Polymer Processing Aid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

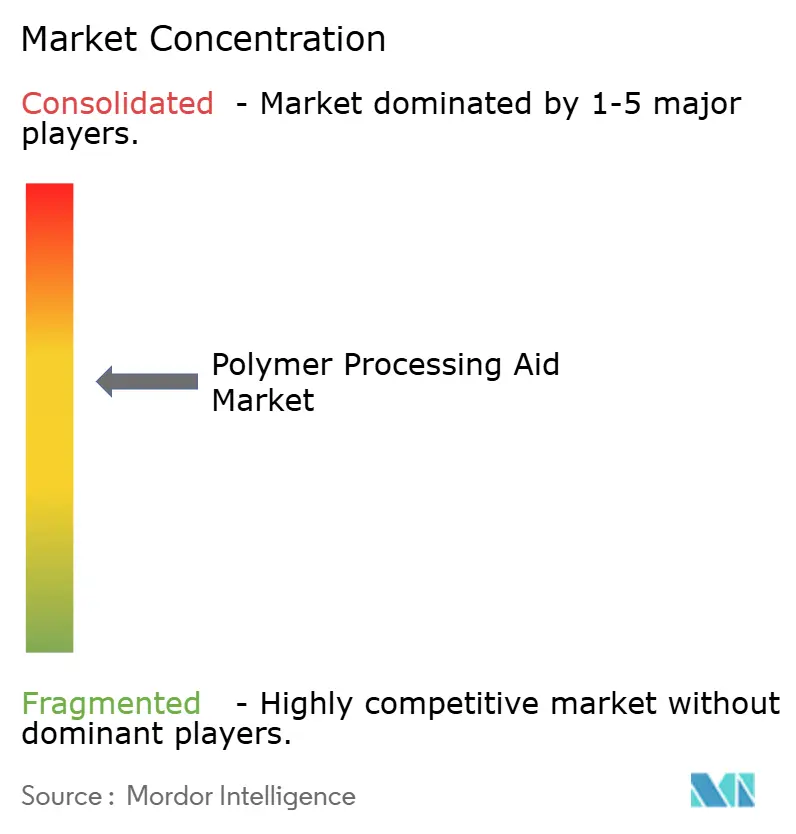

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polymer Processing Aid Market Analysis by Mordor Intelligence

The Polymer Processing Aid Market size was valued at USD 1.94 billion in 2025 and is estimated to grow from USD 2.02 billion in 2026 to reach USD 2.54 billion by 2031, at a CAGR of 4.69% during the forecast period (2026-2031). Multiple forces underpin this trajectory. Major polyolefin producers are relocating capacity from Europe and North-East Asia toward integrated cracker complexes in the Middle East and Southeast Asia, lowering feedstock costs and raising downstream demand for high-shear-stable processing aids. At the same time, regulatory deadlines in the European Union and the United States compel resin makers to qualify non-PFAS chemistries, lifting average selling prices by 15-25% relative to legacy fluoropolymer-based grades. Flexible packaging converters are the biggest consumers of PPAs, yet melt-spun hygiene nonwovens and raffia tape extrusion are growing faster as e-commerce logistics, medical filtration, and woven sack exports accelerate in Asia-Pacific. Consolidation among upstream polyolefin giants, most prominently the 2026 combination of Borouge and Borealis, creates scale advantages that favor vertically integrated additive suppliers with regional compounding, food-contact dossiers, and recycling-compatibility toolkits.

Key Report Takeaways

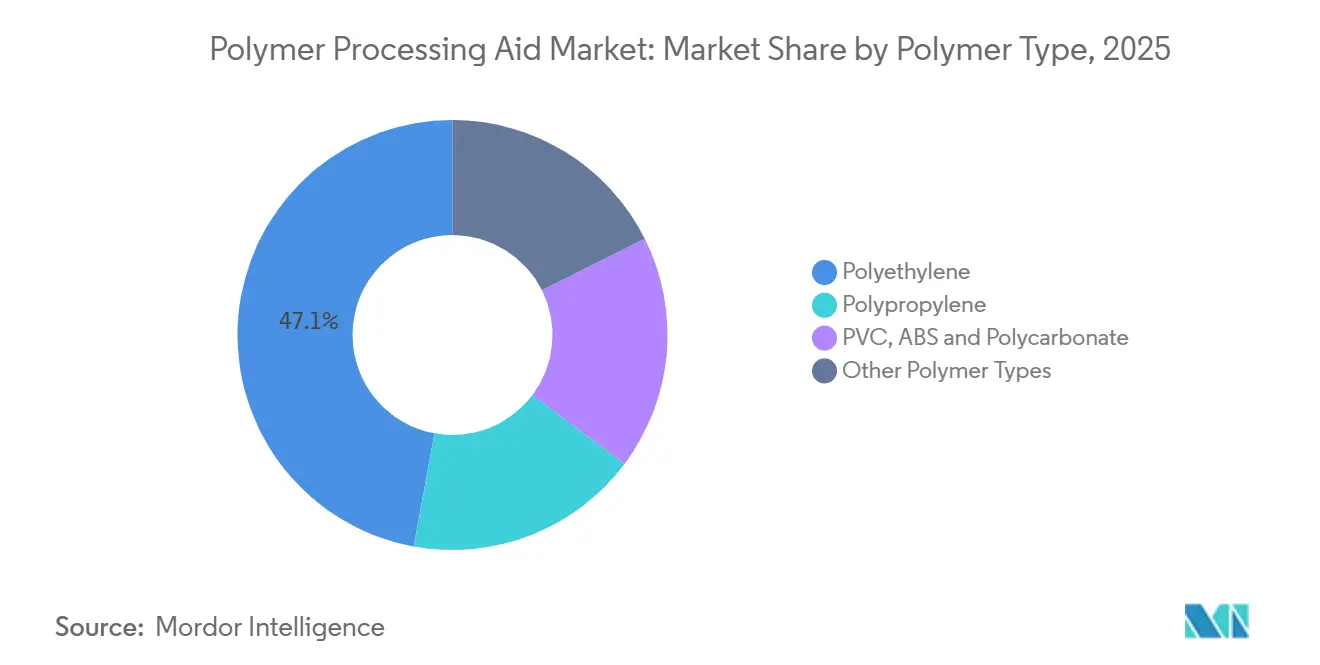

- By polymer type, polyethylene led with a 47.12% share of the Polymer processing aid market in 2025, while polypropylene is forecast to advance at a 4.89% CAGR during the forecast period (2026-2031).

- By application, blown and cast film captured 54.18% revenue in 2025; fibers and raffia are projected to post a 4.78% CAGR during the forecast period (2026-2031).

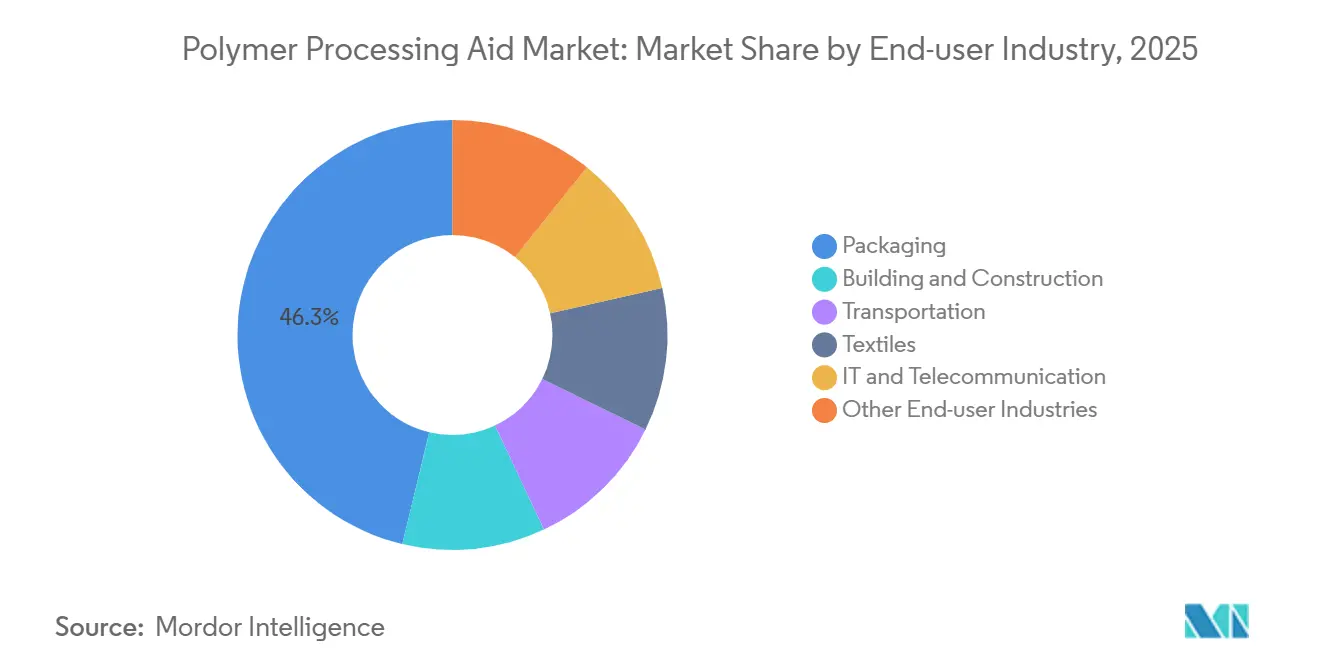

- By end-user industry, packaging dominated with 46.25% of consumption in 2025, whereas transportation is set to expand at a 4.71% CAGR over 2026-2031.

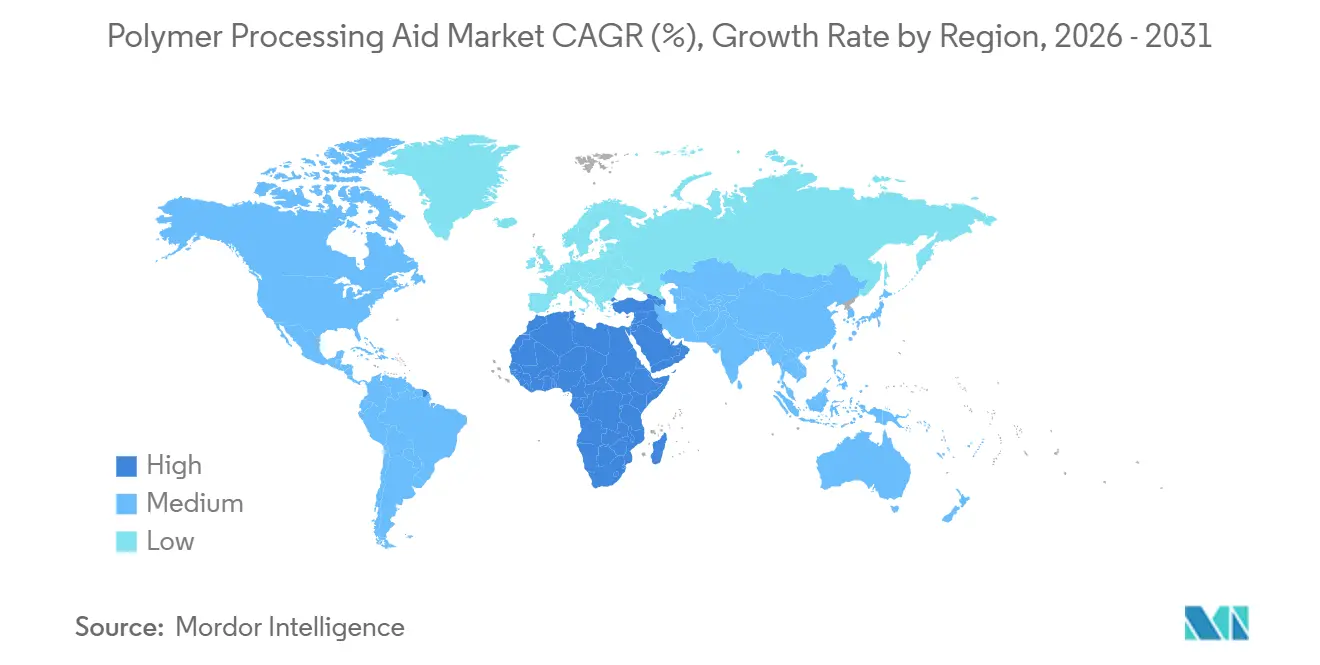

- By geography, Asia-Pacific held 42.05% of global sales in 2025; the Middle East and Africa are expected to record the fastest growth at a 4.73% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polymer Processing Aid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for polypropylene & polyethylene flexible packaging | +1.2% | Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of PVC and HDPE in infrastructure projects | +0.9% | Middle East, North America, South Asia | Long term (≥ 4 years) |

| Boom in APAC plastic converting capacity | +1.1% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Shift to low-/non-PFAS PPAs driven by new regulations | +0.8% | Europe, North America, cascading to export-oriented Asia-Pacific | Short term (≤ 2 years) |

| Surging melt-spun non-woven demand for medical filtration | +0.6% | North America, Europe, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Polypropylene & Polyethylene Flexible Packaging

E-commerce fulfilment and on-the-go consumption are prompting converters to down-gauge films while preserving puncture resistance and clarity. Flexible packaging sales reached USD 45 billion in 2024, and polyethylene films made up 68% of volume thanks to sealability and moisture barrier performance. India-based UFlex commissioned a 36,000 tons per year BOPET (Biaxially-Oriented Polyethylene Terephthalate) line in 2025 that doses PFAS (per- and polyfluoroalkyl substances)-free polymer processing aids (PPAs) to trim film thickness from 12 μm to 9 μm without losing dart-drop strength. Line speeds exceeding 400 m/min generate melt temperatures above 240°C, encouraging the adoption of liquid siloxane aids at 0.1-0.4% to prevent shark-skin defects. Suppliers with ISO 22000-certified food-contact grades enjoy a clear advantage as snack-food brands tighten migration limits.

Growth of PVC and HDPE in Infrastructure Projects

Urbanization programs in the Gulf Cooperation Council and South Asia are expanding water-distribution and conduit networks that rely on rigid polyvinyl chloride (PVC) and high-density polyethylene (HDPE) pipe. Shintech’s USD 3.4 billion Plaquemine expansion will add 625,000 tons per year of ethylene and 500,000 tons per year of VCM by 2030, supplying North American pipe extruders enjoying 7-9% demand growth. TA’ZIZ is building a USD 1.99 billion PVC complex scheduled for 2028 start-up to serve the Middle-East construction. These projects boost demand for acrylic-copolymer PPAs that enhance fusion rates in rigid profiles and comply with potable-water standards such as India’s IS 4985.

Boom in APAC Plastic Converting Capacity

China’s polyethylene capacity hit 34.31 million tons per year in 2024 and will exceed 39 million t/y by end-2026, while polypropylene climbs past 55 million tons per year as coal-to-olefin lines start in Ningxia and Shandong. Converters face squeezed spreads. North China Linear Low-Density Polyethylene (LLDPE) margins fell to CNY 428 (USD 59.49) per ton in April 2025, so faster cycle times and lower scrap become critical, boosting PPA uptake. Thailand and Vietnam plan 7 million tons of additional polyolefins and bio-PE by 2030, requiring specialty PPAs compatible with renewable feedstocks.

Shift to Low-/Non-PFAS PPAs Driven by New Regulations

From February 2025, EU REACH Annex XVII restricts PFAS, and the United States Environmental Protection Agency's (EPA) Toxic Substances Control Act (TSCA) reporting must be filed by May 2025. Clariant responded with AddWorks PPA 101 FG and 122 G for direct food contact[1]Clariant AG, “AddWorks PPA 101 FG Launch,” clariant.com. Ampacet released ProVital+ Proflow 1485 in September 2025 for ISO 10993-compliant medical extrusion. Avient introduced Hiformer liquid grades in February 2026 for Asian film lines, reflecting the region’s 61% share of Borouge’s sales. Price premiums are offset by easier regulatory clearance and brand-owner acceptance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and price volatility of fluoropolymer-based PPAs | -0.5% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Stringent PFAS substance regulations limiting formulations | -0.3% | Europe, North America, export-oriented Asia-Pacific | Medium term (2-4 years) |

| Recycling contamination due to residual PPAs in waste streams | -0.2% | Europe, North America, emerging in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost and Price Volatility of Fluoropolymer-Based PPAs

Polytetrafluoroethylene (PTFE)-type aids sold for USD 13,348-13,545 per ton in North America in Q4 2025, up 18% YoY, versus USD 6,018 per ton in Asia-Pacific, where discounts are narrowing as Chinese plants confront energy levies. Each USD 1,000 per ton swing moves converter costs by USD 0.50-2.00 per ton of film or pipe, eroding margins already stuck near 6%. Multi-year supply contracts with price ceilings mitigate exposure but impede quick switching to new PFAS-free grades.

Stringent PFAS Substance Regulations Limiting Formulations

California, Maine, and Minnesota ban intentionally added PFAS in consumer goods starting 2025-2032, forcing nationwide distributors to meet the strictest rule. Demonstrating residual migration below 10 ppb often disqualifies legacy PPAs, and pilot trials for replacements cost USD 0.5-1 million plus 6-12 months, hitting mid-sized converters hardest. Mergers and acquisition is gathering pace as larger players spread compliance budgets across higher volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Polyethylene Dominates, Polypropylene Accelerates

Polyethylene held 47.12% of the Polymer Processing Aid market share in 2025, owing to blown-film leadership; however, polypropylene formulations are forecast to grow at a 4.89% CAGR to 2031, powered by melt-spun non-woven hygiene fabrics. Within polyethylene, LDPE-LLDPE stretch film consumed 38% of additive tonnage, while HDPE pipe and bottle applications represented 62%. Tasnee’s planned 3.3 million tons per year petrochemical expansion will lift HDPE demand in the Gulf and intensify local need for high-melt-strength PPAs[2]Sahm Capital Insights, “Tasnee Petrochemical Expansion,” sahmcapital.com.

Reformulation pressure is higher in polypropylene as raffia-tape lines in India and China insist on PFAS-free grades that keep tensile strength above 250 MPa even with 20-30 % CaCO₃ filler. Outside polyolefins, PVC, ABS, and PC together absorbed 18% of the 2025 volume, but acetylene-route PVC shutdowns in China and higher VCM costs restrict near-term growth. Niche engineering resins such as PA and POM accounted for the remaining 8%, calling for PPAs that retain dimensional stability at more than 120°C.

By Application: Film Extrusion Leads, Fibers Gain Momentum

Blown Film and Cast Film commanded 54.18% of 2025 revenue in the Polymer Processing Aid market. Liquid siloxane PPAs enable cast-PP lines to hit 400 meters per minute without shark skin, meeting printability demands for snack-food laminates. Fibers and raffia are set to expand at a 4.78% CAGR to 2031 as woven sacks, jumbo bags, and geotextiles proliferate across South and Southeast Asia.

The switch to halogen-free flame-retardant sheathing in wire and cable application in Europe promotes polyolefin-rich compounds that need smooth-flow additives. Blow-molded HDPE bottles' market share relies on PPAs to curb parison sag. Pipe and tube market share in 2025 was supported by municipal water upgrades in the Gulf. Injection molding, thermoforming, and rotomolding rounded out the market share with specialized requirements for warpage-free large parts.

By End-user Industry: Packaging Prevails, Transportation Surges

The packaging sector held 46.25% market share in 2025, spanning flexible films, rigid containers, and protective foams, with e-commerce logistics driving demand for puncture-resistant polyethylene mailers and tamper-evident polypropylene pouches. Transportation applications are forecast to expand at 4.71% CAGR through 2031, the fastest among end-user segments, as automakers substitute steel and aluminum with fiber-reinforced thermoplastics to achieve 10-15% mass reduction in body panels, battery enclosures, and underbody shields. SABIC introduced LNP Elcrin compounds incorporating 30-45% post-consumer recycled content and thermally conductive grades for electric-vehicle battery modules, formulations that require PPAs to maintain fiber wet-out and prevent void formation during injection molding.

Building and construction end-users' consumption in 2025 was concentrated in PVC window profiles, HDPE corrugated drainage pipe, and polycarbonate glazing panels. The sector's growth is tied to urbanization in the Gulf Cooperation Council, where Borouge is expanding polyolefin capacity to over 6.6 million tonnes per year by 2028. Textiles application's market share was represented by polypropylene spunbond and meltblown fabrics for disposable hygiene products, such as diapers, feminine-care pads, and surgical gowns, requiring PPAs that maintain fiber uniformity and prevent nozzle clogging during high-speed spinning. IT and telecommunication applications, serving fiber-optic cable jacketing and electronics housings, where flame-retardant polycarbonate and ABS compounds demand PPAs compatible with brominated or phosphorus-based additives.

Geography Analysis

Asia-Pacific generated 42.05% of 2025 revenue, underpinned by China’s 34.31 million tons per year PE and 43.69 million tons per year PP capacity and India’s fast-growing film sector. Oversupply trims margins, so converters emphasize cost-effective, low-dose PPAs. Braskem’s Thai bio-ethylene project and UFlex’s new lines illustrate the region’s tilt toward circular and bio-based feedstocks, demanding compatible additives.

The Middle East and Africa is the growth engine, forecast at a 4.73% CAGR to 2031. Borouge, QatarEnergy, and Amiral collectively add more than 4 million tons of HDPE and LLDPE by 2028, linked to ethane crackers that deliver 20-30% lower feed costs than European naphtha plants. The freshly merged Borouge Group International wields 13.6 million tons per year of polyolefins, pressuring suppliers to offer integrated PPA-masterbatch services close to Ruwais and Ruwais Logistics Park.

North America held a substantial market share in 2025, with Shintech’s Plaquemine and LyondellBasell’s CirculenRenew lines pulling through demand for mass-balance-certified PPAs. Europe's market share is hampered by 5.4 million tons of capacity closures since 2022 and energy costs 3-4× Gulf rates. Investments have shifted to niche circular projects like Borealis’s high-melt-strength PP line for 50% PCR inclusion, a specification that strains conventional additives. South America accounted for a smaller market share, with Braskem’s Brazilian upgrades requiring PPAs that tolerate tropical ambient temperatures and elevated melt temps.

Competitive Landscape

The Polymer Processing Aid market is moderately consolidated. Patent activity around constrained-geometry catalysts and hyperbranched polyolefin elastomers aims to embed melt-fracture resistance directly into the polymer, a potential long-term threat to standalone additive demand. Meanwhile, Borouge Group International’s 13.6 million tons per year scale will tilt procurement toward suppliers that can anchor labs in Abu Dhabi or Vienna and commit to research and development on recyclability-compatible chemistries.

Polymer Processing Aid Industry Leaders

Arkema

Dow

DAIKIN INDUSTRIES, Ltd.

Clariant

The Chemours Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Avient Corporation expanded its Hiformer Non-PFAS Process Aid portfolio into the Asian market. The expansion introduces two new liquid grades tailored for polyolefin film applications. These formulations now feature both siloxane-based and non-siloxane-based non-PFAS liquid process aids

- October 2025: Cargill, Incorporated, unveiled its latest innovation, the Incroflo P50 additive. This polymer processing aid (PPA) is tailored for polyolefins. This advancement significantly boosts polymer melt flow and extrudability, all while steering clear of intentionally added halogens in the plastics manufacturing process.

Global Polymer Processing Aid Market Report Scope

Polymer Processing Aids (PPAs) are additives added to the base polymer to improve the material's processability, processing properties, and the end product's quality.

The Polymer Processing Aid market is segmented based on polymer type, application, end-user industry, and geography. The market is segmented by polymer type into polyethylene, polypropylene, PVC, ABS, polycarbonate, and other polymer types. The market is segmented by application into blown film and cast film, wire and cable, extrusion blow molding, fibers and raffia, pipe and tube, and other applications. By end-user industry, the market is segmented into packaging, building and construction, transportation, textiles, IT and telecommunication, and other end-user industries. The report also covers the size and forecasts for the Polymer Processing Aid market in 16 countries across major regions. Each segment's market sizing and forecasts are based on value (USD).

| Polyethylene | LLDPE |

| LDPE | |

| HDPE | |

| Polypropylene | |

| PVC, ABS and Polycarbonate | |

| Other Polymer Types |

| Blown Film and Cast Film |

| Wire and Cable |

| Extrusion Blow Molding |

| Fibers and Raffia |

| Pipe and Tube |

| Other Applications |

| Packaging |

| Building and Construction |

| Transportation |

| Textiles |

| IT and Telecommunication |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Polymer Type | Polyethylene | LLDPE |

| LDPE | ||

| HDPE | ||

| Polypropylene | ||

| PVC, ABS and Polycarbonate | ||

| Other Polymer Types | ||

| By Application | Blown Film and Cast Film | |

| Wire and Cable | ||

| Extrusion Blow Molding | ||

| Fibers and Raffia | ||

| Pipe and Tube | ||

| Other Applications | ||

| By End-user Industry | Packaging | |

| Building and Construction | ||

| Transportation | ||

| Textiles | ||

| IT and Telecommunication | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Polymer processing aid market by 2031?

It is expected to reach USD 2.54 billion by 2031, reflecting a 4.69% CAGR over 2026-2031.

Which polymer type will grow fastest in additive demand?

Polypropylene PPAs are forecast to post the highest growth at 4.89% CAGR, driven by non-woven hygiene fabric and raffia tape extrusion.

Why are PFAS-free PPAs attracting a price premium?

EU REACH and U.S. EPA deadlines require non-PFAS formulations; compliant grades command 15-25% higher prices but simplify regulatory approval.

Which region offers the best growth outlook for suppliers?

The Middle East and Africa is set to expand at a 4.73% CAGR through 2031, powered by new ethane-based polyolefin complexes.

Page last updated on: