Medical Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

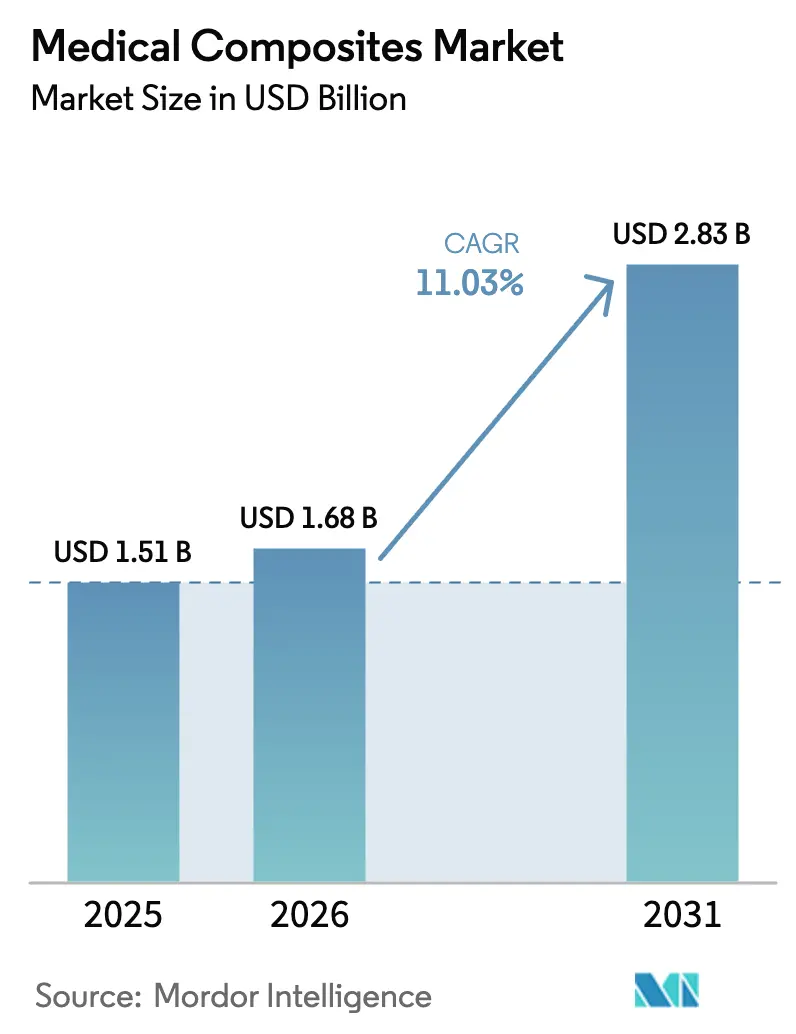

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.83 Billion |

| Growth Rate (2026 - 2031) | 11.03% CAGR |

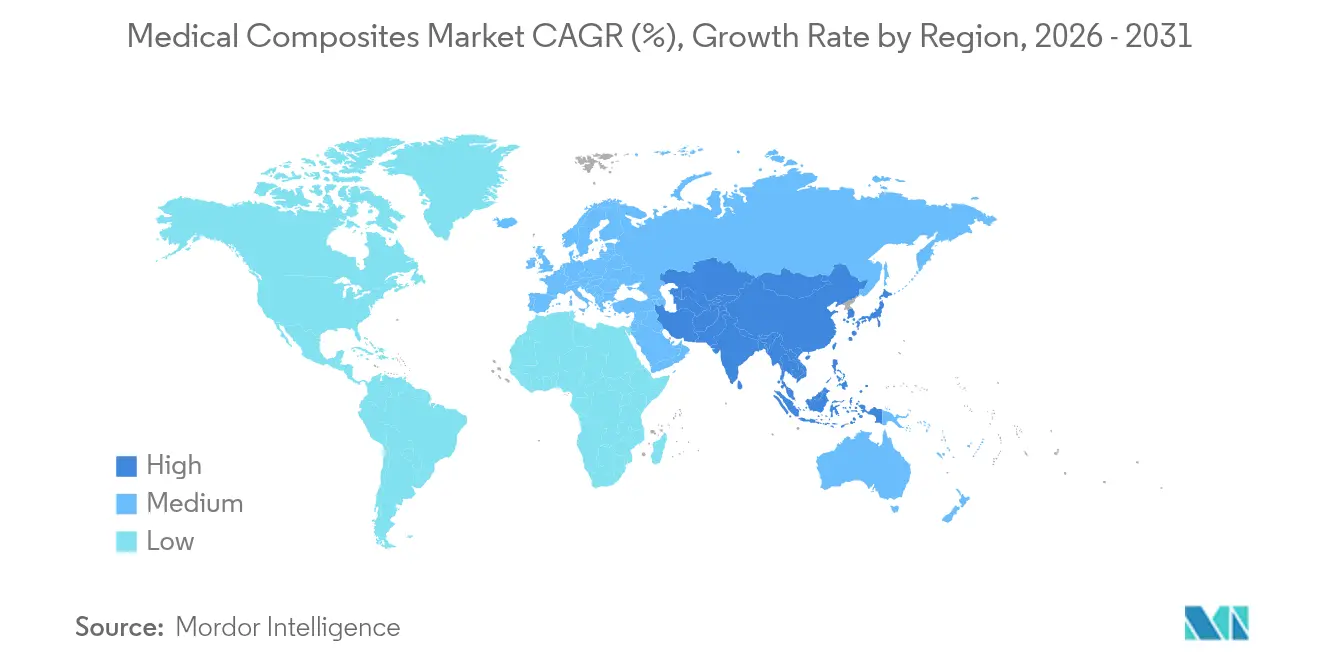

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Composites Market Analysis by Mordor Intelligence

Medical Composites Market size in 2026 is estimated at USD 1.68 billion, growing from 2025 value of USD 1.51 billion with 2031 projections showing USD 2.83 billion, growing at 11.03% CAGR over 2026-2031.

Population aging, fast-tracked regulatory clearances for carbon-fiber PEEK implants, and a device industry pivot toward lightweight, MRI-compatible materials collectively fuel demand. Device makers gain clear clinical advantages from enhanced diagnostic visibility, lower instrument mass, and higher fatigue resistance in long-term implants, prompting hospitals to specify composites for next-generation systems. Rising procedure volumes for minimally invasive and robot-assisted surgeries keep order pipelines full, while additive manufacturing unlocks cost-effective customization. Continuous material R&D especially in bioactive ceramics broadens the addressable application pool, amplifying revenue streams across global supplier networks.

Key Report Takeaways

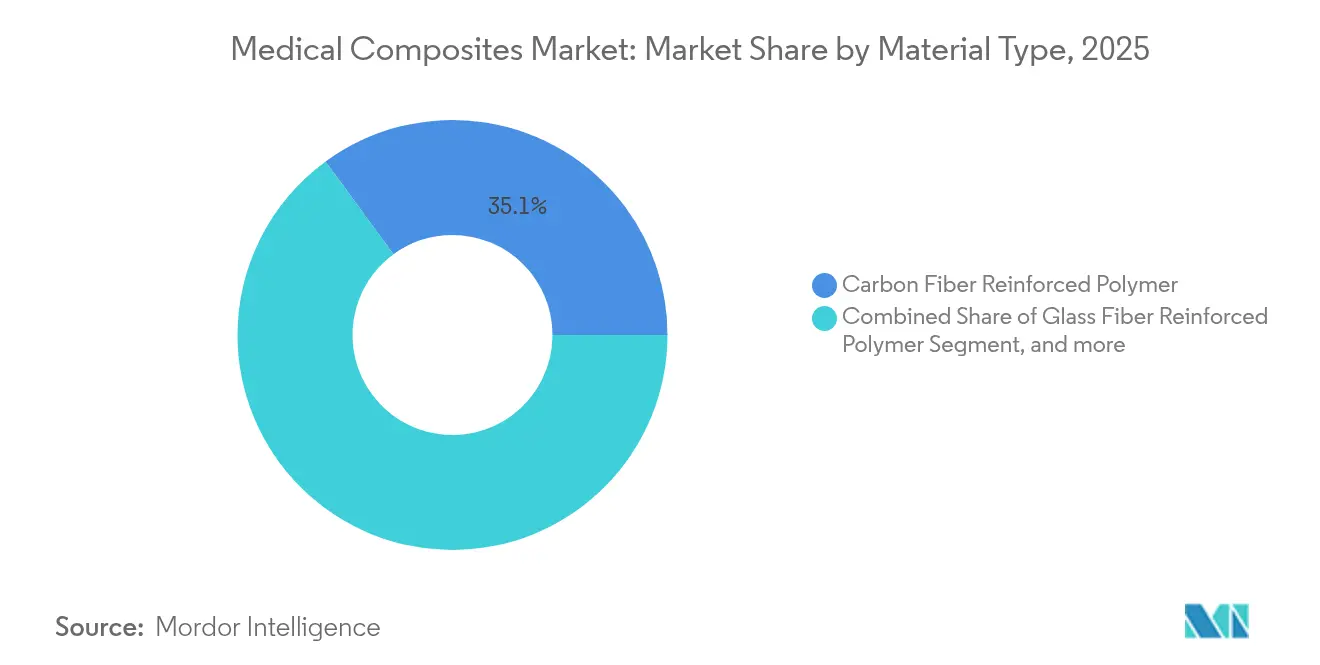

- By material type, carbon fiber reinforced polymer led with 35.05% of the medical composites market share in 2025, whereas ceramic matrix composites are forecast to expand at a 11.73% CAGR through 2031.

- By polymer matrix, PEEK held 41.22% share of the medical composites market size in 2025, while PMMA & acrylics are projected to advance at 12.95% CAGR between 2026-2031.

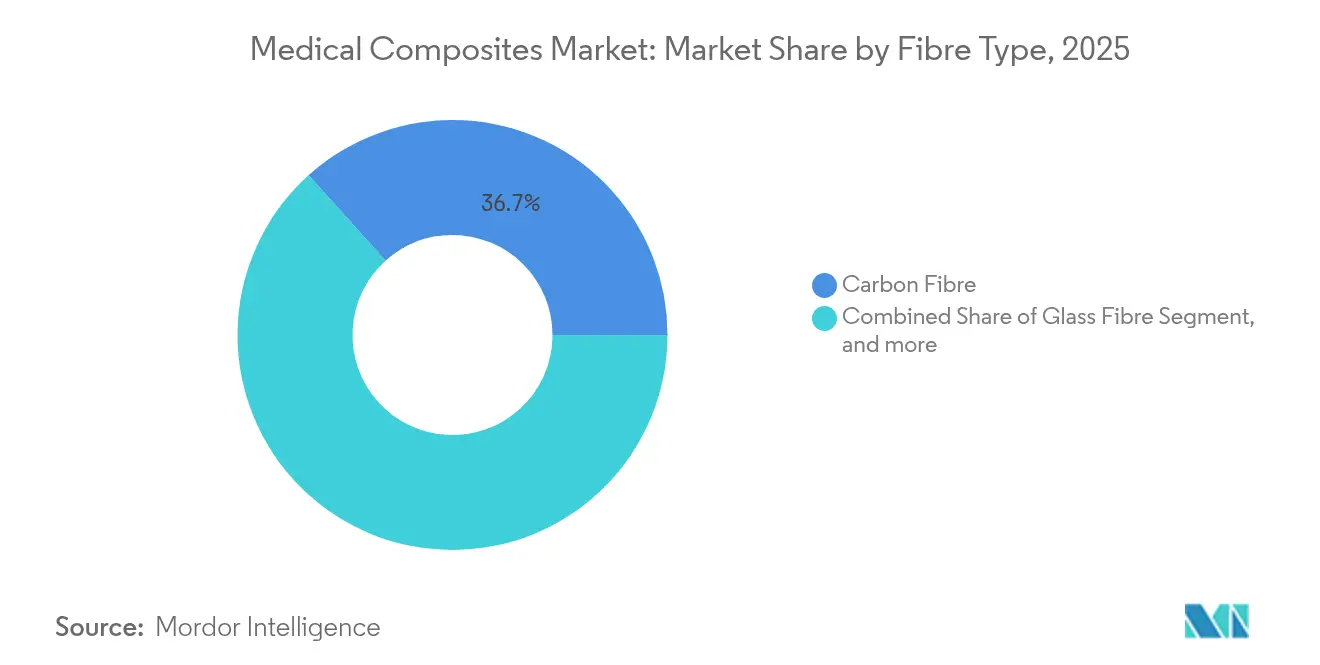

- By fibre type, carbon fibre commanded 36.68% share in 2025; aramid & other high-performance fibres are poised for the fastest 13.42% CAGR to 2031.

- By application, diagnostic imaging components accounted for 32.15% of the medical composites market size in 2025 and tissue engineering scaffolds are moving ahead at 14.9% CAGR through 2031.

- By geography, North America dominated with 41.10% share in 2025, while Asia-Pacific is forecast to post a 11.98% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging chronic disease burden & aging population | +2.8% | North America, Europe | Long term (≥ 4 years) |

| Growing demand for lightweight, MRI-compatible tools | +2.1% | North America, EU, APAC | Medium term (2-4 years) |

| Advancements in minimally invasive & robotic surgery devices | +1.9% | North America, APAC | Medium term (2-4 years) |

| Rapid adoption of robot-assisted composite instruments | +1.6% | North America, EU, APAC | Short term (≤ 2 years) |

| Regulatory fast-track for carbon-fiber PEEK implants | +1.4% | North America, EU | Short term (≤ 2 years) |

| Expansion of diagnostic imaging infrastructure | +1.2% | APAC, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Chronic Disease Burden & Aging Population

Orthopedic surgeons increasingly prefer composite implants because carbon fiber’s fatigue resistance outperforms titanium, lowering revision rates for elderly patients. The demographic surge strengthens long-term demand visibility, encouraging suppliers to scale capacity and pursue wider indications. Tissue engineering scaffolds benefit as clinicians adopt bio-resorbable lattices that obviate secondary removal surgeries. Composite producers respond by tailoring degradation profiles and surface chemistries that promote osteointegration. Insurance payors, under pressure to cut re-operation costs, further validate composite solutions, tightening hospital formularies around proven, durable materials. Consequently, the medical composites market registers steady procurement even during broader economic slowdowns.

Growing Demand for Lightweight, MRI-Compatible Tools

Radiolucent composites remove image artifacts, letting surgeons monitor implant placement in real time across fluoroscopy, CT, and MRI suites.[1]3D Systems, “FDA Clears VSP Cranial Implant,” 3dsystems.com Lower instrument weight reduces intra-operative fatigue, trimming procedure times and enhancing patient outcomes. Hospitals standardize composite imaging tables and positioning systems to guarantee uniform quality across modalities. Robotics vendors adopt carbon-fiber joints to sharpen kinematic accuracy while keeping payloads manageable for precision drive units. As reimbursement models reward efficiency, healthcare providers increasingly specify MRI-compatible composite sets, widening the installed base and locking in recurring replacement sales.

Advancements in Minimally Invasive & Robotic Surgery Devices

Composite shafts and end-effectors bring high stiffness and low mass, critical for robotic arms performing delicate cardiac and neurological interventions.[2]CompositesWorld, “Carbon Fiber Use in Medical Robotics,” compositesworld.com Automated fiber placement enables intricate geometries unattainable with machined metal, allowing single-use laparoscopic tools that hit target cost thresholds. As OEMs integrate haptic sensors directly into composite lay-ups, surgeons gain real-time tactile feedback without compromising sterilization cycles. Regulatory filings for robot-ready composite disposables climbed sharply in 2024, indicating commercial readiness. The resulting throughput boost at ambulatory surgery centers reinforces the medical composites market growth trajectory.

Rapid Adoption of Robot-Assisted Composite Instruments

Embedded fiber-optic arrays inside composite grippers feed force data to control algorithms, enhancing precision during soft-tissue manipulation.[3]Boyd Biomedical, “Sensor-Enabled Composite Surgical Instruments,” boydbiomedical.com Material biocompatibility passes stringent cytotoxicity screens, supporting direct tissue contact across multiple reuse cycles. Automated lay-up processes shrink unit costs, enabling broader specialty adoption beyond flagship robotic platforms. Customizable modulus profiles within a single part allow differential flex, matching anatomical contours while retaining structural safety margins. The pace of design iterations accelerates as digital twin simulations predict composite performance, driving swift regulatory submissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs & limited supply chain depth | -1.8% | Global | Medium term (2-4 years) |

| Stringent multi-region regulatory approvals | -1.2% | North America, EU | Long term (≥ 4 years) |

| End-of-life recycling challenges for composite devices | -1.5% | Europe, North America, APAC | Long term (≥ 4 years) |

| Machining & sterilization complexity | -0.9% | Manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Costs & Limited Supply Chain Depth

Medical-grade carbon fiber commands a premium because only a handful of producers meet ISO 13485 documentation and purity thresholds. Autoclave and laser-machining assets involve high capital outlays, raising entry barriers for new entrants. Disruptions in precursor supply ripple across implant lines, with lead times stretching past 24 weeks during 2024 aerospace demand spikes. OEMs mitigate by dual-sourcing fibers and investing in in-house prepreg lines, yet cost pass-throughs persist, restraining adoption in price-sensitive emerging markets.

Stringent Multi-Region Regulatory Approvals

Composite formulations rarely enjoy predicate equivalence, forcing full biocompatibility dossiers in each jurisdiction. European MDR rules mandate clinical data for class III composite implants, prolonging validation cycles. SMEs divert R&D capital to protocol compliance, decelerating pipeline breadth. Post-market surveillance obligations add operating overhead, impacting cash flow during scale-up. Convergence efforts under IMDRF remain incomplete, leaving multi-year uncertainty for globally oriented device brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: CFRP Dominance Drives Innovation

CFRP commanded 35.05% of the medical composites market in 2025, substantiating its role as the backbone of imaging tables, orthopedic plates, and robotic arm components. The segment benefits from unmatched strength-to-weight ratios that allow thinner profiles without sacrificing load tolerance. Imaging OEMs capitalize on CFRP’s radiolucency to achieve artifact-free scans, widening its institutional footprint. Meanwhile, the medical composites market size for ceramic matrix composites is projected to advance at a 11.73% CAGR, propelled by bioactivity that accelerates osteointegration. Development programs pair hydroxyapatite-infused ceramics with resorbable polymers, offering hybrid constructs that knit gradually with host tissue. Production cost curves trend downward as pressureless sintering and microwave sintering reduce cycle times. Hybrid and bio-based composites linger in early-stage trials, yet targeted properties such as antimicrobial efficacy attract clinical attention.

CFRP suppliers deploy automated fiber placement to curtail scrap rates and drive consistent mechanical performance batch-to-batch. Hospitals value the reduced infection risk linked to CFRP’s chemical inertness, while insurers flag lower re-operation incidence in postoperative audits. Ceramic matrix innovators leverage additive manufacturing to print lattice structures that match patient-specific defect geometries, shortening operating room time. As surgical robotics shifts toward smaller, outpatient-compatible systems, lightweight ceramic-carbon hybrids offer the stiffness surgeons expect. This evolving material mix ensures the medical composites market retains a robust innovation funnel.

By Polymer Matrix: PEEK Leadership Faces PMMA Challenge

PEEK held 41.22% share in 2025, its elastic modulus mirroring cortical bone and thereby mitigating stress-shielding after implantation. Surgeons prefer PEEK cages for spinal fusion because post-operative imaging clearly distinguishes bone growth around the implant. The medical composites market size expansion for PMMA & acrylics, set for 12.95% CAGR, rests on dental and vertebroplasty demand where low cost and flowable curing matter. Antimicrobial PMMA bone cements containing silver ions are clearing clinical pathways, aiding infection control. Polypropylene retains niche use in catheter components needing chemical resistance at low budgets.

Advances in extrusion-based 3D printing broaden PEEK implant geometries, supporting porous architectures that invite tissue in-growth. Composite matrix developers now blend PEEK with carbon nanotubes to elevate thermal conductivity, facilitating RF ablation probes. PMMA innovators experiment with bioactive glass microspheres to couple radiopacity with controlled elution of therapeutic ions. Regulatory bodies call for robust leachables data, pushing polymer formulators to refine additive packages carefully. The resulting competition ensures that the medical composites market continues to diversify matrix offerings without compromising safety.

By Fibre Type: Carbon Fibre Strength Meets Aramid Innovation

Carbon fibre captured 36.68% of the medical composites market share in 2025, owing to its high modulus of 230 GPa and compatibility with sterilization via gamma irradiation. Its dominance spans robotic struts, external fixation rods, and operating-room furniture. Aramid fibres, forecast at 13.42% CAGR, entice wound-care firms for antibacterial dressings and implantable meshes. Glass fibre remains the economical workhorse in single-use scopes and infusion pump housings, where rigid strength tops imaging visibility.

Surface-sized carbon fibres bond tightly with PEEK matrices, minimizing delamination risk during cyclical spinal loading. Aramid’s intrinsic toughness resists impact damage, suiting trauma plates exposed to abrupt forces. Researchers coat aramid yarns with chitosan to enhance cell adhesion, a breakthrough that extends its relevance to regenerative scaffolds. Hybrid lay-ups combining carbon and aramid enable tailored stiffness gradients, meeting orthopedic demands for proximal flexibility and distal rigidity. Together these developments reinforce the medical composites industry’s ability to customize mechanical response.

By Application: Imaging Components Lead, Tissue Engineering Accelerates

Diagnostic imaging components held 32.15% share in 2025, proof that radiolucent composites sit at the center of modern radiography suites. Carbon-fiber tabletops support up to 250 kg loads while attenuating X-rays by less than 1 mm aluminum equivalence, boosting detector sensitivity. Hospitals equip angiography rooms with composite C-arm covers to maintain clear fluoroscopic views. Simultaneously, the medical composites market size allocated to tissue engineering scaffolds is on track for 14.9% CAGR, spurred by bioresorbable lattices that deliver stem cells and growth factors directly at defect sites. As payors reimburse regenerative therapies, scaffold demand scales beyond academic centers into mainstream orthopedics.

Composite surgical instruments continue upward adoption as OR managers target instrument sets that combine durability with ergonomic lightness. Orthopedic implants see renewed interest in carbon-PEEK nails and plates capable of real-time monitoring via integrated strain sensors. Dental clinicians move to composite abutments that blend with enamel, pleasing cosmetic dentistry clients. Drug-delivery reservoirs, molded from PEEK-carbon blends, achieve dose control accuracy within 3%, making them prime candidates for implantable infusion pumps. Collectively, applications illustrate how the medical composites market marries performance with clinical utility.

Geography Analysis

North America secured 41.10% of the medical composites market in 2025, underpinned by a robust reimbursement ecosystem and continuous R&D investments from players such as 3M and Stryker. The United States accounts for the lion’s share, coupling early technology adoption with large-scale hospital networks that standardize composite instrument trays. Canada, leveraging its single-payer system, funds procurement of advanced MRI-compatible tables to cut wait times. Mexico’s maquiladora corridor attracts device OEMs seeking cost-optimized composite component production while remaining proximate to US regulatory oversight. Federal funding for orthopedic research sustains pipeline momentum, preserving North American leadership.

Asia-Pacific registers the fastest 11.98% CAGR through 2031, a testament to expanded health insurance coverage, burgeoning middle-class demand, and concerted industrial policies in China and India. Chinese composite producers benefit from state incentives that lower precursor import tariffs, boosting domestic supply capacity. Japan integrates composites into surgical robotic exports, reinforcing the region’s high-tech image. India’s National Medical Devices Policy 2025 encourages local manufacture of carbon-fiber implants, targeting reduced import dependencies. Southeast Asian nations invest in radiotherapy centers, each specifying carbon-epoxy patient couches, further swelling regional uptake across the medical composites market.

Europe retains a mature yet innovative profile, with stringent MDR rules nudging suppliers toward traceable, high-quality composite lines. Germany spearheads application engineering, embedding smart sensors into spinal rods for postoperative monitoring. The United Kingdom’s Catapult network supports SME trials of recyclable thermoplastic composites, aligning with National Health Service carbon-footprint mandates. France pilots hospital take-back programs for single-use composite devices, collecting lifecycle data critical to future regulatory relief. Italy’s Lombardy cluster ramps autoclave capacity, exporting orthopedic plates across the EU. Such coordinated initiatives keep Europe integral to technological progress even as growth moderates.

Competitive Landscape

The medical composites market remains moderately fragmented, with the top five suppliers holding significant market share and combined revenue, leaving room for nimble entrants. Material science giants like Toray Industries license aerospace-grade carbon fibre to medical molding houses, ensuring consistent throughput. Device specialists such as Victrex leverage proprietary PEEK compounds, bundling material and design services for OEM partners. Recent deal flow underscores consolidation: Integer Holdings acquired Precision Coating in January 2025 to vertically integrate surface treatments, expanding its share in orthopedic and cardiovascular composites. Similarly, DuPont’s 2024 purchase of Donatelle Plastics secured access to ISO 13485 injection-molding capacity, accelerating customized implant programs.

Competition intensifies in diagnostic imaging accessories where price parity pressures margins, prompting differentiation via antimicrobial topcoats or embedded RFID asset tracking. Meanwhile, tissue engineering scaffolds foster niche competition centered on bioactive additives and controlled porosity. R&D focus clusters on automated fiber placement, defect-detection AI, and low-temperature recycling of PEEK-carbon blends. Patent filings for composite sterilization techniques grew 18% year-on-year, indicating a race to streamline reprocessing without material degradation. Overall, strategic emphasis pivots toward life-cycle value propositions and sustainability to satisfy hospital procurement scorecards.

Medical Composites Industry Leaders

3M

Dentsply Sirona

Evonik Industries AG

Toray Industries Inc.

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: 3D Systems has achieved a groundbreaking milestone in the medical composites space by delivering the world’s first Medical Device Regulation (MDR)-compliant 3D-printed PEEK facial implant. In partnership with University Hospital Basel (Switzerland), the company enabled a successful patient-specific implant procedure using VESTAKEEP i4 3DF PEEK by Evonik, printed on the EXT 220 MED platform.

- September 2024: Nvision Biomedical Technologies, in collaboration with Invibio Biomaterial Solutions (a Victrex plc company), has announced FDA clearance for the world’s first 3D-Printed Interbody Fusion System constructed from PEEK-OPTIMA using Bond3D additive manufacturing. The jointly developed spinal solution includes Cervical and Anterior Lumbar Interbody Fusion (ALIF) devices engineered with advanced porous architectures designed to stimulate multi-directional bone ingrowth, optimize fixation, and preserve PEEK’s inherent imaging and biomechanical benefits.

Global Medical Composites Market Report Scope

Medical composites are materials that are specifically designed for use in medical and healthcare applications. They are composed of two or more distinct materials with different properties combined to create a material that possesses unique characteristics suitable for medical purposes.

The medical composites market is segmented by material type (carbon, ceramic, and other material types), product type (surgical instruments, diagnostic equipment, body implants, tissue engineering, and other product types), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across significant regions globally.

The report offers the value (in USD) for the above segments.

| Carbon Fiber Reinforced Polymer (CFRP) |

| Glass Fiber Reinforced Polymer (GFRP) |

| Ceramic Matrix Composites |

| Other Materials |

| PEEK |

| Polypropylene (PP) |

| PMMA & Acrylics |

| Others |

| Carbon Fibre |

| Glass Fibre |

| Aramid & Other High-Performance Fibres |

| Surgical Instruments |

| Diagnostic Imaging Components |

| Orthopedic Implants |

| Dental Implants |

| Tissue Engineering Scaffolds |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Carbon Fiber Reinforced Polymer (CFRP) | |

| Glass Fiber Reinforced Polymer (GFRP) | ||

| Ceramic Matrix Composites | ||

| Other Materials | ||

| By Polymer Matrix | PEEK | |

| Polypropylene (PP) | ||

| PMMA & Acrylics | ||

| Others | ||

| By Fibre Type | Carbon Fibre | |

| Glass Fibre | ||

| Aramid & Other High-Performance Fibres | ||

| By Application | Surgical Instruments | |

| Diagnostic Imaging Components | ||

| Orthopedic Implants | ||

| Dental Implants | ||

| Tissue Engineering Scaffolds | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical composites market?

The medical composites market size reached USD 1.68 billion in 2026 and is forecast to climb to USD 2.83 billion by 2031.

Which material dominates the medical composites market?

Carbon Fiber Reinforced Polymer leads, holding 35.05% share in 2025 because of its high strength-to-weight ratio and radiolucency.

Which region is growing the fastest for medical composites?

Asia-Pacific is projected to register a 11.98% CAGR through 2031, driven by expanding healthcare infrastructure and local manufacturing capacity.

Why is PEEK widely used in composite implants?

PEEK’s modulus closely matches bone, it tolerates repeated sterilization, and its radiolucency enables clear post-operative imaging.

What are the main restraints hindering wider adoption of medical composites?

High production costs, complex multi-region regulatory approvals, recycling challenges, and intricate machining and sterilization processes temper growth.

How fragmented is the competitive landscape?

The market is moderately fragmented; the top five suppliers hold significant market share combined revenue, leaving significant space for new entrants and niche innovators.

Page last updated on: