Specialty Polymers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 157.64 Billion |

| Market Size (2031) | USD 170.91 Billion |

| Growth Rate (2026 - 2031) | 1.63% CAGR |

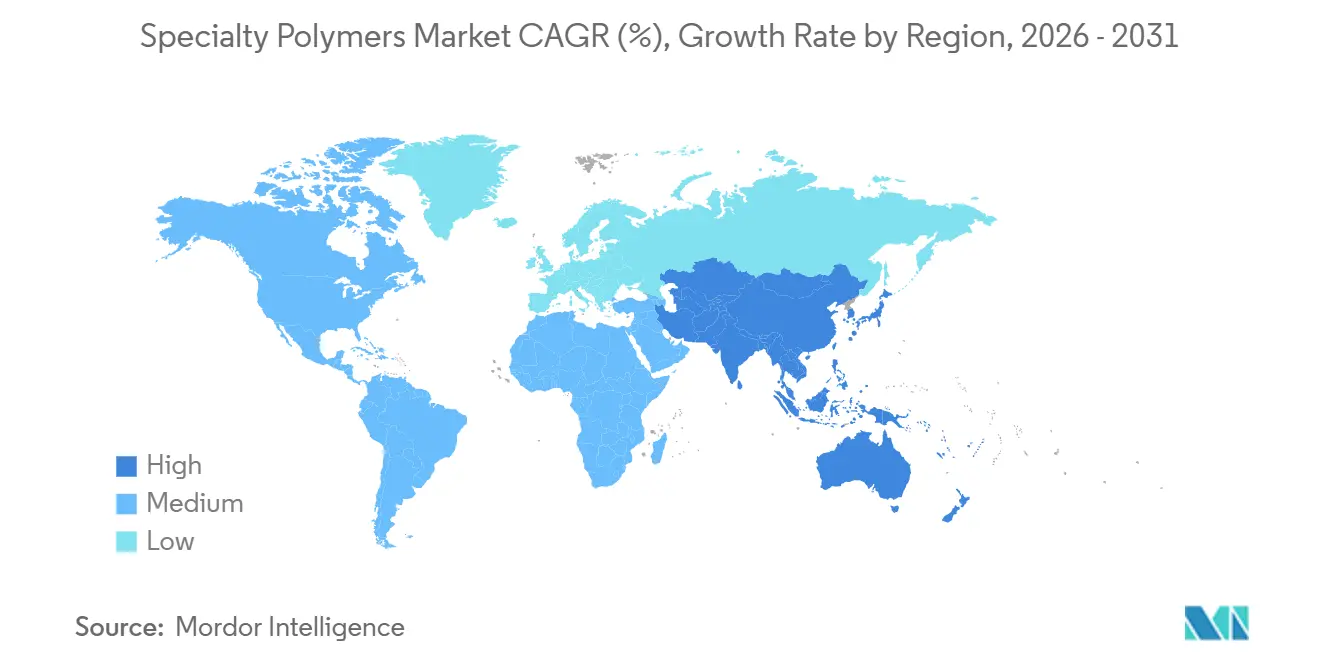

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Polymers Market Analysis by Mordor Intelligence

The Specialty Polymers Market size is expected to increase from USD 155.11 billion in 2025 to USD 157.64 billion in 2026 and reach USD 170.91 billion by 2031, growing at a CAGR of 1.63% over 2026-2031. Demand is uneven across material classes: specialty thermoplastics keep their foothold in automotive under-hood systems and semiconductor tooling, whereas carbon-fiber composites accelerate on the back of next-generation aircraft programs and large-scale offshore wind installations. End-use momentum is likewise split, with automotive commanding the largest revenue base but healthcare registering the quickest expansion as biocompatible grades move deeper into implantables and drug-delivery devices. Asia-Pacific anchors almost one-half of global consumption, buoyed by Chinese electric-vehicle battery growth and Indian pharmaceutical manufacturing upgrades, while North America and Europe pivot toward circular-economy mandates that favor chemical recycling and bio-based feedstocks. Competitive intensity remains high because regional specialists carve out profitable niches even as global majors defend share with capacity additions and R&D spending tied to battery and electronics supply chains.

Key Report Takeaways

- Specialty thermoplastics led with 38.46% revenue share in 2025, while specialty composites are forecast to expand at a 6.28% CAGR through 2031.

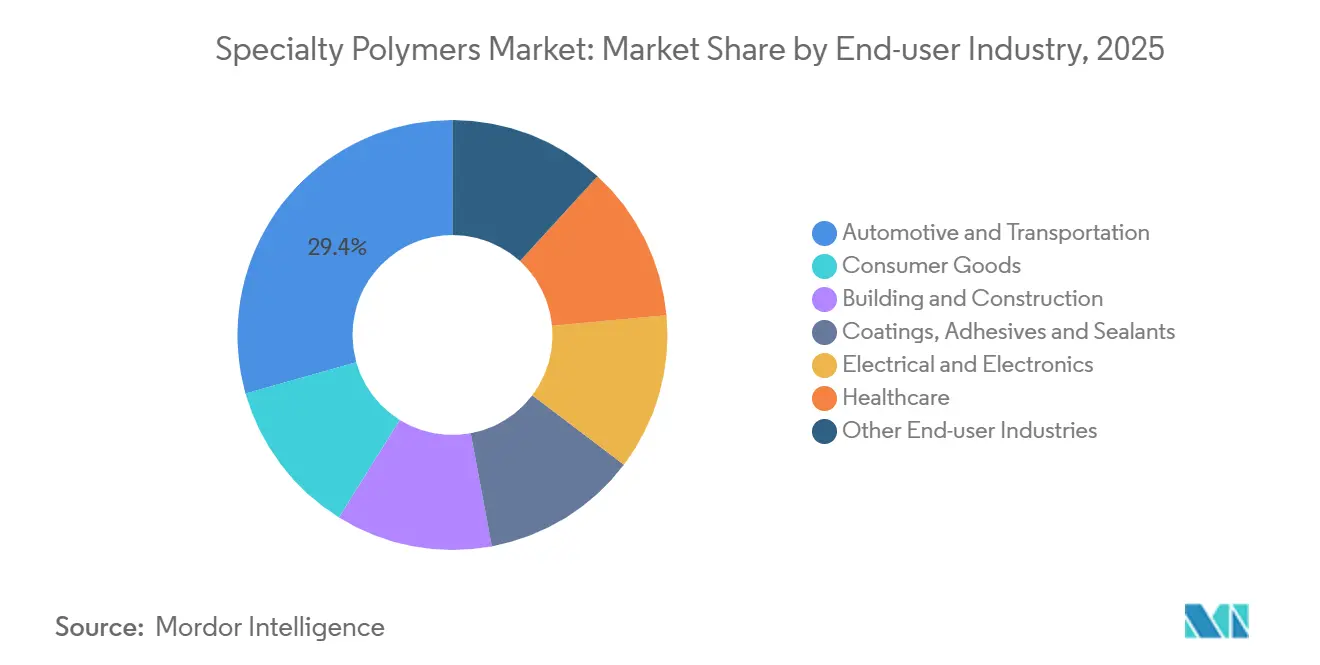

- Automotive and transportation held 29.38% of the specialty polymers market share in 2025, whereas healthcare is advancing at a 6.41% CAGR to 2031.

- Asia-Pacific accounted for 45.27% of global demand in 2025, and the region is projected to grow at a 5.94% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Specialty Polymers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting demand in automotive and aerospace | +2.1% | Global, concentrated in North America, Europe, Asia-Pacific automotive hubs | Medium term (2–4 years) |

| Expanding construction and electronics uses | +1.8% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥4 years) |

| Abundant gas-based feedstocks | +0.9% | Middle East, U.S. Gulf Coast, Appalachia | Short term (≤2 years) |

| 3-D printable specialty polymer filaments uptake | +0.7% | North America and Europe, early Asia-Pacific adoption | Medium term (2–4 years) |

| Perovskite-solar encapsulation film boom | +0.5% | China, Japan, emerging Europe and Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Demand in Automotive and Aerospace

More stringent fuel-economy and emissions regulations are urging automakers and aircraft OEMs to trim weight by swapping steel and aluminum with structural carbon-fiber composites and glass-fiber-reinforced thermoplastics that pare mass by 30–50% without sacrificing crash performance. Boeing’s composite-rich 787 Dreamliner cuts fuel burn 20% versus aluminum predecessors, validating polymer matrices that withstand 60,000 pressurization cycles. Electric-vehicle battery packs increasingly rely on flame-retardant polycarbonate and polyamide 6,6 to reach 400-mile ranges while meeting UL 94 V-0 standards. The U.S. Department of Energy directed USD 200 million in 2025 toward lowering carbon-fiber costs below USD 10 per kg, a threshold seen as critical for mass-market vehicle adoption.

Expanding Construction and Electronics Uses

Polyimide films rated above 400 °C glass-transition temperature now replace epoxy laminates in 5G base-station circuit boards, safeguarding signal integrity at 28 GHz frequencies. China installed more than 3.6 million 5G base stations by end-2025, generating sustained demand for low-loss liquid-crystal polymers and fluoropolymers. In construction, spray polyurethane foam insulation delivering R-6.5 per inch is mandated in updated International Energy Conservation Code revisions, cutting building energy loads by up to 40%. Germany earmarked EUR 1.5 billion in 2025 to retrofit commercial property envelopes with high-performance polymer insulation.

Abundant Gas-Based Feedstocks

Saudi Aramco’s 1.5 Mt/a ethane cracker in Jubail began operations in 2024, enabling ethylene costs 25–30% below European naphtha routes. Henry Hub natural-gas prices averaged USD 2.80 per MMBtu in 2025, allowing U.S. Gulf Coast ethylene cash costs near USD 300 per t and supporting exports of specialty polyethylene and EVA copolymers. Appalachian shale output reached 35 Bcf/d in 2025, underpinning propylene supply for polypropylene-based thermoplastic elastomers in automotive interiors. The International Energy Agency expects global LNG prices to converge by 2028, narrowing cost differentials.

3-D Printable Specialty Polymer Filaments Uptake

ASTM F3091, issued in 2024, standardized mechanical testing for fused-filament-fabrication grades and hastened FAA certification of PEEK and PEI parts for aircraft interiors[1]ASTM International, “Standard F3091 — 24,” astm.org. Evonik’s VESTAKEEP i4 G filament achieved ISO 10993 compliance in 2025, enabling patient-specific cranial implants that osseointegrate within 12 weeks. FDA guidance released in 2025 clarified sterilization validation for additively manufactured medical devices, lowering hospital adoption barriers. Stratasys captured 40% of aerospace tooling applications in 2025 with its ESD-safe Antero 840CN03 carbon-nanotube-filled PEEK filament.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility | -1.4% | Global, acute in import-dependent Europe and Asia-Pacific | Short term (≤2 years) |

| Rapid technology replacement cycles | -0.8% | North America and Asia-Pacific electronics hubs | Medium term (2–4 years) |

| Biodegradable-mandate drag on conventional grades | -0.6% | Europe, China, India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Brent prices oscillated between USD 70 and USD 90 per barrel during 2024–2025, and Henry Hub ranged from USD 2.50 to USD 4.20 per MMBtu, driving a 35% swing in ethylene and propylene costs. European producers reliant on Brent-indexed naphtha faced cash-cost disadvantages above USD 400 per t versus U.S. shale-gas peers, squeezing margins. BASF calculated a USD 10 per barrel oil uptick trims specialty-polymer operating margins by roughly 150 basis points when price pass-through lags. Smaller compounders lack hedging scale, making long-term contracts risky when spot spikes surface.

Rapid Technology Replacement Cycles

The shift from 4G to 5G antenna substrates cut polyimide film lifecycles from five years to 18 months, forcing suppliers to amortize R&D over smaller volumes. Foldable-display OEMs moved from PET to ultra-thin colorless polyimide in under two years, rendering capacity dedicated to legacy grades obsolete. The semiconductor roadmap foresees a transition from epoxy mold compounds to LCP substrates by 2027, compelling polymer suppliers to run parallel development programs until market consensus forms. Retrofit of reactors can cost more than USD 50 million per line and require 12-18 months of downtime, handicapping firms with inflexible footprints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Thermoplastics Anchor Revenue, Composites Lead Growth

Specialty thermoplastics delivered 38.46% of 2025 revenue, reflecting entrenched positions in automotive under-hood, semiconductor wet benches, and single-use medical device housings. PEEK, PPS, and liquid-crystal polymers satisfy thermal and chemical resistance benchmarks unmet by commodity resins, sustaining price premiums and operating margins above 20%. Specialty composites, while smaller in absolute size, climb at a 6.28% CAGR through 2031 as aerospace and offshore wind adopt carbon-fiber-reinforced polymers that reach tensile strengths above 600 MPa and endure 10 million fatigue cycles. Because composites reduce aircraft fuel burn 20–25%, program adoption (A350 XWB, 787, future narrow-body designs) validates the value proposition even at high dollar-per-pound material costs.

Thermosets remain important in printed-circuit boards and structural adhesives yet grow below the market average because cross-linked networks challenge recyclability targets in EU and U.S. automotive regulations. The specialty polymers market size for thermosets therefore trails the composites CAGR as OEMs scrutinize end-of-life pathways. Specialty elastomers occupy lucrative niches in EV battery seals and semiconductor wafer-handling where fluoroelastomers resist electrolytes and plasma etchants. Ultra-high-molecular-weight polyethylene and PTFE round out the portfolio with critical roles in orthopedic implants and chemical process linings, aided by ISO 21304 and ASTM D3159 certifications that protect incumbents from fast-moving entrants.

By End-User Industry: Automotive Dominates, Healthcare Accelerates

Automotive and transportation accounted for 29.38% of specialty polymers consumption in 2025. Lightweight glass-fiber-reinforced polyamide 6 battery trays cut mass 40%, enabling 400-mile driving ranges on 80-kWh packs. Yet healthcare advances quickest, clocking a 6.41% CAGR through 2031 as implantable PEEK cages and PEI surgical instruments withstand 134 °C steam sterilization while preserving mechanical integrity. The specialty polymers market size for healthcare is projected to outpace automotive by mid-decade as additive manufacturing delivers patient-specific devices that cut revision surgeries 30%.

Electronics end-uses hinge on low-loss dielectrics for 5G antennas and semiconductor encapsulants, driving demand for LCP and fluoropolymers with dielectric constants below 3.0 and dissipation factors under 0.005. Building and construction applications revolve around spray polyurethane foam and polyisocyanurate insulation aligned with International Energy Conservation Code R-value thresholds, underscoring polymer contributions to building-sector decarbonization. Consumer goods and recreational equipment adopt thermoplastic elastomers that combine a rubber-like feel with injection moldability. Coatings, adhesives, and sealants capitalize on waterborne polyurethane dispersions to meet VOC caps across North America and Europe.

Geography Analysis

Asia-Pacific held 45.27% of the global specialty polymers market share in 2025 and is set to expand at a 5.94% CAGR to 2031. Domestic Chinese lithium-ion battery output topped 750 GWh in 2025, consuming roughly 150,000 t of polypropylene and polyethylene separators[2]Ministry of Industry and Information Technology, “China Battery Output Statistics 2025,” miit.gov.cn. India’s specialty polymer exports for drug-delivery systems jumped 28% in 2025 as hydroxypropyl methylcellulose and PVA gained traction in controlled-release tablets. Vietnam and Thailand collect electronics-assembly investment that requires high-purity polyimide films meeting IPC-4101 specifications, while Japan and South Korea channel government funds into colorless polyimide substrates for foldable displays.

North America leverages shale-gas economics and Inflation Reduction Act incentives. DOE awarded USD 3.1 billion in 2025 to battery mega-factories, boosting demand for PVDF binders and polyethylene separators. Canada’s Nova Chemicals green-lit a CAD 2 billion high-density polyethylene build-out aimed at pipe and liner applications. Mexico’s 3.5 million-unit light-vehicle output in 2025 relies on reinforced thermoplastics compounded in Querétaro and Nuevo León for USMCA supply chains.

Europe’s specialty polymers market is shaped by REACH compliance and end-of-life recycling directives. German mechanical recyclers processed 180,000 t of engineering thermoplastics in 2025, up 22% from 2023. France devoted EUR 800 million in 2025 to chemical recycling pilots for PET and PLA monomer recovery. The UK’s GBP 150 million investment targets carbon-fiber recycling, recovering 95% of tensile strength for aerospace reuse. Middle Eastern producers capitalize on sub-USD 250 per t ethylene cash costs, exporting specialty polyethylene and EVA to Asian converters. South America remains focused on Brazilian automotive and packaging outlets serviced by Braskem’s São Paulo polypropylene compounding hub.

Value Chain Analysis

The specialty polymers value chain begins with upstream feedstocks and intermediates (petrochemical derivatives and specialty monomers), along with catalysts, solvents, and performance additives (flame retardants, stabilizers, conductive fillers). Polymerization and resin manufacture lead into compounding, formulation, and conversion into semi-finished forms (films, fibers, compounds, and masterbatches) that are qualified by end users including automotive, electronics, healthcare, construction, and aerospace. Distributors are particularly influential for many specialty grades, aggregating volumes, managing regulatory documentation, and providing technical service for converters that need small lots and frequent grade changes.

The main frictions show up in feedstock and energy cost volatility, batch scheduling constraints, high minimum order quantities, and geographic concentration for some monomers and high-purity grades. These factors can heighten lead-time risk when logistics or ports are disrupted. In 2026, several moves pointed to tighter collaboration and more regional routing between producers and downstream users: Covestro signed an MoU with BYD for long-term co-development of advanced materials for EVs and energy storage (July 2026), Teknor Apex formed a joint venture with Shriram Polytech in India to supply advanced polymer compounds (April 2026), and Evonik expanded its VISIOMER Specialty Methacrylates distribution partnership with IMCD to include the United States (March 2026).

Competitive Landscape

The global specialty polymers market is moderately consolidated, with the top five manufacturers operating in the market accounting for a considerable market share. In the recent period, leading players such as BASF recorded significant operating margins by targeting safety-critical fuel systems and medical housings. Niche leaders like Invibio dominate implantable-grade PEEK by leveraging ISO 13485 quality systems and extensive biocompatibility dossiers that impose 18-24 month qualification barriers for new entrants. Patent filings in high-temperature 3D-printing filaments climbed 40% between 2024 and 2025, underscoring intensified competition for aerospace tooling and end-use parts.

Specialty Polymers Industry Leaders

BASF SE

Evonik Industries AG

Covestro

Arkema Group

3M

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Demand pull from batteries, semiconductors, and high-temperature electronics is translating into targeted capacity additions and more localized supply. That creates whitespace for qualified, application-specific grades that can reduce requalification cycles for OEMs. Arkema commissioned a new Rilsan Clear transparent polyamide unit in Singapore in January 2026 (tripling global capacity), and it also started up a 15% PVDF capacity expansion at Calvert City, Kentucky in June 2026 to serve energy storage and semiconductor applications, highlighting opportunities for suppliers that can deliver consistent purity, traceability, and regional availability.

Circularity and lower-carbon product attributes continue to shape procurement and design choices, particularly where customers require mass-balance or renewable-energy-based claims while maintaining performance. BASF introduced Ultrason P 3010 BMB, a biomass-balanced polyphenylsulfone (PPSU) grade (March 2026), and Covestro expanded its footprint in isocyanate derivatives by acquiring two former Vencorex production sites in Rayong, Thailand and Freeport, Texas (July 2026), supporting opportunities in specialty polyurethane systems and downstream formulations. Investment into adjacent enabling capacity also supports specialty polymer production, including Air Liquide announcing over USD 200 million for a high-efficiency partial oxidation unit at Oxea's Bay City, Texas site (July 2026), aligned with broader moves toward integrated, resilient chemical manufacturing platforms.

Recent Industry Developments

- July 2026: BASF expanded its portfolio of biomass-balanced additives for architectural coatings. The update supports formulators seeking lower-footprint inputs while maintaining performance in coatings, adhesives, and sealants applications that consume specialty polymer systems.

- March 2026: Evonik expanded its strategic distribution partnership with IMCD for VISIOMER Specialty Methacrylates to include the United States. The step improves product reach and supply continuity for specialty methacrylates used across high-value formulations, supporting faster customer qualification and broader penetration in North America.

- March 2025: Covestro opened a Shanghai innovation hub with a pilot line for chemical recycling of polycarbonate and TPU, targeting around 90% monomer purity. The addition reinforces regional R&D and pilot capability for circular feedstock pathways, helping downstream users test recycled-content solutions for regulated and performance-critical applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the specialty polymers market is defined as the value of high performance polymer materials sold into industrial and consumer end uses, where the material is selected for properties like heat, chemical, or mechanical resistance.

Scope exclusions: Commodity plastics used in standard-grade packaging and general-purpose applications are excluded from this market sizing.

Segmentation Overview

- By Type

- Specialty Elastomers

- Specialty Composites

- Specialty Thermoplastics

- Specialty Thermosets

- Other Types

- By End-user Industry

- Automotive and Transportation

- Consumer Goods

- Building and Construction

- Coatings, Adhesives and Sealants

- Electrical and Electronics

- Healthcare

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi-Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to map the supply chain and pin down where value is created, priced, and reported for specialty polymers. We relied on public sources such as the USGS, US Census Bureau manufacturing and trade releases, Eurostat, UN Comtrade, and OECD industry statistics to understand macro movement in polymer production, trade, and downstream consumption.

To convert industry signals into model-ready inputs, company annual reports, investor presentations, and credible trade association publications were reviewed, followed by cross-checking with reputable news coverage. For fill-in context, paid subscriptions supporting company financials and intelligence, patent lookups, and shipment-level import and export views were also used selectively where public data was thin or delayed. These desk sources are illustrative only, and many other references were consulted for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and short surveys across resin producers, compounders, distributors, and downstream buyers in major end-use industries like automotive, construction, electronics, and healthcare. We used these discussions to validate price ranges, typical contract and spot dynamics, adoption shifts by region, and to sanity-check the demand pool assumptions that desk research alone could not confirm.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 50% |

| Mid tier: 54% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 19% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production, trade, and downstream conversion indicators are used to reconstruct regional demand and then translated into value using realistic price bands. To keep the totals grounded, selective bottom-up approximations are used as a cross-check, such as rolling up a sampled set of supplier revenues by specialty polymer lines and then reconciling that with channel checks on volumes and average selling prices.

Key inputs used in the model include specialty polymer price spreads versus general-purpose resin, capacity additions and utilization trends in high performance resin lines, import and export flow shifts for higher value polymer grades, end-use activity signals (construction starts, vehicle output, and electronics production), and substitution intensity where specialty materials replace conventional grades. For the forecast, scenario analysis is applied, where base-case end-use growth, expected pricing progression, and adoption rates are adjusted using what industry participants expect to hold true by region. When bottom-up data is incomplete for smaller suppliers, gaps are handled through peer benchmarking and region-specific scaling factors, and then rechecked with primary feedback before finalizing.

Data Validation & Update Cycle

Validation is done in layers, starting with variance checks between the model output and independent signals like trade flows, capacity news, and end-use production trends. Any large jumps are reviewed, and the assumptions behind volumes, pricing bands, and mix are revisited before sign-off, followed by a second analyst review to reduce avoidable errors.

The study is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major capacity start-ups, policy shifts affecting trade, or sharp feedstock-driven price moves. Before delivery, we run a final update pass so the client receives the most current view that can be supported by the latest available data and primary checks.

Mordor Intelligence's Specialty Polymers Market Size Compared With Other Published Estimates

Published market numbers for specialty polymers often vary because each publisher draws the line differently on what counts as specialty, and because price and volume assumptions are refreshed at different times. Differences also come from how much is modeled from end-use demand signals versus how much is inferred from broad chemical totals.

Commodity plastics used in standard-grade packaging sit outside Mordor Intelligence's scope, which can widen the spread versus estimates that blend specialty materials with higher-value portions of general-purpose resin demand. Gaps are also created by how average selling prices are escalated (spot-heavy assumptions versus contract-weighted ranges), how trade is treated in regional rollups, and whether the model is validated against capacity utilization and downstream output checks before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 157.64 B (2026) | |

| Global Consultancy A | USD 185.10 B (2024) | Uses an earlier base year and applies a faster growth curve, and the summary scope suggests broader inclusion across forms and sources which can lift totals when specialty versus non-specialty boundaries are not tightly filtered. |

| Industry Publisher B | USD 92.19 B (2025) | Reports a lower current value that can result from narrower counting of product groups and more conservative price bands, and it may also reflect a tighter cut on what is treated as specialty within elastomers, thermoplastics, thermosets, and composites. |

The comparison shows that timing and classification drive most of the gap, not a single data point. By keeping the demand pool tied to end-use signals and then pressure-testing pricing and mix with real market feedback, the final number stays traceable to clear inputs that can be repeated and updated.

Key Questions Answered in the Report

What is the value of the specialty polymers market in 2026?

The market is estimated to be valued at USD 157.64 billion in 2026.

How fast is Asia-Pacific demand for specialty polymers growing?

Asia-Pacific demand is forecast to rise at a 5.94% CAGR through 2031.

Which material type is expanding the quickest?

Carbon-fiber-reinforced specialty composites are projected to grow at a 6.28% CAGR.

Why is healthcare the fastest-growing end-user?

Biocompatible polymers for implantables and drug-delivery devices are driving a 6.41% CAGR in healthcare applications.

What factor most threatens specialty polymer margins?

Feedstock price volatility can compress operating spreads by as much as 150 basis points for every USD 10 per barrel uptick in crude prices.

Page last updated on: