Artificial Sweetener Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 5.38 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Artificial Sweetener Market Analysis by Mordor Intelligence

The artificial sweetener market size is expected to grow from USD 4.09 billion in 2025 to USD 4.28 billion in 2026 and is forecast to reach USD 5.38 billion by 2031 at 4.63% CAGR over 2026-2031. This growth indicates a shift in focus toward creating better-quality products, introducing innovative formulations, and expanding their use in various industries, rather than just increasing production. The rising demand for artificial sweeteners is largely driven by consumers who are managing weight, diabetes, and other metabolic health issues. Regulatory organizations like the FDA and EFSA continue to confirm the safety of approved low-calorie sweeteners, as long as they are consumed within the recommended limits. In terms of types, sucralose remains a strong performer, while newer options like advantame are growing faster than others. When it comes to forms, powdered sweeteners continue to dominate, but liquid sweeteners are gaining popularity due to their convenience. Among applications, beverages remain the largest segment, but the use of artificial sweeteners in pharmaceuticals is growing rapidly. The artificial sweetener market is moderately concentrated, with major players such as Cargill, Archer Daniels Midland, and Ingredion leading the competition. These companies benefit from their vertically integrated supply chains, global research and application labs, and diverse product portfolios. Their ability to innovate and adapt to changing consumer preferences helps them maintain a strong position in the market.

Key Report Takeaways

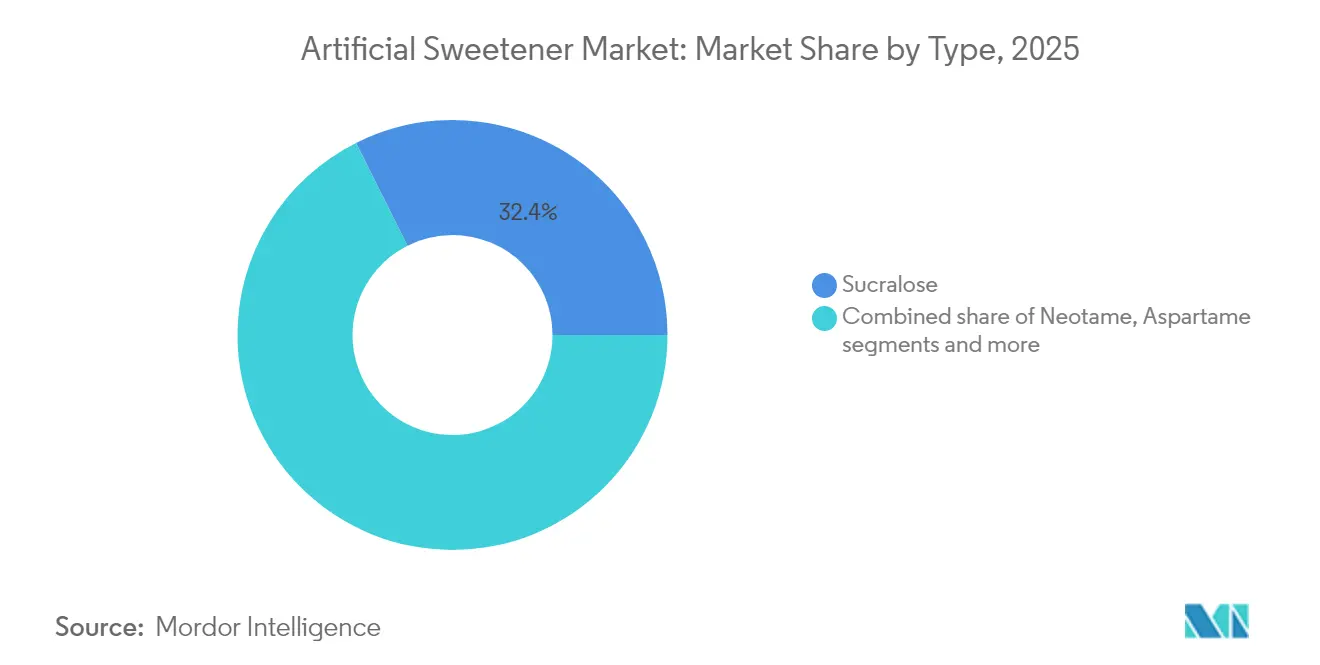

- By type, sucralose led with 32.41% artificial sweetener market share in 2025, whereas advantame is forecast to expand at a 5.82% CAGR through 2031.

- By form, the powder segment commanded 72.96% of the artificial sweetener market size in 2025, and liquid solutions show the fastest growth at 5.88% CAGR to 2031.

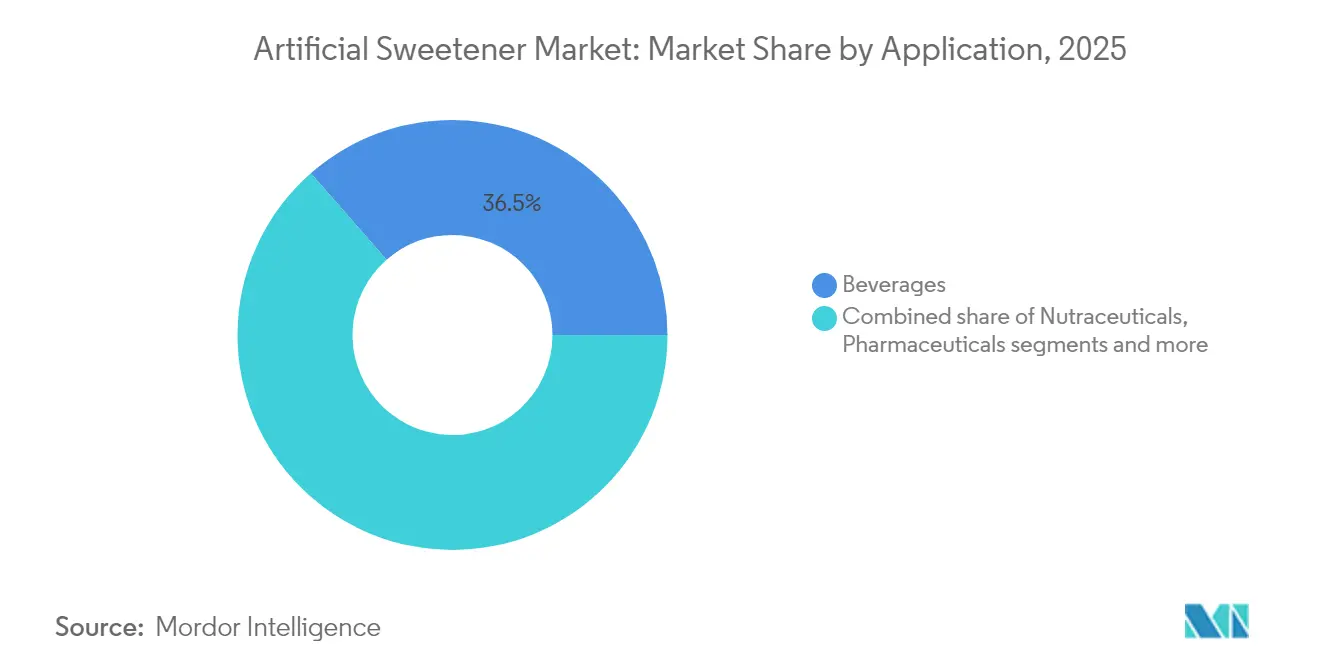

- By application, beverages accounted for 36.45% of revenue in 2025, while pharmaceuticals and nutraceuticals are projected to grow 6.18% annually through 2031.

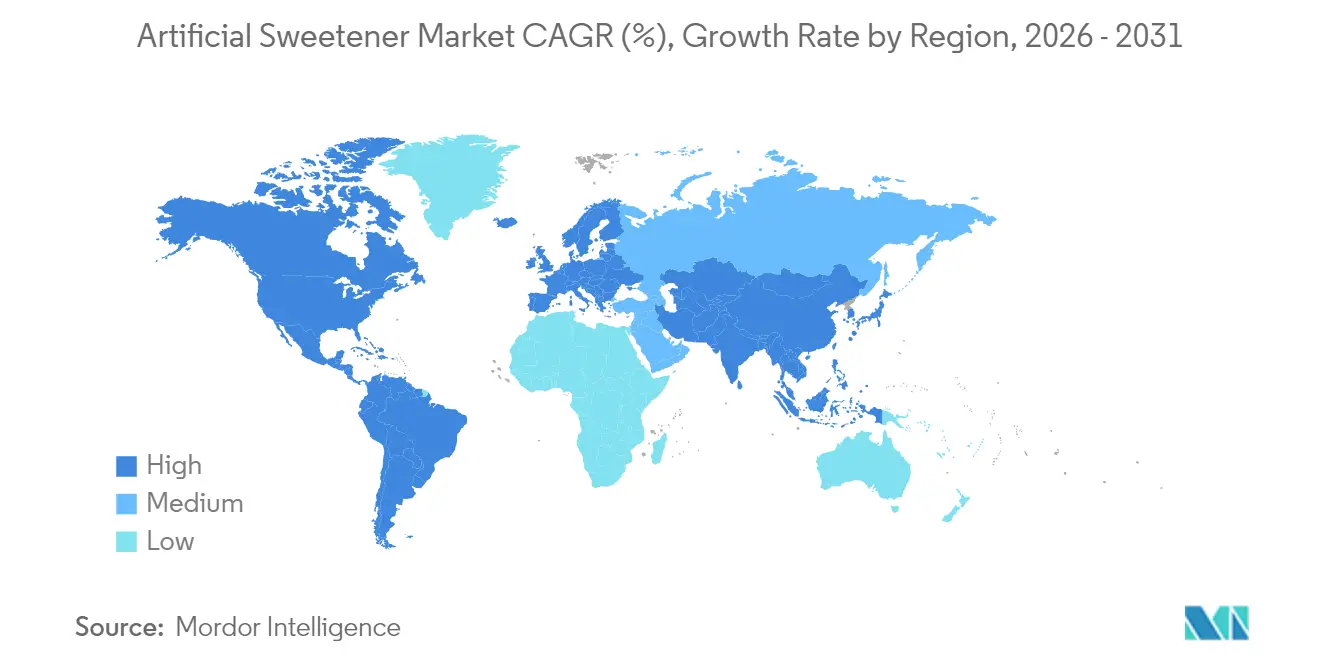

- By geography, Asia-Pacific contributed 31.78% of the share of artificial sweeteners in 2025, and the Middle East and Africa are projected to post the highest regional CAGR at 6.07% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Sweetener Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of obesity and diabetes driving artificial sweetener adoption | +1.2% | Global, with highest impact in North America and Asia-Pacific | Long term (≥ 4 years) |

| Increasing penetration of sugar-free confectionary products | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Longer shelf life of artificial sweeteners | +0.3% | Global, particularly relevant in emerging markets | Short term (≤ 2 years) |

| Surging consumer demand for zero-calorie beverages | +1.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Consumer inclination towards sugar substitutes in weight management | +0.9% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Technological advancement enhancing sweetener taste and stability | +0.7% | Global, with innovation centers in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of obesity and diabetes driving artificial sweetener adoption

The global artificial sweeteners market is steadily growing, mainly due to the rising rates of obesity and diabetes, which are encouraging people to switch to low-calorie and sugar-free alternatives. According to the International Diabetes Federation, approximately 589 million adults worldwide are currently living with diabetes, and this number is expected to increase to 853 million by 2050[1]Source: Diabetes Atlas Org, "Diabetes Global Report 2000 — 2050," diabetesatlas.org. Similarly, the World Obesity Federation estimates that by 2035, over 750 million children aged 5–19 will be overweight or obese[2]Source: World Obesity Org, "World Obesity Atlas 2024," worldobesity.org. To tackle these health issues, healthcare providers are increasingly using artificial sweeteners like aspartame and sucralose in clinical nutrition plans. Hospitals are also expanding their sugar-free meal options to help patients better manage their diets. Pharmaceutical companies are incorporating heat-stable sweeteners such as sucralose into medications to improve their taste, making it easier for patients to take them as prescribed. This growing demand from the healthcare and pharmaceutical sectors ensures a stable and reliable foundation for the artificial sweeteners market, supporting consistent growth even when consumer preferences change.

Increasing penetration of sugar-free confectionery products

The rising preference for healthier treats is driving the growth of sugar-free confectionery products. This shift has encouraged leading global confectionery brands to reformulate their best-selling products to stay competitive in the market. Sugar-free options, including chocolates, gums, and gummies, are increasingly occupying premium shelf space in North America and Europe. At the same time, the Asia-Pacific region is gradually seeing the introduction of new sugar-free product lines. According to Food Insights, as of 2024, 66% of American consumers are actively working to reduce their sugar intake, an increase from 61% in previous years[3]Source: Food Insights, "2024 IFIC Food and Health Survey," foodinsight.org. This trend highlights the growing popularity of the zero-sugar food and beverage category, as consumers are showing a greater willingness to pay more for healthier alternatives. To cater to this demand, manufacturers are turning to artificial sweeteners like sucralose and neotame, often combined with flavor enhancers, to closely mimic the taste of traditional products. This strategy not only helps retain customer loyalty but also enables companies to address challenges such as sugar taxes.

Surging consumer demand for zero-calorie beverages

The rising demand for zero-calorie beverages is driving significant growth in the artificial sweeteners market, as manufacturers innovate to align with changing consumer preferences. A 2024 survey by Archer Daniels Midland Company highlights that a large portion of the global population is actively reducing sugar consumption, with countries like Mexico, Spain, Romania, and Brazil reporting that nearly 90% of their populations are limiting or avoiding sugar[4]Source: Archer Daniels Midland, "ADM Launches Sweet Insights Tool For Navigating Sugar Reduction Trends, Worldwide," adm.com. To cater to this shift, leading sweetener producers such as Tate & Lyle, PureCircle (a subsidiary of Ingredion), and JK Sucralose are creating advanced formulations that closely replicate the taste and texture of sugar. For instance, Tate & Lyle introduced its Zerose® Allulose Liquid in 2024, offering new formats specifically designed for beverages, while Ingredion expanded its BESTEVIA® Reb M line of stevia-based sweeteners, optimized for zero-calorie sodas and sparkling waters. These innovations are enabling beverage companies to reformulate products like sodas, ready-to-drink coffees, and alcohol-free spirits with improved taste and stability.

Technological advancement enhancing sweetener taste and stability

Advancements in technology are making artificial sweeteners more versatile, tastier, and better suited for a wide range of food and beverage applications. Precision fermentation techniques are now enabling the production of rare steviol glycosides like Reb M and Reb D on a large scale. These newer versions of stevia offer a cleaner, more sugar-like taste, eliminating the bitterness that was common in earlier formulations. For example, Avansya, a joint venture between Cargill and DSM-Firmenich, has developed high-purity sweeteners, Eversweet, that allow for completely sugar-free products without sacrificing flavor. Advantame, which is about 20,000 times sweeter than regular sugar, is gaining popularity due to its excellent heat stability, making it ideal for baked goods and ultra-high-temperature (UHT) dairy products. At the same time, innovations in encapsulation and co-crystallization are improving the shelf life, solubility, and performance of sweeteners in challenging product environments, such as acidic beverages and high-protein shakes.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent regulatory scrutiny and labeling requirements | -0.6% | Global, with varying intensity by region | Medium term (2-4 years) |

| Consumer preference for "clean or natural label" and additive-free products | -0.9% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Potential carcinogenicity sweeteners like saccharin and aspartame | -0.7% | Global, with highest impact in health-conscious markets | Medium term (2-4 years) |

| Consumer inclination towards plant-based sweeteners | -0.5% | North America and Europe, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory scrutiny and labeling requirements

Regulatory challenges are becoming a significant hurdle for the artificial sweeteners market, with new rules and health concerns shaping the industry in 2024. For instance, the World Health Organization's earlier classification of aspartame as "possibly carcinogenic" has pushed many brands to reformulate their products to address consumer concerns. Similarly, the European Food Safety Authority (EFSA) recently lowered the acceptable daily intake (ADI) for erythritol to 0.5 g/kg, forcing manufacturers to adjust formulations and update product labels to comply with the new standards. EFSA is reassessing other sweeteners like acesulfame K, creating further uncertainty for the industry. Around the world, varying regulations, such as additive limits imposed by the Gulf Cooperation Council, are compelling companies to adopt market-specific strategies. To manage these challenges, businesses are investing in larger compliance teams to handle the increasing legal complexities, rising operational costs, and the risk of sudden regulatory changes that could impact ingredient approvals.

Consumer preference for “clean or natural label” and additive-free products

Consumers are showing a growing preference for clean-label and additive-free products, which is posing significant challenges for the artificial sweeteners market. This shift is particularly evident among health-conscious individuals and younger demographics. A 2025 study published in MDPI found that 74.1% of parents and 54.2% of students view artificial sweeteners negatively, despite their approval by regulatory authorities. This skepticism has led many consumers, especially Gen Z and millennials, to closely examine ingredient labels and choose natural alternatives such as stevia, monk fruit, or unrefined sugars. To address these concerns, artificial sweetener manufacturers are adapting by emphasizing fermentation-based production processes, improving transparency in their supply chains, and showcasing better environmental sustainability practices. However, despite these efforts, the negative perception of artificial sweeteners remains a significant barrier, particularly in markets where consumers prioritize natural and clean-label products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Performance Edge Sustains Sucralose while Advantame Outpaces Rivals

Sucralose continues to dominate the artificial sweeteners market in 2025, holding a 32.41% market share due to its excellent heat stability and neutral flavor, which make it a preferred choice for beverages and baked goods. Its widespread regulatory approvals across major regions further strengthen its market presence. Meanwhile, advantame is expected to grow at the fastest rate, with a projected CAGR of 5.82% through 2031. This growth is driven by its ultra-high sweetness potency, which helps manufacturers reduce ingredient costs, particularly in large-scale production of carbonated soft drinks. Although the World Health Organization's review of aspartame raised concerns, the sweetener remains a staple in legacy diet sodas, where consumer loyalty is tied to familiar taste profiles.

Regulatory developments are also shaping the market, with the European Food Safety Authority (EFSA) maintaining its support for steviol glycosides. A 2025 EFSA opinion is expected to authorize the use of stevia in four new food categories, signaling a growing acceptance of natural sweeteners. This regulatory flexibility is encouraging global manufacturers to combine stevia with sucralose or advantame, creating sweetener blends that mimic the taste of sugar while keeping production costs in check. Suppliers with extensive patent portfolios and advanced application support capabilities are well-positioned to capitalize on these trends, particularly during major beverage contract renewals.

By Form: Powder Incumbency Meets Rising Liquid Convenience

Powder commanded 72.96% of the artificial sweetener market in 2025 thanks to its superior shelf stability, easy tonnage transport, and compatibility with dry-blend bakery mixes. Pharmacies and nutraceutical firms value consistent granulation when cross-blending actives, tightening demand for micronized grades. Liquid formats, however, advance at a 5.88% CAGR, championed by ready-to-drink beverage categories where homogeneous dispersion under high-speed filling is essential. Liquid sucralose concentrates reduce dissolution times and cleaning cycles, cutting overall line downtime for co-packers. Suppliers now develop concentrated syrups that carry 1.5× the sweetness of earlier versions, compressing freight footprints and storage costs.

Advancements in technology are further bridging the performance gap between powder and liquid formats. Encapsulated powder variants now offer improved wettability, providing bakery producers with a versatile option when thermal stability is a priority. Similarly, liquid blends have been enhanced with shelf-stable antimicrobial systems approved in both the U.S. and EU, extending their unopened shelf life to up to 24 months. These innovations are intensifying competition between the two formats, prompting procurement managers to reassess their total cost-of-ownership models during each contract cycle. As a result, both powder and liquid formats are evolving to meet the diverse needs of manufacturers across various industries.

By Application: Beverage Primacy Endures as Pharmaceuticals Accelerate

Beverages held 36.45% revenue in 2025 and represent the traditional growth engine for the artificial sweetener market. The segment benefits from embedded consumer awareness, well-proven manufacturing protocols, and retailer acceptance of diet sub-brands. Sports nutrition powders, energy drinks, and sparkling waters all rely on high-intensity sweeteners to balance flavor and calorie constraints. However, pharmaceutical and nutraceutical applications are poised for a 6.18% CAGR, propelled by the need to mask active-compound bitterness in pediatric syrups and chewable tablets. Heat-resistant sucralose and advantame enable zero-sugar medicaments that comply with diabetic-friendly guidelines, while ensuring product stability during global cold-chain disruptions.

The bakery and confectionery sectors are also witnessing steady growth as companies reformulate traditional products to meet consumer demand for healthier indulgences. Popular items like cookies, cakes, and fillings are now being produced with innovative blend systems that combine polydextrose with high-potency sweeteners. These formulations help achieve sugar-reduction goals without compromising texture or taste. Ingredient suppliers offering comprehensive solutions are gaining a competitive edge, as manufacturers prefer working with single-source providers to ensure functionality, sensory appeal, and regulatory compliance. This trend highlights the growing importance of partnerships between ingredient developers and food manufacturers in meeting evolving consumer preferences.

Geography Analysis

Asia-Pacific dominated the global artificial sweetener market in 2025, accounting for 31.78% of the total volume. This growth is driven by the expansion of beverage manufacturing facilities and increasing health awareness in countries like China, India, and Japan. In India, proposed front-of-pack labeling norms are encouraging companies to reformulate their products to meet upcoming regulatory requirements. Meanwhile, China benefits from its domestic stevia cultivation and advancements in precision fermentation, which help reduce lead times for manufacturers. Additionally, rising middle-class incomes and urbanization are boosting the demand for sugar-free snacks, energy drinks, and diabetic-friendly food products, creating a strong foundation for the market in this region.

The Middle East and Africa are experiencing the fastest growth, with a projected CAGR of 6.07%. Governments in the Gulf Cooperation Council (GCC) are implementing nutrition strategies to reduce sugar consumption, leading to reforms in school canteens and public-sector procurement policies favoring low-calorie alternatives. Investments in food-processing parks in Saudi Arabia and the UAE are supporting local production, reducing dependency on imports, and improving supply chain efficiency. Furthermore, the region faces a high prevalence of diabetes, with nearly 1 in 5 adults affected in some Gulf states. This alarming statistic is driving institutional efforts to promote sugar-substitution programs and healthier dietary options.

North America and Europe remain critical markets for artificial sweeteners, despite slower volumetric growth. In the United States, consumer trust in FDA regulations supports steady adoption, while companies continue to reformulate products to avoid litigation risks. In Europe, the demand for clean-label products is pushing manufacturers to develop hybrid sweetener systems that combine botanical extracts with small amounts of sucralose to meet both taste and regulatory standards. Additionally, both regions are focusing on reshoring ingredient production to mitigate geopolitical risks. For instance, specialty chemical companies are setting up fermentation facilities in the U.S. Midwest and Western Europe, reducing reliance on Asian imports and ensuring timely supply for major beverage manufacturers.

Regulatory Landscape

Regulation of artificial sweeteners continues to be shaped by periodic safety re-evaluations, updated impurity specifications, and differences in approval pathways across regions. In the European Union, EFSA actions have been especially influential. In 2025, EFSA completed its re-evaluation of acesulfame K (E 950) and revised the ADI to 15 mg/kg bw/day, alongside recommendations to update specifications for impurities (including 5-chloro-acesulfame and acetylacetamide). In February 2026, EFSA concluded that sucralose (E 955) remains safe for currently authorized uses with an ADI of 15 mg/kg bw/day, but it could not confirm safety for certain proposed use extensions in fine bakery wares due to concerns around high-temperature processing byproducts.

Regulators are also enabling newer production methods for sweetener molecules, which changes how suppliers position fermentation- and enzyme-enabled offerings alongside legacy synthetic sweeteners. EFSA issued a January 2026 opinion finding no safety concerns for a modified manufacturing process for enzymatically produced steviol glycosides (E 960c) using additional genetically modified production strains. In the United States, the FDA GRAS pathway continues to support commercialization of high-purity sweetener ingredients made via novel processes. In April 2026, FDA closed GRAS Notice GRN 1294 for rebaudioside M produced using enzymatic treatment, issuing a no-questions letter for use as a general-purpose sweetener (excluding infant formula).

Value Chain Analysis

The value chain covers feedstocks and intermediates (petrochemical and fine-chemical inputs for synthetic routes, plant-based inputs for steviol glycosides and monk fruit, and fermentation media and enzymes for bio-based routes), manufacturing (chemical synthesis, extraction/purification, and increasingly precision fermentation/bioconversion), and downstream formulation into powders and liquids for beverages, bakery, dairy, confectionery, and pharmaceutical customers. Large ingredient suppliers such as Cargill, ADM, Ingredion, Roquette, and Tate & Lyle compete with specialists by pairing production with application labs, regulatory support, and blending capabilities, since many buyers procure systems (sweetener plus masking, bulking, and texture components) rather than a single molecule.

Recent investments and alliances show how supply is being diversified across geographies and technologies, affecting lead times, cost structures, and risk management. In February 2026, Tate & Lyle and Manus launched the Yume brand under their Sweetener Alliance, including Yume M Stevia Sweetener produced at the Manus Augusta BioFacility in Georgia. Manus also disclosed commercial-scale US production of fermentation-made monk fruit sweetener at the same site in June 2026, reducing reliance on crop-dependent sourcing. In Europe, Pentasweet began construction of a 65 million euro brazzein production facility in Lithuania in April 2026, signaling a move toward scalable sweet-protein supply. Separately, Amai Proteins secured FDA GRAS status for its sweet protein sweelin in February 2026 and Singapore Food Agency approval in May 2026, underscoring how multi-jurisdiction clearances function as a gating step before broader food and beverage formulation wins.

Competitive Landscape

The artificial sweetener market is moderately concentrated, with major players like Cargill, Incorporated, Archer Daniels Midland Company, Ingredion Inc., and Roquette Frères dominating through their vertically integrated supply chains and extensive product portfolios. These companies leverage their global application labs, regulatory expertise, and logistics networks to maintain a competitive edge. However, as the market matures, even these leaders are seeking ways to differentiate themselves. For instance, Ingredion’s expansion of its PureCircle unit in Malaysia in 2025 highlights its strategic focus on natural sweeteners while continuing to offer conventional options. This approach allows them to cater to evolving consumer preferences while staying competitive.

Mid-sized companies are carving out their niche by focusing on regional markets and offering tailored solutions. These firms often build strong relationships with local bottlers and emphasize agility in customization to meet specific client needs. Start-ups in the space are also gaining traction, particularly those working on innovative technologies like precision-fermented rare sugars or enzymatic conversion processes. These advancements attract venture capital and licensing deals, especially when they promise faster production times or unique taste profiles. Collaborations between sweetener innovators and major flavor houses are further accelerating product development, enabling quicker market entry for new offerings.

Sustainability is becoming a key focus area for competition in the artificial sweetener market. Companies are increasingly highlighting the environmental benefits of their products, such as the reduced carbon footprint of fermentation-derived sweeteners compared to traditional extraction methods. These sustainability metrics are often used to appeal to retailers that prioritize eco-friendly procurement practices. Partnerships between ingredient suppliers and biopolymer packaging firms are emerging, showcasing a commitment to holistic solutions that go beyond just the sweetener itself. This integrated approach not only addresses consumer demand for sustainability but also strengthens the overall value proposition for businesses in the market.

Artificial Sweetener Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Ingredion Inc.

-

Roquette Frères

-

Tate & Lyle PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Formulation demand is splitting into two opportunity lanes: (1) reformulation where approved high-intensity sweeteners remain central for sugar and calorie reduction targets, and (2) reformulation where brands remove artificial sweeteners to support clean-label positioning, shifting mix toward botanicals, fermentation-derived sweeteners, and sweet proteins. In 2026, major brand actions reinforced the second lane across mainstream categories, including PepsiCo's complete reformulation of Muscle Milk protein shakes to exclude artificial sweeteners (May 2026) and Kraft Heinz's launch of Jell-O Simply without artificial sweeteners (May 2026). These changes create space for suppliers that can combine sweetness with taste modulation and texture solutions that work in high-protein and dessert applications while aligning with simplified label goals.

On the supply side, new bio-manufacturing capacity and alliances are expanding the set of practical ingredients for sugar reduction beyond traditional artificial sweeteners. Manus began commercial-scale US production of a fermentation-based monk fruit sweetener at its Augusta, Georgia, facility in June 2026, and Pentasweet started construction of a 65 million euro brazzein facility in Lithuania in April 2026. Together, these initiatives improve industrial-scale access to ingredients that were previously constrained by agricultural supply chains. For incumbent artificial sweetener suppliers, the most actionable opportunity is increasingly tied to integrated systems (sweetener plus bulking, masking, and process stability), especially for beverages and baked goods where taste, browning, and mouthfeel constraints drive repeat purchasing and long-term supply agreements.

Recent Industry Developments

- June 2026: ADM introduced SweetRight Stevia Echo, a bioconversion-produced stevia sweetener positioned for deeper sugar replacement with fewer off-notes and lingering taste. The launch points to a shift from commodity sweeteners toward engineered glycoside profiles and application-ready solutions that help beverage and food manufacturers reformulate at scale.

- February 2025: Ingredion announced a partnership with Oobli to accelerate development of sweet-protein and stevia-based sweetener systems. The collaboration broadened Ingredion's toolkit beyond traditional high-intensity options, supporting multi-ingredient systems that address sweetness, taste masking, and label preferences in beverages and other applications.

- June 2024: United Kingdom food safety authorities granted expedited approval for Ingredion PureCircle steviol glycosides produced via bioconversion. This approval expanded the regulatory footprint for bioconversion-derived stevia ingredients, improving commercialization pathways for higher-purity glycoside solutions used in sugar-reduced formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the artificial sweeteners market covers the value generated from the sale of high intensity, low calorie sweetening ingredients used to replace sugar in food, beverage, and related end uses, across all major regions.

Scope exclusions: We exclude regular sugars and sweetening ingredients that are not classed as artificial sweeteners, and we do not count finished packaged products where the sweetener value cannot be separately identified.

Segmentation Overview

-

By Type

- Acesulfame K

- Advantame

- Saccharin

- Sucralose

- Neotame

- Aspartame

- Others

-

By Form

- Powder

- Liquid

-

By Application

- Bakery and Confectionary

- Dairy and Frozen Desserts

- Beverage

- Pharmaceutical

- Neutraceuticals

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping demand and supply signals that are visible in public data, then aligning them to how artificial sweeteners are regulated and sold. We rely on sources such as the US FDA and the European Food Safety Authority for permitted sweetener lists and use limits, and we use government trade statistics portals to read import and export patterns for key sweetener categories.

To ground the demand pool, we also reference data from bodies such as the World Health Organization, the US Department of Agriculture, and the Food and Agriculture Organization, plus peer reviewed nutrition and food science journals that discuss usage trends and reformulation. Company annual reports, investor presentations, and industry association websites help validate capacity moves, while reputed press coverage supports pricing commentary. We also use a paid subscription for company financials and a patent database selectively to cross check product activity and innovation. These examples are not exhaustive, and many other public and paid sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with sweetener manufacturers, ingredient distributors, food and beverage formulators, and a few regulatory and technical experts, so assumptions behind volume, pricing, and substitution trends could be stress tested. Because this is a global market, we balanced views across APAC, EMEA, and the Americas to reflect different labeling rules, beverage mixes, and reformulation timelines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 32% | EMEA: 29% |

| Smaller Players: 19% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top down model where food and beverage production, reformulation intensity, and trade flows are used to reconstruct the demand pool for artificial sweetener ingredients, then translated into value using observed pricing bands. After forming that total, we cross check it with selective bottom up approximations, including supplier revenue cues, sampled volume by application, and channel feedback on average selling prices. We adjust the output when gaps are repeatedly flagged by these independent checks.

Inputs that matter in this market include high intensity sweetener penetration in beverages, changes in sugar reduction labeling and taxation signals, shifts between powder and liquid forms, application level usage rates in bakery and dairy, and relative pricing changes between major molecules (which often drives substitution). For forecasting, we use scenario analysis supported by primary expert views, since regulatory moves and reformulation cycles can create step changes that a straight line trend misses. Where data is thin in smaller countries, we proxy volumes using consumption and manufacturing indicators, then scale using trade and regional mix checks.

Data Validation & Update Cycle

Model outputs are validated through consistency checks across independent signals, including whether implied sweetener demand matches known application growth and whether price movements align with raw material and supply commentary. Outliers are reviewed in a second pass, followed by a senior analyst review that focuses on assumptions most sensitive to the final value. If variances remain unexplained, we re contact sources to resolve the drivers.

The report is refreshed annually, and interim updates are made when material events occur, including regulatory approvals, major capacity additions, or sudden cost shifts. Before delivery, we do a final data pass so clients receive the latest updated view tied to the same repeatable calculation steps.

Mordor Intelligence's Artificial Sweeteners Market Sizing Compared With Other Published Estimates

Published market sizes can differ even when the topic appears to match closely, because studies often count different sweetener families, choose different base years, or mix ingredient sales with finished product value. Differences also show up when one publisher uses longer forecast windows and others keep a shorter cycle, which can shift the implied near term number.

The key drivers in this market are usually scope boundaries (whether sugar alcohols or broader sugar substitutes are included), the way application demand is converted into ingredient volumes, and how average selling prices are updated during periods of cost volatility and reformulation. Currency timing and how each study treats regional trade and re exports also matter, particularly when APAC volumes are large and product mixes vary by country.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.28 B (2026) | |

| Industry Publisher A | USD 7.20 B (2024) | Uses an earlier base year and a narrower type list on the page, but it can still land higher when price assumptions and segment mapping are not reconciled back to ingredient level demand by application. |

| Global Publisher B | USD 9.30 B (2026) | Includes sugar alcohols and a broader definition of artificial sweeteners, which expands the counted volume beyond high intensity ingredient sales used in many market models. |

The table shows a wide spread. In Mordor Intelligence's model, the total is limited to high intensity artificial sweetener ingredients sold into applications, with adjacent sugar alcohol value kept out to avoid mixing scopes. With a clear inclusion rule like this, we can tie year to year movement to a limited set of drivers such as beverage penetration, pricing bands, and form mix, then explain changes in a way that can be rechecked.

Key Questions Answered in the Report

What is the current size of the artificial sweetener market?

The artificial sweetener market size is USD 4.28 billion in 2026 and is projected to reach USD 5.38 billion by 2031.

Which sweetener type holds the largest market share?

Sucralose leads with 32.41% market share due to its broad regulatory acceptance and heat stability.

Why are liquid sweeteners gaining momentum?

Middle East and Africa is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region offers the highest growth prospects?

The Middle East and Africa shows the fastest 6.07% CAGR, supported by diabetes-prevention policies and expanding food-processing capacity.

Page last updated on: