Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.97 Billion |

| Market Size (2026) | USD 6.21 Billion |

| Market Size (2031) | USD 6.46 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Food Ingredient Market Analysis by Mordor Intelligence

The Brazil food ingredient market size is expected to grow from USD 5.97 billion in 2025 to USD 6.21 billion in 2026 and is forecast to reach USD 6.46 billion by 2031 at 4.01% CAGR over 2026-2031. Health-driven reformulation, front-of-pack warning labels, and rising household demand for functional foods are reshaping procurement strategies for processors. Ingredient suppliers are pivoting from bulk commodities toward biosolutions and clean-label inputs that deliver a higher margin per kilogram, even though this shift moderates volume growth. Multinational players continue to invest heavily; Cargill alone deployed USD 1.1 billion between 2022 and 2026, yet local formulators remain competitive by leveraging proximity to soy-crushing and poultry complexes. Regulatory friction persists, but Normative Instruction 281 has marginally eased dossier requirements by accepting foreign safety evaluations.

Key Report Takeaways

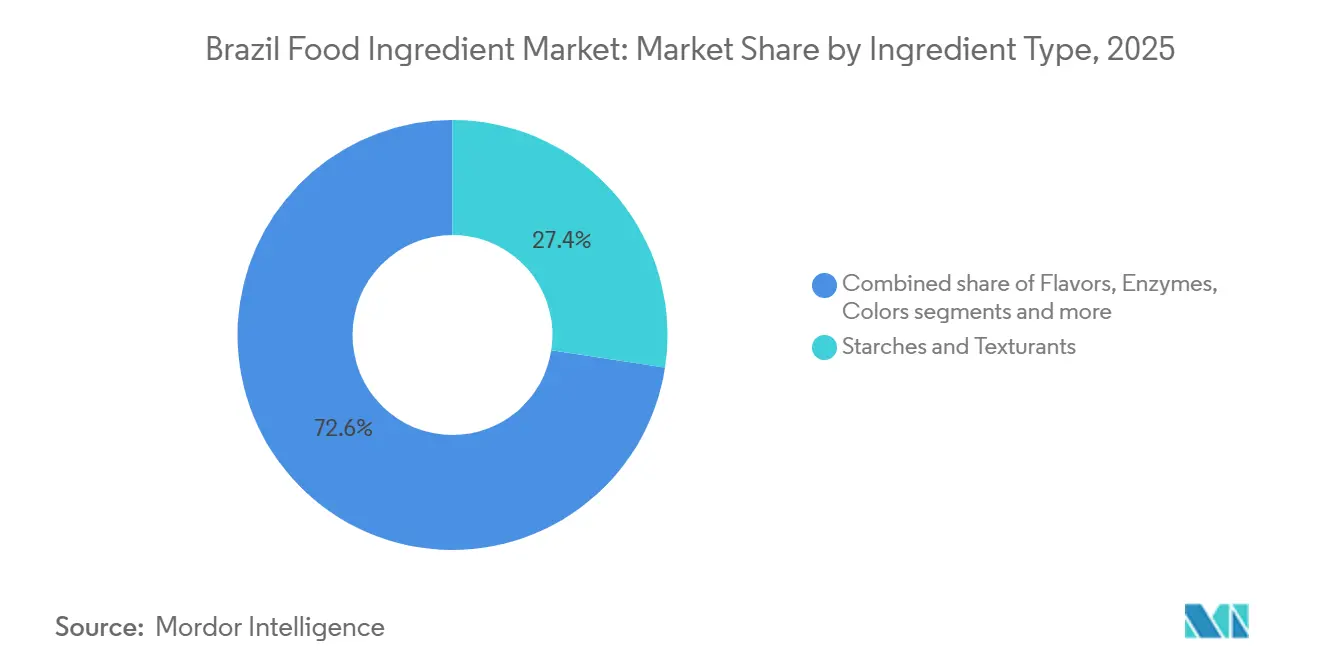

- By ingredient type, starches and texturants captured 27.42% of the Brazil food ingredient market share in 2025, while enzymes are projected to expand at a 5.43% CAGR through 2031.

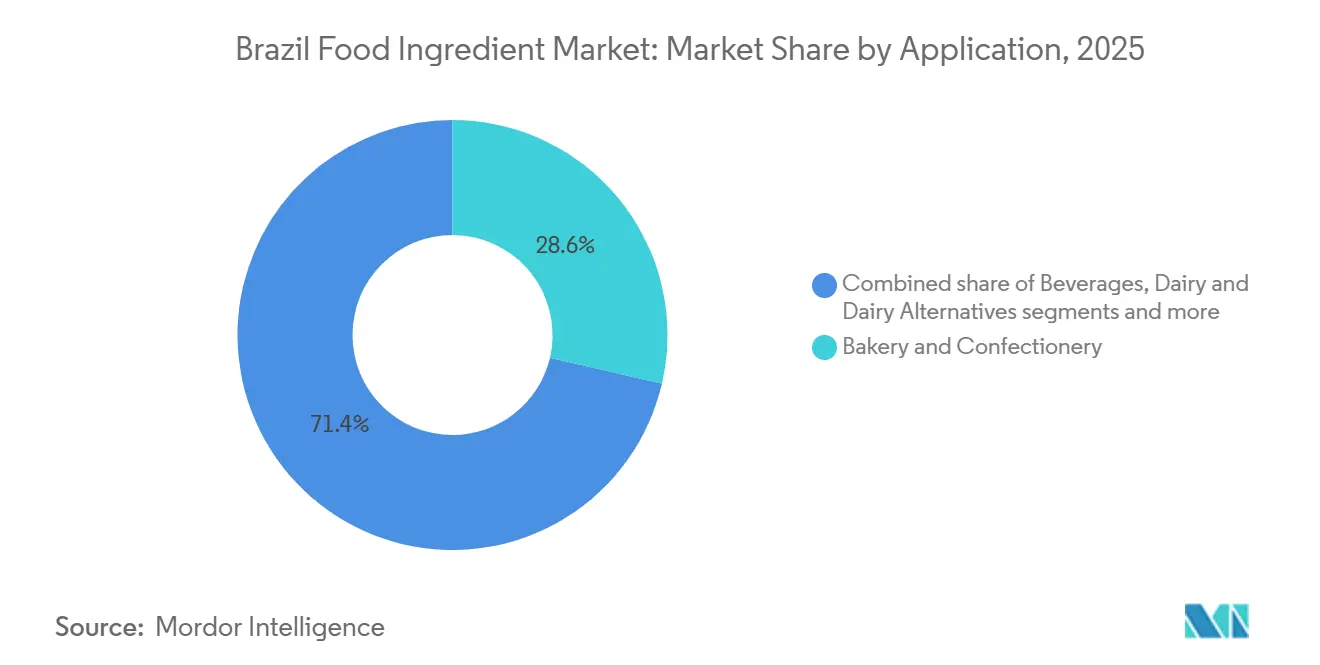

- By application, bakery and confectionery accounted for 28.64% share of the Brazil food ingredient market size in 2025, whereas sweet and savory snacks are advancing at a 5.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Food Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened consumer focus on preventive nutrition and better-for-you diets | +0.8% | National, with early gains in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Increasing preference for natural, clean-label, and minimally processed ingredients | +1.1% | National, strongest in Southeast and South regions | Short term (≤ 2 years) |

| Expansion of Brazil's food and beverage processing industry | +0.7% | National, concentrated in São Paulo, Paraná, Minas Gerais | Long term (≥ 4 years) |

| Growing adoption of vegan, plant-based, and cruelty-free inputs | +0.6% | National, urban centers leading adoption | Medium term (2-4 years) |

| Acceleration in fortified, functional, and value-added product launches | +0.9% | National, with premium segments in Southeast | Short term (≤ 2 years) |

| Advancements in food processing and ingredient technologies | +0.5% | National, technology hubs in São Paulo, Campinas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened consumer focus on preventive nutrition and better-for-you diets

Consumer focus on preventive nutrition and healthier dietary choices is driving demand for innovative food ingredients in Brazil. Rising health consciousness, particularly in response to chronic conditions like diabetes, is a key factor. The International Diabetes Federation reports that the number of adults (aged 20–79 years) with diabetes in Brazil reached 16.6 million in 2024 and is projected to grow to 24.0 million by 2050 [1]Source: International Diabetes Federation, "Brazil - Diabetes Country Report 2000 — 2050," diabetesatlas.org. This has increased interest in clean-label ingredients, such as Cargill’s starches and texturants, which offer native, label-friendly solutions for low-calorie formulations. Alternative sweeteners like Tate & Lyle's EUOLIGO® FOS and TASTEVA® M support sugar reduction while enhancing fiber content and gut health in functional snacks and beverages. Natural flavors and colors, such as DSM-Firmenich's Vibelly™ carotenoids, are replacing synthetic dyes to meet regulatory requirements and consumer demand for transparent labeling in wellness drinks. Kerry’s Puremul™ emulsifiers provide plant-based stabilization for oils and fats in dairy alternatives, while enzymes improve processing efficiency. Additionally, fermentation-derived preservatives from Kerry naturally extend shelf life, and cultures and yeasts support probiotic fortification, aligning with preventive nutrition goals. These advancements cater to urban consumers seeking fortified, low-sugar options, reflecting a broader shift toward wellness-focused consumption and driving market growth.

Increasing preference for natural, clean-label, and minimally processed ingredients

The increasing demand for natural, clean-label, and minimally processed ingredients is reshaping the food ingredient market in Brazil. Rising health awareness among consumers, coupled with regulatory measures such as ANVISA's updated labeling requirements, is driving the shift away from artificial additives. This trend is evident in the adoption of clean-label native starches, like those from Ingredion, which replace chemically modified alternatives to maintain texture in bakery products without chemical processing. Similarly, plant-derived sweeteners, such as Olam International's stevia extracts, deliver natural sweetness while supporting minimal processing in beverages. Flavors sourced from natural botanicals enhance authentic taste profiles without synthetic additives, while plant-based emulsifiers, such as those from DuPont (now part of IFF), stabilize emulsions in dairy alternatives, ensuring clean-label compliance. Natural colors from fruits and vegetables are replacing synthetic dyes in snacks, and enzymes from Novozymes improve processing efficiency while maintaining whole-food purity. Sustainable oils and fats, such as sunflower oil, provide healthier lipid bases, complemented by citric acid-based acidulants for natural pH maintenance. Fermented cultures act as natural preservatives, and yeasts enable clean fermentation for probiotic-enriched products. These innovations collectively support transparent ingredient lists, aligning with the preferences of health-conscious urban consumers seeking wellness-focused yet indulgent food options.

Expansion of Brazil’s food and beverage processing industry

The expansion of Brazil’s food and beverage processing industry is driving significant growth in the food ingredient market, with the sector expected to generate USD 233 billion in revenues in 2024, marking a 9.9% increase from 2023, as reported by the Brazilian Food Processors’ Association (ABIA) [3]Source: United States Department of Agriculture (USDA), "Food Processing Ingredients Annual - Brazil, April 2025," apps.fas.usda.gov . This growth is creating heightened demand for specialized inputs to support the booming snack and bakery production. Key contributors include ADM's modified tapioca starches, which enhance viscosity in processed sauces, and Beneo's chicory root inulin, which stabilizes low-sugar pastry fillings without crystallization. Givaudan’s bitterness-masking solutions ensure consistent flavor profiles in large-scale beverage production, while BASF’s plant-derived emulsifiers improve fat dispersion in ready-to-eat meals. Sensient’s annatto extracts maintain color vibrancy during extended processing, and AB Enzymes’ solutions accelerate hydrolysis for faster dairy analogue production. Oils and fats, such as Bunge's high-oleic sunflower varieties, provide oxidative stability for shelf-stable snacks. Additionally, acidulants like fumaric acid balance acidity in concentrates, nisin cultures act as preservatives in high-capacity packaging, and Lesaffre’s yeasts enhance bread fermentation yields. Amid record exports and increasing urban demand for convenience foods, these innovations collectively enable manufacturers to meet the evolving needs of processors with reliability and efficiency.

Growing adoption of vegan, plant-based, and cruelty-free inputs

The growing adoption of vegan, plant-based, and cruelty-free ingredients is transforming the food ingredient industry in Brazil as dietary preferences shift from niche to mainstream consumption. According to the Good Food Institute, 26% of Brazilians consume plant-based meats at least once a month, while 5% identify as vegan or vegetarian, driving demand for animal-free ingredient systems [2]Source: Good Food Institute, "The Brazilian Consumer and the Plant-based Market 2024," gfi.org.br. This trend has increased reliance on plant-based starches and texturants, such as specialty pea and tapioca solutions from Roquette, to replicate meat-like textures and binding properties. Natural plant-derived colors and flavors developed by Sensient Technologies are being incorporated to enhance sensory appeal while maintaining cruelty-free attributes. Enzyme and fermentation-based solutions from Novonesis support protein modification and flavor development in dairy and meat analogues without animal-derived inputs. Plant-based emulsifiers and stabilizers from Palsgaard are gaining traction in vegan bakery and confectionery formulations, replacing traditional egg- or dairy-based systems. Oils and fats sourced from vegetables, including specialty blends from Bunge, enable clean-label, plant-based reformulations. Additionally, acidulants, cultures, and yeast designed for plant-based fermentation help manufacturers achieve authentic taste and texture while adhering to cruelty-free claims. These innovations align with evolving consumer ethics, environmental awareness, and the growing popularity of flexitarian diets, driving structural growth in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in raw material prices and supply availability | -0.9% | National, with acute impact on cocoa, coffee, sugar supply chains | Short term (≤ 2 years) |

| Stringent ANVISA registration requirements and lengthy customs processes | -0.6% | National, affecting imported specialty ingredients | Medium term (2-4 years) |

| Logistical bottlenecks and infrastructure limitations | -0.4% | National, concentrated in North and Northeast regions | Long term (≥ 4 years) |

| Increasing consumer skepticism toward artificial additives and synthetic ingredients | -0.5% | National, strongest in urban Southeast markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuations in raw material prices and supply availability

Fluctuations in raw material prices and supply availability are creating significant challenges for the food ingredient industry in Brazil, driven by climate-impacted crops and import dependencies. These issues are particularly critical as the sector is projected to reach USD 233 billion in revenues by 2024, according to ABIA. Starches and texturants, such as Sudstarches' corn-derived products, are experiencing cost increases due to regional droughts affecting maize harvests, essential for bakery production. Alternative sweeteners like Archer Daniels Midland's inulin variants are disrupted by beet shortages, impacting sugar-reduced dairy formulations. Flavors, including Firmenich's citrus extracts, are affected by orange yield fluctuations in São Paulo, while emulsifiers like Croda's soy-based lecithins face price surges linked to soybean export growth. Colors such as Naturex's anthocyanins are vulnerable to berry supply gaps. Enzymes, including Amano Enzyme's glucose oxidase formulations, are impacted by wheat supply fluctuations, while oils and fats, such as Viterra's palm imports, are challenged by rising global freight costs and port backlogs. Other ingredients, including acidulants, preservatives, cultures, and yeasts, face similar supply chain disruptions. As processing growth outpaces domestic sourcing and competes with export demands, manufacturers are forced to adopt formulation adjustments and hedging strategies, limiting their ability to innovate and respond swiftly to market needs.

Logistical bottlenecks and infrastructure limitations

Infrastructure limitations and logistical challenges are disrupting supply chains for perishable food ingredients in Brazil, hindering timely delivery and increasing operational risks for manufacturers. Road and rail deficiencies across the vast geography delay transportation from ports to inland processors, exacerbating spoilage risks for temperature-sensitive products such as Avebe's potato starches, which rely on cold-chain logistics. Similarly, Südzucker's isomaltulose faces humidity damage in inadequate storage, compromising its quality for beverage production. Flavors derived from Mane's essential oils degrade during extended transit times, while Evonik's plant-based emulsifiers require stable temperatures to prevent separation. Novonesis natural betalains are prone to fading without refrigerated logistics, and Genencor's enzyme formulations lose activity when exposed to heat during shipments. Oils and fats, such as Cargill's specialty shea butter, are vulnerable to rancidity due to multimodal delays, including congestion at Santos port. Additional challenges include contamination risks for Roquette's malic acid in poor storage, reduced efficacy of Kemin's natural preservatives after exposure, disruptions to cryogenic handling of cultures due to power outages, and loss of viability for Angel Yeast's products in humid conditions. These persistent issues, coupled with rising export demands and urban processing hubs, force manufacturers to maintain costly inventories, hindering their ability to innovate efficiently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Enzymes Outpace Commodity Texturants

Starches and texturants held the largest share of 27.42% in the Brazil Food Ingredient Market in 2025, driven by their widespread application in bakery and confectionery products. However, growth in this segment is slowing as manufacturers increasingly adopt enzyme-modified systems that deliver equivalent viscosity at nearly 30% lower dosage, reducing overall volume demand while enhancing cost efficiency. Alternative sweeteners are also gaining traction, supported by ANVISA’s labeling reforms that encourage sugar reduction strategies. These shifts highlight a transition from bulk functionality to precision-driven ingredient optimization, reflecting evolving consumer and regulatory demands.

Enzymes are anticipated to grow at a compound annual growth rate (CAGR) of 5.43% during 2026–2031, the fastest among ingredient types. This growth is attributed to the adoption of biocatalysts by processors aiming to achieve clean-label objectives without compromising texture, shelf life, or processing efficiency. Suppliers such as Novozymes are advancing enzyme solutions for viscosity control, dough strengthening, and sugar reduction, aligning with reformulation trends. Meanwhile, flavors and colors are moving toward natural sourcing, supported by regulatory clarity under RDC 8/2024. Companies like Givaudan are expanding their portfolios, including natural colors such as spirulina blues and turmeric yellows. Collectively, these developments underscore a shift toward value-added, regulation-compliant, and application-specific innovations in Brazil’s food manufacturing industry.

By Application: Snacks and Dairy Alternatives Drive Ingredient Innovation

Bakery and confectionery held the largest share, accounting for 28.64% of ingredient demand in 2025. However, these segments are experiencing maturity as per-capita indulgence slows, prompting reformulation efforts. Companies like Givaudan are introducing enzyme-modified starches and clean-label flavors to maintain sensory appeal without increasing caloric content. Beverages are also witnessing accelerated adoption of natural colors and flavors, enhancing visual differentiation and reinforcing consumer perceptions of clean-label quality. Sweet and savory snacks, projected to grow at a CAGR of 5.38% through 2031, represent the fastest-growing application. Urbanization and the expansion of e-commerce are driving impulse purchases of portion-controlled formats. Ingredient manufacturers, such as Ingredion Incorporated, are supplying starches and texturants to improve texture, crispness, and shelf life, while Tate & Lyle’s alternative sweeteners support reduced-sugar offerings aligned with health-conscious consumption.

Dairy and dairy alternatives are diverging, with traditional dairy products fortified with calcium and vitamin D to counter the rise of plant-based substitutes. Oat and almond beverages are leveraging enzymes from Novonesis to enhance mouthfeel and prevent sedimentation, addressing prior technical challenges. Meat and meat alternatives are converging through hybrid formulations blending plant and animal proteins, requiring tailored texturants and emulsifiers from Palsgaard. Additionally, sauces, dressings, and condiments are incorporating modified starches and clean-label emulsifiers to ensure freeze-thaw stability, meeting the needs of chilled meal kits. Ready-to-eat and fortified foods are integrating functional ingredients at premium pricing, reflecting Brazil’s evolving focus on health and convenience.

Geography Analysis

The Southeast and South regions of Brazil, including São Paulo, Rio de Janeiro, Minas Gerais, Paraná, and Rio Grande do Sul, hold the largest share of specialty-ingredient imports in 2024. These regions benefit from advanced processing capabilities and a consumer base willing to pay premiums for clean-label, natural, and functional product attributes. Manufacturers such as Palsgaard and Novonesis, specializing in emulsifiers, natural colors, and enzymes, are strategically located in these areas to cater to high-demand segments like dairy alternatives, bakery, and confectionery. This regional concentration supports timely innovation, regulatory compliance, and efficient supply chain operations.

São Paulo state serves as a critical hub for ingredient consumption, supported by a USD 233 billion food-processing industry and a population of 215 million, as reported by the USDA in 2024. Industrial clusters in Campinas, Piracicaba, and the ABC Paulista region benefit from proximity to ports, universities, and research and development centers. Leading ingredient manufacturers, including Ingredion Incorporated (starches and texturants), Tate & Lyle (alternative sweeteners), and Givaudan (flavors), leverage these advantages to optimize logistics and reduce operational costs, ensuring competitive distribution compared to more dispersed locations.

Emerging growth opportunities are evident in the Northeast, North, and Central-West regions. The Northeast is experiencing increased urbanization and rising disposable incomes, driving demand for packaged and fortified foods. The North region utilizes the Manaus Free Zone tax benefits and Amazon River logistics to supply inland processors at competitive costs. Central-West states such as Mato Grosso, Mato Grosso do Sul, and Goiás capitalize on agricultural surpluses to provide raw materials for starches, oils, and other functional ingredients. Companies like Cargill strengthen supply chain resilience in these regions, supporting Brazil’s diverse ingredient market and ensuring nationwide access to functional and clean-label solutions.

Competitive Landscape

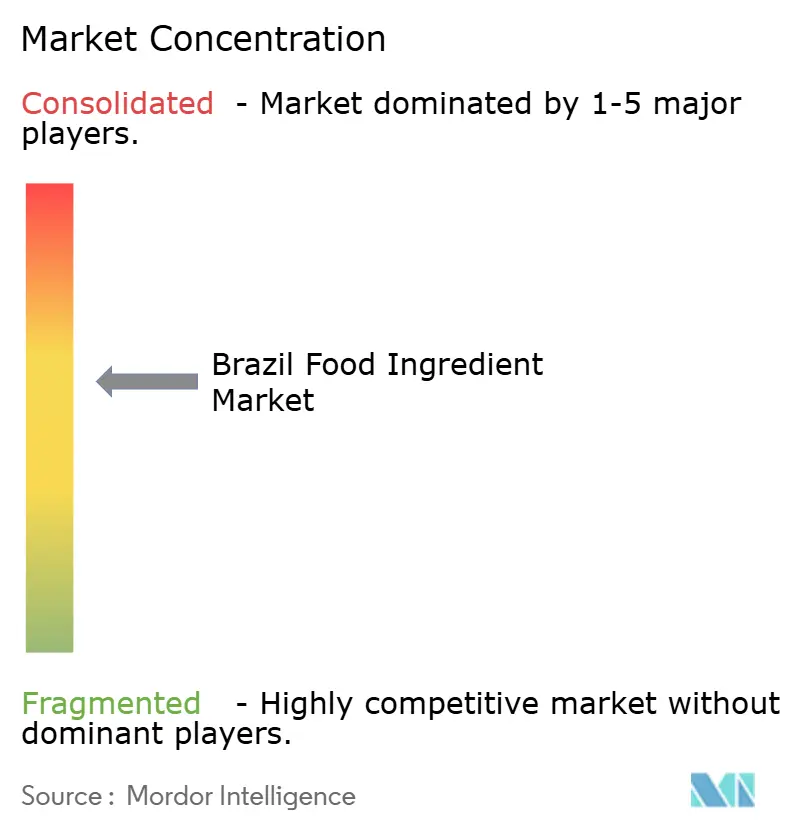

The Brazil Food Ingredient Market is moderately consolidated, with multinational companies utilizing their scale, diverse portfolios, and technical expertise to compete with specialized regional players and commodity traders entering value-added segments. Companies such as Cargill, ADM, and Kerry Group utilize vertical integration, from raw material processing to ingredient formulation, to offer bundled solutions that streamline procurement for food manufacturers. This strategy enables them to dominate high-demand segments, including starches, oils, and protein ingredients, while supporting the development of clean-label and functional products. By 2025, these companies are expected to capture a significant portion of market demand, driven by their ability to meet evolving consumer preferences and industry requirements.

Specialized regional players complement the dominance of multinationals by focusing on niche applications such as enzyme-modified starches, natural colors, and fermentation-based cultures. These players cater to emerging categories like plant-based dairy alternatives and fortified bakery products. For instance, Novonesis provides enzyme solutions that enhance texture and mouthfeel, along with cultures that promote digestive wellness and support clean-label claims. Their agility and in-depth understanding of local market dynamics allow them to quickly adapt to changing regulatory standards and consumer preferences for natural, functional, and minimally processed ingredients.

Commodity traders are increasingly entering value-added segments by partnering with established ingredient suppliers to diversify their offerings. Moving beyond basic starches, oils, and sugars, they are incorporating alternative sweeteners, flavors, and emulsifiers to capture premium pricing opportunities. Companies such as Givaudan and Palsgaard demonstrate how global expertise in natural flavors and specialty emulsifiers can be localized to meet the needs of Brazilian processors seeking functional innovation. The competitive landscape reflects a balance between scale-driven multinationals, agile regional innovators, and commodity players transitioning into value-added solutions, fostering diverse growth across Brazil’s food ingredient market.

Brazil Food Ingredient Industry Leaders

-

Kerry Group

-

Cargill Inc.

-

Tate & Lyle Plc

-

Ingredion Inc.

-

Archer Daniels Midland (ADM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Synergy Flavors Inc., a subsidiary of the Ireland-based Carbery Group, announced the acquisition of Solutaste, a São Paulo-based manufacturer and distributor of flavors and ingredients. This marked Synergy’s second acquisition in Brazil, strengthening its presence in the food and beverage market in South America.

- October 2025: Palsgaard initiated the production of its Emulpals powdered cake emulsifiers in Brazil. Emulpals was a plant-based, clean-label emulsifier range developed for bakery premixes to improve aeration, softness, and production efficiency. These products enabled manufacturers to replace saturated or trans fats with unsaturated liquid oils. Emulpals applied to various cake formulations by adjusting dosage and recipe components. Palsgaard Brazil provided technical support through its application center, assisting manufacturers in creating products with diverse crumb structures, densities, and ingredient profiles.

- April 2024: Prinova, a prominent nutraceutical distribution company, acquired Aplinova as part of its strategy to expand its global presence. This acquisition followed Prinova's earlier purchases of the Brazilian flavor company Flavor Tec and the international distribution organization The Ingredient House. Through this acquisition, Prinova's customers gained access to Aplinova's technical expertise and specialized knowledge in natural flavors and sugar reduction.

Brazil Food Ingredient Market Report Scope

Food ingredients are added to a variety of food products to perform various functions, such as improving the overall safety and effectiveness, maintaining the nutritional value of food products, and improving the taste, texture, and appearance of the final food product.

Brazil's food ingredients market is segmented by type and application. Based on type, the market is segmented into starch and sweetener, flavors and colorants, acidulants and emulsifiers, preservatives, enzymes, edible oil and fats, and other types. Based on application, the market is segmented into bakery products, beverages, meat, poultry, seafood, dairy products, confectionery, and other applications.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Ingredient Type

| Starches and Texturants |

| Alternative Sweeteners |

| Flavors |

| Emulsifiers |

| Colors |

| Enzymes |

| Oils and Fats |

| Other Ingredients (Acidulants, Preservatives, Cultures, Yeast) |

By Application

| Beverages |

| Sauces, Dressings and Condiments |

| Bakery and Confectionery |

| Dairy and Dairy Alternatives |

| Meat and Meat Alternatives |

| Sweet and Savory Snacks |

| Other Applications (Functional and Fortified Food and Ready to Eat) |

| By Ingredient Type | Starches and Texturants |

| Alternative Sweeteners | |

| Flavors | |

| Emulsifiers | |

| Colors | |

| Enzymes | |

| Oils and Fats | |

| Other Ingredients (Acidulants, Preservatives, Cultures, Yeast) | |

| By Application | Beverages |

| Sauces, Dressings and Condiments | |

| Bakery and Confectionery | |

| Dairy and Dairy Alternatives | |

| Meat and Meat Alternatives | |

| Sweet and Savory Snacks | |

| Other Applications (Functional and Fortified Food and Ready to Eat) |

Key Questions Answered in the Report

What is the current value of the Brazil food ingredient market?

It reached USD 6.21 billion in 2026 and is projected to climb to USD 6.46 billion by 2031.

Which ingredient segment is growing the fastest?

Enzymes lead, expanding at 5.43% CAGR during 2026-2031 as processors seek clean-label shelf-life solutions.

What regulatory change most affects formulation strategy?

ANVISA’s front-of-pack warning system under RDC 843/2024 drives reduced sugar, salt, and saturated-fat formulations.

Where are the biggest growth opportunities?

Natural colors, plant-based proteins, and fortified snack applications show the highest forward CAGRs.

Page last updated on: