Natural Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

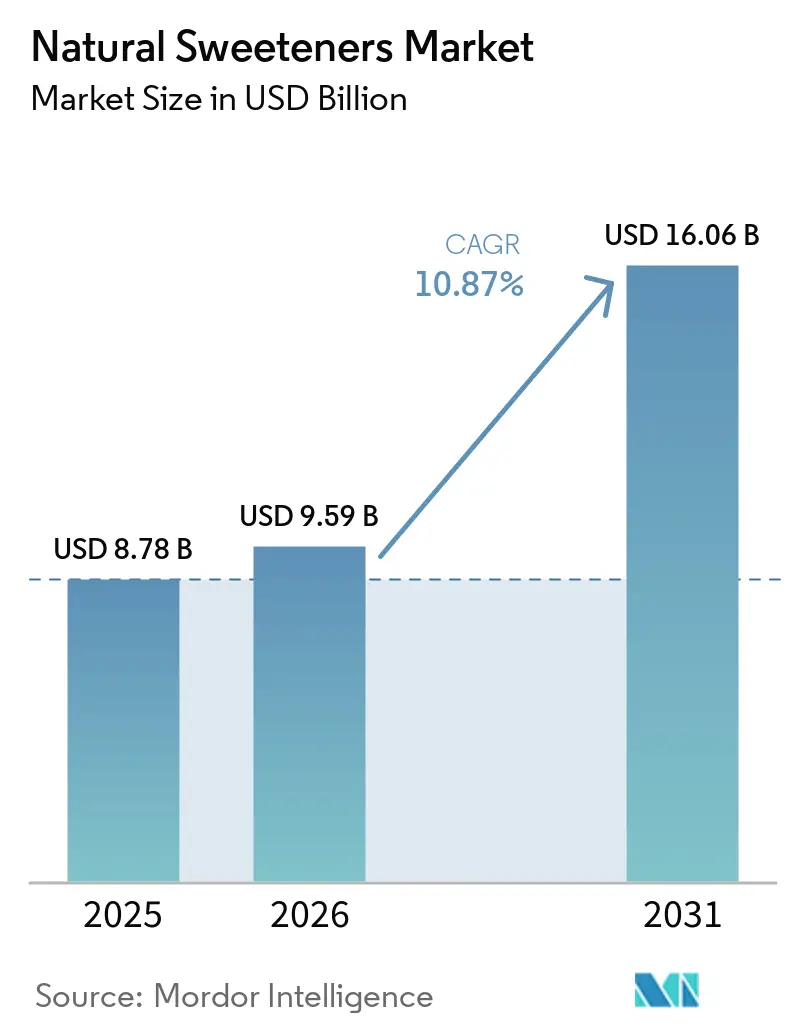

| Market Size (2026) | USD 9.59 Billion |

| Market Size (2031) | USD 16.06 Billion |

| Growth Rate (2026 - 2031) | 10.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Natural Sweeteners Market Analysis by Mordor Intelligence

The natural sweeteners market size is expected to grow from USD 8.78 billion in 2025 to USD 9.59 billion in 2026 and is forecast to reach USD 16.06 billion by 2031 at 10.87% CAGR over 2026-2031. The market expansion is attributed to the increasing consumer transition toward healthier dietary alternatives and heightened awareness regarding health conditions such as obesity, diabetes, and cardiovascular diseases. The escalating recognition of potential health implications associated with synthetic and high-calorie sweeteners has generated substantial demand for natural alternatives. The food and beverage industry's implementation of clean label practices and incorporation of natural ingredients in product formulations corresponds to consumer requirements for transparency and health-conscious options. Moreover, governmental policies advocating sugar reduction and regulatory frameworks supporting natural sweetener utilization further facilitate market expansion.

Key Report Takeaways

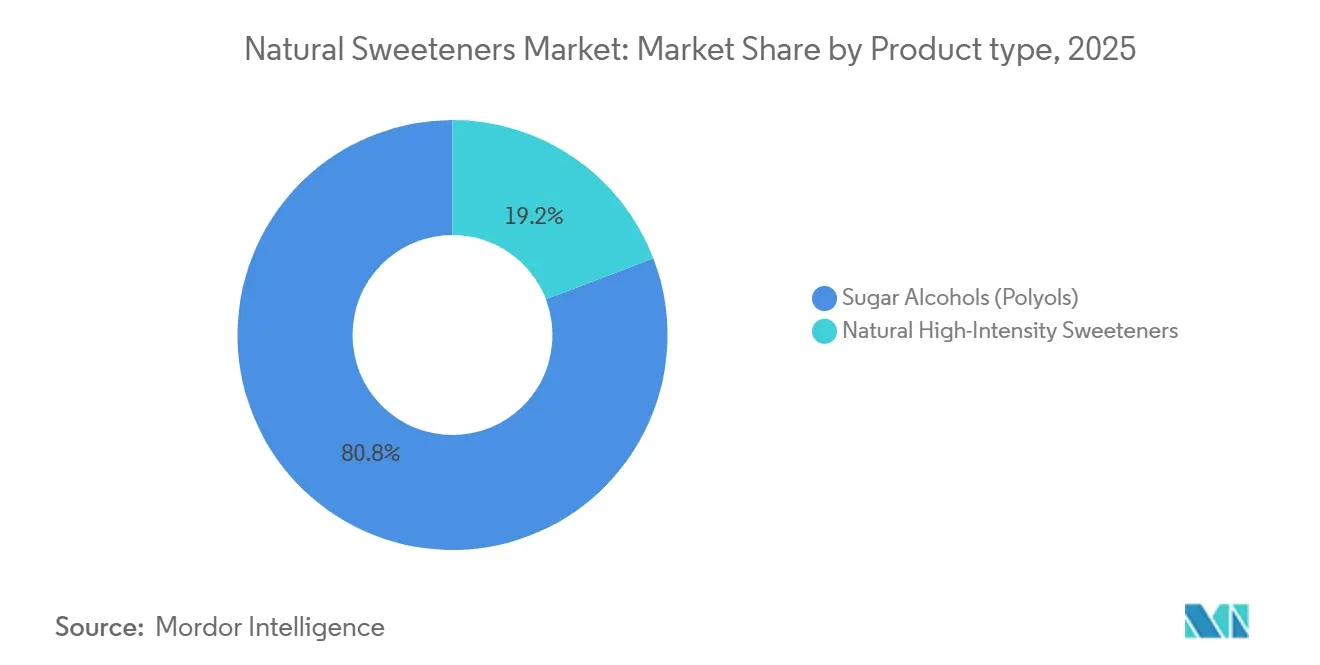

- By product type, sugar polyols sweeteners held 80.81% of the natural sweeteners market share in 2025, and natural high-intensity sweeteners are set to rise at a 13.01% CAGR through 2031.

- By form, solid formats commanded 81.10% revenue in 2025, while liquid/syrup forms are poised for a 11.90% CAGR to 2031.

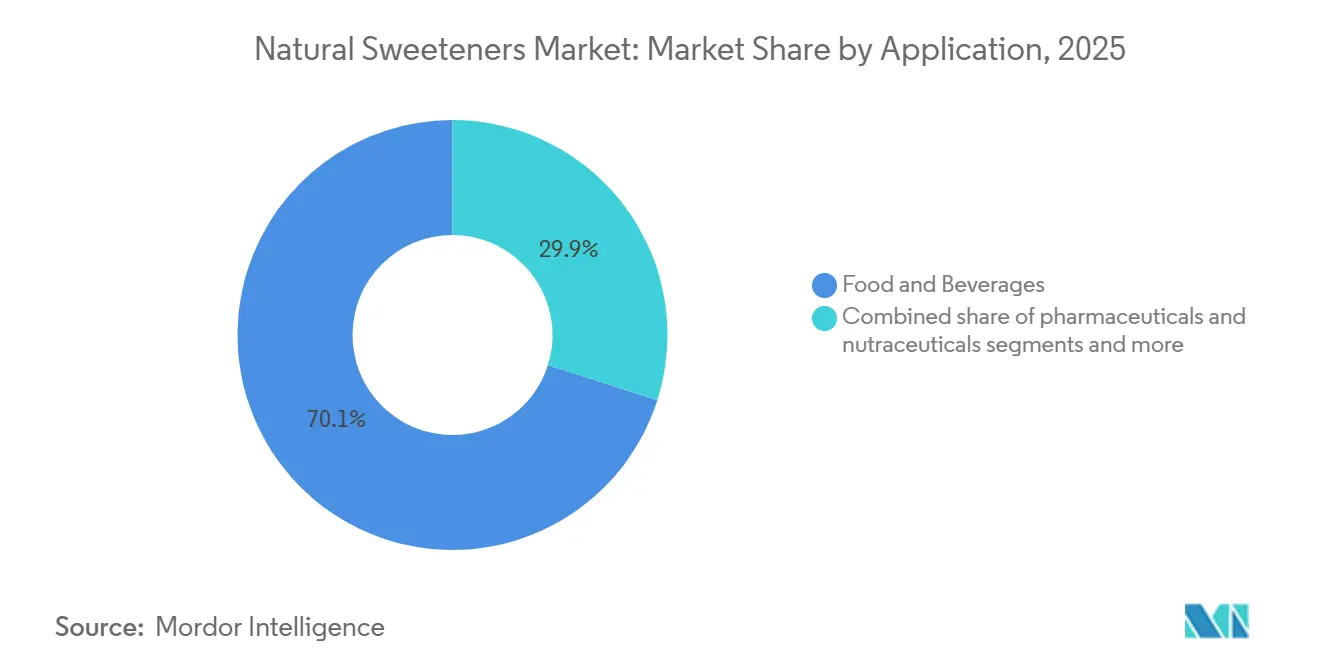

- By application, food and beverages accounted for 70.12% of the natural sweeteners market size in 2025, and pharmaceuticals and nutraceuticals will climb at a 12.35% CAGR by 2031.

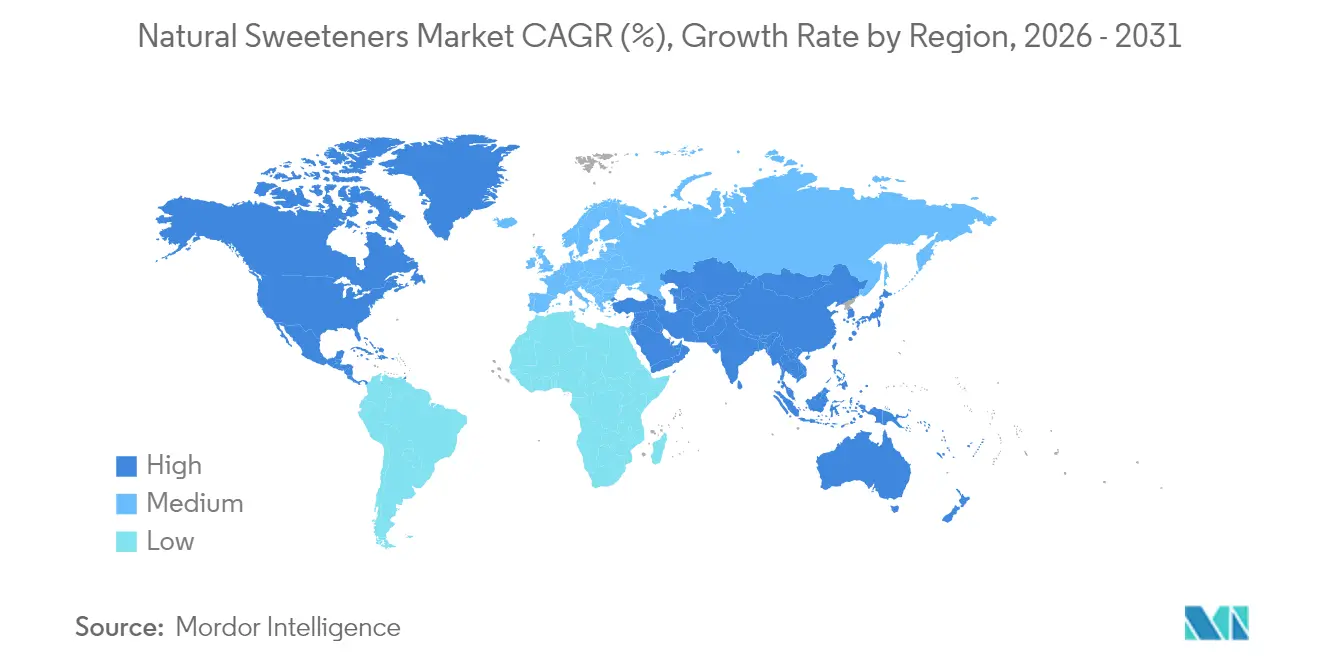

- By region, North America led with a 35.23% revenue slice in 2025, whereas Asia-Pacific is forecast to pace ahead at a 11.83% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Natural Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer awareness about health risks associated with artificial sweeteners | +2.1% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Rising prevalence of diabetes and obesity | +1.8% | Global, with significant impact in North America, Europe, and urban centers in Asia-Pacific | Long term (≥ 4 years) |

| Increasing adoption of natural ingredients in food and beverage manufacturing | +1.5% | Global, with higher adoption rates in developed markets | Medium term (2-4 years) |

| Government regulations supporting the use of natural sweeteners over artificial alternatives | +1.2% | North America, Europe, and progressive adoption in Asia-Pacific | Short term (≤ 2 years) |

| Technological advancements improving the taste and functionality of natural sweeteners | +1.0% | Global, with faster adoption in developed markets with advanced research and development capabilities | Medium term (2-4 years) |

| Rising disposable income enables consumers to purchase premium natural sweetener products | +0.8% | Asia-Pacific, Latin America, and emerging markets with growing middle class | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing consumer awareness about health risks associated with artificial sweeteners

The natural sweeteners market is primarily driven by increasing consumer awareness about potential health risks associated with artificial sweeteners. Health authorities' scrutiny and scientific research have raised concerns about the long-term safety of synthetic sweeteners, including aspartame, saccharin, and sucralose. The International Agency for Research on Cancer's (IARC) 2023 classification of aspartame as "possibly carcinogenic to humans" has heightened public concern and increased demand for natural alternatives [1]Source: International Agency for Research on Cancer (IARC), "Aspartame hazard and risk assessment results released"www.iarc.who.int. Moreover, artificial sweeteners may adversely affect gut microbiota, potentially impacting metabolic functions and glucose regulation. These findings have led to increased skepticism toward synthetic additives, particularly among health-conscious consumers and individuals managing diabetes or obesity, resulting in a shift toward clean-label and natural ingredients.

Rising prevalence of diabetes and obesity

According to the International Diabetes Federation, approximately 589 million adults (20-79 years) are living with diabetes, with over 4 in 5 adults (81%) in low- and middle-income nations [2]Source: International Diabetes Federation, "Diabetes around the world in 2024", idf.org. Alarmingly, over half of these individuals lack access to treatment. In response to this pressing health challenge, there's been a surge in demand for glucose-neutral sugar substitutes. Natural sweeteners, notably stevia and monk fruit, have gained prominence due to their zero glycemic index. These sweeteners are now integral to medical nutrition therapy for diabetes patients. Studies highlight that steviol glycosides can boost insulin sensitivity and improve glucose tolerance. The U.S. Department of Agriculture's Dietary Guidelines for Americans 2025-2030 recommend that added sugars should constitute no more than 10% of daily caloric intake, further emphasizing the shift towards natural sweeteners. As obesity rates climb, especially in emerging markets leaning towards Western diets, the natural sweeteners market continues to flourish, suggesting this growth trend will persist well beyond the forecast period.

Increasing adoption of natural ingredients in food and beverage manufacturing

The clean-label movement has shifted from a niche trend to a core consumer demand. The Organic Trade Association (OTA) reported that U.S. organic product sales reached USD 71.6 billion in 2024. This shift has led food and beverage manufacturers to feature natural sweeteners in sugar reduction strategies. Natural sweeteners are now used in savory products, balancing flavors and reducing sodium. The FDA's Nutrition Innovation Strategy has supported natural ingredient adoption in food formulations. Companies are addressing challenges like stability and taste through research and development. Advances in flavor modulation and improved manufacturing processes have enabled broader market penetration. Growing consumer awareness of health benefits further drives demand.

Government regulations supporting the use of natural sweeteners over artificial alternatives

Regulatory frameworks are fostering growth for natural sweeteners through incentives and restrictions. The FDA's final rule on "healthy" claims, effective February 2025, limits added sugars while exempting products with high-intensity natural sweeteners. Sugar taxes have also improved the cost competitiveness of natural sweeteners. From the 2025-26 school year, the USDA's new school nutrition standards will require reduced added sugar in meals, driving demand for natural sweeteners in schools. The European Food Safety Authority's re-evaluation of sweeteners may influence market dynamics with updated safety assessments. Government-backed campaigns on sugar reduction are increasing consumer awareness and preference for natural alternatives. Policymakers are likely to further support natural sweeteners to address healthcare costs tied to diet-related diseases. Major markets, including the European Union, are considering additional measures to reduce sugar consumption and promote healthier options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs compared to artificial sweeteners | -0.9% | Global, with higher impact in price-sensitive markets in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Limited availability of raw materials for natural sweetener production | -0.7% | Global, with particular impact on stevia and monk fruit supply chains originating in Asia | Short term (≤ 2 years) |

| Competition from Artificial Sweeteners may hamper the market growth | -0.6% | Global, with stronger impact in cost-sensitive applications and developing markets | Medium term (2-4 years) |

| Technical Challenges in Food Processing Applications | -0.5% | Global, with higher impact in complex food formulations requiring specific functional properties | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher production costs compared to artificial sweeteners

Natural sweeteners face significant market penetration challenges due to their higher production costs compared to artificial alternatives like aspartame and sucralose. This cost difference impacts mass market applications and price-sensitive regions, where manufacturers operate with minimal margins and consumers demonstrate limited willingness to pay premium prices for natural ingredients. The elevated production costs restrict natural sweeteners' adoption across various food categories, despite increasing consumer interest. While established natural sweeteners like stevia have achieved some cost reductions through economies of scale, new alternatives such as monk fruit and rare sugar alcohols maintain substantial price premiums. The U.S. International Trade Commission's investigation into erythritol imports from China illustrates how production costs and pricing affect market dynamics, with domestic producers competing against lower-cost imports. Despite production technology improvements, costs remain a limiting factor in the medium term, especially in applications where price sensitivity outweighs clean-label preferences.

Limited availability of raw materials for natural sweetener production

Supply chain vulnerabilities hinder market growth in the natural sweeteners industry, making sourcing more complex than synthetic alternatives. Agricultural supply chains are critical to national and economic security, especially for specialized crops used in natural sweeteners. Stevia leaf production's geographic concentration increases risks from climate events, political unrest, and trade disputes. Similarly, monk fruit supply is vulnerable due to its cultivation being limited to southern China. The agricultural nature of these ingredients creates challenges in yield and quality consistency, complicating production planning. Companies are addressing these issues through vertical integration and regional diversification. While fermentation-based biotechnology offers potential to reduce agricultural input reliance, it currently serves only premium segments as it scales. Raw material constraints, especially during peak demand or supply disruptions, will continue to limit market growth until alternative methods reach commercial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: High-Intensity Sweeteners Lead Innovation Wave

Sugar alcohols (polyols) made up the largest portion of the natural sweeteners market, contributing 80.81% of the total revenue in 2025. This segment leads the market due to its extensive use in sugar-free and low-calorie food and beverage products, such as candies, baked goods, chewing gum, and dairy substitutes. Popular sugar alcohols like erythritol, xylitol, maltitol, and sorbitol provide sweetness with fewer calories compared to regular sugar. This makes them a preferred choice for manufacturers aiming to cater to health-conscious consumers. Additionally, these sweeteners offer functional benefits, such as adding bulk, improving texture, and enhancing stability, making them suitable for a wide range of food applications.

Natural high-intensity sweeteners are expected to grow the fastest, with a projected CAGR of 13.01% during 2026–2031. The increasing demand for clean-label, plant-based, and low-calorie sweetening options is driving the popularity of ingredients like stevia and monk fruit extracts. Food and beverage companies are increasingly using these sweeteners to reduce sugar content while maintaining the desired sweetness in their products. Advances in extraction methods and taste-masking technologies are further improving the quality of these sweeteners, making them more appealing for use in beverages, snacks, dairy products, and nutritional supplements. This trend reflects the growing consumer focus on healthier and more natural alternatives to traditional sugar.

By Form: Liquid Formats Gain Momentum

Solid sweeteners dominate the market with a 81.10% share in 2025. The Liquid/Syrup segment will grow at 11.90% CAGR from 2026 to 2031, primarily due to its superior performance in beverages, the largest and fastest-growing end-use category. Beverage manufacturers prefer liquid sweeteners because they dissolve faster, spread more evenly, and work efficiently in continuous production lines. Ready-to-drink beverage producers especially benefit from liquid sweeteners during cold-fill processing, as this method protects sensitive ingredients and uses less energy.

Food manufacturers continue to choose solid sweeteners because they need exact measurements, longer shelf life, and efficient transportation. New encapsulation technologies have made solid sweeteners better by improving their stability, controlling how they release, and reducing unwanted tastes. Companies now produce both solid and liquid sweeteners to serve more applications and reach wider markets. This dual approach helps manufacturers meet diverse customer needs across the food and beverage industries.

By Application: Food and Beverages Drive Market Growth

The Food and Beverages segment holds a dominant 70.12% market share in 2025. Beverages represent the primary application area, particularly in carbonated soft drinks, where manufacturers are reformulating products to reduce sugar content and artificial ingredients. The Food and Drug Administration (FDA)'s Front-of-Package Nutrition Information rule, introduced in January 2025, requires clear labeling of nutrients, including added sugars, influencing beverage manufacturers to adjust their formulations. In food applications, bakery and confectionery products are the main adopters of natural sweeteners, as these categories typically contain high levels of sugar and must meet consumer demand for healthier alternatives.

The pharmaceuticals and nutraceuticals sector is steadily growing at a CAGR of 12.35% through 2031 as natural sweeteners gain traction in functional foods, dietary supplements, and over-the-counter medications. Their low glycemic impact makes them ideal for diabetic and health-conscious consumers, with applications in sugar-free vitamins, lozenges, and syrups. Regulatory approvals further support their use in pediatric and geriatric products. The Personal Care and Cosmetics segment, though smaller, shows potential. Xylitol is used in oral care for dental benefits, while other sweeteners are incorporated into lip balms and skincare for their humectant and soothing properties, aligning with the clean beauty trend.

Geography Analysis

North America leads the natural sweeteners market with a 35.23% share in 2025, driven by stringent regulatory frameworks and high consumer awareness of health issues associated with sugar consumption. The region's well-established food and beverage industry, combined with regulations on sugar intake, supports market growth. The presence of key industry players has strengthened research and development activities and product innovation. The increasing prevalence of lifestyle-related diseases influences market expansion. According to the Centers for Disease Control and Prevention's National Diabetes Statistics Report, more than 38 million Americans have diabetes (about 1 in 10), and about 90% to 95% have type 2 diabetes, creating substantial demand for sugar alternatives .

Asia-Pacific is the fastest-growing region with a projected CAGR of 11.83% from 2026-2031, driven by increasing health consciousness, rising disposable incomes, and growing prevalence of lifestyle diseases in countries like China and India. China dominates regional production of key natural sweeteners, including stevia and monk fruit, providing local manufacturers with competitive advantages through vertical integration and supply chain control. Japan represents a mature market with high natural sweetener penetration, having approved stevia before Western markets, while India emerges as a high-growth opportunity due to its large diabetic population and government initiatives to reduce sugar consumption.

Europe maintains a significant market presence, characterized by stringent regulatory standards and consumer preferences for clean-label products. The European Food Safety Authority's ongoing re-evaluation of sweeteners, including erythritol's safety assessment in December 2023, demonstrates the region's methodical approach to natural sweetener adoption. The European Commission's Farm to Fork Strategy supports natural sweetener adoption through its focus on sustainable food systems and healthier diets. The United Kingdom's sugar tax on soft drinks, implemented in 2018 and expanded in 2024, has increased demand for natural sweeteners in beverages. Nordic countries lead adoption rates with consumers willing to pay premiums for natural products, while Southern European markets show growing interest based on traditional emphasis on natural ingredients and Mediterranean dietary patterns.

Competitive Landscape

The natural sweeteners market demonstrates a fragmented competitive structure, with regional and global market players dominating the market. Major players in the market are Tate & Lyle Plc, Archer Daniels Midland Company, Cargill Incorporated, DSM-Firmenich AG, and Ingredion Incorporated, among others. These industry leaders have developed robust vertical integration strategies across their value chains to optimize operational efficiency, maintain quality control, and strengthen their cost competitiveness in the global market.

Companies are pursuing strategic collaborations and acquisitions to enhance their market positions, expand product portfolios, and acquire new technologies. For instance, in October 2024, Tate & Lyle PLC partnered with Manus, a bio alternatives scale-up platform, to launch stevia Reb M, representing the first large-scale commercialization of an all-Americas-sourced, manufactured, and bio-converted stevia Reb M ingredient.

Stringent regulatory frameworks and compliance requirements significantly influence the competitive dynamics. Manufacturers must strategically adapt their product development, manufacturing processes, and market entry strategies to meet diverse regulatory standards across different geographical regions. This regulatory compliance is crucial for maintaining market access and expanding global market presence while ensuring product safety and quality standards.

Natural Sweeteners Industry Leaders

-

Cargill Inc.

-

Archer-Daniels-Midland Company

-

Tate & Lyle PLC

-

Ingredion Incorporated

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: NutraEx Food, Inc. launched Bi-Sugar, created through its dry-embedding technology that bonds L-arabinose to regular sugar and another natural sweetener. Bi-Sugar can be used in beverages, bakery products, confectionery, and dairy applications, while also providing caramel notes.

- August 2024: Howtian introduced SoPure Dorado, a natural sweetener designed to address the increasing demand for minimally processed, plant-based products. SoPure Dorado is an unrefined golden stevia extract that functions as a zero-calorie sweetener.

- July 2024: Tate & Lyle PLC introduced Optimizer Stevia 8.10, a stevia composition that provides a taste profile similar to sugar at high replacement levels while being more cost-effective than comparable sweeteners.

- May 2024: Ingredion introduced PureCircle Clean Taste Solubility Solution, a drop-in stevia ingredient. The product exhibits 100 times higher solubility than Reb M stevia and can achieve complete sugar reduction.

Global Natural Sweeteners Market Report Scope

Natural Sweeteners are sugar substitutes obtained from natural or organic sources like plants, microbes, and other sources. The natural sweeteners market is segmented based on product type, form, application, and geography. By product type, the market is segmented into Natural High-Intensity Sweeteners, Sugar Alcohols (Polyols), and Others. By form, the market is segmented into Solid and Liquid/Syrup. By application, the market is segmented into Food and Beverages, Pharmaceuticals & Nutraceuticals, Personal Care & Cosmetics, and Other Applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Natural High-Intensity Sweeteners | Stevia |

| Monk Fruit (Luo Han Guo) | |

| Others | |

| Sugar Alcohols (Polyols) | Xylitol |

| Sorbitol | |

| Mannitol | |

| Erythritol | |

| Others |

| Solid |

| Liquid/Syrup |

| Food and Beverages | Food | Bakery and Confectionery |

| Dairy and Desserts | ||

| Meat and Savory Products | ||

| Sauces, Dressings and Spreads | ||

| Other Processed Foods | ||

| Beverages | Soft Drinks | |

| Sport Drinks | ||

| Other Beverages | ||

| Pharmaceuticals and Nutraceuticals | ||

| Personal Care and Cosmetics | ||

| Other Applications | ||

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Natural High-Intensity Sweeteners | Stevia | |

| Monk Fruit (Luo Han Guo) | |||

| Others | |||

| Sugar Alcohols (Polyols) | Xylitol | ||

| Sorbitol | |||

| Mannitol | |||

| Erythritol | |||

| Others | |||

| By Form | Solid | ||

| Liquid/Syrup | |||

| By Application | Food and Beverages | Food | Bakery and Confectionery |

| Dairy and Desserts | |||

| Meat and Savory Products | |||

| Sauces, Dressings and Spreads | |||

| Other Processed Foods | |||

| Beverages | Soft Drinks | ||

| Sport Drinks | |||

| Other Beverages | |||

| Pharmaceuticals and Nutraceuticals | |||

| Personal Care and Cosmetics | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current size of natural sweeteners market?

The market is valued at USD 9.59 billion in 2026 and is projected to reach USD 16.06 billion by 2031.

Which segment holds the largest natural sweeteners market share?

Sugar Alcohols (Polyols) captured 80.81% revenue in 2025.

Which region is growing the fastest for natural sweeteners?

Asia-Pacific shows the sharpest rise, advancing on a 11.83% CAGR through 2031.

Why are liquid natural sweeteners gaining popularity?

Liquids dissolve faster, improve process efficiency in beverages, and support cold-fill lines, fueling a 11.90% CAGR for this form.

Page last updated on: