Biomaterials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

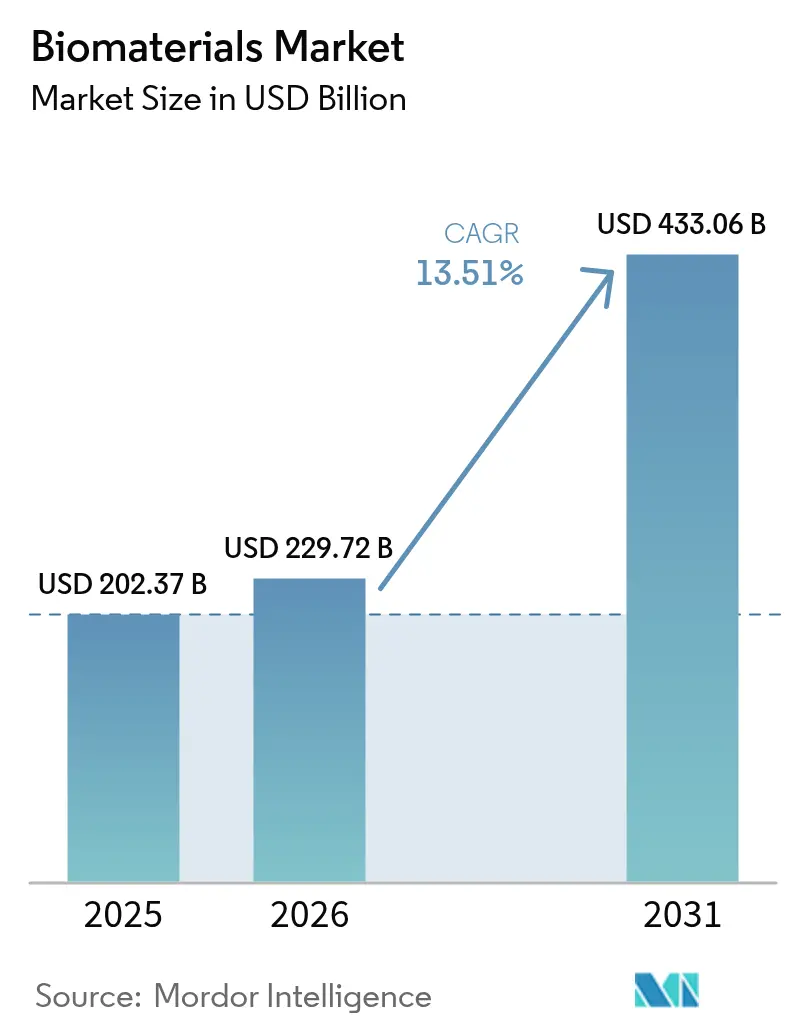

| Market Size (2026) | USD 229.72 Billion |

| Market Size (2031) | USD 433.06 Billion |

| Growth Rate (2026 - 2031) | 13.51% CAGR |

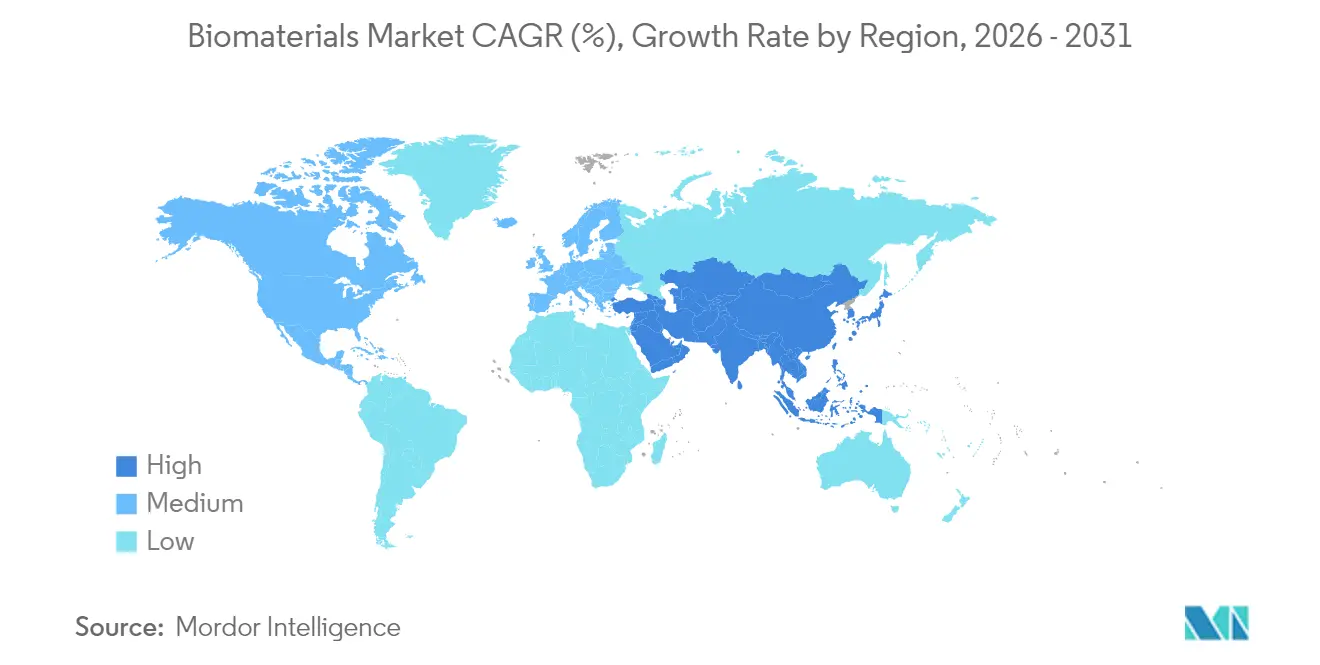

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomaterials Market Analysis by Mordor Intelligence

Biomaterials Market size in 2026 is estimated at USD 229.72 billion, growing from 2025 value of USD 202.37 billion with 2031 projections showing USD 433.06 billion, growing at 13.51% CAGR over 2026-2031.

Growth gathers momentum from aging‐driven procedure volumes, rapid regenerative medicine breakthroughs, and streamlined regulatory pathways. Polymeric materials keep demand buoyant thanks to their adaptability in cardiovascular stents and orthopedic inserts, while waste-derived natural materials expand quickly as circular-economy mandates intensify. North America benefits from 1,041 FDA breakthrough device designations that de-risk commercialization, yet Asia-Pacific outpaces with double-digit growth backed by China’s fivefold rise in knee replacements and Japan’s induced-pluripotent-stem-cell (iPSC) innovations. Strategic acquisitions—such as Enovis’ EUR 800 million purchase of LimaCorporate—underscore vertical-integration moves aimed at buffering raw-material shortages and EU MDR compliance bottlenecks[1]Source: Enovis Corporation, “Enovis Completes Acquisition of LimaCorporate,” enovis.com .

Key Report Takeaways

- By material type, polymeric materials led with 40.15% of biomaterials market share in 2024, while natural biomaterials are projected to post the fastest 14.67% CAGR to 2030.

- By origin, synthetic biomaterials accounted for 70.60% of the biomaterials market size in 2024; natural counterparts expand at a 14.84% CAGR through 2030.

- By application, orthopedics captured 38.27% of biomaterials market size in 2024, while tissue engineering and regenerative medicine record the highest 15.01% CAGR to 2030.

- By geography, North America retained 42.23% biomaterials market share in 2024; Asia–Pacific is set to chart the fastest 15.19% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biomaterials Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population-led surge in joint-replacement volumes | +3.2% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Rapid advances in regenerative medicine & 3-D bioprinting | +2.8% | North America & EU leading, APAC catching up | Medium term (2-4 years) |

| Expansion of cardiovascular interventions using bio-stents | +2.1% | Global, with emerging market acceleration | Medium term (2-4 years) |

| Government R&D grants and fast-track approvals for breakthrough implants | +1.9% | North America & EU primarily | Short term (≤ 2 years) |

| Emergence of 4-D stimuli-responsive biomaterials | +1.4% | North America & EU research hubs | Long term (≥ 4 years) |

| Circular-bioeconomy push for waste-derived natural biomaterials | +1.1% | EU leading, global adoption following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging population-led surge in joint-replacement volumes

Primary knee arthroplasty volumes in the United States alone are projected to climb 673% by 2030, and Germany anticipates a 55% rise in knee arthroplasties by 2040. Younger and more active patients now represent a majority of candidates, forcing implant developers to prioritize wear resistance and osseointegration longevity. Colombia projects 39,270 lower-limb arthroplasties by 2050, 52.7% of which will involve women, spurring gender-specific biomaterial formulations. The sustained procedure pipeline cushions the biomaterials market against traditional healthcare spending cycles.

Rapid advances in regenerative medicine & 3-D bioprinting

The Canadian government’s CAD 72.75 million grant to Aspect Biosystems signals policy confidence in bioprinted tissues, while machine-learning-driven modelling achieves R² > 0.999 for shape predictions in 4D scaffolds. FDA clearance of Symvess, the first acellular tissue-engineered vessel, establishes precedent and accelerates clinical translation. As regulatory clarity improves, venture activity spreads to Asia–Pacific, where Japan’s iPSC-based corneal epithelial transplants underscore regional competitiveness, further strengthening the biomaterials market outlook.

Expansion of cardiovascular interventions using bio-stents

Biodegradable platforms are displacing permanent metallic stents by mitigating late thrombosis, and tantalum-niobium alloys enable precise 3-D printed, patient-specific devices. Teleflex’s EUR 760 million purchase of BIOTRONIK’s vascular arm validates growth prospects for drug-coated balloons and resorbable scaffolds. Coupled with predictive degradation modelling, developers can fine-tune stent lifecycles, compressing time-to-market and reinforcing the biomaterials market trajectory.

Government R&D grants and fast-track approvals for breakthrough implants

The FDA’s Breakthrough Devices Program has conferred 1,041 designations, 128 of which have secured marketing authorization, sharply reducing commercialization risk. NIH bioengineering grants and RMAT pathways funnel capital into orthopedic and cardiovascular implants. Early adopters such as Amphix Bio and Renovos leverage these mechanisms to speed orthopedic graft alternatives into clinics, bolstering innovation pipelines across the biomaterials market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production & surgical costs of next-gen biomaterials | -2.3% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Lengthy multi-phase regulatory & clinical validation timelines | -1.8% | Global, with EU MDR creating additional complexity | Long term (≥ 4 years) |

| Supply-chain volatility for specialty alloying elements (e.g., Nb, Ta) | -1.5% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Environmental scrutiny over synthetic-polymer leachables | -0.9% | EU leading, North America following, global adoption expected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production & surgical costs of next-gen biomaterials

Inflation and supply chain shocks inflated contract manufacturing costs during 2024, while polytetrafluoroethylene shortages forced insourcing and inventory stockpiling, impairing cash flow for small device makers. Tantalum prices climbed to USD 5,190 per kg in 2023, tightening margins for specialty implant suppliers. EU MDR compliance adds 18–24 months and significant certification costs, prompting 50% of surveyed European firms to trim portfolios.

Lengthy multi-phase regulatory & clinical validation timelines

Only 4,873 MDR certificates were issued against 14,539 applications in 2023, creating a backlog that limits new product launches and risks device shortages in Europe. Academic labs struggle with quality-management adaptation, while the FDA’s expanded chemical-analysis guidance lengthens U.S. biocompatibility testing cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polymeric Strength Meets Natural Disruption

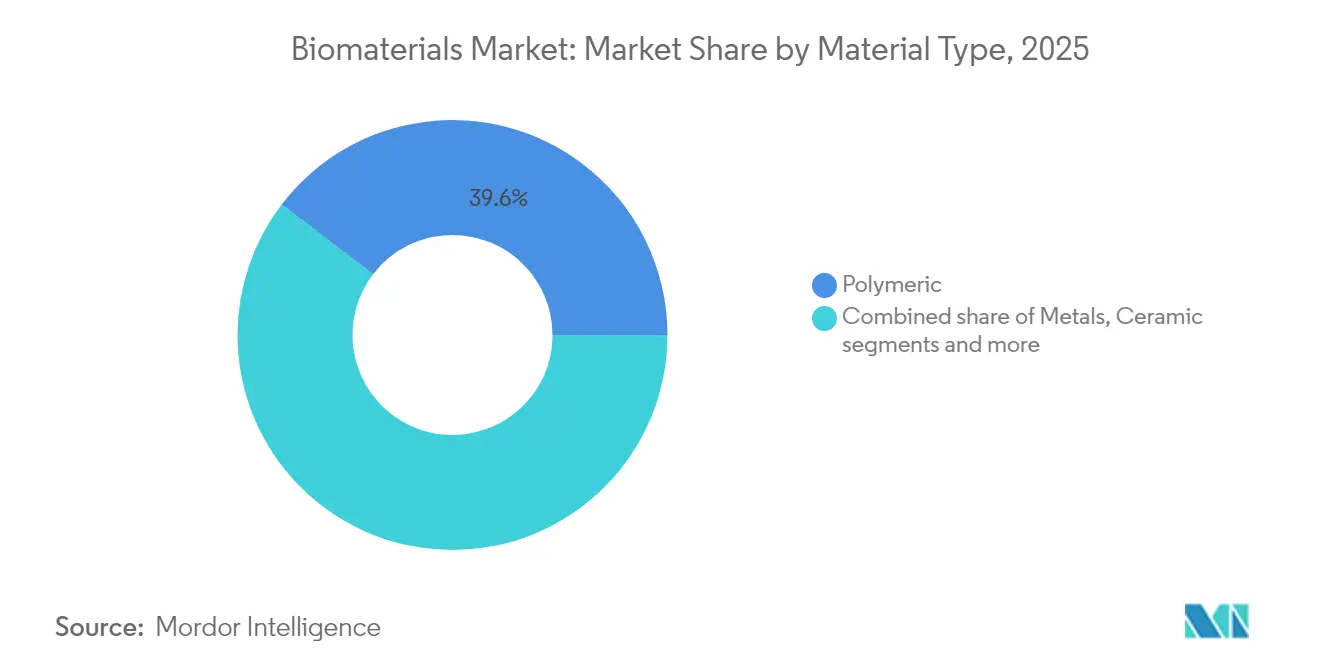

Polymeric materials retained a 39.62% share of the biomaterials market in 2025, dominating cardiovascular and orthopedic uses. Fish-waste collagen and insect-derived chitosan speed n atural-material uptake, driving a 14.52% CAGR that challenges polymeric supremacy. Composite hybrids marry metallic strength with polymeric elasticity, meeting load-bearing preferences in younger arthroplasty patients. Shape-memory polymers produced via 4D printing enable scaffolds that conform in vivo, a differentiator for tissue-engineering firms seeking reimbursement premiums.

Natural candidates also benefit from EU circular-economy incentives, accelerating collagen extraction from sardine scales and upcycling crustacean waste. Metallic biomaterials, though vulnerable to tantalum-and-niobium supply risks, remain indispensable in hip prostheses demanding high fatigue resistance. The biomaterials market continues to reward suppliers able to hedge raw-material volatility through recycling and dual-sourcing strategies.

By Origin: Synthetic Dominance Faces Sustainable Momentum

Synthetic materials accounted for 70.05% of biomaterials market size in 2025 thanks to well-established production and predictable performance. However, natural alternatives are expanding at a 14.71% CAGR on the back of precision-fermentation collagen, biobased polymers, and bacterial cellulose hydrogels that achieve comparable mechanical integrity. Regulatory scrutiny of synthetic-polymer leachables is nudging developers toward bio-based substitutes, particularly in pediatric and long-term implants.

Synthetic innovators focus on biodegradable poly-lactic-co-glycolic acid and polyhydroxyalkanoates that resorb safely, shielding margins against potential bans on persistent polymers. Natural newcomers leverage patents in lignocellulosic biomass conversion, turning forestry residues into medical-grade nanofibers, widening supplier diversity and tempering synthetic price power.

By Application: Orthopedic Lead Challenged by Regenerative Upswing

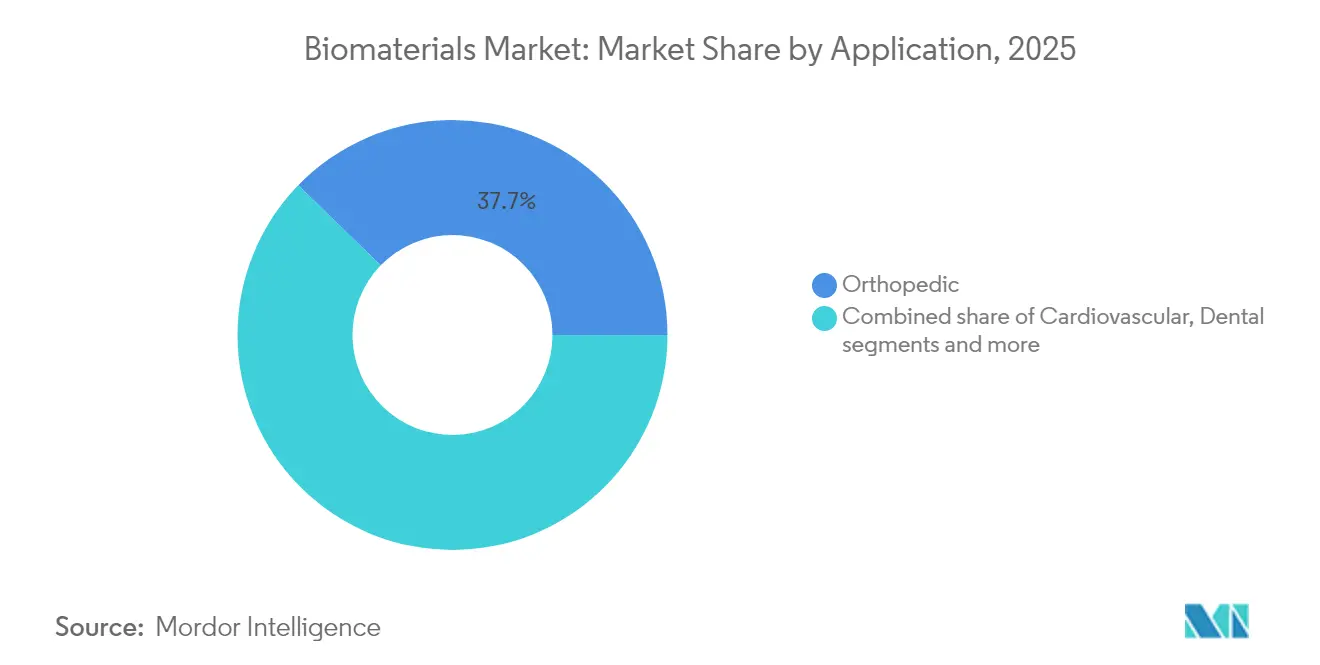

Orthopedic devices captured 37.74% of biomaterials market size in 2025, supported by record hip-and-knee volumes. Yet tissue engineering and regenerative medicine post the strongest 14.86% CAGR, as FDA approvals such as Symvess and local iPSC corneal grafts validate biological substitutes. Cardiovascular segments accelerate through bio-stents, and dental players deploy 3-D printing for chair-side crowns, shortening treatment cycles.

Plastic-surgery and neurology fields emerge as next-wave adopters, integrating bioresorbable meshes and neural-interface polymers that limit inflammation. Wound-healing solutions combine antimicrobial peptides with hydrogel matrices to tackle diabetic ulcers prevalent in aging populations. Overall, diversified clinical pipelines cushion the biomaterials market against single-segment reliance.

Geography Analysis

North America held 41.78% of biomaterials market share in 2025, buoyed by 1,041 FDA breakthrough designations and heavy corporate R&D. Established reimbursement and robust surgeon training programs encourage rapid adoption of premium implants signals federal backing for bioprinting ventures.

Europe grapples with MDR bottlenecks—only 4,873 certificates were issued from 14,539 applications in 2023—delaying launches and prompting some manufacturers to withdraw legacy devices. Despite this, Germany expects knee-replacement incidence to climb 55% by 2040, guaranteeing demand once compliance hurdles ease. EU circular-bioeconomy grants also fast-track insect-derived chitosan plants, giving natural materials an early-mover edge.

Asia–Pacific charts the fastest 15.03% CAGR, propelled by China’s fivefold jump in knee replacements and Japan’s first-in-human iPSC corneal transplants. Even with venture funding down 22% from 2021 highs, the region’s medtech sector still targets USD 225 billion in 2030 revenue, encouraging global OEMs to localize manufacturing. South Korea and Australia add capacity through advanced composite printing hubs, while India’s growing middle class amplifies volume demand for cost-efficient implants.

Competitive Landscape

Consolidation is accelerating as firms secure raw-material pipelines and regulatory expertise. Enovis acquired LimaCorporate for EUR 800 million, adding 3-D printed Trabecular Titanium know-how and lifting its reconstruction revenue target to USD 1 billion. Teleflex’s EUR 760 million takeover of BIOTRONIK’s vascular arm expands its interventional cardiology reach amid rising resorbable-scaffold demand[2]Source: Teleflex Incorporated, “Teleflex to Acquire BIOTRONIK’s Vascular Intervention Business,” teleflex.com.

Innovation advantages accrue to companies harnessing 4D printing and machine-learning optimisation. Stryker logged 11.9% net-sales growth in Q1 2025, bolstered by record Mako robotic-system installations. Zimmer Biomet’s FDA-cleared cementless partial knee underpins its foot-and-ankle diversification, following the Paragon 28 buyout. Smaller innovators exploit regulatory fast-tracks—Curiteva’s trabecular PEEK interbody system won 510(k) clearance, showcasing additive-manufactured polymer potential.

White-space niches surface in biodegradable photopolymers and smart materials that adjust to body temperature or pH, where university spin-outs partner with OEMs for scaled production. Meanwhile, supply-chain resilience is a focal point; U.S. import dependence on Brazilian tantalum raises concerns as China increases its Latin-American influence. Integrated majors able to multi-source or recycle critical metals fortify their strategic positions in the biomaterials market.

Biomaterials Industry Leaders

Koninklijke DSM N.V.

Corbion NV

Noble Biomaterials, Inc.

Dentsply Sirona

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Zimmer Biomet completed its Paragon 28 takeover to cement presence in the USD 5 billion foot-and-ankle niche.

- February 2025: Teleflex acquired BIOTRONIK’s vascular intervention unit for EUR 760 million, adding drug-coated balloons and resorbable scaffolds.

Global Biomaterials Market Report Scope

As per the scope of the report, biomaterials are substances that have been engineered to interact with biological systems for a medical purpose, either a therapeutic (treat, augment, repair, or replace a tissue function of the body) or a diagnostic one.

The biomaterials market is segmented by type of biomaterial (natural biomaterial, metallic biomaterial, ceramic biomaterial, and polymeric biomaterial), application (neurology, cardiology, orthopedics, ophthalmology, wound care, dental, plastic surgery, and other applications), and geography (North America, Europe, South America, Asia-Pacific and the Middle East and Africa). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (USD) for all the above segments.

| Metals |

| Polymeric |

| Ceramic |

| Composite |

| Natural |

| Synthetic |

| Natural |

| Orthopedic |

| Cardiovascular |

| Dental |

| Wound Healing |

| Neurology |

| Plastic Surgery |

| Tissue Engineering & Regeneration |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Metals | |

| Polymeric | ||

| Ceramic | ||

| Composite | ||

| Natural | ||

| By Origin | Synthetic | |

| Natural | ||

| By Application | Orthopedic | |

| Cardiovascular | ||

| Dental | ||

| Wound Healing | ||

| Neurology | ||

| Plastic Surgery | ||

| Tissue Engineering & Regeneration | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the biomaterials market?

The Biomaterials Market size is USD 229.72 billion in 2026 and is projected to reach USD 433.06 billion by 2031 at a 13.51% CAGR.

Which segment holds the largest share in the biomaterials market?

Polymeric materials led with 39.62% biomaterials market share in 2025, mainly due to cardiovascular and orthopedic applications.

Which region is growing the fastest?

Asia–Pacific posts the highest 15.03% CAGR through 2031 because of China’s rising joint-replacement volumes and Japan’s regenerative-medicine advances.

What are the main growth drivers for the biomaterials industry?

Key drivers include aging demographics, breakthroughs in regenerative medicine and bioprinting, expanding cardiovascular interventions, and supportive fast-track regulatory programs.

How is regulation affecting biomaterials commercialization in Europe?

EU MDR implementation has generated certificate backlogs, with only 4,873 approvals out of 14,539 applications in 2023, delaying product launches and increasing compliance costs.

Page last updated on: