Polyphenol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 3.13 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polyphenol Market Analysis by Mordor Intelligence

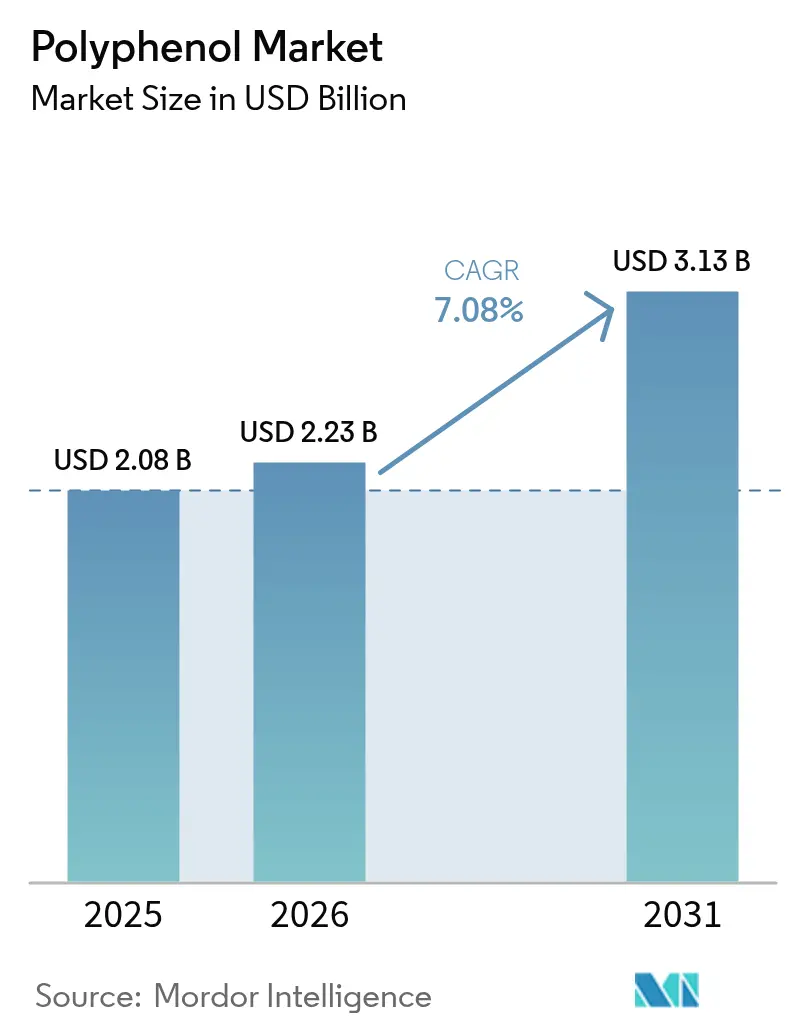

The polyphenol market size in 2026 is estimated at USD 2.23 billion, growing from 2025 value of USD 2.08 billion with 2031 projections showing USD 3.13 billion, growing at 7.08% CAGR over 2026-2031. This growth trajectory reflects the market's maturation beyond traditional antioxidant applications, driven by breakthrough encapsulation technologies that address the fundamental bioavailability challenge that has historically limited polyphenol efficacy in consumer products. These advancements tackle the bioavailability challenges that have long hindered the effectiveness of polyphenols in consumer products. The FDA's 2028 rollout of updated "healthy" food labeling criteria, as highlighted by the U.S. Department of Health and Human Services [1]Source: U.S. Department of Health and Human Services, "Updated the definition of the 'healthy' nutrient content claim to reflect modern nutrition science and dietary guidelines.", www.govinfo.gov , is set to open new avenues for polyphenol-enhanced products. This regulatory shift, coupled with a surge in demand for functional beverages and nutricosmetics, underscores the market's evolution. Furthermore, firms are not just racing to innovate; they're also investing in sustainable extraction methods from waste streams, bolstering supply resilience and mitigating input risks. Early adopters are setting themselves apart with proprietary nano-delivery systems, ensuring traceability through vertical integration, and swiftly adapting to the tightening "healthy" labeling regulations across the U.S., Canada, and the EU. The Asia-Pacific region, buoyed by a burgeoning middle class and governmental pushes for self-sufficiency in nutraceuticals, promises a significant long-term growth trajectory for the polyphenol market.

Key Report Takeaways

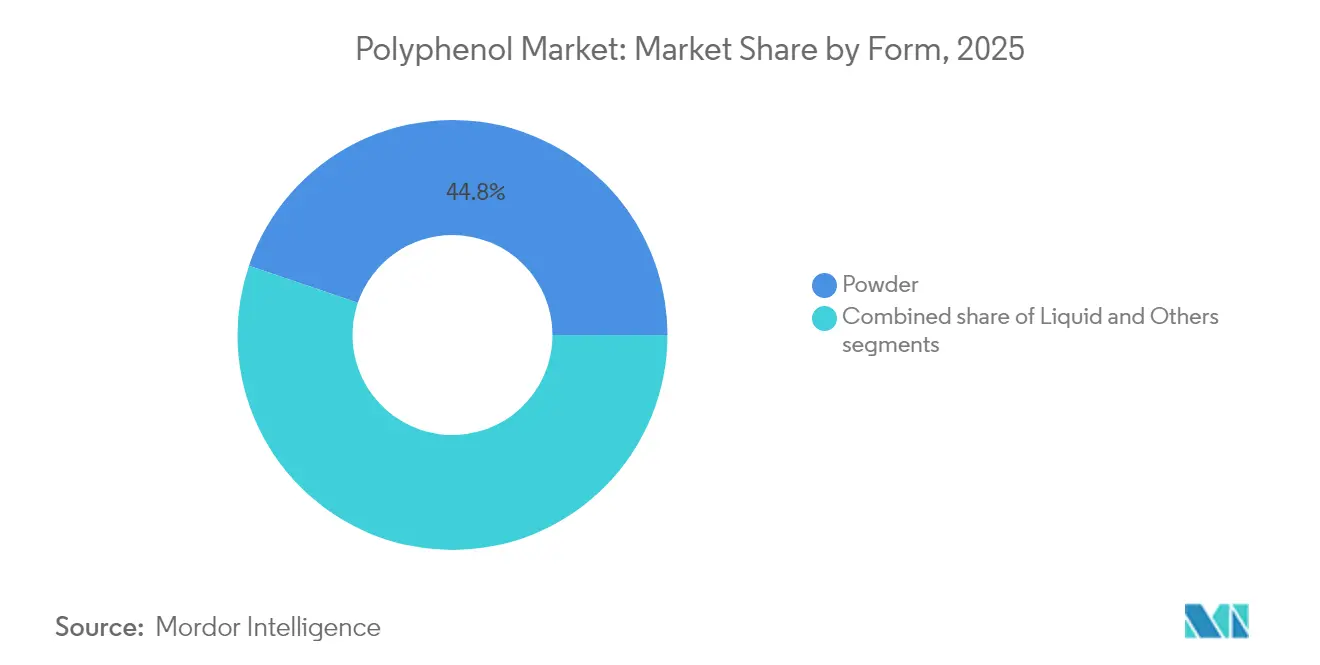

- By form, powders led with 44.78% of polyphenol market share in 2025, whereas liquids are poised for the fastest 8.08% CAGR through 2031.

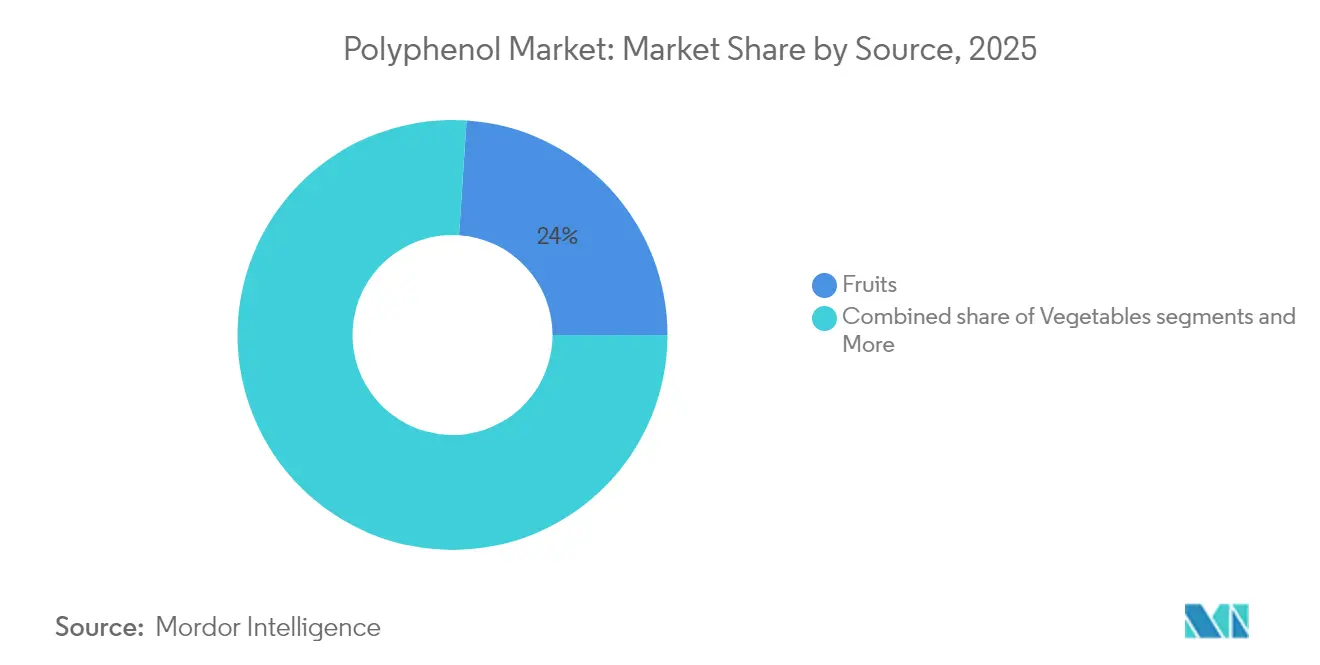

- By source, fruits held 23.96% of the polyphenol market in 2025, while the vegetables category, built around seaweed and agricultural residues, is set to rise at an 8.48% CAGR.

- By application, dietary supplements dominated with 32.96% contribution to the polyphenol market size in 2025; cosmetics and personal care is projected to outpace all other uses at an 8.63% CAGR to 2031.

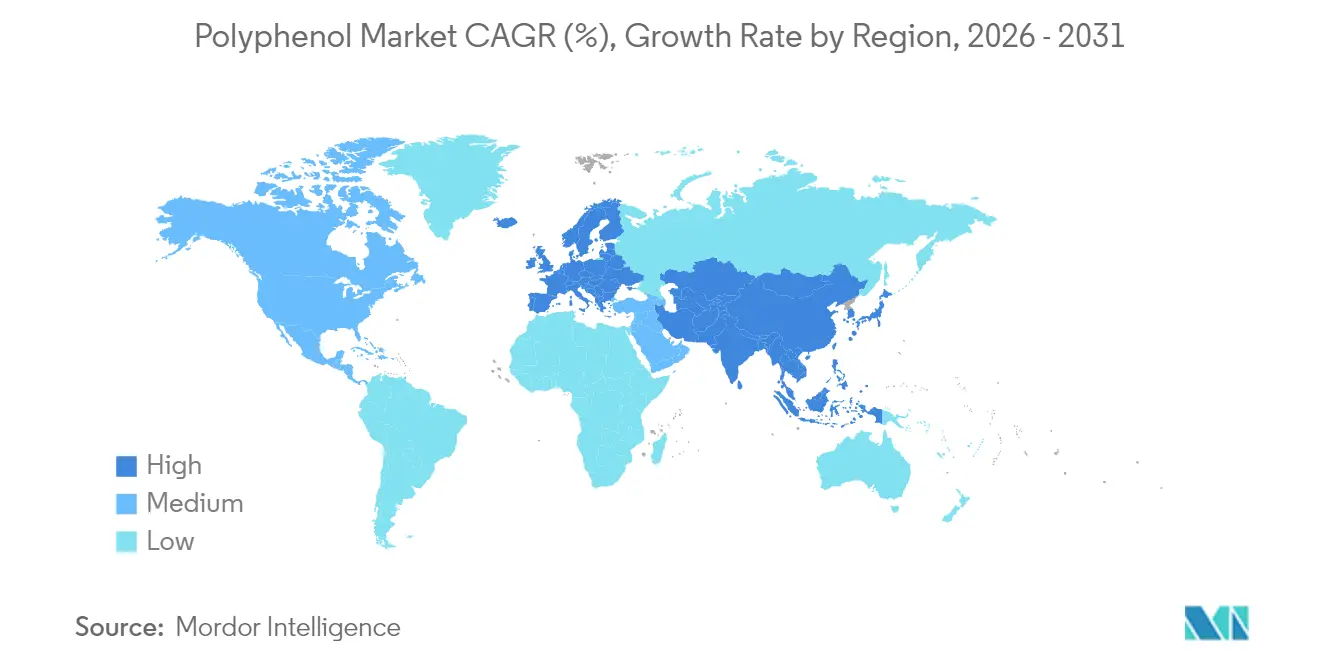

- By geography, Europe held 33.88% of the polyphenol market in 2025, while the Asia-Pacific is set to rise at an 8.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyphenol Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising popularity of natural antioxidants in dietary supplements | +1.8% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Growing awareness of anti-inflammatory and cardiovascular benefits | +1.5% | Global; pronounced in Asia-Pacific aging cohorts | Long term (≥ 4 years) |

| High demand for plant-based ingredients in cosmetic formulations | +1.2% | Europe and North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shifting consumer preferences toward organic and clean labels | +1.0% | North America and Europe core; urban Asia-Pacific spillover | Medium term (2-4 years) |

| Innovation in polyphenol extraction and encapsulation technologies | +0.9% | Global; research and development centered in developed markets | Long term (≥ 4 years) |

| Polyphenols as natural food preservatives | +0.8% | Global; regulatory scope varies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of natural antioxidants in dietary supplements

The dietary supplement industry's pivot toward natural antioxidants is reshaping polyphenol demand patterns, with manufacturers increasingly positioning these compounds as scientifically-validated alternatives to synthetic antioxidants. Recent research demonstrates that polyphenol-rich extracts exhibit dose-dependent efficacy, with optimal consumption levels varying significantly based on individual metabolic profiles. This personalized nutrition approach is driving premium product development, as companies recognize that standardized dosing fails to maximize therapeutic potential. Regulatory clarity is accelerating adoption, with the FDA's 75-day premarket notification system providing clearer pathways for polyphenol-based dietary ingredients [2]Source: U.S Food and Drug Administration, "Pathways for polyphenol-based dietary ingredients", www.fda.gov. The shift toward evidence-based marketing is compelling manufacturers to invest in clinical trials, creating a competitive advantage for companies with robust research capabilities. Additionally, the rising consumer awareness of the health benefits associated with polyphenols is further fueling market growth. The increasing prevalence of chronic diseases, such as cardiovascular disorders and diabetes, is also driving demand for polyphenol-enriched products.

Growing awareness of anti-inflammatory and cardiovascular benefits

Cardiovascular health applications are emerging as a primary growth driver, with polyphenols demonstrating measurable impacts on heart failure and cardiac hypertrophy through multiple molecular pathways. Clinical evidence shows polyphenols regulate heart failure-related molecules, prevent mitochondrial dysfunction, and improve lipid profiles, positioning them as viable alternatives to pharmaceutical interventions. The Mediterranean diet's association with longevity has elevated olive polyphenols specifically, with hydroxytyrosol and oleuropein showing promise in mitigating neurological complications associated with COVID-19. Nano-drug delivery methods are addressing bioavailability limitations that have historically constrained therapeutic applications, enabling more precise dosing and enhanced treatment outcomes. The aging global population is driving demand for preventive healthcare solutions, with polyphenols positioned as accessible interventions for age-related cardiovascular decline. Regulatory bodies are increasingly recognizing cardiovascular health claims, with the FDA's Significant Scientific Agreement standard providing pathways for validated health claims

High demand for plant-based ingredients in cosmetic formulations

The convergence of food and cosmetics industries is creating unprecedented opportunities for polyphenol applications, driven by consumer demand for "nutricosmetics" that deliver beauty benefits from within. This trend reflects a fundamental shift in consumer perception, where beauty products are increasingly viewed as extensions of health and wellness regimens rather than purely aesthetic solutions. Polyphenols' antioxidant and anti-inflammatory properties make them ideal for addressing skin aging, with formulations increasingly incorporating food-derived compounds to enhance efficacy and consumer appeal. The sustainability narrative is particularly compelling, as cosmetic manufacturers leverage food industry byproducts to create eco-friendly formulations that resonate with environmentally conscious consumers. Regulatory advantages favor plant-based ingredients, as natural compounds face fewer restrictions compared to synthetic alternatives, enabling faster product development cycles. As consumers become more discerning, the demand for transparency in ingredient sourcing and formulation processes has surged, pushing brands to prioritize clarity in their marketing.

Shifting consumer preferences toward organic and clean labels

Clean-label positioning has become a competitive necessity rather than a differentiation strategy, with consumers increasingly scrutinizing ingredient lists and demanding transparency in product formulations. This shift is particularly pronounced in developed markets, where regulatory frameworks support organic certification and clean-label claims, creating market premiums for compliant products. The functional beverages sector is experiencing rapid growth as manufacturers respond to consumer demand for natural ingredients with recognizable health benefits. Polyphenols' natural origin and established safety profiles position them advantageously against synthetic alternatives, particularly as regulatory scrutiny of artificial additives intensifies. The plant-based food market's challenges with taste and texture are driving innovation in polyphenol applications, as these compounds can enhance both nutritional profiles and sensory characteristics. Supply chain transparency is becoming increasingly important, with consumers demanding traceability from source to shelf, creating opportunities for vertically integrated polyphenol producers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Low bioavailability of polyphenols in native form | -1.5% | Global, with varying regulatory responses | Medium term (2-4 years) |

| High cost of extraction and purification processes | -1.2% | Global, with cost pressures highest in price-sensitive markets | Short term (≤ 2 years) |

| Limited shelf stability in end-product application | -1.7% | Global, especially in Asia-Pacific and North America | Short term (≤ 2 years) |

| Bitterness and astringency affecting broader consumer appeal | -1.4% | Global, with more impact on Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low bioavailability of polyphenols in native form

The bioavailability challenge represents the most significant technical barrier to polyphenol market expansion, with native forms demonstrating limited absorption and rapid degradation that constrains therapeutic efficacy. Research indicates that polyphenol bioavailability varies significantly due to chemical structure and individual metabolism, with daily intake estimated at approximately 1 gram but actual absorption rates remaining disappointingly low. This limitation has historically prevented polyphenols from achieving pharmaceutical-grade applications, relegating them to nutraceutical and functional food categories with less stringent efficacy requirements. Advanced delivery systems, including nanoencapsulation and targeted formulations, are emerging as solutions, but these technologies add significant cost and complexity to product development. The challenge is particularly acute in liquid formulations, where polyphenol stability is compromised by environmental factors including pH, temperature, and light exposure. Regulatory bodies are increasingly demanding bioavailability data to support health claims, creating additional compliance burdens for manufacturers seeking to market polyphenol-based products with therapeutic positioning.

High cost of extraction and purification processes

Production cost pressures are constraining market growth, particularly in price-sensitive segments where polyphenol premiums cannot be justified by consumer willingness to pay. Conventional extraction methods require significant energy inputs and solvent consumption, while advanced techniques like supercritical fluid extraction demand substantial capital investment that many smaller producers cannot afford. The challenge is compounded by raw material variability, with polyphenol content fluctuating based on source quality, seasonal factors, and processing conditions, creating supply chain inefficiencies that increase production costs. Purification requirements for pharmaceutical and high-end cosmetic applications demand additional processing steps that further escalate costs, limiting market accessibility for price-conscious consumers. Economies of scale remain elusive for many polyphenol producers, as market fragmentation prevents the volume consolidation necessary to achieve cost-competitive production. The sustainability imperative is adding complexity, as environmentally responsible extraction methods often carry premium costs that must be absorbed by manufacturers or passed to consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Challenged by Liquid Innovation

Powder formulations maintain market leadership with 44.78% share in 2025, driven by superior stability profiles and cost-effective manufacturing processes that enable broad commercial adoption across dietary supplements and functional food applications. The established supply chain infrastructure for powder handling provides logistical advantages, while extended shelf life reduces inventory risks for manufacturers and retailers. However, liquid formulations are experiencing the fastest growth at 8.08% CAGR through 2031, reflecting breakthrough innovations in stabilization technologies and consumer preference for convenient, ready-to-consume formats.

Liquid polyphenol products are gaining traction in the functional beverages, where manufacturers are leveraging advanced encapsulation techniques to overcome traditional stability challenges. The "Others" category, encompassing innovative delivery formats like gummies and fortified foods, represents emerging opportunities as manufacturers explore novel applications to differentiate their offerings. Microencapsulation technology is enabling powder formulations to achieve enhanced bioavailability while maintaining cost advantages, with spray drying and emulsion-based methods becoming industry standards. The convergence of form and function is creating hybrid products that combine the stability of powders with the convenience of liquids, positioning the market for continued innovation in delivery mechanisms.

By Application: Supplements Lead While Cosmetics Accelerate

In 2025, dietary supplements command a dominant 32.96% share of the polyphenol market, bolstered by regulatory frameworks endorsing health claims and a growing consumer trust in polyphenols as scientifically-backed wellness agents. This segment reaps the rewards of well-established distribution channels and savvy marketing strategies that spotlight preventive healthcare benefits. Meanwhile, the cosmetics and personal care sector emerges as the fastest-growing application, boasting an impressive 8.63% CAGR through 2031. This surge is fueled by the rising nutricosmetics trend and a consumer shift towards natural ingredients celebrated for their antioxidant prowess. As consumers increasingly prioritize health and wellness, the demand for polyphenol-infused products is set to soar, further solidifying their market position.

Functional foods and beverages are experiencing steady growth as manufacturers incorporate polyphenols to enhance nutritional profiles and support clean-label positioning. The berry beverage market illustrates this trend, with products leveraging natural sweetness and bioactive compounds to address diabetes management and weight control applications. Animal feed applications remain niche but show potential as livestock producers seek natural alternatives to synthetic additives for improving animal health and product quality. The convergence of applications is creating cross-category opportunities, with companies developing polyphenol ingredients that serve multiple end-use markets simultaneously. Regulatory harmonization across applications could accelerate growth, as standardized safety assessments and health claim procedures reduce market entry barriers for innovative polyphenol products.

By Source: Fruit Leadership Faces Waste Stream Disruption

Fruits command the largest source segment with 23.96% market share in 2025, benefiting from established extraction infrastructure and consumer familiarity with fruit-derived health benefits. Traditional sources like grapes, berries, and citrus fruits continue to dominate due to well-documented polyphenol profiles and regulatory approval for health claims. As the market matures, there's a growing emphasis on educating consumers about lesser-known fruits, potentially broadening the market's scope. Vegetable sources are gaining momentum, growing at a CAGR of 8.48% during the forecast years as manufacturers recognize the untapped potential of processing byproducts, with fruit and vegetable waste representing supply chain losses that can be converted into valuable polyphenol extracts. The increasing demand for clean-label and natural ingredients in food and beverages further supports the dominance of fruit-derived polyphenols.

However, the other category is expanding through 2031, driven by innovative utilization of agricultural waste streams and exploration of novel sources like seaweed and industrial byproducts. The circular economy imperative is driving investment in waste valorization technologies, with companies developing sustainable extraction methods that transform agricultural residues into high-value polyphenol ingredients. As industries grapple with waste management challenges, the push towards valorization not only addresses environmental concerns but also opens new revenue streams. Additionally, partnerships between agricultural producers and tech firms are becoming commonplace, accelerating the development and adoption of these sustainable extraction methods. The growing interest in plant-based diets is further encouraging the exploration of alternative polyphenol sources.

Geography Analysis

Europe holds 33.88% of the market share, supported by stringent regulatory standards that favor natural ingredients and comprehensive sustainability initiatives that align with polyphenol production from agricultural waste streams. The European Commission'sinvestment in seaweed polyphenol research illustrates regional commitment to innovative applications, with projects demonstrating commercial viability in both dietary supplements and personal care products. Germany's leadership in plant-based innovation and the UK's post-Brexit regulatory flexibility are creating competitive advantages for polyphenol producers.

Asia-Pacific emerges as the fastest-growing region through 2031 with a CAGR of 8.22%, with China and India driving demand through expanding middle classes and increasing health consciousness. The Indian nutraceutical market reached USD 6.1 billion in 2023 with 11.4% projected growth, creating substantial opportunities for polyphenol-based dietary supplements, according to Protein Foods and Nutrition Development Association of India. Japan's aging population and advanced regulatory framework for functional foods position the country as a premium market for innovative polyphenol applications.

North America maintains regional market leadership in 2024, driven by established dietary supplement infrastructure and consumer willingness to pay premiums for scientifically-validated health ingredients. The region benefits from clear regulatory frameworks that support health claims, with the FDA's updated "healthy" food labeling criteria creating new opportunities for polyphenol-fortified products. Canada's significant government investment in plant-based research and the U.S. biomass supply chain initiative are creating favorable conditions for polyphenol market expansion.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The polyphenol market exhibits moderate fragmentation, indicating significant consolidation opportunities as established players seek to capture market share through strategic acquisitions and vertical integration. Competition intensity remains manageable due to technical barriers in extraction and purification processes, which create natural moats for companies with proprietary technologies and established supply chains. Major players in the market include Cargill, Incorporated, Givaudan SA, International Flavors & Fragrances Inc., and DSM-Firmenich AG.

Opportunities abound in emerging sectors such as animal feed and industrial preservatives, where polyphenols stand poised to supplant synthetic alternatives, all while aligning with sustainability mandates. Notably, patent activity surrounding nano-formulations and delivery systems underscores a robust research and development investment trend, with firms pioneering proprietary encapsulation technologies to tackle bioavailability challenges. The growing demand for natural and clean-label products further drives the adoption of polyphenols in these applications. Additionally, the increasing awareness of the environmental impact of synthetic chemicals is pushing industries to explore sustainable alternatives like polyphenols.

As technology adoption emerges as a pivotal competitive edge, firms boasting advanced extraction methods are reaping benefits: heightened yields, superior product quality, and diminished production costs. Borregaard's biorefinery model serves as a testament, showcasing how businesses harness sustainable production techniques to carve out advantages in eco-aware markets. Companies investing in innovative extraction technologies are also better positioned to meet the rising demand for high-purity polyphenols. Furthermore, collaborations between industry players and research institutions are accelerating the development of cost-effective and scalable production methods.

Polyphenol Industry Leaders

-

Botanic Healthcare

-

Givaudan SA

-

International Flavors and Fragrances (IFF)

-

A. Holliday and Company Inc.

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Borregaard expanded its biorefinery operations with enhanced lignin and wood-based vanillin production capabilities, positioning the company as a leading supplier of sustainable polyphenol precursors for multiple industries, including food, pharmaceuticals, and agriculture

- December 2024: The FDA finalized updated "healthy" food labeling criteria that will take effect in February 2028, creating new opportunities for polyphenol-fortified products to qualify for beneficial health positioning.

- June 2024: European research project on seaweed polyphenols demonstrated commercial viability for anti-inflammatory applications in dietary supplements and personal care products.

- March 2024: The USDA released its comprehensive biomass supply chain plan emphasizing sustainable sourcing for biobased products including polyphenols, with government support for research, development, and market expansion initiatives.

Global Polyphenol Market Report Scope

Polyphenols are naturel compounds found abundantly in plants, including flavonoids, tannic acid, ellagitannin and phenolic acid, that greatly benefit the human body and help fight disease.

The global polyphenol market is segmented by form, source, application, and geography. On the basis of form, the market is segmented into liquid, powder, and others. On the basis of source, the market is segmented into plant extracts, fruits, vegetables, cocoa, and others. On the basis of application, the market is segmented into functional foods, dietary supplements, beverages, others. On the basis of geography, the study provides an analysis of the polyphenol market in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

| Liquid |

| Powder |

| Others |

| Fruits |

| Vegetables |

| Cocoa |

| Others |

| Functional Foods |

| Beverages |

| Dietary Supplements |

| Animal Feed |

| Cosmetics and Personal Care |

| Others |

| United States | Canada |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Liquid | |

| Powder | ||

| Others | ||

| By Source | Fruits | |

| Vegetables | ||

| Cocoa | ||

| Others | ||

| By Application | Functional Foods | |

| Beverages | ||

| Dietary Supplements | ||

| Animal Feed | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Geography | United States | Canada |

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the polyphenol market?

The polyphenol market size is valued at USD 2.23 billion in 2026 and is projected to reach USD 3.13 billion by 2031.

Which segment holds the largest share of the polyphenol market?

Powder formulations lead with 44.78% of global polyphenol market share, owing to their stability and cost efficiency.

Why are encapsulation technologies important for polyphenols?

Encapsulation boosts bioavailability and stability, enabling polyphenols to perform effectively in beverages, supplements, and cosmetics.

Which region is expected to witness the highest growth?

Asia-Pacific is the fastest-growing region through 2031 with a CAGR of 8.22%, propelled by expanding middle-class consumers in China and India and supportive functional-food regulations.

Page last updated on: