Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

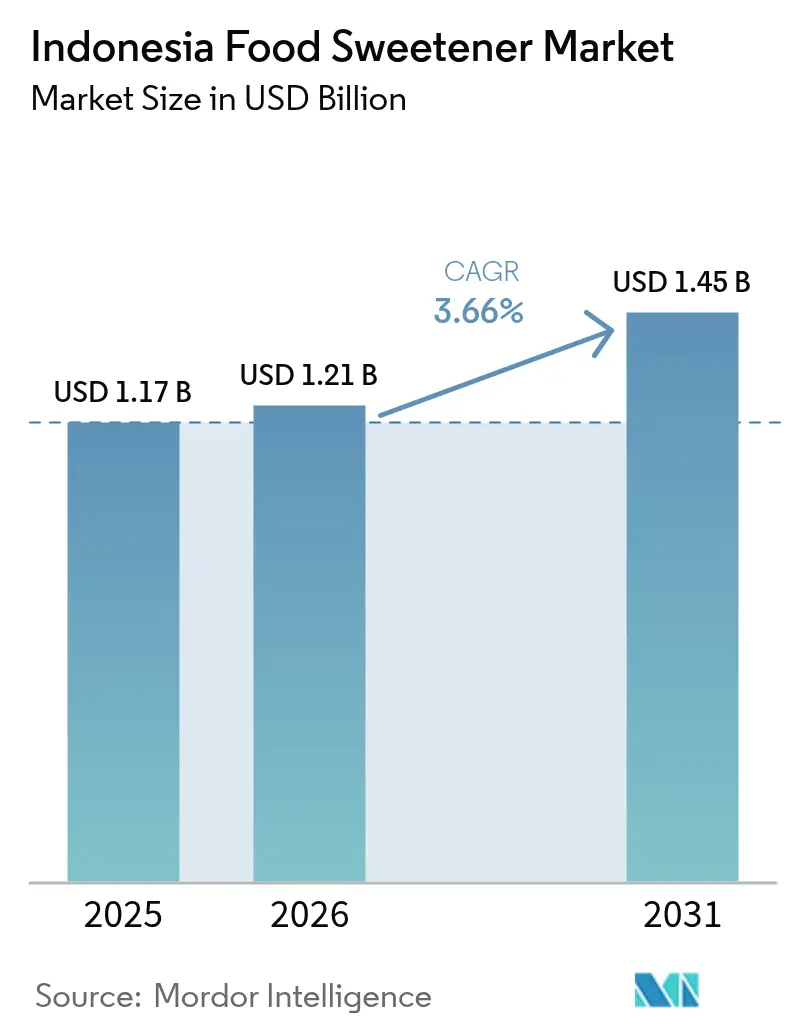

| Base Year Market Size (2025) | USD 1.17 Billion |

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Food Sweetener Market Analysis by Mordor Intelligence

Indonesia food sweetener market size in 2026 is estimated at USD 1.21 billion, growing from 2025 value of USD 1.17 billion with 2031 projections showing USD 1.45 billion, growing at 3.66% CAGR over 2026-2031. This moderate expansion signals a sector in transition as health-conscious shoppers, fiscal measures on sugar, and mandatory halal labeling reshape purchase choices. A prolonged dependency on imported raw sugar continues to expose local supply to global price swings, yet broadening domestic cultivation of stevia, palm sugar, and coconut sugar offers a partial hedge against that exposure. Large beverage fillers have started to reformulate flagship products to cut taxable free-sugar content, while bakery producers are experimenting with sweetener blends that preserve texture at lower caloric loads. The gradual rise of middle-class households with higher discretionary income sustains overall demand for indulgent items, but spending is shifting toward “better-for-you” SKUs that rely on high-intensity or natural alternatives rather than bulk sucrose.

Key Report Takeaways

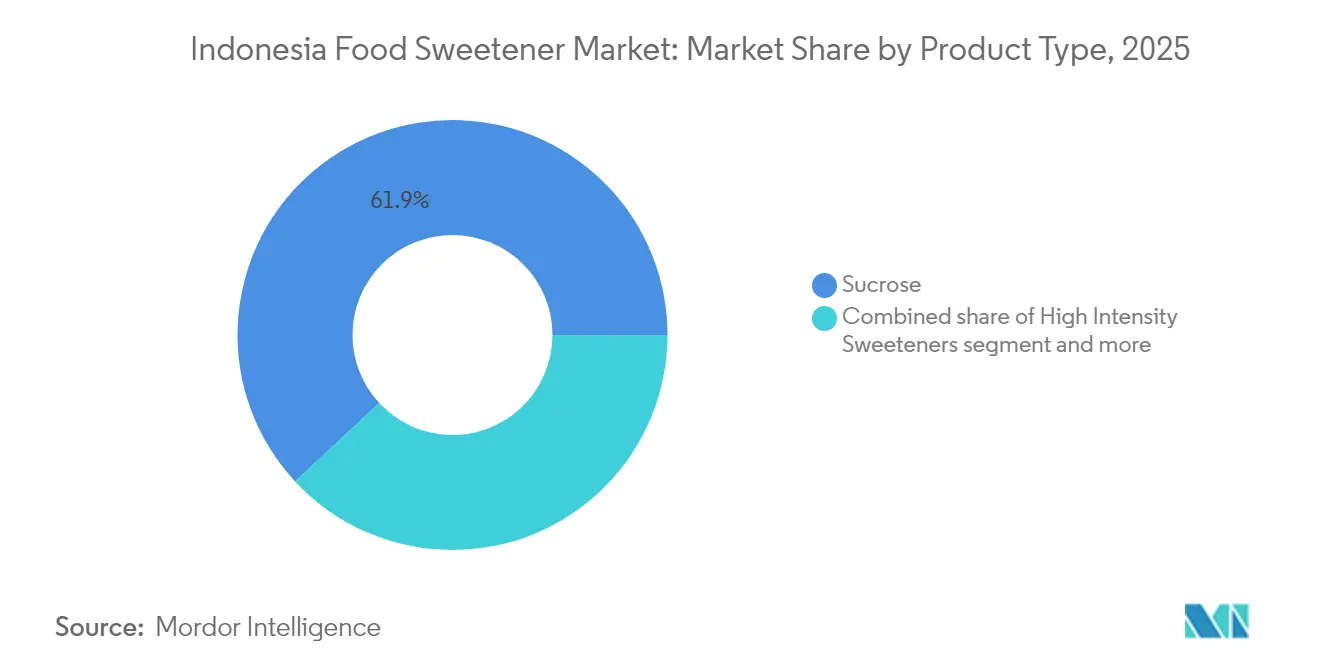

- By type, sucrose led with 61.92% of Indonesia's food sweetener market share in 2025, and high-intensity sweeteners are forecast to expand at a 4.57% CAGR through 2031.

- By form, powder commanded 71.88% share of the Indonesian food sweetener market size in 2025, while liquid formats are projected to grow at a 4.43% CAGR through 2031.

- By source, synthetic variants represented 68.05% revenue share in 2025; natural sources are set to register the fastest growth at 4.46% CAGR to 2031.

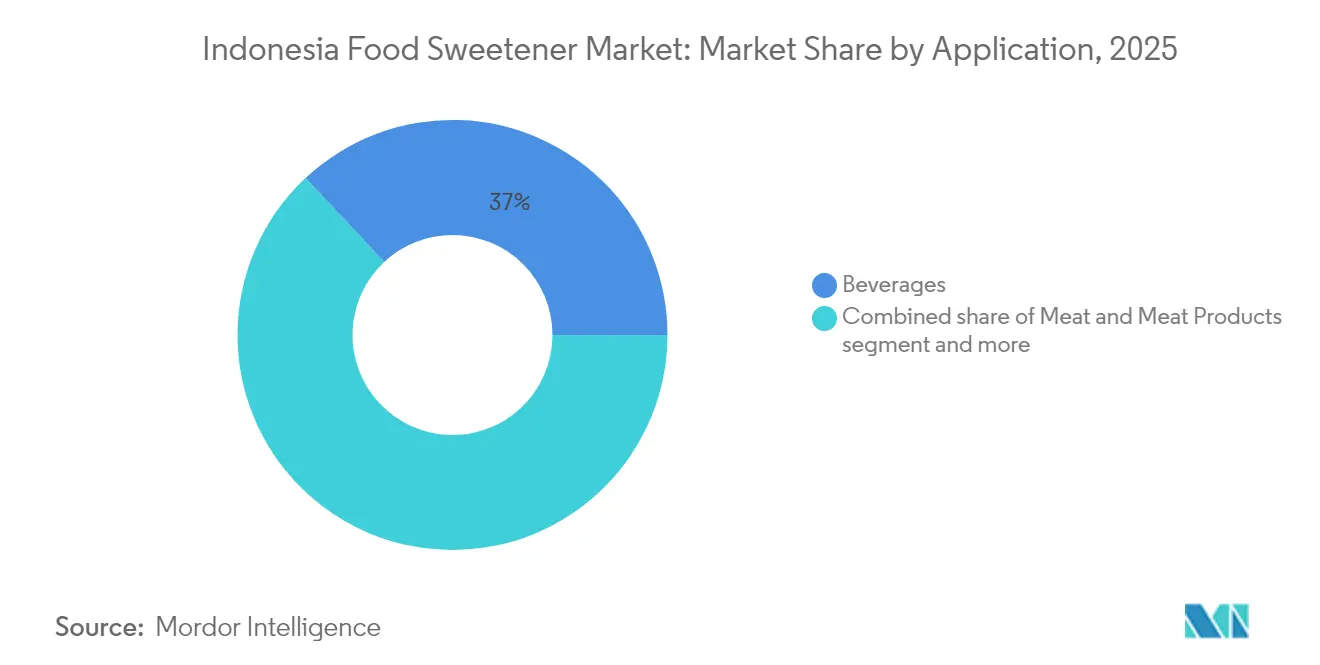

- By application, beverages held 36.98% of the Indonesian food sweetener market in 2025; bakery and confectionery are advancing at a 4.78% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Food Sweetener Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed-food boom elevating bulk sucrose demand | +1.2% | National, concentrated in Java and urban centers | Medium term (2-4 years) |

| Booming demand for low-calorie beverage in urban regions | +0.8% | Urban Indonesia, particularly Jakarta, Surabaya, Bandung | Short term (≤ 2 years) |

| Increasing prevalence of diabetes and obesity | +0.7% | National, with higher impact in urban areas | Long term (≥ 4 years) |

| Shift toward food personalization and controlled nutrition | +0.5% | Urban middle-class demographics | Medium term (2-4 years) |

| Strong demand for flavored dairy products reduces sugar | +0.4% | National, driven by government nutrition programs | Medium term (2-4 years) |

| Consumer behaviour toward clean label products | +0.6% | Urban and semi-urban regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Processed-food boom elevating bulk sucrose demand

The growing processed food industry in Indonesia is significantly driving the demand for bulk sucrose. According to data from the Indonesian Ministry of Industry, the processed food sector has been expanding at a robust pace, contributing substantially to the country's GDP. World Bank data reveals that in 2023, urban areas in Indonesia housed approximately 59% of the nation's total population [1]Source: World Bank, "Urban population (% of total population) - Indonesia", www.data.worldbank.org. As processed foods often require sucrose as a key ingredient for flavor enhancement, preservation, and texture improvement, the demand for bulk sucrose is witnessing a notable rise. Furthermore, government initiatives aimed at boosting the food and beverage industry, such as tax incentives and infrastructure development, are expected to further support the growth of the processed food sector. This, in turn, is likely to sustain the upward trajectory of bulk sucrose demand in the forecast period.

Booming demand for low-calorie beverage in urban regions

The increasing demand for low-calorie beverages in urban regions is a significant driver of the Indonesia Food Sweetener Market. This trend is fueled by growing health consciousness among urban consumers, who are actively seeking healthier alternatives to traditional sugary drinks. In 2024, the International Diabetes Federation reported a diabetes prevalence rate of 11.3% in the country [2]Source: International Diabetes Federation, "Diabetes in Indonesia (2024)", www.idf.org. In response, the government has launched initiatives to encourage healthier eating habits, emphasizing the adoption of low-calorie products.The government has also introduced public awareness campaigns, such as the "Isi Piringku" program, which emphasizes balanced nutrition and reduced sugar intake. Additionally, the Indonesian Food and Beverage Association (GAPMMI) has reported a steady rise in the production and consumption of low-calorie beverages, reflecting a shift in consumer preferences. GAPMMI further highlights that urbanization and rising disposable incomes have contributed to the growing demand for premium and health-focused products, including beverages sweetened with innovative alternatives like stevia, sucralose, and erythritol.

Increasing prevalence of diabetes and obesity

The increasing prevalence of diabetes and obesity is fueling the market growth. According to data from the Indonesian Ministry of Health, the prevalence of diabetes in the country has been steadily rising, and obesity rates have also surged. These health concerns have led to a growing demand for low-calorie and sugar-free sweeteners as consumers seek healthier alternatives to traditional sugar. Indonesia's Ministry of Health is intensifying its battle against obesity, aiming to keep the nation's obesity rate steady at 21.8% through the end of 2024 [3]Source: Ministry of Health, "Ministry to maintain obesity prevalence at 21.8 percent until 2024", www.en.antaranews.com. The ministry's strategy, as highlighted by the Director of Non-Communicable Diseases Prevention and Control, zeroes in on addressing conditioned risk factors and social determinants, targeting the journey from being merely overweight to becoming obese. Furthermore, associations such as the Indonesian Diabetes Association have been actively promoting awareness about the risks of excessive sugar consumption, further driving the adoption of alternative sweeteners in the market. This trend is expected to continue during the forecast period, supported by government initiatives aimed at reducing sugar intake and promoting healthier lifestyles.

Shift toward food personalization and controlled nutrition

The shift toward food personalization and controlled nutrition is emerging as a significant driver in the Indonesia food sweetener market. Consumers are increasingly seeking customized food products that cater to their specific dietary needs, preferences, and health goals. This trend is fueled by growing health awareness, advancements in nutritional science, and the availability of innovative sweetener solutions. The rising prevalence of lifestyle-related diseases, such as diabetes and obesity, has further accelerated the demand for controlled nutrition, prompting consumers to opt for sweeteners that support healthier lifestyles. Additionally, the increasing penetration of digital health tools and mobile applications has enabled consumers to monitor their nutritional intake more effectively, driving the adoption of personalized food products. Manufacturers are responding by developing tailored sweetener products that align with individual requirements, such as low-calorie, natural, or functional sweeteners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny and labeling requirements | -0.9% | National, with higher compliance costs for smaller manufacturers | Short term (≤ 2 years) |

| Rising demand for clean label and natural food products | -0.6% | Urban and semi-urban markets | Medium term (2-4 years) |

| Health concerns over artificial sweeteners' carcinogenic properties | -0.4% | National, particularly educated urban demographics | Long term (≥ 4 years) |

| Growing consumer preference for natural plant-based sweeteners | -0.5% | Urban middle-class and health-conscious segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory scrutiny and labeling requirements

The Indonesia Food Sweetener Market faces significant restraint due to stringent regulatory scrutiny and labeling requirements. The government of Indonesia, through agencies such as the National Agency of Drug and Food Control (BPOM), enforces strict regulations to ensure food safety and consumer protection. These regulations mandate comprehensive labeling of food products, including detailed information on sweetener content, usage limits, and potential health impacts. Additionally, compliance with international standards, such as those set by the Codex Alimentarius Commission, further adds to the regulatory burden for manufacturers. Industry associations, including the Indonesian Food and Beverage Association (GAPMMI), have highlighted the challenges faced by producers in adhering to these evolving regulations. Such stringent requirements increase operational costs and can delay product launches, thereby restraining market growth during the forecast period.

Health concerns over artificial sweeteners' carcinogenic properties

Consumers are becoming increasingly aware of potential health risks associated with artificial sweeteners, particularly synthetic ones like aspartame and saccharin, which is constraining market growth. In Indonesia, health authorities and consumer advocacy groups are raising alarms about the potential carcinogenic properties of certain artificial sweeteners, a stance bolstered by international research and regulatory debates. While the government pushes to curb non-communicable diseases like diabetes and obesity, it finds itself in a paradox: promoting artificial sweeteners as healthier sugar substitutes while also questioning their long-term health implications. Community programs educating the public on stevia's safety, in contrast to its artificial counterparts, signal a notable shift towards natural options. Furthermore, heightened media attention on global studies casting doubt on the safety of artificial sweeteners has led to a palpable hesitance among consumers, especially those in urban areas who prioritize health and diligently scrutinize product ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sucrose dominance faces high-intensity challenge

Sucrose accounted for 61.92% of Indonesia's food sweetener market. Its widespread use is attributed to its multi-functional properties, including its ability to act as a bulking agent, aid in crystallization, and enhance flavor. These characteristics make sucrose a preferred choice across various food and beverage applications in the country. Additionally, its cost-effectiveness and ease of availability further strengthen its position as a dominant sweetener in the market.

High-intensity sweeteners, including stevia, sucralose, neotame, and monk-fruit extracts, are gaining traction in the Indonesian market. These sweeteners are increasingly favored due to their low-calorie content and significantly higher sweetness levels compared to sucrose, which allows for smaller quantities to achieve the desired sweetness. The segment is growing at a CAGR of 4.57%, driven by rising consumer demand for healthier and low-calorie alternatives in food and beverage products. Furthermore, the growing awareness of health issues, such as obesity and diabetes, is encouraging manufacturers to incorporate these sweeteners into their product formulations.

By Form: Powder efficiency meets liquid convenience

In 2025, powdered variants dominated Indonesia's food sweetener market, capturing 71.88% of the market share. Their dominance can be attributed to several factors. Powdered sweeteners offer an extended shelf life, which is particularly advantageous in Indonesia's tropical climate with high humidity levels. This characteristic ensures that the product remains stable and usable over a longer period. Additionally, powdered formats are easier to package and transport, making them highly suitable for inter-island shipping, which is a critical logistical requirement in Indonesia's archipelagic geography. Furthermore, powdered sweeteners are widely used in various applications, including dry-mix sauces and instant noodles, due to their compatibility with these products.

Meanwhile, liquid formats are experiencing notable growth, advancing at a 4.43% CAGR. This growth is primarily driven by technological advancements and evolving consumer demands. Beverage companies in Indonesia are increasingly upgrading their production lines with aseptic PET technology, which enhances the safety and shelf life of liquid sweeteners. This technological shift has made liquid formats more appealing for use in beverages and other liquid-based applications. Additionally, liquid sweeteners are gaining traction due to their ability to provide precise metering during continuous syrup preparation, which is essential for maintaining consistency and quality in production processes.

By Source: Synthetic leadership challenged by natural momentum

Synthetic solutions held a dominant 68.05% market share in 2025. This significant share can be attributed to their cost advantages, which make them a preferred choice for manufacturers aiming to optimize production costs. Additionally, robust global supply contracts have ensured a steady and reliable availability of synthetic sweeteners, further solidifying their position in the market. These factors collectively contribute to the widespread adoption of synthetic solutions across various industries in Indonesia.

On the other hand, natural solutions are gaining traction in the Indonesia sweetener market, growing at a CAGR of 4.46%. This growth is primarily driven by increasing consumer demand for halal-compliant products, which align with the dietary preferences of the predominantly Muslim population in the country. Furthermore, the clean-label positioning of natural sweeteners appeals to health-conscious consumers seeking minimally processed and transparent ingredient options. Domestic cultivation initiatives have also played a crucial role in supporting the growth of natural sweeteners, as they promote local production and reduce dependency on imports.

By Application: Beverage leadership yields to bakery innovation

In 2025, beverages accounted for a significant 36.98% share of Indonesia's food sweetener market, amounting to USD 433 million. This dominance highlights the entrenched consumer preference for sweetened beverages, including tea, carbonated drinks, and dairy-based beverages. The popularity of sweetened tea remains a cultural staple, while carbonated drinks continue to attract a broad consumer base due to their refreshing appeal. Additionally, the growing demand for flavored and sweetened dairy drinks, such as milk-based beverages and yogurt drinks, further drives the segment's growth. The beverage sector's reliance on sweeteners is expected to remain robust, supported by evolving consumer tastes and the introduction of innovative product offerings by manufacturers.

The bakery and confectionery segment is experiencing notable growth, with a compound annual growth rate (CAGR) of 4.78%. This expansion is fueled by the rising café culture and the proliferation of premium croissant chains in Indonesia's metropolitan areas. Urban consumers, particularly millennials and young professionals, are increasingly drawn to artisanal bakery products and high-quality confectionery items. The growing presence of international bakery chains and local premium brands has further enhanced the availability of diverse offerings, catering to evolving consumer preferences. Sweeteners play a crucial role in this segment, as they are integral to the production of cakes, pastries, chocolates, and other confectionery products. The segment's growth trajectory is expected to continue, driven by urbanization, increasing disposable incomes, and the rising demand for indulgent and premium bakery products.

Geography Analysis

Indonesia, the world's largest archipelagic nation, presents a distinctive geographical landscape that significantly influences its sweetener market. With over 17,000 islands, the country faces logistical complexities that shape distribution networks. These challenges have led to a preference for shelf-stable powder sweeteners, which are easier to transport and store compared to liquid alternatives. The fragmented geography necessitates efficient supply chain strategies to ensure product availability across diverse regions, making distribution a critical factor in market development.

Java, Indonesia's most economically significant island, plays a pivotal role in the sweetener market. As the center of economic activity, Java hosts key urban hubs such as Jakarta, Surabaya, and Bandung, which drive both manufacturing and consumption. These cities serve as focal points for market growth, with their dense populations and higher purchasing power fostering demand for a wide range of sweetener products. The concentration of industrial and commercial activities in Java also facilitates the establishment of manufacturing facilities, streamlining production and distribution processes.

Dietary preferences across Indonesia vary significantly, reflecting the country's cultural and regional diversity. In rural areas, traditional sweeteners like palm sugar and coconut sugar remain deeply ingrained in local culinary practices and cultural traditions. These natural sweeteners are widely used in traditional dishes and beverages, maintaining their relevance in rural markets.

Regulatory Landscape

Indonesia regulates food sweeteners primarily through the National Agency of Drug and Food Control (BPOM) for processed foods and the National Food Agency (Badan Pangan Nasional, BPN) for fresh food categories, which creates distinct compliance tracks for additive functionalities that overlap across product types. BPOM Regulation No. 11/2019 serves as a core reference for permitted food additives (BTP), including sweeteners, with category-linked maximum use levels that manufacturers must follow in product formulation and labeling.

Regulatory tightening has continued through targeted updates, including BPOM Regulation No. 22/2023, which updates the list of prohibited raw materials and substances that cannot be used as food additives, raising screening and supplier-qualification requirements for importers and local blenders. Peraturan Badan Pangan Nasional Nomor 12 Tahun 2025 (enacted in December 2025 and published in early 2026) expands and formalizes requirements for food additives and processing aids used in fresh food, adding additional documentation and conformity checks for portfolios that serve both fresh and processed segments.

Value Chain Analysis

The value chain runs from upstream agricultural feedstocks, including domestic sugarcane and traditional crops for palm and coconut sugar (as well as limited domestic stevia cultivation), to a large import channel for raw materials and specialty ingredients. Commodity sugars are split between plantation white sugar for household channels produced by domestic mills, and refined sugar produced by a smaller set of refineries that rely on imported raw sugar and distribute primarily to the food and beverage industry under controlled allocation mechanisms.

Midstream activity includes refining and conversion into industrial sweeteners, such as starch-based syrups and polyols, followed by downstream blending. Global ingredient companies and local operators tailor sweetener systems for beverages, bakery, confectionery, dairy, and sauces, with Tereos FKS and PT Sugarindo Inti Bioplant supporting industrial starch and syrup sweeteners. Distribution relies on ingredient distributors and direct supply agreements to large food and beverage manufacturers concentrated in Java, where inter-island logistics favor shelf-stable powder formats. A recurring bottleneck is dependence on imported sugar and certain specialty non-sugar sweeteners, with availability influenced by government commodity-balance and import-allocation controls that shape procurement timing, pricing, and continuity for industrial users.

Competitive Landscape

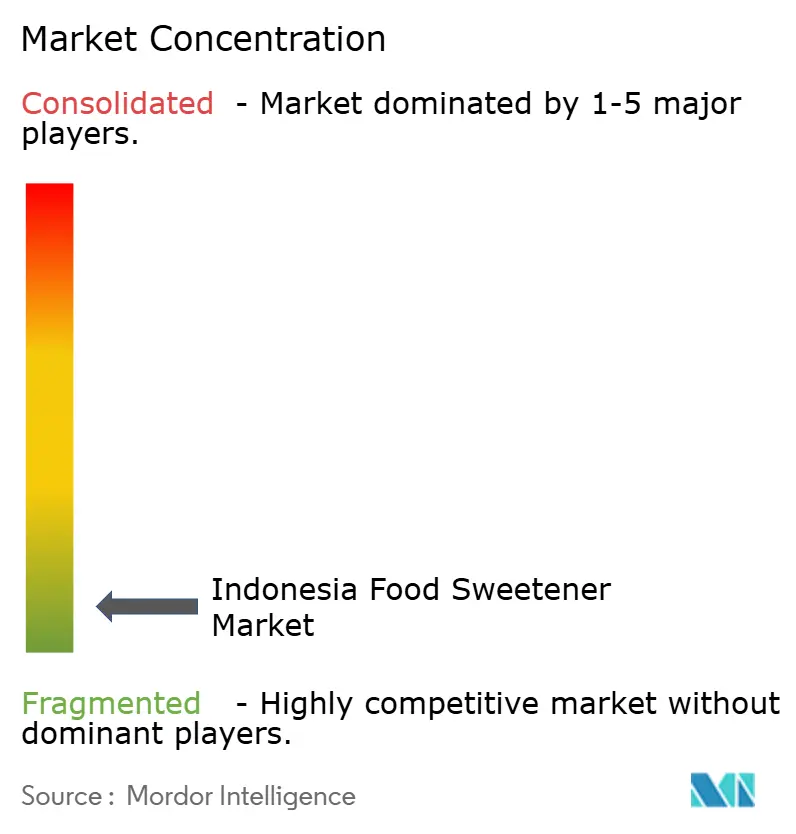

Indonesia's sweetener market is highly fragmented. The market dynamics allow global companies to leverage their technological expertise and extensive supply chain networks, while local firms capitalize on their deep understanding of cultural preferences and regulatory frameworks. This balance between global and local players fosters a competitive environment where diverse strategies can thrive.

Global leaders such as Cargill, Tate & Lyle, and Ingredion dominate the market by utilizing their advanced technological capabilities and economies of scale. These companies focus on optimizing production processes, ensuring consistent product quality, and maintaining robust supply chain operations to meet the growing demand for sweeteners. Their ability to innovate and adapt to global trends, such as the increasing demand for low-calorie and natural sweeteners, further strengthens their market position.

On the other hand, domestic players in the Indonesian sweetener market rely on their cultural insights and regulatory expertise to gain a competitive edge. These companies are well-versed in local consumer preferences and are adept at navigating the country's regulatory landscape, which can be complex and challenging for foreign entrants. The competitive dynamics are increasingly shifting toward innovation-driven differentiation, with both global and local players investing heavily in R&D and forming strategic partnerships.

Indonesia Food Sweetener Industry Leaders

-

Roquette Frères

-

Cargill, incorporated

-

Ingredion Incorporated

-

Archer Daniels Midland Company

-

Tate and Lyle PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Front-of-pack and nutrition policy actions are creating identifiable opportunities for sugar-reduction solutions across beverages and other processed foods. Demand is shifting toward high-intensity sweeteners, polyols, and blended systems that preserve taste and texture while lowering sugar load. In 2026, the Ministry of Health issued KMK HK.01.07/MENKES/301/2026 introducing Nutri-Level nutritional labeling and health messaging for ready-to-eat foods, and BPOM finalized updated front-of-pack nutrition labeling requirements for processed foods (Regulation No. 10/2026). With BPOM also communicating transition-period incentives for voluntary Nutri-Level adoption in packaged drinks, manufacturers have a near-term commercial incentive to accelerate reformulation and differentiate portfolios using alternative sweeteners.

Supply-side opportunities center on expanding local capability in application development, blending, and technical services that help manufacturers comply with labeling, meet halal expectations, and maintain sensory performance, particularly in the beverage segment that led the market by application in 2025. Trade bodies such as GAPMMI (food and beverage manufacturers) and P3JI (corn refiners producing starch-based inputs) offer organized counterparts for ingredient suppliers to coordinate reformulation toolkits, ingredient availability, and standards alignment. Investments that deepen Indonesia-based formulation and customer support, including local blending and specialty solution development for sweeteners and texturizers, align with archipelagic distribution constraints that favor stable formats and reliable supply continuity.

Recent Industry Developments

- July 2026: Indonesia finalized updated front-of-pack nutrition labeling requirements for processed foods, reinforcing the Nutri-Level approach that grades products based on sugar, salt, and fat content. This increases the commercial value of sugar-reduction formulations and raises demand for high-intensity sweeteners and blends that help brands achieve better label outcomes.

- March 2026: Roquette inaugurated a starch and polyol pilot center at its Lianyungang plant to accelerate application development for starch- and polyol-based ingredients. The added pilot capability supports faster innovation cycles and customer collaboration in sweetener-adjacent systems used in beverages and confectionery formulations supplied into Asian markets.

- August 2024: Cargill opened a new blending facility at its Pandaan site in East Java, strengthening its local capability in starches, sweeteners, and texturizers. The facility improves responsiveness for customized sweetener solutions and supports faster localization of formulations for Indonesian and broader Asian food and beverage customers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of sweeteners sold into food and beverage manufacturing in Indonesia, including caloric sweeteners and high-intensity options used to deliver sweetness and related functional roles in finished products.

Scope exclusions: Non-food uses (such as pharmaceuticals, personal care, and tabletop retail packs sold directly to consumers) are excluded from this sizing.

Segmentation Overview

-

By Type

- Sucrose (Common Sugar)

-

Starch Sweeteners and Sugar Alcohols

- Dextrose

- High Fructose Corn Syrup (HFCS)

- Maltodextrin

- Sorbitol

- Xylitol

- Others

-

High Intensity Sweeteners (HIS)

- Aspartame

- Saccharin

- Neotame

- Stevia

-

By Form

- Powder

- Liquid

- Others

-

By Source

- Natural

- Synthetic

-

By Application

- Bakery and Confectionary

- Dairy and Frozen Desserts

- Beverage

- Meat and Meat Products

- Soups, Sauces, and Dressings

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with pinning down Indonesia-specific demand signals and supply availability before any modeling assumptions were locked. We reviewed public references such as Statistics Indonesia (BPS) releases, UN Comtrade trade flows, FAOSTAT sugar balance style indicators, and relevant Codex and BPOM food additive guidance to understand permitted use and typical product placement.

To avoid relying on one data stream, we cross-checked with company annual reports, investor presentations, and credible press coverage on sweetener capacity, imports, and pricing moves. Patent databases were also used selectively to understand where formulation activity is heading, especially for high-intensity sweeteners and blends. The desk sources listed here are illustrative only, and additional public references were consulted to collect, validate, and clarify the final inputs.

Primary Interviews and Surveys

Primary conversations and short surveys were used to turn desk signals into usable ranges for pricing, inclusion rates, and substitution between sugar, starch-based sweeteners, sugar alcohols, and high-intensity options. We spoke with manufacturers, ingredient distributors, formulators, and downstream buyers so the model reflects how volumes and prices shift in Indonesia across packaged foods and beverages, not only how products are described in public sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | |

| Mid tier: 59% | Functional/Unit leaders: 39% | |

| Smaller Players: 15% | Managers: 47% |

Market-Sizing & Forecasting

Sizing was built mainly from a top-down demand pool, where Indonesia food and beverage output indicators and sweetener inclusion rates were used to reconstruct consumption by major application groups, then translated into value using realistic average selling prices. Once the total was formed, selective bottom-up checks were run through sampled supplier and distributor sell-in, plus channel checks on typical price bands, which helped correct outliers.

Inputs that mattered most included refined sugar and specialty sweetener import volumes, local production and capacity utilization signals, application-wise reformulation activity, price spread between sugar and alternatives, and packaging and beverage volume trends that change sweetener intensity. For the forecast, scenario analysis was used to reflect different paths for health-led sugar reduction, regulatory actions, and commodity price cycles, and scenario weights were refined through expert feedback. Where direct splits were not available, gaps were handled using proportional allocation based on reported product mix and validated with interview ranges, so the steps stay repeatable.

Data Validation & Update Cycle

Validation was done by comparing model outputs against independent signals, including trade totals, apparent consumption logic, and price movements that should track the same direction as the value series. Large variances were flagged, traced back to the driver assumptions, and then rechecked through follow-up discussions when a mismatch could not be explained by seasonality or one-off events.

Before sign-off, the full model goes through a second-analyst review to test formulas, year-on-year movement, and application splits for reasonableness. The report is refreshed annually, and interim updates are made when material events occur that can shift sweetener pricing or availability. Right before delivery, a final pass is completed so clients receive the latest updated view available.

Mordor Intelligence's Indonesia Food Sweetener Market Sizing Compared With Other Published Estimates

Published market values for Indonesia food sweeteners can look far apart because the counted product basket and the priced sales point are not always the same, and the time period and currency handling can further widen the gap. Differences also come from how firms treat blended sweeteners, whether they follow manufacturer selling prices or retail pricing, and how often key assumptions are refreshed.

Tabletop sweeteners sold as direct-to-consumer packs sit outside Mordor Intelligence's scope, which is one practical reason some larger figures appear when those retail channels are added to food manufacturing demand. Another common gap driver is ASP progression, where some estimates apply a single inflation rate across all types, even though sugar, polyols, and high-intensity sweeteners can move differently based on imports, contracts, and mix shifts. Finally, refresh cadence matters because Indonesia can see fast swings in sugar-linked inputs, and older price bases can push totals up or down versus a current-year check.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.17 B (2025) | |

| Global Consultancy A | USD 1.30 B (2023) | Uses an earlier base year and appears to mix food-manufacturing demand with broader sweetener sales, which can lift totals when retail packs and wider channels are included. |

| Industry Publisher B | USD 1.66 B (2025) | Leans on higher assumed price levels and faster mix-shift into specialty sweeteners, and it also applies aggressive growth expectations that are not always tied back to application output signals. |

Overall, the spread is best explained by what is included, which price point is used, and how pricing is carried forward over time. By keeping the demand pool tied to food manufacturing use, and by checking the value build with import, output, and pricing signals, the sizing remains transparent and easier to reproduce from year to year using the same steps.

Key Questions Answered in the Report

What is the projected value of the Indonesia food sweetener market by 2031?

The market is forecast to reach USD 1.45 billion by 2031, growing at a 3.66% CAGR.

Which product type segment shows the fastest growth rate?

High-intensity sweeteners lead with a projected 4.57% CAGR through 2031, driven by low-calorie beverage reformulation.

Which form factor dominates sales?

Powdered sweeteners hold the largest share, accounting for 71.88% of 2025 revenue thanks to shelf-life and logistics advantages in tropical climates.

Why are natural sweeteners gaining momentum?

Halal certification, clean-label preferences, and local cultivation of stevia and palm sugar are encouraging brands to shift from purely synthetic options.

Page last updated on: