Polyol Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

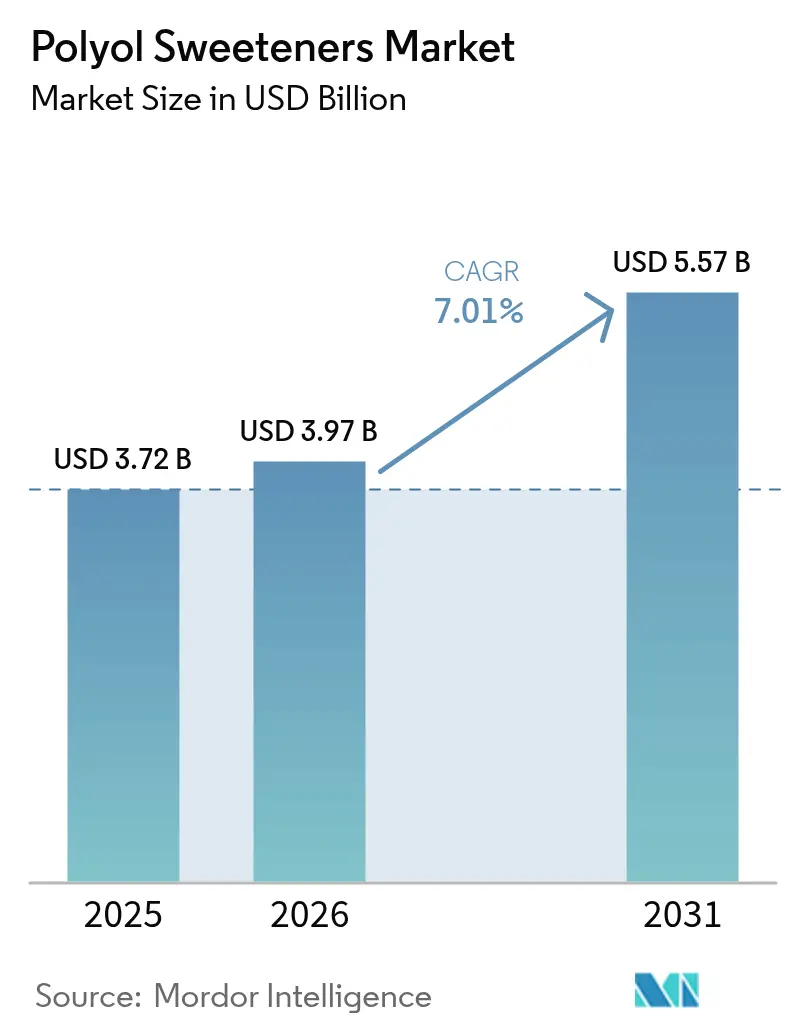

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 5.57 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

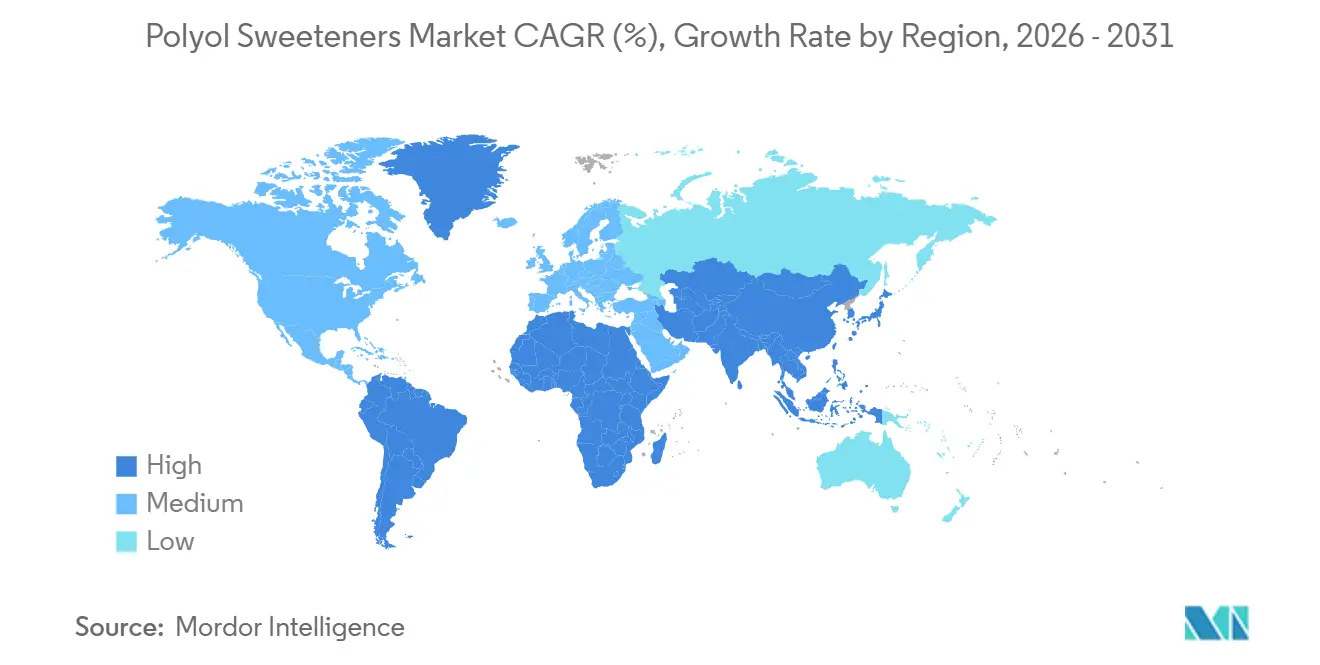

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polyol Sweeteners Market Analysis by Mordor Intelligence

The polyol sweeteners market size is expected to grow from USD 3.72 billion in 2025 and USD 3.97 billion in 2026 to USD 5.57 billion by 2031, with a CAGR of 7.01% during the forecast period of 2026 to 2031. Increased fiscal measures on sugar, such as soda taxes in countries like the United Kingdom and France, are driving product reformulation toward sugar alcohols. Food-grade polyols are witnessing increased demand due to the rising preference for zero-calorie and diabetic-friendly foods, the clean-label trend, and their versatile applications, including pharmaceutical laxatives and pet treats. In December 2023, the European Food Safety Authority (EFSA) re-evaluated erythritol (E 968) and confirmed its safety as a polyol sweetener [1]Source: European Food Safety Authority, "PLS: Re-evaluation of erythritol (E 968) as a food additive," efsa.europa.eu. The assessment highlighted that erythritol is non-genotoxic, helps maintain blood sugar stability, and retains its properties during food processing. These findings reinforce its use in food and beverage manufacturing, particularly for diabetic-friendly and low-calorie products. The Asia-Pacific region dominates production, led by China and India’s strong presence in sorbitol manufacturing, while South America is emerging as the fastest-growing consumption market due to the increasing purchasing power of the middle class. Competitive dynamics and the supply landscape are being influenced by capacity expansions by multinational companies, antidumping investigations in the United States, and advancements in fermentation technology.

Key Report Takeaways

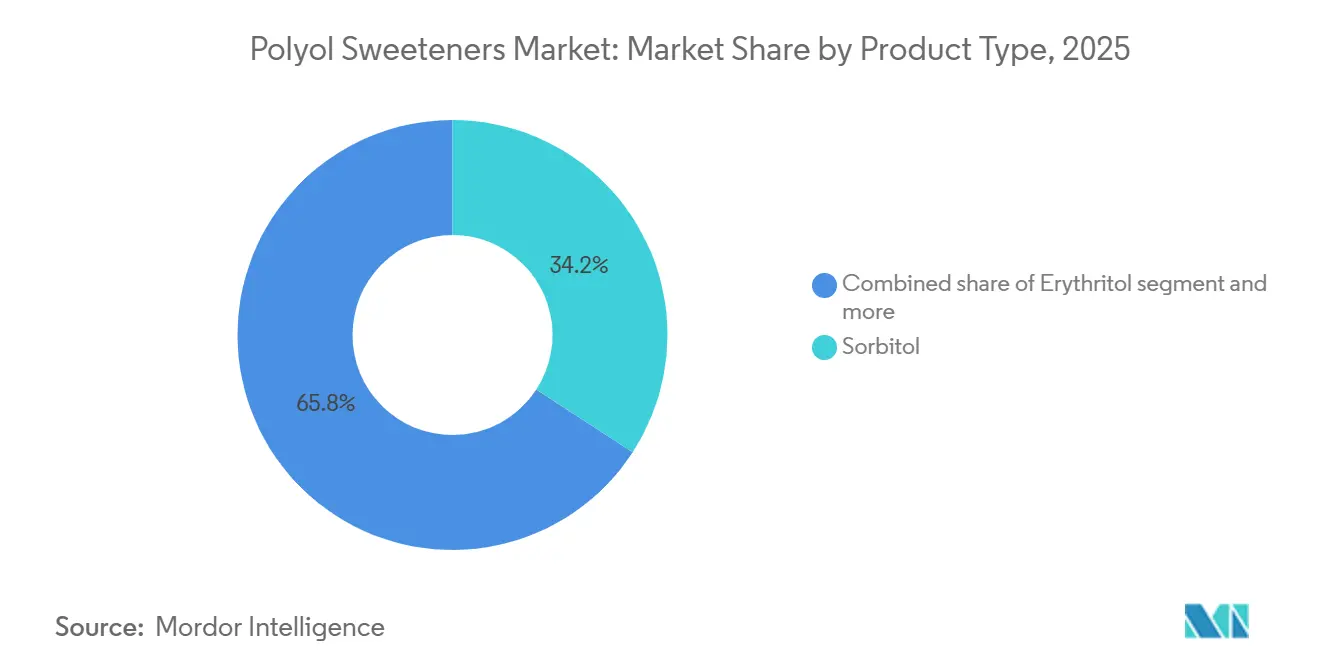

- By product type, sorbitol held 34.17% polyol sweetener market share in 2025; fermentation-derived erythritol is forecast to post the fastest 7.38% CAGR through 2031.

- By form, powder grades commanded 68.09% share of the polyol sweetener market size in 2025, while liquid formats are set to advance at 7.96% CAGR during 2026-2031.

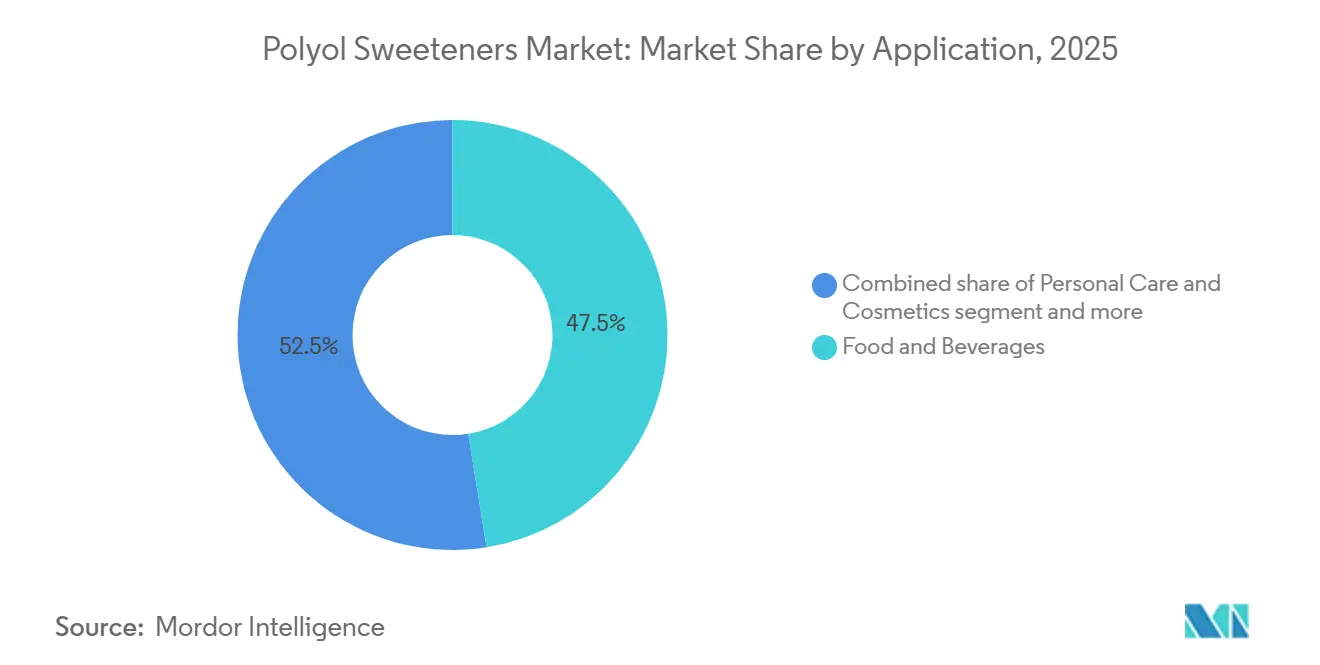

- By application, food and beverages led with 47.47% revenue share in 2025; personal care and cosmetics are projected to grow at 7.58% CAGR to 2031.

- By geography, Asia-Pacific captured 39.18% of 2025 revenue; South America is poised for the highest 7.15% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyol Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift towards sugar-free confectionery boosting polyols usage | +1.2% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Rising demand for low-calorie sweeteners in food industry | +1.0% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Increasing diabetic population accelerating polyol adoption in food | +0.9% | Global, concentrated in Asia-Pacific , North America, Middle East | Long term (≥ 4 years) |

| Surge in clean label trends encouraging use of naturally derived polyols | +0.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Application of sorbitol in pharmaceuticals as laxatives and tablet binders | +0.6% | Global, with regulatory influence from FDA, EMA, USP | Long term (≥ 4 years) |

| Expanding pet food market incorporating safe sweetening agent like sorbitol | +0.4% | North America, Europe, emerging Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer shift towards sugar free confectionery boosting polyols usage

Sugar-free confectionery reformulation has become a key focus for manufacturers as they address consumer demand for indulgent products without adverse metabolic effects. The European Union's Regulation 1333/2008 on food additives sets maximum permissible levels for polyols in confectionery, providing a standardized framework that minimizes reformulation risks and facilitates faster product launches. Ingredients such as maltitol and isomalt are increasingly used in hard candies and chocolates due to their ability to replicate the bulk and mouthfeel of sucrose, allowing manufacturers to achieve "no added sugar" claims while maintaining texture. Erythritol, with its zero-calorie profile, is emerging as a preferred choice in gummy formulations, where it is combined with high-intensity sweeteners to offset bitterness. This trend extends beyond calorie reduction, reflecting a broader shift in positioning confectionery as a functional snack category aligned with wellness trends. Companies that effectively blend polyols can secure price premiums and maintain shelf presence amidst competition from plant-based and protein-enriched alternatives.

Rising demand for low-calorie sweeteners in food industry

Food manufacturers are utilizing polyols to balance taste expectations with the demands of nutritional labeling. The growing integration of polyols into mainstream product lines reflects increasing consumer health awareness, driven by rising obesity rates and concerns about metabolic health. The World Health Organization's (WHO) 2024 recommendations against using non-sugar sweeteners for weight control specifically exclude polyols, acknowledging their unique metabolic properties and functional advantages [2]Source: World Health Organization, “Guideline on the Use of Non-Sugar Sweeteners,” who.int. Beverage applications are particularly notable, as liquid polyol syrups can be incorporated into production lines originally designed for high-fructose corn syrup, reducing the need for significant investment in new dosing equipment. However, managing gastrointestinal tolerance remains a challenge. Excessive polyol consumption can cause laxative effects, leading formulators to combine different sugar alcohols and adjust serving sizes to remain below the 10-gram-per-serving threshold, which typically prevents consumer complaints.

Increasing diabetic population accelerating polyol adoption in food

The growing global diabetic population is influencing ingredient requirements in packaged foods. Polyols, with their low glycemic index, ranging from 0 for erythritol to 9 for maltitol, compared to 65 for sucrose, are becoming integral to diabetic-friendly product formulations. According to the International Diabetes Federation, over 589 million adults worldwide are expected to be affected by diabetes in 2024, driving consistent demand for polyols in such formulations [3]Source: International Diabetes Federation, "Diabetic Population Worldwide" idf.org. Food manufacturers are addressing this demand by introducing diabetes-care product lines that prominently incorporate polyol-based sweeteners, often supported by clinical trials demonstrating their ability to maintain post-prandial glucose stability. The Asia-Pacific region is experiencing particularly strong growth due to the rising prevalence of diabetes in emerging economies and improved access to specialized diabetic products through healthcare system reforms. This demographic trend ensures long-term market stability, as diabetes management necessitates ongoing dietary adjustments, sustaining the demand for polyols.

Surge in clean label trends encouraging use of naturally derived polyols

Clean-label requirements are shaping polyol sourcing strategies, leading to a division in approaches. Erythritol, produced through the fermentation of glucose by Moniliella pollinis or similar yeasts, is classified as "naturally derived," appealing to consumers focused on ingredient origins. The growing demand for recognizable, naturally derived ingredients is driving manufacturers to prioritize plant-based sources and traditional extraction methods. Xylitol, sourced from birch bark, and erythritol, produced via natural fermentation, are priced at a premium as consumers associate natural origins with enhanced safety. The clean-label movement also influences production methods, favoring enzymatic and fermentation processes over chemical hydrogenation for polyol manufacturing. Regulatory agencies are supporting this shift by streamlining approval processes for naturally derived polyols while maintaining strict safety standards that align with consumer preferences. This trend is particularly significant in personal care and cosmetics, where polyols' natural humectant properties complement the clean beauty movement's focus on botanical and naturally derived ingredients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of polyols compared to traditional sugar | -0.7% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Limited consumer awareness in developing economies | -0.5% | Asia-Pacific emerging markets, Middle East and Africa, parts of South America | Medium term (2-4 years) |

| Inconsistent labeling regulation across jurisdictions | -0.3% | Global, fragmentation between European Union (EU), United States, Asia-Pacific standards | Long term (≥ 4 years) |

| Need for technical expertise in polyol formulation for texture optimization | -0.3% | Global, particularly affecting small and mid-sized manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of polyols compared to traditional sugar

Polyol production costs are significantly higher than traditional sugar prices, with erythritol costing 3-4 times more than sucrose. The high costs stem from complex manufacturing processes, such as specialized fermentation and hydrogenation, which require significant investments in equipment, skilled labor, and quality control. Additionally, sugar price volatility exacerbates the cost disparity, as lower sugar prices widen the gap and reduce manufacturers' motivation to adopt polyols. This price sensitivity heavily influences product formulation decisions within the food and beverage industry. Production volumes of specialty polyols, including erythritol and xylitol, remain much lower compared to more established polyols like sorbitol, limiting economies of scale. This constrained production capacity leads to higher unit costs and reduced operational efficiency. The cost disparity is particularly pronounced in developing markets, where consumer price sensitivity hinders the adoption of premium ingredients, thereby restricting market growth in regions with significant demographic potential. Furthermore, the limited availability of raw materials and processing facilities in these regions intensifies the production cost challenges.

Limited consumer awareness in developing economies

Consumer education gaps in the Asia-Pacific, Middle East, and Latin American markets hinder the adoption of polyols, despite their favorable health profiles. Many consumers are unfamiliar with terms such as "sorbitol" or "erythritol," often perceiving them as synthetic additives rather than naturally derived sweeteners. This misconception is further aggravated by limited space for on-pack communication and low health literacy rates, which make it challenging to effectively convey benefits such as a low glycemic index or dental health advantages. Multinational brands have attempted to address these issues through mass-media campaigns promoting the role of sugar alcohols in diabetes management. However, these initiatives require long-term investments and face significant challenges, including competition from sugar-industry lobbying. The regulatory environment provides some support; mandatory front-of-pack nutrition labeling in countries like Chile, Mexico, and Peru highlights high sugar content, indirectly increasing the appeal of polyols. Nevertheless, these measures fall short of actively endorsing sugar alcohols as preferred alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fermentation-Derived Erythritol Outpaces Hydrogenated Polyols

Sorbitol is projected to maintain the largest market share at 34.17% in 2025, supported by decades of infrastructure investment and well-established supplier relationships across food, pharmaceutical, and industrial applications. This growth is driven by its zero-calorie positioning and biotechnological production methods, which avoid the "chemical processing" perception associated with hydrogenated polyols. Maltitol occupies a middle ground, being preferred in sugar-free chocolate due to its sucrose-like sweetness profile. However, its adoption is limited by higher costs and minimal differentiation compared to blended polyol systems. Isomalt caters to niche applications such as hard candies and cough drops, where its resistance to crystallization and moisture absorption supports its premium pricing.

Erythritol is experiencing the strongest market expansion, with a CAGR of 7.38% through 2031. This growth is attributed to its zero-calorie properties and sucrose-like taste profile, aligning with increasing consumer demand for natural, low-calorie sweeteners. Its applications are expanding in beverages, baked goods, and dairy products. Additionally, erythritol's excellent digestive tolerance and tooth-friendly characteristics enhance its market appeal. Maltitol continues to hold a significant position in sugar-free confectionery production, valued for its browning properties and ability to replicate sugar's functionality in chocolate and baked goods.

By Form: Liquid Polyols Gain Ground in Ready-to-Use Beverage Applications

Powder polyols accounted for 68.09% of the market share in 2025, underscoring their dominance in applications such as confectionery, baking, and pharmaceutical tableting, where crystalline structure and flowability are essential. Liquid polyols, on the other hand, are projected to grow at a compound annual growth rate (CAGR) of 7.96% from 2026 to 2031. This growth is driven by beverage manufacturers' preference for ready-to-use syrups, which eliminate the dissolution step and reduce production cycle times. The choice of form also impacts logistics costs; liquid polyols transported in isotanks or flexitanks achieve lower per-kilogram freight costs on long-haul routes compared to bagged powder. However, they incur higher storage costs due to their larger volumetric requirements.

Powder erythritol offers non-hygroscopic properties, maintaining its free-flowing characteristics even in humid climates, which simplifies warehousing in tropical markets. Manufacturers targeting the tabletop sweetener segment favor the powder form, as it enables portion-controlled sachets and shaker dispensers that replicate the user experience of sugar. Additionally, hybrid solutions are gaining traction, with suppliers introducing agglomerated powders that dissolve quickly in cold liquids, bridging the convenience gap between traditional powder and liquid forms.

By Application: Personal Care Formulations Leverage Polyols' Humectant Properties

The food and beverages segment accounted for 47.47% of application revenue in 2025. However, the personal care and cosmetics segment is projected to grow at a compound annual growth rate (CAGR) of 7.58% from 2026 to 2031, driven by formulators' recognition of polyols' multifunctional benefits beyond sweetening. Sorbitol's hygroscopic properties make it an effective humectant in skincare formulations, helping to retain skin hydration by drawing moisture from the environment. Additionally, xylitol's antimicrobial properties help reduce the need for preservatives in oral care products. Pharmaceutical applications are experiencing steady growth, supported by sorbitol's dual functionality as a laxative and excipient. Compliance with United States Pharmacopeia standards ensures the batch-to-batch consistency required by drug manufacturers.

Industrial applications, including polyurethane foam production and alkyd resin synthesis, represent a smaller yet stable revenue stream. These applications are less influenced by consumer trends due to long-term supply contracts and technical specifications that favor established polyol grades. The pet food segment, while limited in overall volume, commands premium pricing due to stringent safety standards and the requirement for pharmaceutical-grade purity in veterinary therapeutics.

Geography Analysis

Asia-Pacific is projected to hold a 39.18% market share in 2025, establishing itself as a key producer and consumer of polyols. China's manufacturing capacity plays a significant role in shaping global supply chains. The region's growth is driven by the expanding pharmaceutical sectors in India and Southeast Asia, where polyols are utilized as excipients in generic drug production. Additionally, increased health awareness in urban areas has boosted the consumption of sugar-free products. Advances in biotechnology-based polyol production, particularly through fermentation processes, position the region as a global hub for polyol technology development.

South America is expected to exhibit the highest growth rate, with a CAGR of 7.15% through 2031. This growth is supported by the expansion of food processing industries and favorable economic conditions that encourage the adoption of premium ingredients. Government healthcare programs further drive the pharmaceutical sector, increasing the demand for polyol excipients in generic drug production. The Middle East and Africa present significant growth potential, particularly in the pharmaceutical sector, where improved healthcare infrastructure is driving demand for polyol-based drug delivery systems. Economic diversification into food processing and pharmaceutical manufacturing creates opportunities for polyol suppliers, especially those focusing on regulatory compliance and establishing local partnerships.

North America and Europe maintain strong market positions due to high-value applications and stringent regulatory standards that foster innovation in polyol formulations. Regulatory bodies such as the FDA and EFSA provide safety assessments and support for polyols, creating a stable environment that encourages investment in new applications and production methods. These regions are at the forefront of clean label trends and the use of natural polyols, with consumers willing to pay premium prices for sustainably sourced and environmentally friendly products. In Europe, regulations promoting sugar reduction in processed foods sustain polyol demand, while in North America, diabetes management protocols incorporate polyol-containing products as part of treatment plans.

Regulatory Landscape

Polyol sweeteners are regulated primarily as food additives, with usage conditions and labeling requirements that vary by jurisdiction. In the European Union, polyols such as sorbitol, xylitol, mannitol, maltitol, isomalt, lactitol, and erythritol fall under Regulation (EC) No 1333/2008, supported by specifications in Regulation (EU) No 231/2012, including the mandatory consumer warning that excessive consumption may induce laxative effects on relevant products. EFSA continues its systematic re-evaluation program for food additives authorized before 20 January 2009, and its December 2023 re-evaluation of erythritol (E 968) reaffirmed the additive's safety for authorized uses, reinforcing regulatory continuity for key low-calorie reformulation pathways.

A notable compliance update impacting specialty nutrition is the European Commission's Regulations (EU) 2026/189 and 2026/196, effective 18 February 2026, which introduced tighter purity specifications, including heavy metal limits and microbiological criteria, for additives used in foods intended for vulnerable populations (including infants/young children and foods for special medical purposes). Globally, international risk assessment work continues through FAO/WHO's Joint Expert Committee on Food Additives (JECFA), while in the United States many common polyols maintain a pathway to market through FDA frameworks, including GRAS use for several established sugar alcohols. This supports multi-region suppliers managing parallel compliance dossiers and label strategies across major end markets.

Value Chain Analysis

The polyol sweeteners value chain begins with upstream agricultural and carbohydrate inputs, primarily starch and glucose streams sourced from corn, wheat, cassava, and other plant feedstocks. These inputs move into conversion and purification stages, where producers manufacture hydrogenated polyols (for example, sorbitol and maltitol) and fermentation-derived polyols (notably erythritol) using specialized processing equipment and quality systems aligned to food and, where relevant, pharmacopeial requirements. Producers with integrated grain processing footprints can reduce exposure to feedstock volatility and logistics constraints, while manufacturers serving pharmaceutical and specialty food customers invest more heavily in analytical controls and documentation.

Midstream participants include ingredient manufacturers and solution providers that supply standardized grades (powder and liquid) and increasingly offer application support for texture, bulking, humectancy, and stability. Companies such as Ingredion position polyols within broader formulation systems alongside texturants, while regional specialists such as Gulshan Polyols Ltd combine starch derivatives with polyol production to support cost and supply continuity. Downstream, distribution runs through ingredient distributors and direct supply to confectionery, bakery, beverage, dairy, pharma, and personal care manufacturers. Logistics choices differ by form, with liquids commonly shipped in bulk (for example, isotanks/flexitanks) and powders in bags, creating different cost and handling trade-offs for global brands and contract manufacturers.

Competitive Landscape

The polyols market demonstrates moderate consolidation, with global companies such as Cargill, Roquette, and Archer Daniels Midland holding significant production capacity and established customer relationships. However, regional specialists maintain a notable market share through cost leadership and localized services. Opportunities exist in fermentation-based production of novel polyols and in developing applications for industrial segments like bio-based polyurethane precursors, where sustainability requirements are driving the replacement of petroleum-derived polyols.

Smaller players, such as Gulshan Polyols in India and Beijing Stevia in China, are leveraging lower labor costs and government subsidies to offer competitive pricing, particularly in sorbitol and maltitol, where product differentiation is minimal. Major players are pursuing vertical integration strategies, controlling agricultural feedstock sourcing while expanding into food, pharmaceutical, and industrial applications. Companies are also adopting biotechnology-based production methods, including advanced fermentation processes, to gain cost advantages in competitive polyol segments.

Technology adoption is emerging as a key competitive factor. Producers investing in continuous fermentation and membrane-based purification are achieving 15% to 20% yield improvements compared to batch processes. These advancements translate into margin expansion, enabling further capacity additions and customer acquisition. This focus on technological innovation is positioning companies to strengthen their market presence and meet evolving industry demands.

Polyol Sweeteners Industry Leaders

-

Archer Daniels Midland Company

-

Cargill, Inc

-

Ingredion Incorporated

-

Roquette Frères

-

International Flavors & Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are expanding where manufacturers need both sweetness reduction and functional replacement for sugar's bulk, particularly in confectionery, bakery, and beverage systems that require texture and stability. Suppliers are responding with integrated reformulation toolkits that combine polyols with other structural ingredients (such as starches and texturizers) and high-intensity sweeteners, reflecting the report's emphasis that polyols are used for more than sweetness, including mouthfeel, humectancy, and processing performance. The World Health Organization's 2024 guideline on non-sugar sweeteners excluded polyols from its recommendation against use for weight control, supporting continued development focus on sugar alcohols versus some alternative sweetener classes.

On the supply side, investment-led regionalization creates whitespace for local and near-market sourcing, especially for high-volume liquid polyols and fast-growing fermentation-derived grades. In May 2024, MOL Group inaugurated a 200,000 tons/year polyol production complex in Tiszaújváros, Hungary, and in December 2024 Baolingbao Biology announced up to USD 85 million to build a 30,000 tons/year sugar substitute facility in the United States, signaling efforts to diversify production footprints closer to demand centers. In Europe, the January 2026 publication of Regulations (EU) 2026/189 and 2026/196, tightening purity and microbiological requirements for additives in foods for vulnerable populations, increases demand for higher-specification polyol grades and favors suppliers that can document compliance and provide consistent, low-contaminant materials for infant and FSMP formulations.

Recent Industry Developments

- June 2026: Roquette launched NEOSORB AG, a plant-based multifunctional polyol range for agriscience applications, including liquid solutions such as NEOSORB AG S50 and NEOSORB AG L20. The move broadens polyols positioning beyond traditional food and pharma uses into crop and agricultural input applications. It also strengthens Roquette's differentiation around functionality, not only sweetening, which supports premiumization in selected end uses.

- January 2025: TEHRAN established the first sorbitol production facility in Iran and West Asia with an annual capacity of 7,500 tons of 70% liquid sorbitol. The facility increases regional availability of liquid sorbitol for pharmaceutical and food uses and can reduce dependence on imported bulk polyols. It also reflects continued investment in localized production where logistics and supply assurance influence buyer decisions.

- July 2024: Covestro (India) inaugurated a new Polyol Tank Farm in Kandla, Gujarat (Kutch district) to improve storage and supply chain efficiency for polyols used in its Performance Materials business. Expanded storage infrastructure supports more stable, responsive deliveries to customers and helps manage variability in inbound and outbound logistics. The project highlights how downstream handling and distribution assets can become a competitive lever alongside production capacity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers polyol sweeteners (sugar alcohols) sold as ingredients and used mainly for sweetening, bulking, and moisture control in food and beverages, pharmaceuticals, and personal care. Values are measured at the ingredient sales level across regions.

Scope exclusions: The sizing does not include polyurethane-grade polyols, finished consumer goods that contain polyols, or calorie sweeteners like sucrose and HFCS.

Segmentation Overview

-

By Product Type

- Erythritol

- Sorbitol

- Maltitol

- Isomalt

- Others

-

By Form

- Powder

- Liquid

-

By Application

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Industrial

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and to build a clean set of demand signals before any modeling started. We referenced public sources such as USDA food supply tables and ingredient context notes, FAO food balance style statistics, UN Comtrade trade flows mapped to sugar alcohol HS-linked categories, the US FDA database for ingredient and labeling context, and EFSA opinions where ingredient safety and use guidance affects adoption.

To make the dataset usable, we also reviewed annual reports, investor presentations, and credible press coverage to understand capacity additions, expansion timelines, and end-use pull in reduced-sugar formulations. A patent database and an import export shipment-level database were used selectively to sanity check where product innovation and cross-border movements were picking up. The desk sources listed here are illustrative only, and additional public references were checked to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work was used to stress-test the desk assumptions and fill gaps that do not show up in public statistics, especially around food reformulation rates and pricing behavior for key polyols. We spoke with participants across ingredient manufacturing, distribution, and large end users, and we balanced coverage across APAC, EMEA, and the Americas so regional adoption patterns were not averaged out too early.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 49% |

| Mid tier: 48% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 15% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where consumption is reconstructed from a demand pool tied to reduced-sugar product activity, ingredient use rates, and observable trade and production signals for sugar alcohol categories. Once the total is formed, it is checked using selective bottom-up approximations, such as sampled supplier revenue splits, distributor channel checks, and a price times volume view for the most traded polyols, and then adjusted when gaps show up.

Inputs used in the model include polyol inclusion rates by application (such as confectionery, bakery, beverages, and pharma excipients), regional pricing bands and expected price progression, import dependence versus local production, the pace of new product launches carrying sugar reduction claims, and regulatory or labeling signals that shift formulation choices. Forecasts are run with multivariate regression, where the drivers above are projected using consensus ranges from interviews, and scenario analysis is applied when price swings or policy changes create visible upside or downside risk. When bottom-up evidence is incomplete in smaller regions, we use conservative penetration assumptions and then re-check totals against trade direction and application demand logic.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final number aligns with real-world signals, not just one dataset. We compare regional totals against independent indicators like trade trends, capacity announcements, and price movement patterns, and then investigate variances that look too sharp to be explained by demand alone.

Before sign-off, the model and assumptions go through stepwise analyst review, and interview follow-ups are triggered when a key variable shifts or a region shows an unusual jump. The report is refreshed annually, and interim updates are made when material events occur, such as a major capacity start-up or a policy change that impacts sugar reduction. Right before delivery, we do a final pass to ensure the latest public data and event impacts are reflected.

Mordor Intelligence's Polyols Market Estimate Compared With Other Published Estimates

Published market sizes for polyols often look far apart because the term polyols can cover different products across industries, and because pricing and volume assumptions are updated on different timelines. The table below shows how much of the spread comes from scope alignment first, and then from forecasting choices.

The table points to a large gap that mostly comes from product definition, where Mordor Intelligence's model counts only food, pharma, and personal care grade polyol sweeteners, while some other estimates include industrial polyurethane polyols and related foam uses, which lifts the total. Differences also arise when pricing is projected as a straight CAGR instead of being tied to feedstock moves, and when currency conversion timing is not aligned to the same base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.97 B (2026) | |

| Global Consultancy A | USD 45.14 B (2025) | This figure aligns to polyurethane-grade polyols used in foams and coatings, so the scope is much broader than sugar alcohol ingredients and captures polymer demand cycles. |

| Industry Publisher B | USD 29.70 B (2025) | The estimate appears to include natural, polyester, and polyether polyols for polyurethane production, and it likely applies a different price and currency timing, which changes the base-year value. |

Reading the three values together, the main takeaway is that picking the right product boundary and then applying repeatable demand and pricing checks keeps the market size interpretable. Our approach stays traceable to ingredient use drivers and realistic price bands, which supports year-over-year comparisons for planning and budgeting.

Key Questions Answered in the Report

How big is the Polyols market in 2026?

The Polyols market size stands at USD 3.97 billion in 2026, on track for a 7.01% CAGR through 2031.

Which product type is growing fastest?

Fermentation-derived erythritol is forecast to expand at 7.38% CAGR between 2026-2031 due to zero-calorie positioning and clean-label appeal.

Why is South America the quickest-growing region?

Sugar-tax policies, middle-class dietary shifts, and new local fermentation capacity are propelling South America at a 7.15% CAGR.

What restrains wider polyol adoption?

High production costs that price polyols at 2-4 times sugar and fragmented labeling rules slow penetration, especially in emerging economies.

Page last updated on: