list, so purchase volumes remain modest.

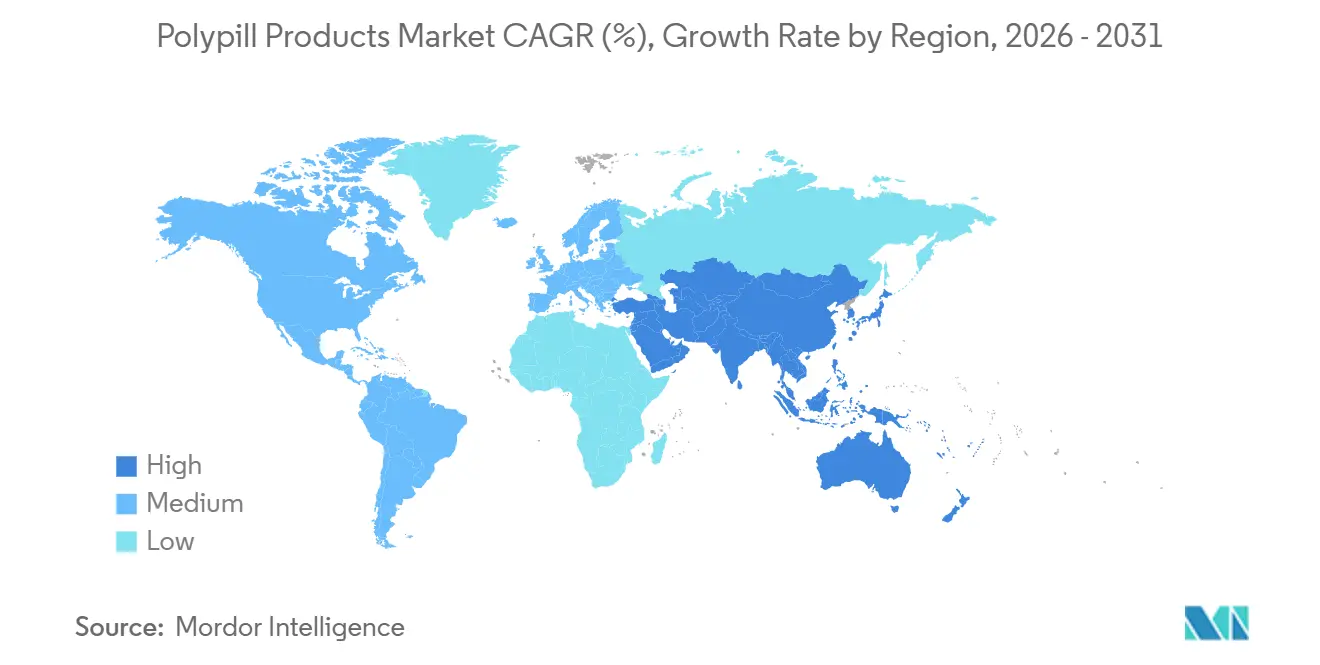

Asia Pacific is set to post a 6.27% CAGR through 2031, the strongest among major regions. China’s volume-based procurement requires public hospitals, which account for about 70% of national drug sales, to obtain at least 60% of their volume from winning bidders at prices up to 90% below prior benchmarks. India’s Production Linked Incentive scheme reserves tenders for local firms, thereby helping Cipla, Dr. Reddy’s, and Sun Pharma scale up multi-parameter formulations. Japan and South Korea have trimmed co-payments on approved polypills, lifting prescription counts within a year of the policy change. Australia lags because its Pharmaceutical Benefits Scheme has not yet listed triple-therapy tablets, restricting uptake to private payers.

Europe, the Middle East & Africa, and South America together form the remainder. Grupo Ferrer’s Trinomia is now approved in multiple European nations, moving the competitive needle beyond single-parameter tablets. Germany’s IQWiG and the UK’s NICE both factor in adherence gains in their QALY models, making reimbursement more favorable for fixed-dose combinations. Sub-Saharan Africa and parts of Latin America benefit from donor-backed access programs that ship at USD 0.10 per day, yet distribution costs still rise in humidity-prone Zone IVb climates, where moisture-barrier blisters are mandatory.

Competitive Landscape

Market structure is moderately concentrated. Innovators such as Abbott, Grupo Ferrer, George Medicines, and Novartis compete in OECD markets where clinical differentiation and branded positioning matter. Indian generics—Cipla, Dr. Reddy’s, Lupin, Sun Pharma—and global generics like Viatris and Teva dominate tender-driven LMIC procurement on razor-thin margins. Abbott’s Polycap retains India formulary slots but now faces local copies priced 40% lower. George Medicines secured the first U.S. approval for a triple antihypertensive polypill in half a decade, giving it a head start while patent shields last. Grupo Ferrer leads Europe’s multi-parameter rollout with Trinomia, leveraging real-world data to secure reimbursement above separate-pill bundles.

Strategy diverges by geography. In China and India, suppliers chase large tenders that guarantee volume but cap prices. In North America and Europe, companies bankroll head-to-head trials to win cost-per-QALY arguments. Sanofi, Pfizer, and Bristol Myers Squibb deploy cost-plus programs across 102 LMICs, building goodwill and eventual brand recognition. Emerging disruptors focus on multilayer tablet patents and 3D printing at the point of care. Equipment outlays near USD 150,000 and regulatory ambiguities currently confine printed polypills to well-funded academic centers.

Polypill Products Industry Leaders

AstraZeneca

Cadila Pharmaceuticals

Cipla, Inc.

Dr Reddy’s Laboratories

Johnson & Johnson (Janssen)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA approved Widaplik (telmisartan/amlodipine/indapamide), the first triple-combination polypill for initial hypertension treatment, marking a paradigm shift toward polypills as first-line therapy rather than salvage options for complex patients.

- May 2025: Merck entered exclusive licensing agreement with Jiangsu Hengrui Pharmaceuticals for HRS-5346, an investigational oral lipoprotein(a) inhibitor, expanding the competitive landscape for novel cardiovascular targets beyond traditional polypill components.

- March 2025: South Korea's Ministry of Food and Drug Safety approved NUVOROZET, a four-component cardiovascular polypill combining telmisartan, rosuvastatin, amlodipine, and ezetimibe, demonstrating regulatory acceptance of comprehensive combination approaches in Asian markets.

- March 2025: AstraZeneca's AZD0780 oral PCSK9 inhibitor demonstrated 50.7% LDL cholesterol reduction in PURSUIT Phase IIb trial, with 84% of participants achieving target levels compared to 13% on statins alone, advancing next-generation polypill component development.

Global Polypill Products Market Report Scope

As per the scope of the report, polypill products are a fixed-dose combination of several other combinations of drugs targeting different parameters of the disease.

The Polypill Products Market Report is Segmented by Product Type (Single-Parameter Polypills, Multi-Parameter Polypills), Application (Cardiovascular Disease Prevention, Diabetes-linked CV Risk Reduction, Other Therapeutic Areas), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Single-Parameter Polypills |

| Multi-Parameter Polypills |

| Cardiovascular Disease Prevention |

| Diabetes-linked CV Risk Reduction |

| Other Therapeutic Areas |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single-Parameter Polypills | |

| Multi-Parameter Polypills | ||

| By Application | Cardiovascular Disease Prevention | |

| Diabetes-linked CV Risk Reduction | ||

| Other Therapeutic Areas | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the polypill products market?

The polypill products market size is USD 34.18 billion in 2026.

Which product segment is growing faster than the overall market?

Multi-parameter formulations are rising at a 3.06% CAGR, outpacing the 2.58% overall rate.

Why are online pharmacies gaining share?

Digital platforms bundle teleconsultation, auto-refill, and SMS reminders, lifting adherence and driving a 5.18% CAGR for the online channel.

How do LMIC procurement programs affect pricing?

Volume-based tenders in China and India push prices 70%–90% below pre-tender levels, boosting access while compressing margins.

Which recent regulatory shift favors 3D-printed polypills?

The UK’s 2025 Modular Manufacture and Point of Care Regulations permit on-site printing under centralized pharmacovigilance.

Page last updated on: