Aramids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

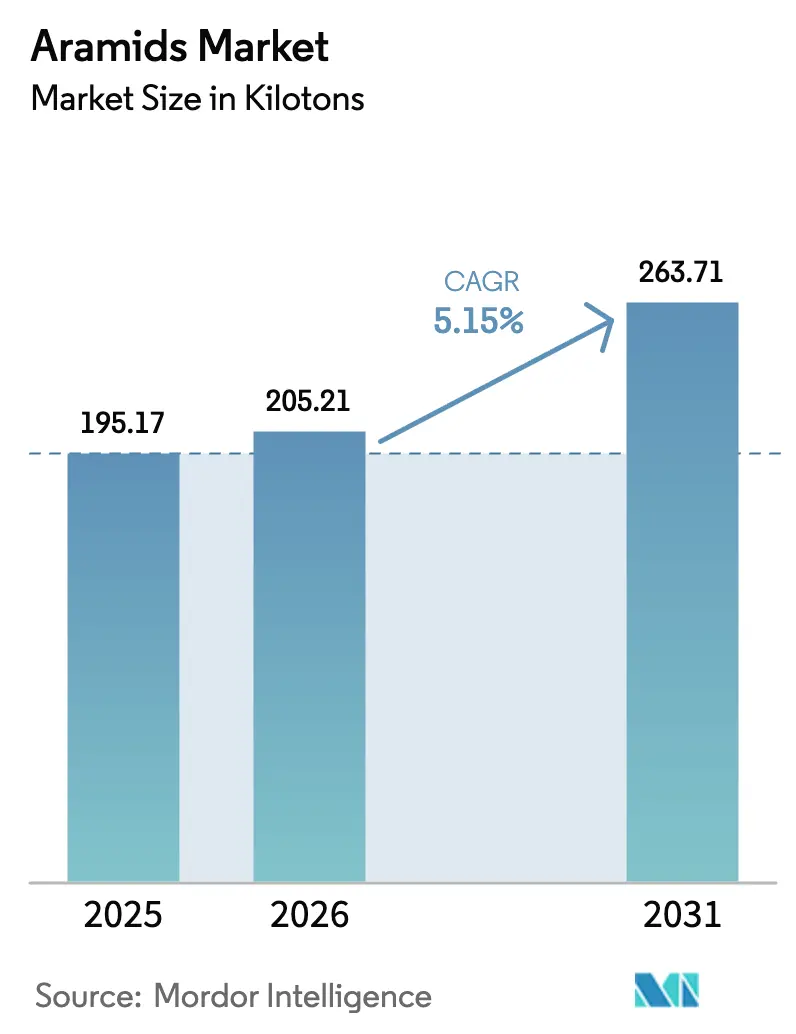

| Market Volume (2026) | 205.21 kilotons |

| Market Volume (2031) | 263.71 kilotons |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aramids Market Analysis by Mordor Intelligence

The Aramids Market size was valued at 195.17 kilotons in 2025 and estimated to grow from 205.21 kilotons in 2026 to reach 263.71 kilotons by 2031, at a CAGR of 5.15% during the forecast period (2026-2031). Demand continues to accelerate because aramid fibers combine high tensile strength, low weight, and thermal stability in ways that conventional steel, nylon, or glass fibers cannot match. Growth-critical use cases span automotive lightweighting, next-generation 5G optical-fiber infrastructure, and defense programs that require durable ballistic protection. Supply chain localization in Asia-Pacific, precursor self-sufficiency in China, and sustained capital spending by leading producers such as Toray and Kolon are further amplifying production capacity. Meanwhile, Middle East & Africa is turning infrastructure modernization into the fastest regional growth pocket, and global regulatory momentum around flame-resistant personal protective equipment (PPE) is creating non-discretionary demand that shields the Aramids market from cyclical downturns.

Key Report Takeaways

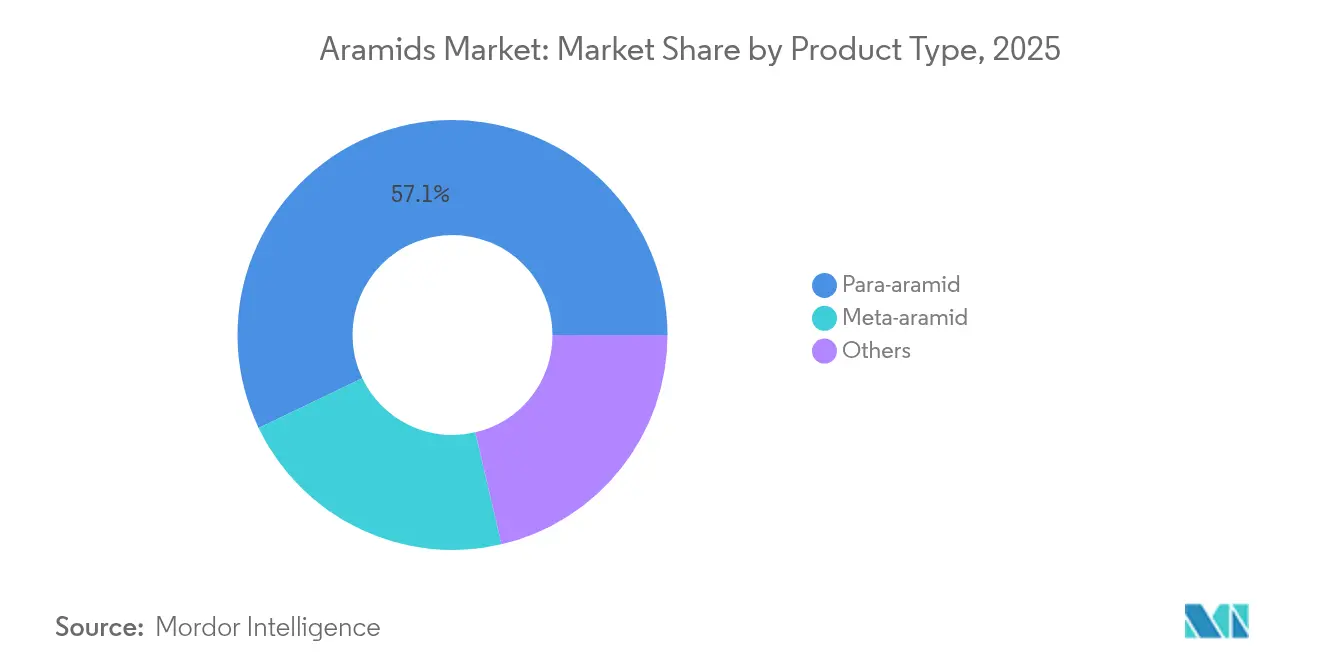

- By product type, Para-aramid led with a 57.11% share of the Aramids market and meta-aramid posted the highest 6.9% CAGR between 2026 and 2031.

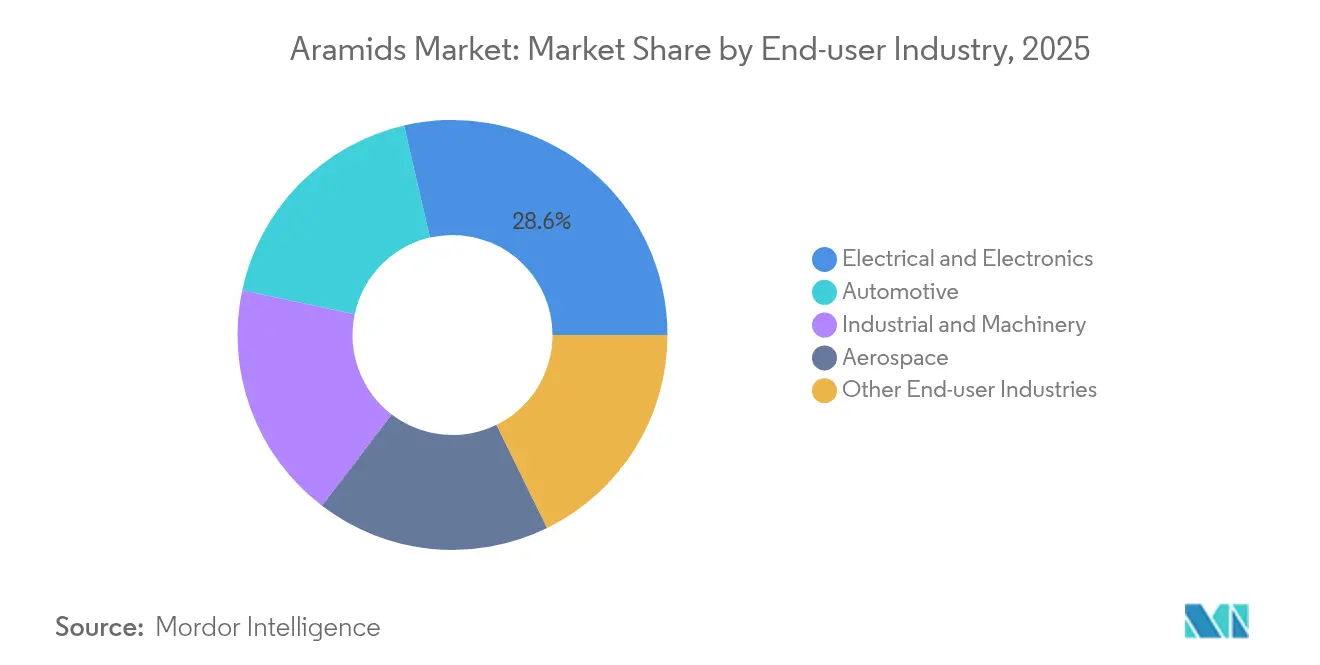

- By end-user industry, the Electrical & Electronics sector captured 28.62% of the Aramids market share in 2025 and is expected to expand at a 7.1% CAGR through 2031.

- By geography, Asia-Pacific dominated with 50.92% of Aramids market share in 2025, while the Middle East & Africa is advancing at a 6.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aramids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting in automotive & aerospace | +1.8% | Global; strongest in Asia-Pacific and Europe | Medium term (2-4 years) |

| Mandatory PPE regulations worldwide | +1.2% | Global; strictest in North America and the EU | Short term (≤ 2 years) |

| Expansion of 5G/FTTx optical-fiber networks | +1.0% | Asia-Pacific core, spillover to North America & Europe | Medium term (2-4 years) |

| Defense budgets boosting ballistic protection | +0.8% | North America, Europe, Middle East & Africa | Long term (≥ 4 years) |

| EV battery-grade aramid separators | +0.7% | Global; early gains in China, Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lightweighting in automotive & aerospace

Automakers and aircraft original equipment manufacturers (OEMs) are embracing aramid reinforcement to reduce weight without compromising durability or safety. Tire makers rely on para-aramid cords that weigh 40% less than steel yet deliver comparable strength, directly improving fuel efficiency or extending electric-vehicle range[1]Toray Advanced Materials, “Gumi Plant Expansion Release,” toray.co.jp. Aerospace users integrate aramid honeycomb cores and prepregs to meet stringent Federal Aviation Administration cabin safety standards while reducing structural mass. Toray’s USD 100 million meta-aramid expansion in Gumi was explicitly justified by surging demand for lightweight vehicle components scheduled to reach assembly lines by late 2025. As governments tighten carbon-emission limits, aramid-based components are moving from niche to baseline specifications, reinforcing the growth trajectory of the aramid market.

Mandatory PPE regulations worldwide

Fire-resistant protective clothing, once considered optional, is rapidly transitioning to a mandated status in the oil & gas, utilities, chemicals, and heavy-metal processing industries. The European Union’s EN ISO 11612:2015 and EN ISO 11611:2015 standards list aramid fibers as benchmark flame-retardant substrates, pushing employers toward inherent-FR fabrics that perform for the entire garment life cycle. The US Occupational Safety and Health Administration references NFPA 2112 and 70E, both of which accept meta-aramid blends as compliant with respect to flash-fire and arc-flash hazards. Because safety non-compliance can halt production and result in fines, corporations are locking in multi-year supply contracts, providing volume stability for leading fiber producers.

Expansion of 5G/FTTx optical-fiber networks

Each 5G small cell requires multiple fiber links, and installers specify aramid yarns as central strength members to protect fragile glass fibers against tension and bending. Teijin’s Twaron reinforcement can handle tensile loads exceeding 3,500 MPa, preventing micro-bends that degrade signal integrity. As Asia’s operators aim to connect 1 billion 5G subscribers by 2027, kilometer-long cables with embedded aramid yarns form a repeat-purchase consumable. Participation by fiber majors and polymer partners in the Sustainable Optical Fiber & Cable Industry Alliance (SOFIA) underscores that the Aramids market is pivotal to resilient telecom infrastructure.

Defense budgets boosting ballistic protection

Para-aramid vests and helmet inserts stop high-velocity rounds with lower back-face deformation than UHMWPE under multi-hit conditions, driving procurement preferences by NATO (North Atlantic Treaty Organization) members and emerging defense forces. The US National Defense Authorization Act appropriations channelled over USD 500 million toward soldier survivability kits in FY 2025, resulting in blanket purchase agreements with aramid fabric integrators[2]U.S. Congress, “FY 2025 NDAA Appropriations,” congress.gov. Middle East modernization and Eastern European rearmament are adding incremental demand as states replace aging steel plates with lighter aramid composites. This strategic imperative elevates para-aramid volumes independently of macro-economic cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and raw-material costs | -1.5% | Global; highest in price-sensitive regions | Short term (≤ 2 years) |

| Competition from UHMWPE and carbon fiber | -0.9% | Global; acute in performance-critical applications | Medium term (2-4 years) |

| Environmental and end-of-life concerns | -0.6% | Primarily Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High production and raw-material costs

Aramid polymerization relies on aromatic diamines and diacid chlorides derived from petrochemicals, whose prices fluctuate with the crude oil market. Energy-intensive spinning under concentrated sulfuric acid further increases unit costs by up to 30% compared to nylon or polyester. Aekyung Chemical’s USD 73 million precursor plant investment in Ulsan aims to alleviate input bottlenecks; however, price volatility persists because para-xylene feedstocks remain globally traded commodities. High capital intensity discourages new entrants and can delay upgrades when cash flows tighten, constraining capacity additions in the Aramids market.

Competition from UHMWPE and carbon fiber

UHMWPE (ultra-high-molecular-weight polyethylene) offers lower density and competitive ballistic performance for soft armor, while carbon fiber delivers higher modulus for aerospace structures. Xingyu Chengyang’s 6,000 tpa UHMWPE line, launching in 2025, will undercut para-aramid by 15-20% in certain cut-protection applications. Carbon fiber pricing declined 8% between 2023 and 2024 due to a surplus of tow capacity in China, prompting composite fabricators to substitute carbon in sporting goods and high-performance automotive panels. These incursions cap premium pricing power across the Aramids market even as niche demand remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Para-aramid dominance faces meta-aramid growth

Para-aramid retained 57.11% of the Aramids market share in 2025, owing to its unrivaled tensile performance of 3,000 MPa and heat resistance exceeding 500 °C. The Aramids market size for para-aramid is projected to grow at a 4.8% CAGR, driven by contracts for ballistic protection and tire reinforcement. End-use reliability requirements tighten vendor qualification cycles, so incumbents such as Teijin and DuPont benefit from high switching costs that protect their market share.

Meta-aramid is on track for the fastest 6.9% CAGR as electrical insulation and inherently flame-retardant garments proliferate within data-center construction, renewable power cabling, and industrial safety programs. Electrical utilities specify meta-aramid papers in high-voltage transformer windings to extend service life to 40 years. Fire-fighter turnout gear blends add moisture barriers without sacrificing breathability, helping manufacturers meet NFPA 1971 2025 edition upgrades. Although absolute tonnage trails para-aramid, sustained double-digit volume growth will lift meta-aramid’s revenue share to 31.40% of the Aramids market size by 2031.

By End User Industry: Electronics sector drives dual leadership

Electrical & Electronics seized 28.62% of the Aramids market share in 2025, propelled by 5G fiber-optic roll-outs and battery separator coatings. The segment is forecasted to grow at a 7.1% CAGR, adding nearly 18 kilotons of incremental demand by 2031. Each kilometer of loose-tube fiber absorbs 45-50 grams of aramid yarns, and Chinese telecom projects alone laid 6.2 million route kilometers in 2024.

Automotive follows as the second-largest consumer, primarily for tire cord, brake pads, and transmission belts that exploit aramid’s elastic modulus stability up to 250 °C. Lightweight EV platforms increase demand for aramid in battery casings and structural composites, but the overall CAGR is tempered to 4.45% due to internal-combustion vehicle volumes plateauing. Industrial & Machinery applications span conveyor belts, high-pressure hoses, and chemically aggressive pump diaphragms that mandate aramid reinforcement. Aerospace remains a smaller tonnage consumer yet commands high value per kilogram due to stringent certification costs, keeping margins above the Aramids industry average.

Geography Analysis

The Asia-Pacific region held a 50.92% market share of the Aramid market in 2025, thanks to its integrated supply chains, which span from benzene derivatives to finished fiber. China accounts for about 70% of global m-phenylenediamine and p-phenylenediamine output, insulating regional producers from external feedstock shocks. Kolon Industries’ 298.9 billion-won capacity doubling in Jeonju lifted South Korea’s aramid output beyond 15,000 tpa in 2024, positioning the country as a tire-cord export hub.

North America commands entrenched defense and aerospace channels, with DuPont’s Kevlar brand being specified in the US Department of Defense's ballistic standards. DuPont’s Water & Protection segment booked USD 5.6 billion in sales in 2023, even as channel inventory corrections shaved 7% volume, highlighting structural demand resilience. European demand concentrates in Germany, France, and the Netherlands, where strict EN ISO PPE mandates lock in meta-aramid garment purchases.

The Middle East & Africa is the fastest-growing region, with a 6.8% CAGR to 2031, as defense procurement and the petroleum sector's PPE converge. Saudi Arabia’s National Industrial Development Program includes optical-fiber backbone expansions that embed aramid yarns, while United Arab Emirates armed forces are upgrading body armor to para-aramid composites. Latin America remains a modest consumer, but Brazilian OEMs have started substituting aramid for asbestos in friction materials to meet forthcoming health regulations, signaling latent upside.

Competitive Landscape

The Aramids market is concentrated. Rising competition from vertically integrated Chinese newcomers such as Shenma Industrial and X-Fiper is compressing average selling prices by 3-4% annually in commodity grades. Strategic responses focus on de-bottlenecking and specialty product streams. DuPont earmarked more than USD 500 million for Kevlar expansion in South Carolina, explicitly targeting higher-margin aerospace and space exploration applications. Future competition will center on process intensification and application engineering rather than volume acquisitions.

Aramids Industry Leaders

TEIJIN LIMITED

HS HYOSUNG ADVANCED MATERIALS

Kolon Industries, Inc.

Yantai Tayho Advanced Materials Co., Ltd.

Arclin

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: In a move valued at around USD 1.8 billion, DuPont's Aramid business, known for its Kevlar and Nomex brands, was acquired by Arclin. Arclin is a portfolio company affiliated with TJC, L.P., and the agreement reached is definitive.

- April 2025: Teijin Limited initiated the integration of Digital Product Passport (DPP) technology with its aramid and carbon fibers. This move bolsters supply chain transparency, enabling the verification of material origins and reinforcing sustainability claims.

Global Aramids Market Report Scope

Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery are covered as segments by End User Industry. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.| Para-aramid |

| Meta-aramid |

| Others |

| Automotive |

| Electrical and Electronics |

| Industrial and Machinery |

| Aerospace |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| Italy | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Para-aramid | |

| Meta-aramid | ||

| Others | ||

| By End User Industry | Automotive | |

| Electrical and Electronics | ||

| Industrial and Machinery | ||

| Aerospace | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Market Definition

- End-user Industry - Automotive, Electrical & Electronics, Industrial & Machinery, Aerospace, and Others are the end-user industries considered under the aramid market.

- Resin - Under the scope of the study, consumption of virgin aramid resin in the primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms