Global Hyperlipidemia Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

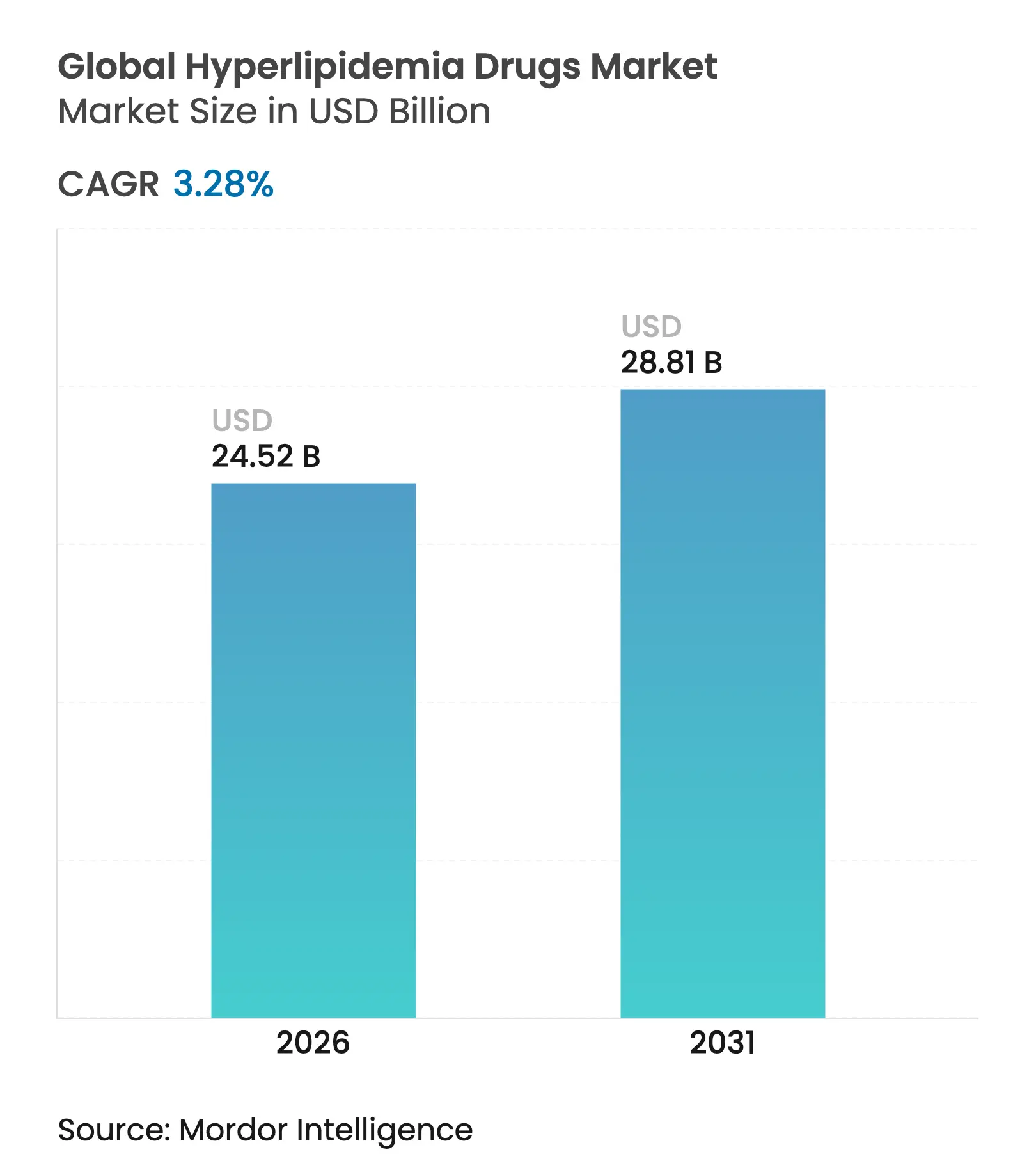

| Market Size (2026) | USD 24.52 Billion |

| Market Size (2031) | USD 28.81 Billion |

| Growth Rate (2026 - 2031) | 3.28 % CAGR |

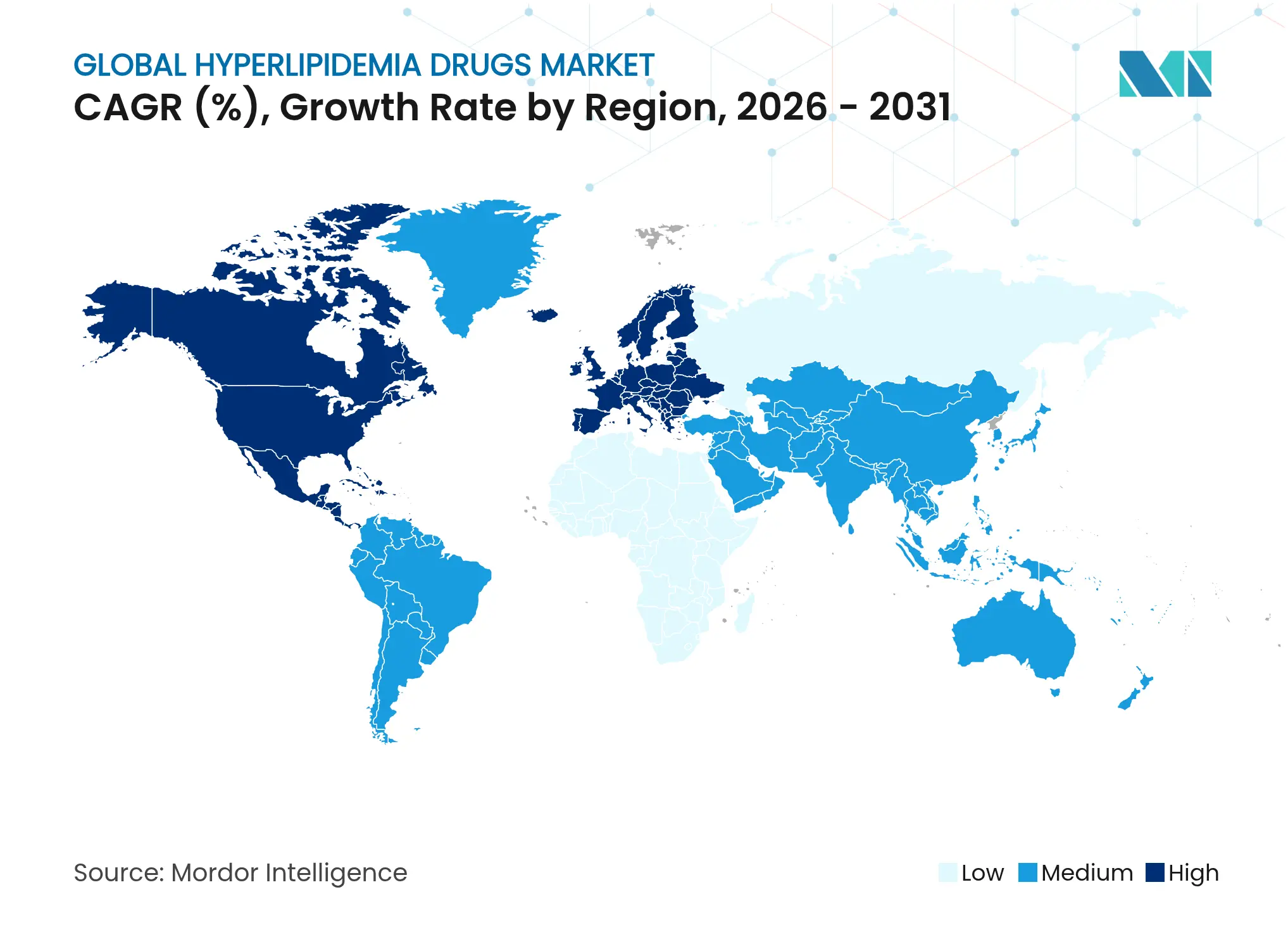

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Global Hyperlipidemia Drugs Market Analysis by Mordor Intelligence

The hyperlipidemia drugs market size is expected to grow from USD 23.74 billion in 2025 to USD 24.52 billion in 2026 and is forecast to reach USD 28.81 billion by 2031 at 3.28% CAGR over 2026-2031. This expansion is propelled by the widening pool of dyslipidemia patients—now exceeding 2 billion adults—as well as steady uptake of premium biologics for very-high-risk cohorts. Novel value-based contracts in the United States and selected European systems reward providers for achieving guideline LDL-C thresholds, reinforcing demand even as generic statins commoditize first-line therapy. Meanwhile, emerging economies contribute sizeable volume gains as national screening initiatives and improved drug affordability broaden treatment coverage. Competitive intensity remains pronounced because patent expiries for branded statins and looming biosimilars for key biologics compel originators to diversify pipelines, often through acquisitions that fast-track next-generation mechanisms.

Key Report Takeaways

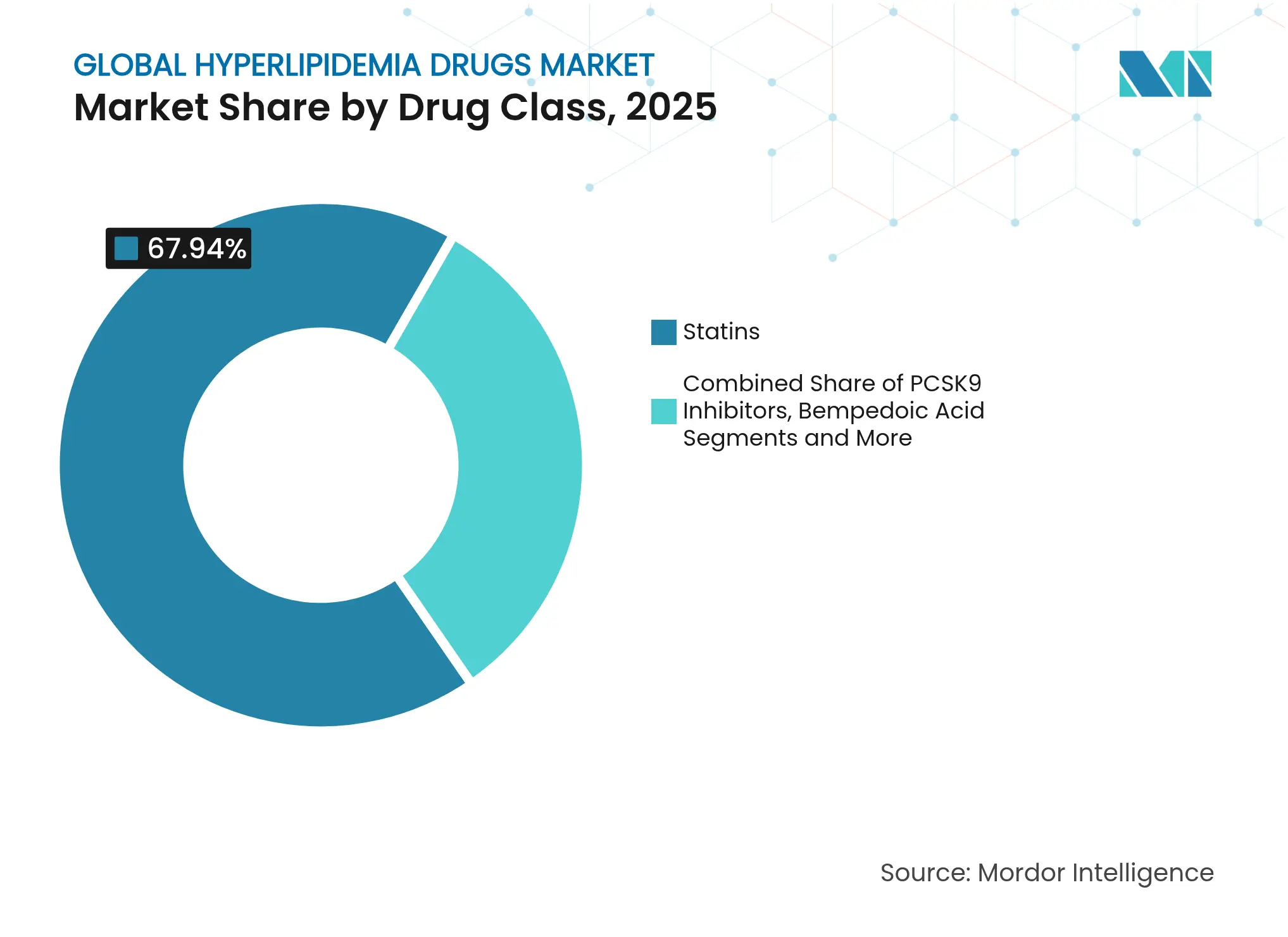

- By drug class, statins led with 67.94% of lipid-lowering drugs market share in 2025; PCSK9 inhibitors are projected to record the fastest 4.28% CAGR through 2031.

- By route of administration, oral therapies accounted for 65.18% of the lipid-lowering drugs market size in 2025, while parenteral products are advancing at a 4.45% CAGR to 2031.

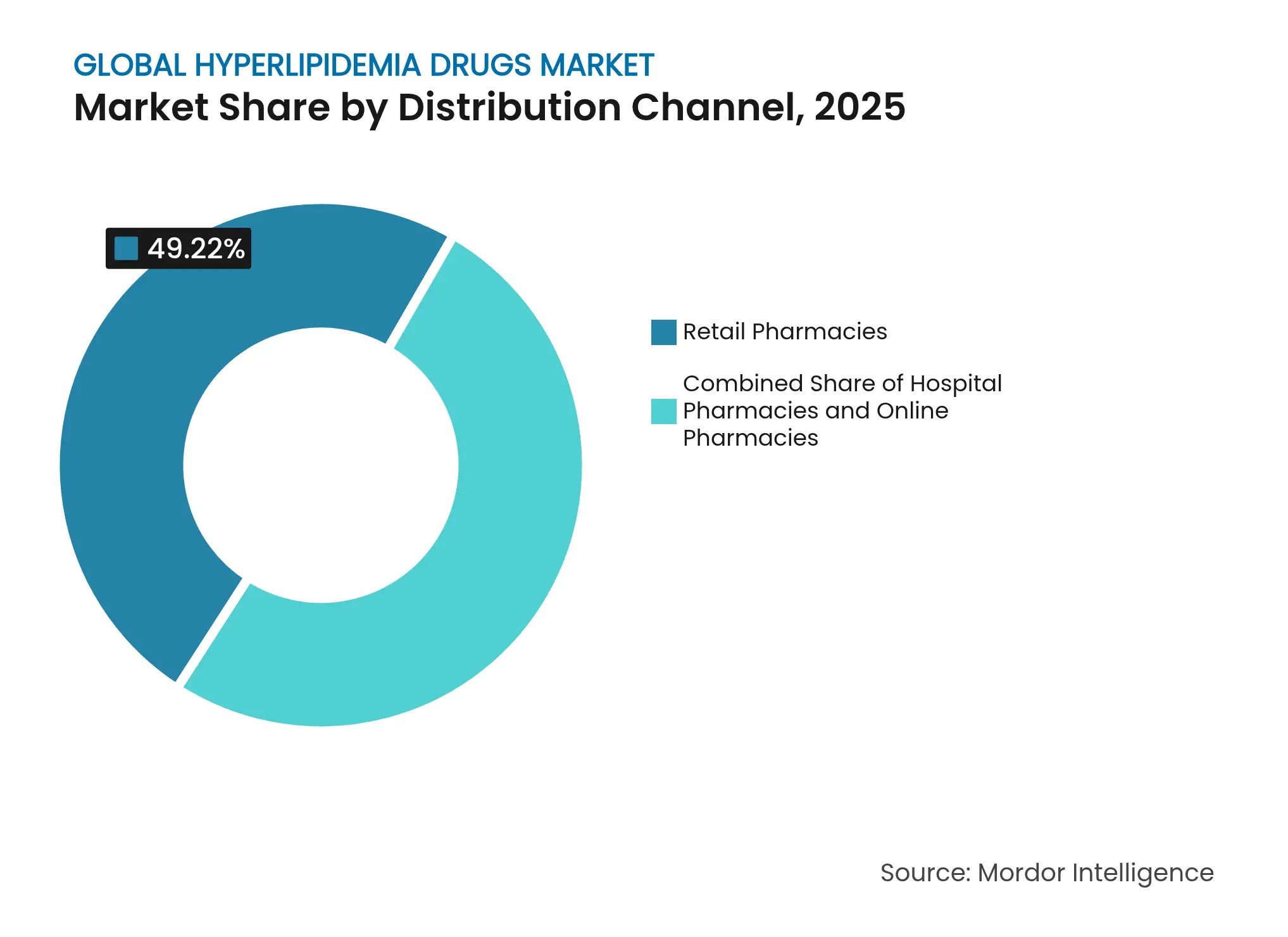

- By distribution channel, retail pharmacies held 49.22% revenue share in 2025; online pharmacies exhibit the highest 4.86% CAGR over the forecast period.

- By geography, North America contributed 45.21% revenue share in 2025 whereas Asia-Pacific is set to expand at a 5.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hyperlipidemia Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing Prevalence Of Dyslipidemia & CVD Risk Factors

Growing Prevalence Of Dyslipidemia & CVD Risk Factors

| +1.2% | Global, with highest impact in Asia-Pacific and Middle East | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.2%

|

Geographic Relevance

:

Global, with highest impact in Asia-Pacific and Middle

East

|

Impact Timeline

:

Long term (≥ 4 years)

|

Rapid Uptake Of Novel Lipid-Lowering Biologics

Rapid Uptake Of Novel Lipid-Lowering Biologics

| +0.8% | North America & EU core markets | Medium term (2-4 years) | |||

Wider Generic Statin Availability Improving Affordability

Wider Generic Statin Availability Improving Affordability

| +0.6% | Asia-Pacific, Latin America, MEA | Short term (≤ 2 years) | |||

Digital Therapeutics & Remote Lipid-Management

Platforms

Digital Therapeutics & Remote Lipid-Management

Platforms

| +0.4% | North America, EU, with spillover to urban Asia-Pacific | Medium term (2-4 years) | |||

Piloting Value-Based Contracts in US and

Europe

Piloting Value-Based Contracts in US and

Europe

| +0.3% | Europe and US | Short term (≤ 2 years) | |||

Value-Based Reimbursement Tied To LDL-C Targets

Value-Based Reimbursement Tied To LDL-C Targets

| +0.5% | North America, select EU markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Prevalence Of Dyslipidemia & CVD Risk Factors

More than 2 billion adults live with elevated cholesterol, and dyslipidemia now contributes to 4.4 million deaths each year [1]American Heart Association, “Heart Disease and Stroke Statistics 2024,” heart.org. Aging populations, processed-food diets and sedentary habits intensify the cardiovascular burden across both wealthy and developing regions. Asia-Pacific records the sharpest prevalence increase, underlining the importance of national screening drives and subsidized statin programs. Familial hypercholesterolemia, newly estimated at 1 in 250 persons worldwide, expands the addressable pool for potent biologics designed for refractory LDL-C control. These epidemiological realities supply an enduring demand floor for the lipid-lowering drugs market.

Rapid Uptake Of Novel Lipid-Lowering Biologics

PCSK9 inhibitors posted a 36% global sales jump in 2024, led by Amgen’s Repatha revenue of USD 2.2 billion. Injectable agents are increasingly prescribed when patients fail to hit LDL-C goals on maximally tolerated statins, a scenario reinforced by guideline updates that favor <70 mg/dL targets for very-high-risk cohorts. FDA clearance of lerodalcibep in 2024, with 56% LDL-C reduction, widened clinician confidence, while inclisiran’s semi-annual dosing improved adherence in real-world settings. The pipeline remains vibrant; Merck’s oral PCSK9 inhibitor MK-0616 achieved late-stage success in 2025, hinting at an oral-biologic paradigm likely to reshape treatment algorithms [2]Merck & Co., “Merck’s MK-0616 Meets Primary Endpoint in CORALreef Phase 3 Program,” merck.com.

Wider Generic Statin Availability Improving Affordability

Price declines of 60–80% for atorvastatin and simvastatin in Asia-Pacific unlocked large-scale prevention programs, notably India’s nationwide dyslipidemia screening that now covers 500 million adults. Ongoing patent cliffs—including rosuvastatin generics—are expected to further compress costs through 2026, enabling broader public-health deployments. Lower unit prices, however, drive manufacturers to extract value through differentiated fixed-dose combinations such as bempedoic-acid/ezetimibe, which offer superior lipid reduction at competitive price points.

Digital Therapeutics & Remote Lipid-Management Platforms

FDA-cleared digital tools that couple medication reminders with real-time lipid analytics have yielded measurable adherence gains and LDL-C improvements. Smartphone-based injection coaching for PCSK9 inhibitors diminishes administration anxiety, while AI algorithms flag high-risk non-adherers, permitting nursing outreach before lapses occur. Hybrid telehealth models that blend virtual visits with point-of-care labs now account for 70% of follow-up appointments at leading lipid clinics, signalling durable behavior change.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Looming patent cliff for remaining branded statins

Looming patent cliff for remaining branded statins

| –0.7% | Global, peak in North America & EU | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

–0.7%

|

Geographic Relevance

:

Global, peak in North America & EU

|

Impact Timeline

:

Short term (≤ 2 years)

|

High cost & prior-authorization hurdles for injectable

biologics

High cost & prior-authorization hurdles for injectable

biologics

| –0.9% | North America, EU, private markets globally | Medium term (2–4 years) | |||

Stringent multi-regional pharmacovigilance requirements

Stringent multi-regional pharmacovigilance requirements

| –0.5% | Global, highest in EU & North America | Medium term (2–4 years) | |||

Supply-chain constraints for LNP & oligonucleotide raw

materials

Supply-chain constraints for LNP & oligonucleotide raw

materials

| –0.3% | Global, affecting RNA-based therapies | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Looming Patent Cliff For Remaining Branded Statins

With rosuvastatin and pitavastatin set to lose exclusivity, originators face revenue erosion estimated at USD 2–3 billion by 2027. Historic precedent shows statin prices collapsing 90% within 18 months of generic entry, forcing innovators to diversify into combination products or entirely new mechanisms. Generic competitors in emerging markets are gearing up for aggressive launches, leveraging existing distribution networks to seize volume rapidly.

High Cost & Prior-Authorization Hurdles For Injectable Biologics

Annual PCSK9 inhibitor therapy often exceeds USD 5,000, triggering payer resistance that materializes as stringent prior-authorization protocols. Documentation of statin intolerance or repeated LDL-C failures is commonly mandated, delaying patient access and curbing physician enthusiasm [3]NHS England, “Commissioning Position on PCSK9 Inhibitors 2024,” england.nhs.uk . While outcome-based contracts are gaining traction, they remain complex to administer and are not yet standard across all payers. Divergent coverage decisions perpetuate inequities, especially in systems with high out-of-pocket exposure.

Segment Analysis

By Drug Class: Statins Anchor Market Despite Biologic Momentum

Statins delivered 67.94% of lipid-lowering drugs market share in 2025 thanks to established safety, once-daily oral dosing and deep generic penetration. Revenue protection stems from high prescription volumes that offset eroding margins, allowing statins to remain the backbone of cardiovascular prevention regimens. PCSK9 inhibitors, though representing a modest revenue base, are projected to post the fastest 4.28% CAGR, powered by robust outcome data that validate intensive LDL-C lowering for atherothrombotic risk reduction. Cholesterol absorption inhibitors, primarily ezetimibe, grow through co-formulations that enhance statin efficacy, while bempedoic acid provides a non-statin oral alternative for statin-intolerant patients, positioning itself as a strategic mid-priced option between generic commoditization and biologic premiums.

As branded statins lose exclusivity and biologic patents face biosimilar threats after 2030, drug-class diversification accelerates. Several ANGPTL3 inhibitors and lipoprotein(a) therapies target high-unmet-need niches, and oral PCSK9 candidates could merge convenience with biologic-level potency. These dynamics are expected to keep the lipid-lowering drugs market competitive while sustaining a steady innovation pipeline that offsets upcoming revenue cliffs.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Oral Dominance Meets Injectable Innovation

Oral delivery generated 65.18% of the lipid-lowering drugs market size in 2025, reflecting patient familiarity and ease of daily dosing. Long-established statins and newer oral agents such as bempedoic acid make this segment cost-efficient and scalable for nationwide cardiovascular programs. Injectable formulations, however, are gaining traction, with parenteral therapies forecast to rise at a 4.45% CAGR through 2031. Twice-yearly inclisiran has demonstrated adherence advantages, shifting perceptions that injections must equal monthly clinic visits.

Enhancements such as auto-injectors reduce training time and improve user confidence; satisfaction scores exceed 80% in recent surveys. Oral PCSK9s on the horizon could disrupt both categories by merging the convenience benefit of tablets with the potency of biologics, illustrating that delivery technology will remain a critical battlefield for share gains within the lipid-lowering drugs market.

By Distribution Channel: Retail Pharmacies Confront Digital Disruption

Retail outlets held 49.22% of 2025 revenue and remain indispensable for high-volume statin dispensing. Their cross-selling of cardiovascular risk-management services (blood-pressure checks, smoking-cessation counselling) sustains relevance. Yet online pharmacies are forecast to grow fastest at a 4.86% CAGR, reflecting escalating consumer preference for home delivery, transparent pricing and subscription-based refills. The COVID-19 pandemic accelerated the comfort level with digital medication fulfillment, and national regulators have since clarified verification standards that reinforce patient safety.

Hospital and specialty pharmacies continue to dominate for high-touch, cold-chain biologics, where on-site counselling and biologic stewardship lower discontinuation rates. As biosimilar PCSK9s emerge, some volume may migrate to retail or mail-order channels that can handle refrigerated products more cost-effectively, suggesting fluid channel boundaries over the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America contributed 45.21% revenue in 2025 owing to sophisticated reimbursement frameworks and early biologic adoption. U.S. payers increasingly embrace shared-savings models that fund PCSK9 inhibitors once patients demonstrate sub-70 mg/dL targets, while Medicare Part D redesign under the Inflation Reduction Act reshapes out-of-pocket trajectories. Canada pioneered a dedicated inclisiran funding route that avoids incremental budget impacts during the first contract cycle, whereas Mexico’s private-insurance expansion lifts branded statin volumes faster than GDP growth.

Europe remains a price-sensitive yet innovation-driven region. Centralized EMA approvals coexist with country-specific evaluations, yielding a mosaic of access timelines. Germany’s HEYMANS study confirmed real-world PCSK9 effectiveness, reinforcing reimbursement in statutory insurance plans. The United Kingdom’s National Health Service uses outcome-based agreements to curb budget risk while ensuring high-risk patients receive biologics promptly. Asia-Pacific delivers the fastest 5.07% CAGR through 2031. China’s Healthy China 2030 plan funds mass cholesterol screening and statin purchase contracts, enlarging the treated population. Japan’s demographic aging sustains steady demand for both generics and high-end biologics; local trials affirm superior LDL-C reduction from novel CETP inhibitors. India, fortified by robust API manufacturing capacity, drives down procured statin costs and exports low-priced formulations across ASEAN markets. Australia integrates PCSK9 inhibitors into the Pharmaceutical Benefits Scheme for acute coronary syndrome patients, illustrating momentum toward broader biologic reimbursement in the region.

Competitive Landscape

Market Concentration

The lipid-lowering drugs market displays moderate consolidation. Top manufacturers leverage first-mover biologic franchises while a long tail of generic suppliers compete on cost efficiency. Amgen, Sanofi and Regeneron protect Repatha and Praluent through device innovations and real-world evidence generation. Meanwhile, Esperion Therapeutics captures the statin-intolerant niche via bempedoic acid, broadening payer options below biologic price points.

Strategic acquisitions intensify, exemplified by Eli Lilly’s USD 1.3 billion purchase of Verve Therapeutics to secure a gene-editing platform for PCSK9 and ANGPTL3 targets. Partnerships between pharma and digital-health firms underpin medication-adherence ecosystems, increasingly seen as competitive differentiators rather than ancillary services. Biosimilar development for evolocumab gathers pace as major patents expire from 2030 onward, positioning large generics players to challenge incumbent pricing and compress biologic margins.

Future competition will hinge on delivery innovation and precision-medicine alignment. Oral PCSK9 inhibitors, if approved, could redraw market hierarchies by undercutting injectable price premiums while matching efficacy. Companies harnessing AI-based lipidomic profiling to fine-tune therapy selection are poised to strengthen customer loyalty and defend share in the evolving lipid-lowering drugs market.

Global Hyperlipidemia Drugs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Merck reported positive Phase 3 CORALreef results for oral PCSK9 inhibitor MK-0616, showing significant LDL-C reduction with once-daily dosing.

- May 2024: Baylor College of Medicine published trial data on plozasiran, an ApoC3-targeted therapy for hyperlipidemia, demonstrating triglyceride and cholesterol modulation.

- March 2024: FDA approved Praulent (alirocumab) for pediatric familial hypercholesterolemia, expanding early-intervention options.

- November 2023: Lupin Limited secured FDA clearance to market generic pitavastatin tablets (1 mg, 2 mg, 4 mg) in the United States.

Table of Contents for Global Hyperlipidemia Drugs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Prevalence Of Dyslipidemia & CVD Risk Factors

- 4.2.2Rapid Uptake Of Novel Lipid-Lowering Biologics

- 4.2.3Wider Generic Statin Availability Improving Affordability

- 4.2.4Piloting Value-Based Contracts in US and Europe

- 4.2.5Digital Therapeutics & Remote Lipid-Management Platforms

- 4.2.6Value-Based Reimbursement Tied To Ldl-C Targets

- 4.3Market Restraints

- 4.3.1Looming Patent Cliff For Remaining Branded Statins

- 4.3.2High Cost & Prior-Auth Hurdles For Injectable Biologics

- 4.3.3Stringent Multi-Regional Pharmacovigilance Requirements

- 4.3.4Supply-Chain Constraints For Lnp & Oligo Raw Materials

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers/Consumers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Drug Class

- 5.1.1Statins

- 5.1.2PCSK9 Inhibitors

- 5.1.3Cholesterol Absorption Inhibitors

- 5.1.4Bempedoic Acid

- 5.1.5Others

- 5.2By Route of Administration

- 5.2.1Oral

- 5.2.2Parenteral

- 5.2.3Others

- 5.3By Distribution Channel

- 5.3.1Hospital Pharmacies

- 5.3.2Online Pharmacies

- 5.3.3Retail Pharmacies

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Amgen

- 6.3.2Sanofi

- 6.3.3Regeneron Pharmaceuticals

- 6.3.4Viatris

- 6.3.5Pfizer

- 6.3.6Merck & Co.

- 6.3.7AstraZeneca

- 6.3.8Daiichi Sankyo

- 6.3.9Esperion Therapeutics

- 6.3.10Novartis

- 6.3.11Johnson & Johnson (Janssen)

- 6.3.12Eli Lilly

- 6.3.13Alnylam Pharmaceuticals

- 6.3.14Arrowhead Pharmaceuticals

- 6.3.15Ionis / Akcea

- 6.3.16CSL Behring

- 6.3.17Amarin Corporation

- 6.3.18Lexicon Pharma

- 6.3.19Chiesi Farmaceutici

- 6.3.20Roche

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Hyperlipidemia Drugs Market Report Scope

As per the scope of this report, hyperlipidemia is a condition that is caused by abnormally high lipid levels in the blood and it is the most common type of dyslipidemia. This disorder can happen due to genetic factors (primary hyperlipidemia) as well as other factors such as unhealthy lifestyle and poor diet (secondary hyperlipidemia). Statins are the first line of treatment for secondary hyperlipidemia. The hyperlipidemia market is segmented by drug class (statins, cholesterol absorption inhibitors, bile acid sequestrants, pcsk9 inhibitors, others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value in USD million for the above segments.