Market Overview

| Study Period | 2021 - 2031 |

|---|---|

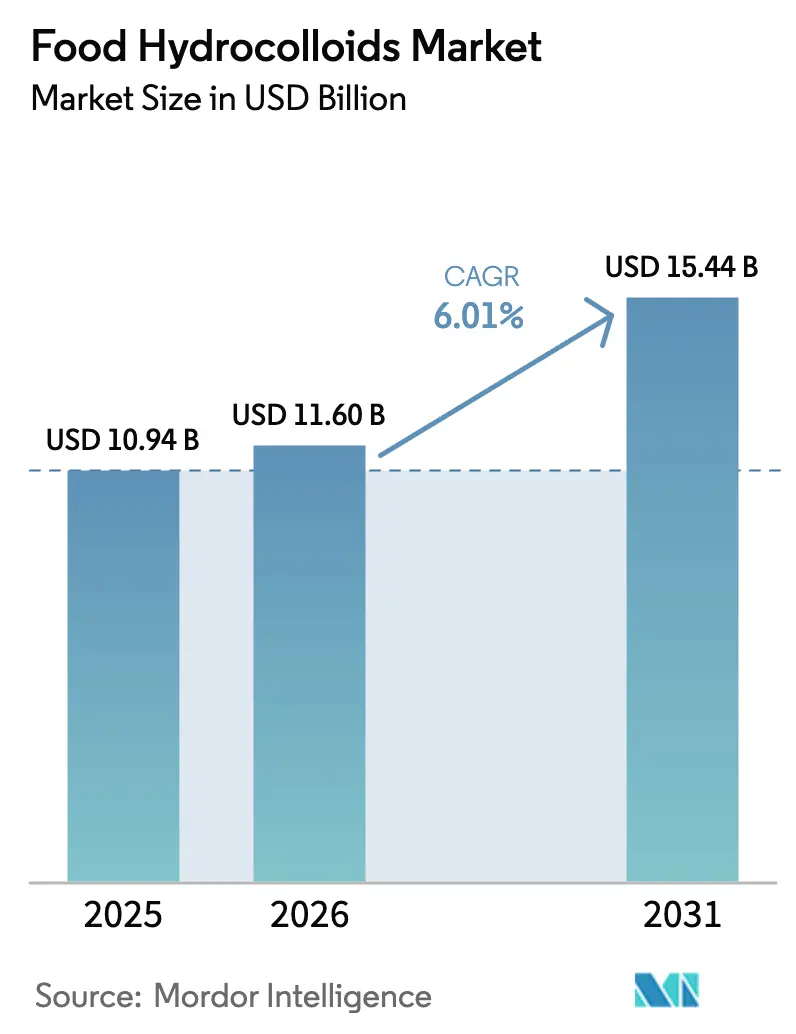

| Market Size (2026) | USD 11.60 Billion |

| Market Size (2031) | USD 15.44 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

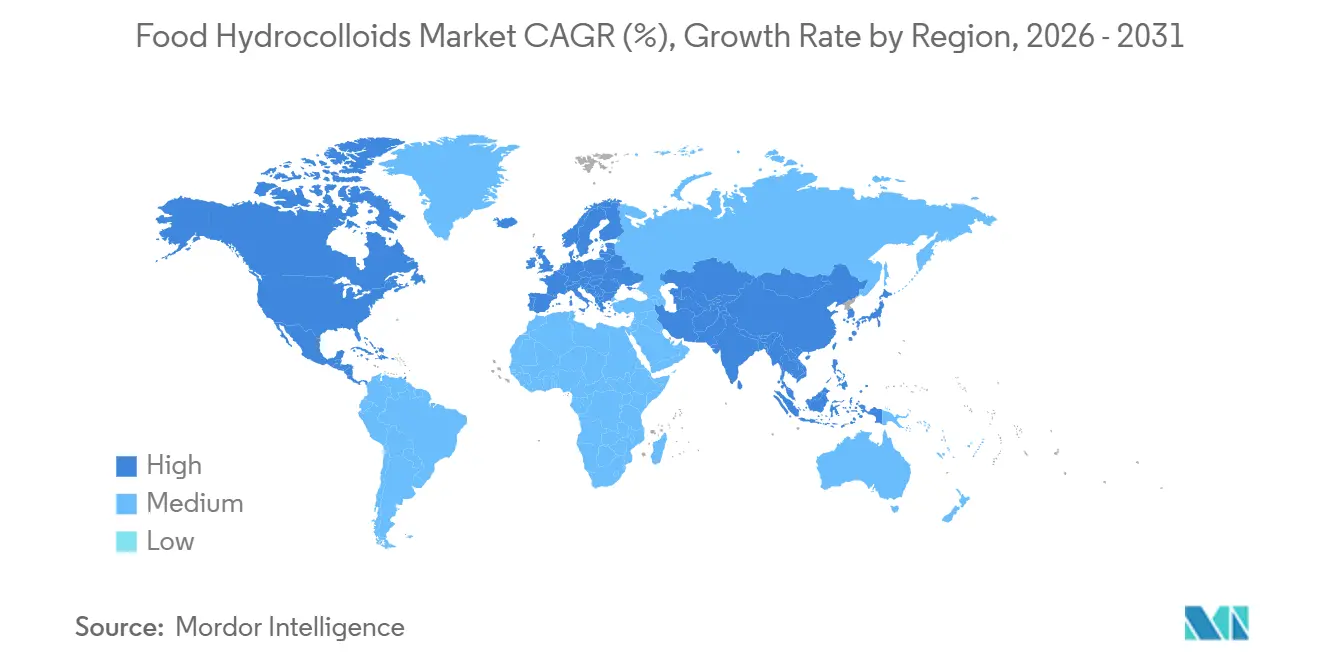

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

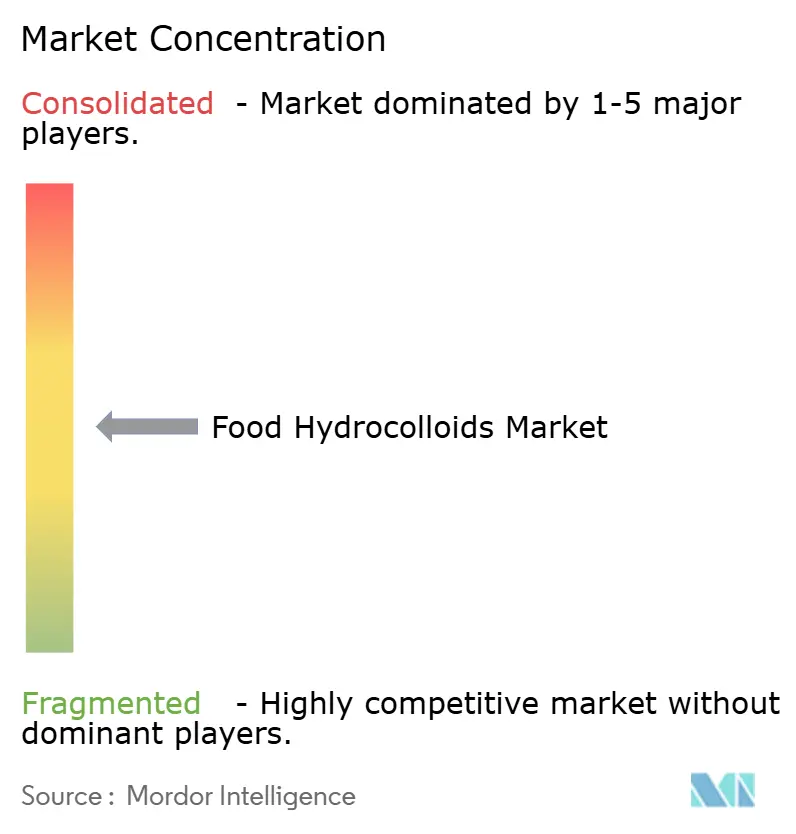

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Hydrocolloids Market Analysis by Mordor Intelligence

The food hydrocolloids market size was valued at USD 10.94 billion in 2025 and estimated to grow from USD 11.60 billion in 2026 to reach USD 15.44 billion by 2031, at a CAGR of 6.01% during the forecast period (2026-2031). The market is evolving beyond traditional commodity cycles, with a heightened emphasis on functional food ingredients that seamlessly deliver texture, stability, and clean-label compliance in various food products. This growth momentum is bolstered by precision fermentation, which mitigates agricultural risks, and seaweed biorefineries, broadening the spectrum of raw material options. Furthermore, additive manufacturing is carving out premium niches in the market, enabling manufacturers to cater to specialized consumer demands. Key competitive focal points include securing botanical and microbial feedstocks, navigating regulatory challenges, and aligning with consumer preferences that favor recognizable plant sources. The increasing demand for clean-label products and sustainable sourcing practices is driving innovation and reshaping product development strategies. As the landscape evolves, strategic investments in capacity, traceable sourcing, and technical services are becoming pivotal in defining competitive trajectories. Companies are also focusing on enhancing their R&D capabilities to develop innovative solutions that meet the dynamic needs of the food and beverage industry.

Key Report Takeaways

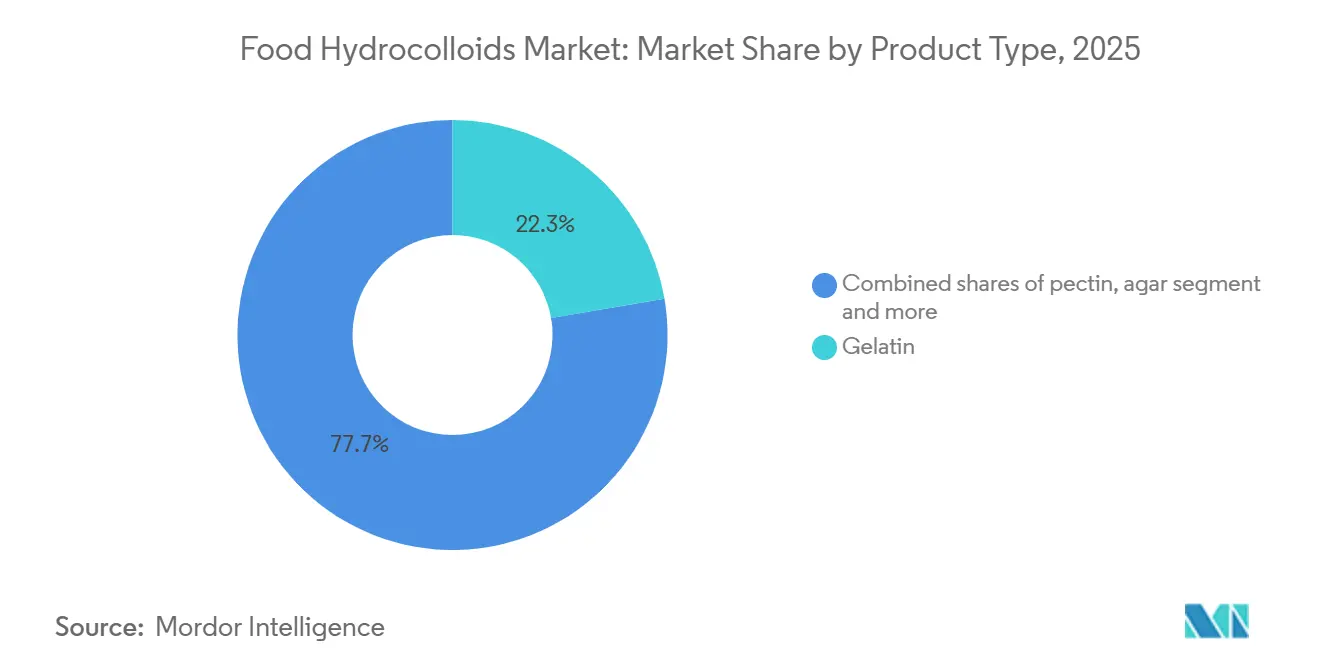

- By type, gelatin led the type segment with 22.30% food hydrocolloids market share in 2025, while pectin recorded the fastest 7.79% CAGR through 2031.

- By form, powder forms controlled 71.44% of the food hydrocolloids market size in 2025; liquid concentrates posted a 6.54% CAGR for 2026-2031.

- By source, botanical sources commanded 53.45% value share in 2025; microbial fermentation grew at a 5.95% CAGR through 2031.

- By application, bakery and confectionery generated 28.77% of the 2025 demand, whereas dairy and desserts advanced at a 6.77% CAGR to 2031.

- By geography, North America captured 33.45% revenue in 2025; Asia-Pacific is on track for a 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Hydrocolloids Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Analysis |

|---|---|---|---|

| Hydrocolloids Gain Traction in Processed Foods | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Clean-label and plant-based ingredient preference | +1.5% | North America, Europe, APAC (Asia-Pacific) urban centers | Long term (≥ 4 years) |

| Functional role in gluten-free and low-fat products | +0.8% | North America and Europe core, spillover to APAC | Medium term (2-4 years) |

| Biorefinery-grade seaweed valorization boosts supply security | +0.6% | APAC core (China, Indonesia, Philippines), spillover to Europe | Long term (≥ 4 years) |

| 3D food printing needs precision rheology ingredients | +0.4% | North America and Europe innovation hubs | Long term (≥ 4 years) |

| Edible and biodegradable packaging films adoption | +0.5% | Europe regulatory push, APAC manufacturing scale | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding use of hydrocolloids as thickening and gelling agents in processed and convenience foods

Ready-to-eat meal manufacturers are embedding hydrocolloid systems to extend ambient shelf life without refrigeration, a capability that matters less for food safety in developed markets than for enabling e-commerce fulfillment models where last-mile cold chain remains prohibitively expensive. Xanthan gum and guar gum blends now stabilize plant-based meat analogs by binding water released during freeze-thaw cycles, preventing the syneresis that plagued early-generation products. Carrageenan maintains suspension in high-protein beverages, addressing a formulation challenge where whey and pea protein isolates precipitate under acidic pH conditions common in fruit-flavored drinks. The shift toward smaller household sizes in urban Asia is driving single-serve packaging formats that require hydrocolloids to maintain viscosity across wider temperature ranges during distribution. Locust bean gum is gaining traction in ambient dessert cups where it delivers creamy mouthfeel without the refrigeration infrastructure that limits distribution in tier-2 and tier-3 cities across India and Southeast Asia.

Clean-label and plant-based ingredient preference

Pectin's accelerated adoption reflects a strategic calculation by food manufacturers: replacing modified starches with fruit-derived hydrocolloids enables "no artificial ingredients" claims across retail channels. According to data from CBI, the Ministry of Foreign Affairs, clean-label products are expected to account for over 70% of product portfolios by 2025-2026, up from 52% in 2021[1]Source: CBI, “Which trends offer opportunities or pose a threat on the European natural food additives market,” cbi.eu. Agar, traditionally used in Asian desserts, is now appearing in European plant-based cheese formulations, where it replicates the melt-and-stretch properties of casein without triggering allergen declarations. The European Food Safety Authority's 2024 re-evaluation of carrageenan, which reaffirmed its safety profile while tightening specifications for degraded forms, has paradoxically strengthened demand for traceable seaweed supply chains that can document molecular weight distributions. Beyond formulation, clean label positioning supports premium pricing models, enabling companies to justify higher input costs. As a result, hydrocolloids are now viewed as strategic tools for brand differentiation, favoring suppliers that offer verified natural sourcing, transparent production practices, and consistent technical reliability.

Functional role in gluten-free and low-fat products

Xanthan gum has emerged as the go-to structure-builder in gluten-free baking, stepping in for the viscoelastic network typically offered by wheat gluten. However, formulators have found that blending xanthan gum with guar gum in a 60:40 ratio effectively diminishes the gummy texture often linked to subpar gluten-free products. Also, the EFSA's re-evaluation of xanthan gum confirms its safety profile even for infant applications, providing regulatory confidence for expanded use across sensitive consumer segments. In the realm of low-fat dairy, manufacturers are turning to microparticulated whey protein and carrageenan systems as substitutes for milkfat. This shift is crucial, as these alternatives replicate the cream's lubricity, and fat reduction is known to compromise mouthfeel perception more than flavor intensity. Methylcellulose, though a modified cellulose and not a conventional hydrocolloid, is playing a pivotal role in plant-based burger patties. It's helping them release moisture and shrink during cooking, mimicking ground beef behavior. This addresses a sensory gap that previously hindered repeat purchases of meat alternatives. As the gluten-free market matures, the criteria for selecting hydrocolloids are evolving. It's no longer just about "functional adequacy" but rather achieving a standard that's "indistinguishable from wheat-based counterparts." Meeting this benchmark often necessitates multi-component systems over single-ingredient solutions.

Biorefinery-grade seaweed valorization boosts supply security

In China and Indonesia, integrated seaweed processing facilities are extracting carrageenan, alginate, and agar from the same biomass feedstock. They then route the lower-grade fractions to produce animal feed and biostimulants. This cascading value model not only boosts processor margins but also stabilizes the hydrocolloid supply. Norway is leveraging its offshore aquaculture infrastructure, initially set up for salmon farming, to cultivate sugar kelp for alginate production. This infrastructure offers sheltered growing sites and established permitting frameworks, significantly cutting down regulatory lead times. In the Philippines, the carrageenan industry is shifting to contract farming models. Here, processors supply seedlings and offer technical assistance to coastal communities. This approach not only secures the supply but also ensures traceability, meeting the EU's due diligence standards for deforestation-free commodities. Thanks to evolving biorefinery economics, previously overlooked seaweed species are now commercially viable. For instance, Sargassum, once deemed a nuisance bloom in the Caribbean, is now being harvested for alginate extraction, turning an environmental challenge into a valuable feedstock. As climate adaptation pushes seaweed cultivation into deeper offshore zones where temperature and nutrient variability are more stable, it is necessitating capital-intensive mooring systems. However, this shift promises a more consistent quality of carrageenan compared to traditional intertidal farming.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price and supply chain volatility | -0.7% | Global, acute in APAC and Middle East | Short term (≤ 2 years) |

| Stringent additive regulations and ingredient perception issues | -0.5% | Europe and North America regulatory cores | Medium term (2-4 years) |

| Seaweed biomass diversion to biostimulant and methane-reduction uses | -0.3% | APAC production zones, Europe demand centers | Long term (≥ 4 years) |

| Anti-dumping tariffs on Chinese xanthan gum | -0.2% | North America and Europe import markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-material price and supply chain volatility

Hydrocolloid processing complexity creates supply chain vulnerabilities and cost pressures that particularly impact smaller manufacturers and emerging market applications. Indonesia's seaweed industry exemplifies these challenges, where limited processing capabilities and unoptimized supply chains prevent capture of higher value-added opportunities in carrageenan and agar production[2]Source: United Nations Industrial Development Organization, "Indonesia’s Seaweed Industry as Key Sources of Growth", hub.unido.org . In early 2025, monsoon failures in Rajasthan, India's primary production hub, also led to a surge in guar gum prices. This incident underscored the concentration risk tied to botanicals reliant on single-origin geographies. Buyers of carrageenan, facing this climate-related supply shock, opted for inventory drawdowns over reformulation. This choice highlighted that the costs of switching often surpass short-term price premiums. Production costs for corn-derived xanthan gum closely follow glucose syrup prices, which are, in turn, influenced by global maize markets. This creates a transmission mechanism where mandates for biofuels and demand for livestock feed have indirect repercussions on hydrocolloid economics. Forward contracting is becoming standard practice for high-volume buyers, yet this risk management tool is unavailable to small and medium food manufacturers who lack the balance sheet capacity to commit to annual volumes, creating a bifurcated market where large players secure preferential pricing and supply assurance

Stringent additive regulations and ingredient perception issues

In 2025, the European Food Safety Authority tightened purity standards for food additives[3]Source: ESFA, "Food additives", efsa.europa.eu. This move compelled hydrocolloid suppliers to enhance their filtration and purification methods. While larger players adapted, many smaller processors found the necessary capital investments daunting, leading some to exit the market and further consolidating supply among the industry's giants. Carrageenan, a widely used hydrocolloid, came under fire after social media campaigns linked it to digestive problems. Although peer-reviewed studies haven't substantiated these claims, the controversy swayed retailers to adjust their private-label specifications, leaning towards alternative stabilizers for their organic product lines. In 2024, the U.S. Food and Drug Administration issued guidance on "natural" claims, ruling that chemically modified hydrocolloids are ineligible for the "natural" label. This decision favored gum arabic and guar gum but sidelined carboxymethylcellulose and hydroxypropyl methylcellulose. Studies on consumer perceptions reveal a linguistic bias: hydrocolloid names derived from Greek or Latin roots, like carrageenan and xanthan, evoke more negative reactions than their common-language counterparts, such as guar gum and locust bean gum. This bias is swaying ingredient choices, regardless of functional performance. Furthermore, regulatory inconsistencies across markets compel multinational manufacturers to tailor their formulations to specific regions. This challenge intensifies with hydrocolloid specifications; for instance, food-grade carrageenan in Asia might need extra testing to align with European standards, potentially extending supply chain lead times by 8-12 weeks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gelatin Dominance and Pectin Clean-Label Surge

Gelatin commanded a 22.30% market share in the year 2025, bolstered by its unique properties in gummy confections and dairy products. Its thermoreversible gelling and melt-in-mouth characteristics stand unrivaled by plant-based substitutes. Furthermore, gelatin's collagen-derived structure offers textural qualities that are hard for formulators to achieve with botanical hydrocolloids. Gelatin's animal-derived nature gives it an edge in markets prioritizing protein fortification over plant-based alternatives. This is especially true in sports and clinical nutrition, where amino acid profiles dictate product choices. Yet, as manufacturers pivot to cater to flexitarian and vegan consumers, gelatin's growth lags behind the broader market.

Pectin is set to expand at a 7.79% CAGR through 2031. Its growth is driven by its plant-based origin, allowing for "no artificial ingredients" claims that fetch a price premium in North American retail. Once limited to jams and jellies, pectin is now making inroads into dairy alternatives and confectionery applications. Health-conscious consumers, who meticulously examine ingredient lists, are the primary audience for pectin's clean-label advantage. This demographic closely aligns with organic and non-GMO buyers, often willing to pay a premium for perceived naturalness. Innovations in pectin extraction and modification are producing grades with enhanced heat stability and calcium reactivity. These advancements are overcoming previous formulation constraints tied to specific pH and temperature ranges.

By Form: Powder Economics and Liquid Efficiency Gains

In 2025, powder formulations captured a dominant 71.44% of the market share, thanks to their lower shipping costs, extended shelf life, and compatibility with existing dry-blending infrastructures in food plants. The flexibility of powder formulations, allowing for batch-to-batch adjustments, further cements their dominance. Unlike liquid systems, which require maintaining multiple SKU inventories, powder blending offers greater adaptability. Powder hydrocolloids seamlessly integrate into standardized quality control protocols, such as moisture content testing and microbial screening. Powder forms shine in applications needing long-term storage or seasonal formulation variations. Dry ingredients boast stability for 18-24 months, outpacing the 6-9 month stability of liquid concentrates, even under refrigeration.

Liquid concentrates are on the rise, growing at a 6.54% CAGR. Manufacturers are prioritizing labor savings and dust control, even if it means overlooking raw material costs. This trade-off proves economically sound when production volumes are high enough to amortize the costs of hydration equipment and floor space. Dairy plants are increasingly turning to liquid carrageenan and pectin. These liquid forms sidestep the sanitation challenge of powder residues in mixing tanks, a hurdle for clean-in-place systems. Moreover, they consume less water in cleaning cycles. Adoption of liquid forms is notably among multinational manufacturers, especially those near hydrocolloid production sites.

By Source: Botanical Leadership and Microbial Innovation

Botanical sources commanded a 53.45% market share for the year 2025, driven by ingredients like guar gum, locust bean gum, pectin, and gum arabic. These plant-derived ingredients resonate with clean-label positioning but tether supply to agricultural cycles. Consumer preference leans towards recognizable ingredient origins. Marketing research consistently highlights that messaging "derived from plants" boosts purchase intent more than "produced through fermentation," even if the latter boasts superior sustainability metrics. This connection, influenced by climate variability, introduces price volatility that manufacturers find challenging to hedge. Guar gum, predominantly sourced from Rajasthan, India, faces geographic risks. Yet, alternative regions in Pakistan and Africa struggle to match the yield consistency of Indian production. Civil conflicts and climate-induced desertification threaten its production continuity, prompting some manufacturers to consider synthetic emulsifiers as backup options, despite the clean-label trade-offs.

Forecasted to grow at a 5.95% CAGR through 2031, microbial fermentation offers unmatched production consistency and potential for genetic optimization. These advantages, unattainable through botanical extraction, are crucial for food manufacturers aiming to minimize formulation variability. Xanthan gum and gellan gum, both derived from fermentation, are reaping benefits from strain engineering advancements. The regulatory landscape for fermentation-derived ingredients is solidifying. FDA and EFSA (European Food Safety Authority) approvals for precision fermentation proteins set a precedent that hydrocolloid producers can leverage for their own GRAS (Generally Recognized As Safe) notifications and novel food applications.

By Application: Bakery Dominance and Dairy Innovation

In 2025, bakery and confectionery applications accounted for 28.77% of hydrocolloid demand. This leading position stems from hydrocolloids' pivotal roles in extending shelf life, enhancing moisture retention, and crafting indulgent textures in cakes, cookies, and candies. Such attributes drive repeat purchases in impulse-driven categories. Bakery manufacturers are increasingly leveraging hydrocolloids to cut sugar and fat content while preserving sensory qualities. This reformulation push aligns with government-mandated nutritional labeling and industry commitments to bolster public health. Meanwhile, confectionery innovations are targeting texture-modified products for both the elderly and children. Here, hydrocolloids play a crucial role in crafting softer, chew-friendly formats, broadening the demographic appeal beyond traditional segments.

Dairy and dessert applications are projected to grow at a 6.77% CAGR through 2031. This growth is fueled by the rise of plant-based yogurt and ice cream formulations. These alternatives rely on stabilizer systems to mimic the structure and mouthfeel typically provided by milk proteins and fats in conventional dairy. Manufacturers are reformulating dairy desserts, swapping out gelatin for carrageenan and pectin. Such positioning not only commands premium pricing but also broadens market reach. Ice cream producers are turning to combinations of locust bean gum and guar gum to manage ice crystal growth during freeze-thaw cycles. This control is especially crucial for home storage, where temperature fluctuations exceed those in commercial cold chains.

Geography Analysis

In 2025, North America commanded a dominant 33.45% share of the market revenue. This leadership can be attributed to the region's hub of food ingredient innovation, expedited FDA GRAS approval processes, and consumers' readiness to pay a premium for functional benefits in packaged foods. The United States has taken the lead with its advanced clean-label movement, driving demand for hydrocolloids. Meanwhile, Canada's plant-based food sector is outpacing the United States fueled by government dietary guidelines advocating a reduction in animal protein consumption. In Mexico, as rising incomes and urbanization tilt consumption towards packaged goods, the processed food industry is expanding. However, the market's price sensitivity leans towards more affordable hydrocolloids, such as modified starches, rather than premium choices like gum arabic and agar.

Asia-Pacific is set to lead with a projected CAGR of 7.25% through 2031, driven by China's modernization of food safety standards, the growth of organized retail in India, and the youthful demographics coupled with increasing disposable incomes in Southeast Asia. China's 2025 revisions to its food additive standards aligned more closely with international hydrocolloid specifications. This move alleviated the regulatory challenges that once compelled multinationals to create unique formulations for the Chinese market. Major seaweed producers, Indonesia and the Philippines, are enhancing their domestic capabilities by processing carrageenan and agar. This vertical integration not only amplifies regional value capture but also diminishes reliance on exports.

Europe's stringent regulations, highlighted by EFSA's thorough evaluations of additives, set high entry barriers. Clean-label innovation is spearheaded by Germany and France. Post-Brexit, the UK has charted a regulatory course distinct from EU norms. This divergence presents challenges for hydrocolloid suppliers, who now face dual approval processes. In South America, Brazil and Argentina dominate the hydrocolloid landscape, primarily driven by their meat processing sectors' need for water and fat binding. The Middle East and Africa, while smaller markets, showcase significant growth potential. This is especially evident in halal-certified products, where alternatives to gelatin, such as agar and carrageenan, are carving out a larger market share. This trend is bolstered as Muslim-majority nations refine and elevate their food processing industries.

Competitive Landscape

The food hydrocolloids market is characterized by a moderate concentration. Global ingredient conglomerates dominate high-volume commodity segments, while specialized processors carve out niches in technical grades and application-specific formulations. Cargill, Incorporated, Tate & Lyle PLC (CP Kelco), and Archer Daniels Midland, through vertical integration in livestock rendering and corn wet milling, have secured a dominant position in the supply of hydrocolloids. This strategy affords them cost advantages that smaller players, lacking comparable scale in upstream raw materials, find hard to match. Meanwhile, Kerry Group and DSM-Firmenich are adopting a distinct approach.

They bundle hydrocolloids with complementary ingredients such as flavors, proteins, and vitamins, crafting integrated solutions. This strategy not only elevates customer switching costs but also pivots competition from mere pricing to enhanced technical service capabilities. Suppliers offering pilot plant testing, regulatory documentation, and sensory optimization are reaping higher margins compared to those merely distributing undifferentiated ingredients. Emerging white-space opportunities lie in precision fermentation-derived hydrocolloids. Startups are harnessing engineered microorganisms to produce traditionally plant-sourced gums, boasting superior purity and consistency. If these production costs achieve commercial viability through scaling, they could disrupt existing botanical supply chains.

Patent analyses indicate a trend: innovation is gravitating towards hydrocolloid blends and advanced delivery systems, rather than entirely new molecules. Given that most traditional hydrocolloids are off-patent, the competitive focus has shifted. It's now more about application expertise than the molecular composition. This evolution benefits companies with robust technical service divisions, overshadowing those that prioritize manufacturing efficiency. The most intense competition is observed in xanthan gum. An expansion of fermentation capacity in China has led to a global oversupply, squeezing margins. In response, Western producers are prioritizing quality certifications, like ISO 22000, and ensuring supply reliability. This strategy resonates with risk-averse food manufacturers, especially those who've faced past supply disruptions.

Food Hydrocolloids Industry Leaders

-

Archer Daniels Midland Company

-

Kerry Group plc

-

International Flavors and Fragrances Inc.

-

Cargill, Incorporated.

-

Tate & Lyle

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Nexira launched the Fair For Life (FFL) certified range of its acacia gum products, namely inavea and Fibregum. This certification emphasizes sustainability and ethical sourcing, spaning the entire value chain, starting from African producers and culminating in manufacturing in France. The inavea product line variants such as inavea Baobab and Acacia, Carob and Acacia, and Cinnamon and Acacia, all clinically validated, are tailored for specific wellness applications in markets like functional beverages, bakery, and dietary supplements.

- May 2025: Sarda Bio Polymers introduced and showcased clean-label, plant-based hydrocolloid solutions for meat and alternative protein applications at the Frankfurt IFFA trade fair. Their offerings include guar gum, cassia tora gum, konjac, xanthan, carrageenan, tamarind xyloglucan, and CMC, designed to enhance texture with minimal processing while emphasizing sustainability and performance.

- October 2024: Jungbunzlauer AG has initiated construction of a USD150 million facility in Canada to produce xanthan gum, a fermentation-derived ingredient used in food, cosmetic, and pharmaceutical products. The facility will utilize locally sourced corn as the primary raw material.

- January 2024: International Flavors and Fragrances Inc. launched Grindsted Pectin FB 420 for baking applications. Grindsted Pectin FB 420 is ideal for baking applications. It has unique sensory qualities for bake-stable fruit fillings and is label-friendly and process-efficient.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the food hydrocolloids market as all plant, microbial, animal, and seaweed-derived polymers intentionally added to food formulations to thicken, gel, stabilize, or replace fat, measured in value terms at the first point of commercial sale.

Scope exclusion: pharmaceutical, cosmetic, and industrial hydrocolloids lie outside this assessment.

Segmentation Overview

-

By Type

- Alginate

- Agar

- Pectin

- Guar Gum

- Locust Bean Gum

- Gum Arabic

- Gelatin

- Carrageenan

- Xanthan Gum

- Other Hydrocolloids

-

By Form

- Powder

- Liquid

-

By Source

- Botanical

- Microbial

- Animal

- Synthetic

-

By Application

- Bakery and Confectionery

- Dairy and Desserts

- Beverages

- Meat and Meat Products

- Soups, Sauces and Dressings

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews were held with procurement managers at dairy, bakery, and plant-based beverage firms across North America, Europe, and Asia Pacific, alongside distributors and formulation chemists. Their inputs clarified average selling prices, functional replacement ratios, and emerging demand pockets, thereby validating desk assumptions and calibrating regional growth expectations.

Desk Research

Mordor analysts first mapped the supply chain using public trade flows, customs data, and production statistics from sources such as UN Comtrade, FAOSTAT, and the United States International Trade Commission. We enriched volume cues with regional association publications like the European Food & Drink Federation and clean-label ingredient registries. Company 10-Ks, investor decks, and press articles retrieved through Dow Jones Factiva helped us benchmark manufacturer revenues. Paid databases, notably D&B Hoovers for company splits and Questel for recent gelling-agent patents, supplied additional granularity. The list above is illustrative; many further public and proprietary references supported fact-finding.

Market-Sizing & Forecasting

A top-down reconstruction that combined production tonnage with average selling prices by polymer class established the 2025 baseline. Results were stress-tested using selective bottom-up checks, supplier roll-ups, and channel volume probes to refine totals. Key model drivers included gelatin and pectin inclusion rates in bakery mixes, dairy dessert penetration, clean-label adoption ratios, import tariff trends, and seaweed harvest yields. Multivariate regression, informed by expert consensus on calorie-reduction trends and retail launch pipelines, generated the 2025-2030 outlook. Gaps in granular tonnage data were bridged through regional trade proxies and calibrated usage coefficients.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance monitoring against quarterly trade and pricing signals, and a senior sign-off. The model refreshes each year, with interim revisions triggered by material events such as regulatory bans on specific gums or abrupt seaweed supply shocks.

Why Mordor's Food Hydrocolloids Baseline Commands Reliability

Published estimates often diverge because firms pick varying ingredient sets, pricing anchors, and update cadences.

Key gap drivers include differing inclusion of non-food applications, one-off survey multipliers, currency year distortions, and less frequent refresh cycles that overlook swift shifts in clean-label demand. By aligning scope strictly to food-grade polymers, applying dual validation, and revisiting prices quarterly, Mordor provides a balanced midpoint that decision-makers can trace back to transparent variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.17 B (2025) | Mordor Intelligence | |

| USD 11.96 B (2023) | Regional Consultancy A | Bundles pharmaceutical and personal-care use, older currency base |

| USD 11.20 B (2023) | Global Consultancy B | Relies on ingredient shipment weights without ASP cross-checks |

| USD 10.40 B (2024) | Industry Research C | Uses single-source producer survey, limited geographic coverage |

In sum, the disciplined scope, dual-track modeling, and continuous validation followed by Mordor Intelligence yield a dependable benchmark that clients can replicate and stress-test with minimal additional data collection.

Key Questions Answered in the Report

What is the current size of the hydrocolloids market and how fast is it growing?

The hydrocolloids market is valued at USD 11.60 billion in 2026 and is projected to reach USD 15.44 billion by 2031, reflecting a 6.01% CAGR.

Which hydrocolloid type leads the market today?

Gelatin holds the largest share, accounting for 22.30% of global revenue in 2025 due to its wide use in pharmaceuticals, confectionery, and traditional food applications.

Which hydrocolloid segment is expanding the fastest?

Pectin’s plant origin, circular economy sourcing from citrus and apple side streams, and suitability for low-sugar and plant-based products support a 7.79% CAGR to 2031.

Which region offers the highest growth potential for hydrocolloid suppliers?

Regulatory modernization in China, retail expansion in India, and seaweed investment in Southeast Asia combine for a 7.25% regional CAGR through 2031 for Asia Pacific.

Page last updated on: