Water-soluble Polymer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

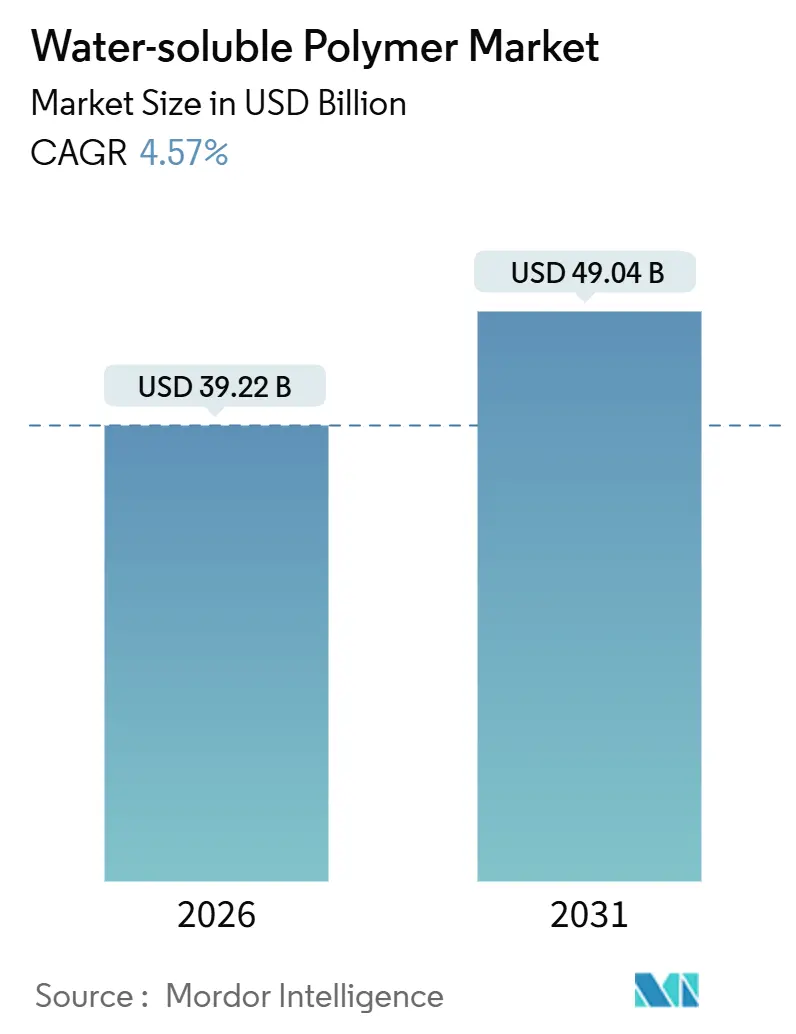

| Market Size (2026) | USD 39.22 Billion |

| Market Size (2031) | USD 49.04 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

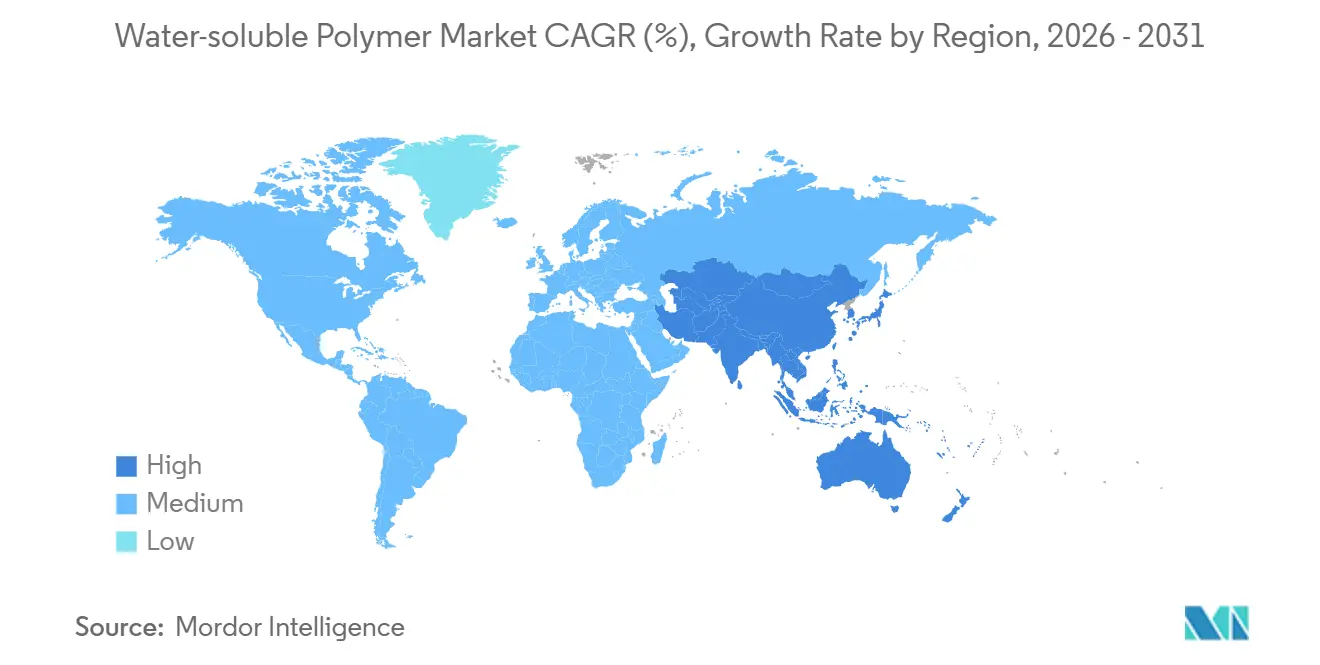

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water-soluble Polymer Market Analysis by Mordor Intelligence

The Water-soluble Polymer Market size is estimated at USD 39.22 billion in 2026, and is expected to reach USD 49.04 billion by 2031, at a CAGR of 4.57% during the forecast period (2026-2031). Ongoing upgrades to tertiary treatment systems in China and the European Union, accelerating shale-gas enhanced oil recovery activity in North America, and growing demand for polyvinyl alcohol (PVA) films in unit-dose household products collectively underpin steady expansion of the water-soluble polymer market. Competitive activity is intensifying as Asian producers leverage integrated acrylonitrile and acrylamide capacity to achieve double-digit cost advantages, pressuring Western suppliers to pivot toward specialty high-charge-density grades. Meanwhile, imminent EU and Chinese restrictions on microplastic release are steering research and development toward enzymatically degradable copolymers and natural hydrocolloids.

Key Report Takeaways

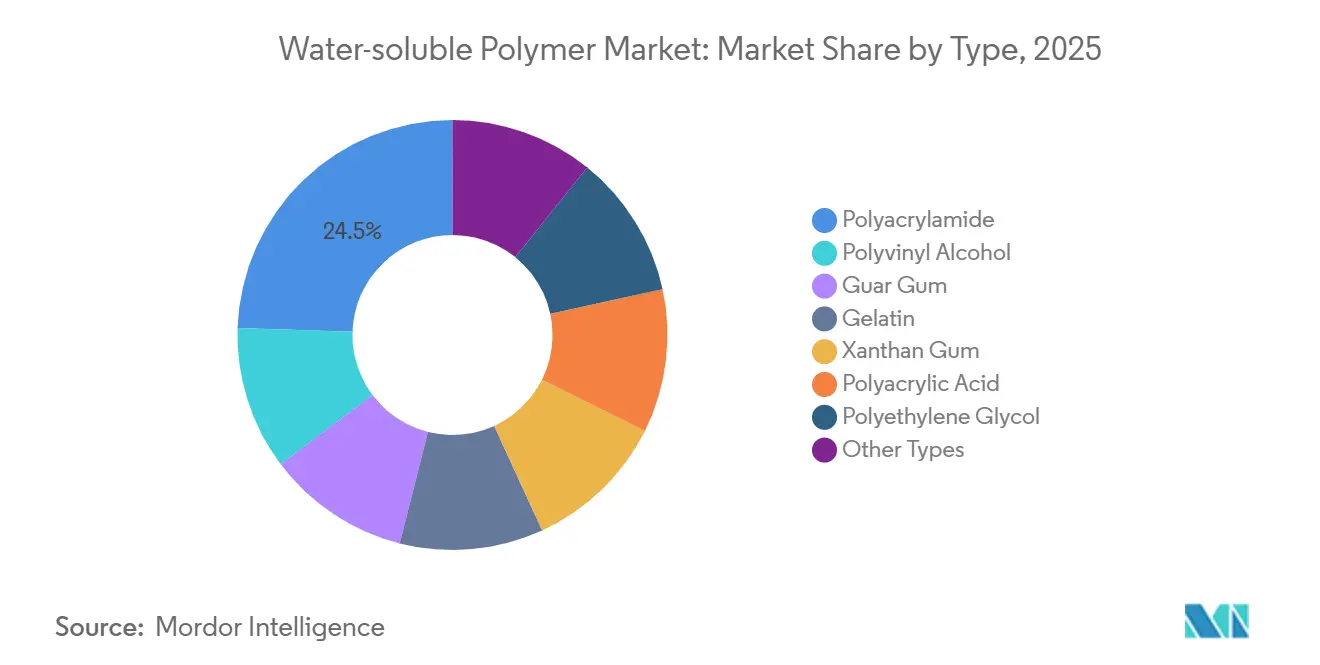

- By type, polyacrylamide led with 24.48% revenue share in 2025, while it also recorded the fastest growth at 4.75% CAGR through 2031.

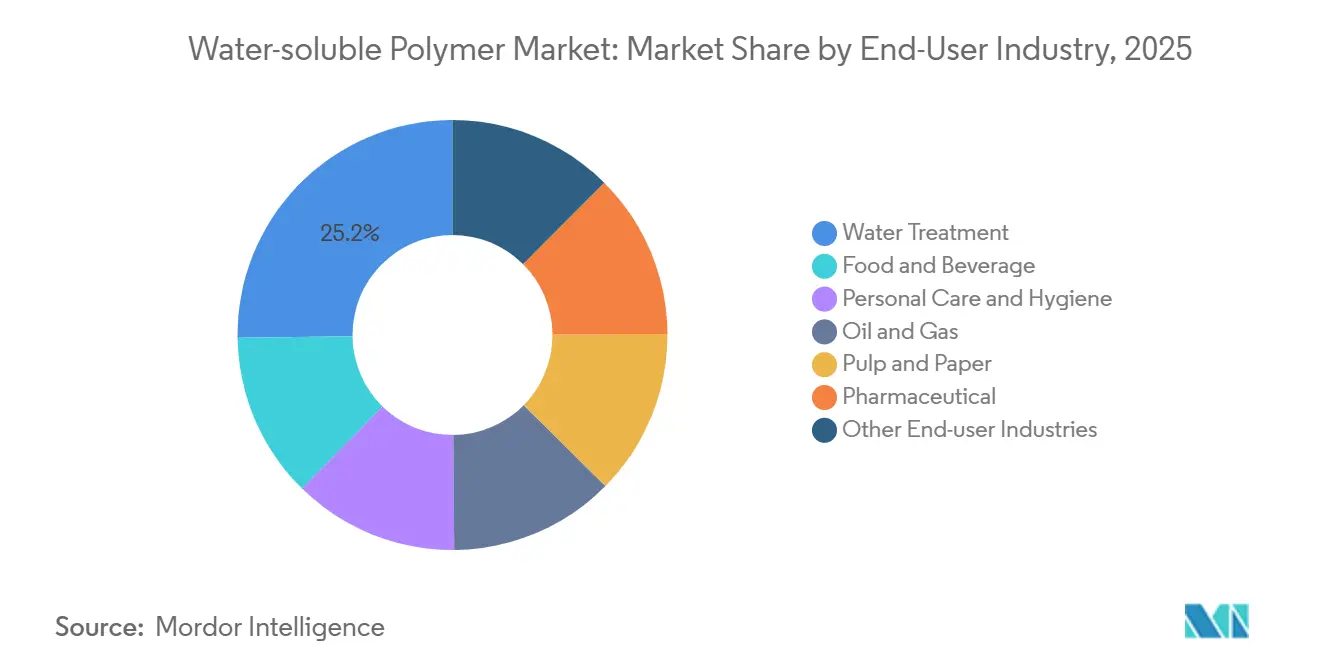

- By end-user industry, water treatment held 25.20% of the water-soluble polymer market share in 2025, whereas pharmaceuticals posted the highest projected CAGR at 5.02% through 2031.

- By geography, Asia-Pacific commanded 50.17% value in 2025 and is expected to expand at a 4.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Water-soluble Polymer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global municipal and industrial wastewater treatment investment | +1.2% | Global, with APAC core and spill-over to MEA | Medium term (2-4 years) |

| Shale-gas EOR polymer demand rebound in North America | +0.6% | North America, primarily United States and Canada | Short term (≤ 2 years) |

| Personal-care formulators accelerating shift toward water-soluble rheology modifiers | +0.5% | Global, led by Europe and North America | Medium term (2-4 years) |

| European Union and Asian phosphorus-free discharge rules boosting advanced polyacrylamides | +0.9% | Europe and APAC (China, Japan, South Korea) | Long term (≥ 4 years) |

| Rapid growth of unit-dose e-commerce packaging using PVA films | +0.7% | Global, with North America and Europe early adopters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Global Municipal and Industrial Wastewater Treatment Investment

In 2025, global spending on wastewater treatment reached significant levels. This surge in investment has driven up the demand for ultra-high-molecular-weight anionic polyacrylamides, known for their ability to reduce sludge volumes and cut disposal costs. By the end of 2025, China implemented nationwide Class 1A effluent limits, leading to increased polyacrylamide consumption[1]Ministry of Housing and Urban-Rural Development China, “Class 1A Standards,” mohurd.gov.cn. Meanwhile, India's National Mission for Clean Ganga allocated substantial funds for the establishment of new sewage plants. Each of these plants will require polymer flocculants. In the Middle East, newly commissioned desalination projects in 2025 are utilizing polyacrylic acid and polyethylene glycol antiscalants. These are essential for safeguarding membranes in a new capacity. Collectively, these initiatives position municipal and industrial players as leaders in the water-soluble polymer market.

Shale-Gas Polymer Demand Rebound in North America

In 2025, North American operators consumed significant volumes of water-soluble polymers, coinciding with crude prices stabilizing. Partially hydrolyzed polyacrylamide, a key player in polymer flooding, boasts an incremental recovery advantage over traditional waterflooding. Meanwhile, xanthan gum is carving out a larger share in high-salinity reservoirs, bolstered by new U.S. capacity that became operational in 2024-2025. Additionally, federal grants are fueling research into thermally stable, degradable copolymers aimed at mitigating formation damage. Collectively, these developments underscore the oilfield's pivotal role in bolstering the water-soluble polymer market.

Personal-Care Formulators Accelerating Shift Toward Water-Soluble Rheology Modifiers

In 2024-2025, personal-care SKUs reformed their formulations, replacing silicones with hydroxyethyl cellulose, polyquaternium-10, and carbomer formulations, all in a bid for a cleaner label. As sulfate-free shampoos gained traction, Ashland's Natrosol line experienced notable growth. In March 2025, BASF introduced a bio-based polyquaternium-87, specifically designed for humidity-resistant hair care. Starting January 2026, amendments to the EU Cosmetics Regulation will mandate complete polymer traceability, nudging brands to collaborate with suppliers boasting robust GMP credentials. These strategic shifts bolster the demand for water-soluble polymers in the personal-care sector.

European Union and Asian Phosphorus-Free Discharge Rules Boosting Advanced Polyacrylamides

Revisions to the EU Urban Waste Water Treatment Directive are set to lower phosphorus limits to 0.5 mg/L by 2027. This move is prompting the adoption of higher-charge-density cationic polyacrylamides in numerous plants. Starting January 2025, China is implementing the same limits in the Yangtze River Economic Belt, leading to increased polyacrylamide usage. Meanwhile, Japan and South Korea are rolling out subsidies and legal mandates to boost the adoption of advanced flocculants. Together, these regulations are bolstering the water-soluble polymer market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.8% | Global, with acute impact in APAC and Europe | Short term (≤ 2 years) |

| Escalating end-of-life and toxicity regulations on non-biodegradable polymers | -0.5% | Europe, North America, and APAC (China, Japan) | Medium term (2-4 years) |

| Forthcoming microplastic limits on soluble/dispersible chemistries | -0.4% | Europe and North America, with APAC monitoring | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

In 2024-2025, acrylonitrile prices fluctuated significantly following propylene disruptions in China. This volatility compressed polyacrylamide margins. Similarly, vinyl acetate monomer prices experienced a notable surge during the same timeframe. Meanwhile, guar gum prices increased sharply as drought conditions in India slashed the harvest. Such fluctuations challenge cost predictability in the water-soluble polymer market.

Escalating End-of-Life and Toxicity Regulations on Non-Biodegradable Polymers

China's draft catalogue aims to phase out specific polyacrylamide grades in agriculture by 2028, citing concerns over acrylamide leaching. In 2024, ECHA initiated a restriction dossier focusing on residual acrylamide levels. Japan, in 2025, reduced the acrylamide limit in food-contact polymers[2]European Chemicals Agency, “REACH Microplastics Restriction,” echa.europa.eu . Additionally, India mandated biodegradability tests for detergent polymers under IS 17088 in 2025. These regulatory moves cast a shadow on the growth prospects of the water-soluble polymer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type – Polyacrylamide Strengthens Flocculation Leadership

Polyacrylamide delivered 24.48% of 2025 revenue and will expand at a 4.75% CAGR to 2031. This growth is largely attributed to newly implemented phosphorous discharge regulations, which favor ultra-high-molecular-weight grades of polyacrylamide. These grades can significantly reduce sludge disposal costs. As a result, polyacrylamide is poised to play a pivotal role in the water-soluble polymer market, especially in treatment chemistries. Meanwhile, PVA films, commonly used in unit-dose detergents, are witnessing strong growth. However, potential restrictions on microplastics present a looming challenge. Guar gum faced challenges due to raw material risks stemming from a crop shortfall in India, leading to a notable shift towards xanthan gum in fracturing fluids. Gelatin continues to dominate the soft-gel capsule market, bolstered by an increase in high-bloom output from contract manufacturing organizations (CMOs) in the Asia-Pacific region. Both polyacrylic acid and sodium polyacrylate are seeing heightened demand in hygiene products and for inhibiting scale in cooling water. This demand surge is further supported by the introduction of new low-residual-monomer grades, which are in line with California’s stringent consumer-product regulations. While PEG remains a sought-after ingredient in injectables and cosmetics, it is under increasing scrutiny, prompting research and development to pivot towards bio-based alternatives. Additionally, cellulose ethers, pectin, and modified starches continue to carve out niche roles in the market, bolstered by their Generally Recognized As Safe (GRAS) status and a natural branding approach.

Polyacrylamide's leading position in the market is not just a testament to its technical prowess but also to China's backward-integrated cost structures. These structures have significantly bolstered the segment's share in the broader water-soluble polymer market. While PVA's rising popularity in consumer pods signals a diversification of revenue streams, suppliers face a pressing challenge: to produce credible biodegradation documentation by 2027 to maintain their market volume. The volatility of guar gum, especially in light of India's crop challenges, has prompted oilfield users to broaden their polymer selections, safeguarding their profit margins from unpredictable weather-related supply disruptions. Suppliers of gelatin, riding the wave of growth in biologics, must remain vigilant against risks like bovine spongiform encephalopathy, emphasizing the need for stringent traceability measures. Producers of polyacrylic acid are now promoting ultra-low-monomer variants, solidifying their foothold in hygiene and household markets, especially as regulatory scrutiny intensifies. As the market evolves, PEG and niche specialty types are expected to shift focus towards the more lucrative pharmaceutical and medical-device sectors. In contrast, natural hydrocolloids are actively seeking efficiencies in fermentation processes to stay competitive against synthetic alternatives.

By End-User – Pharmaceuticals Accelerate While Water Treatment Remains Core

Water treatment accounted for 25.20% of the 2025 demand. As mature utilities complete capacity additions and pivot towards process optimization, growth has moderated. Pharmaceutical manufacturers, especially in Asia-Pacific, are scaling high-purity PEG, PVA, and cellulose ethers for biologics and controlled-release tablets, driving a 5.02% CAGR through 2031. Meanwhile, food and beverage formulators are prioritizing clean-label thickeners, leading to the emergence of new plant-based texturizer blends as substitutes for synthetic options. In personal care, there's a notable shift as formulators move towards sulfate- and silicone-free systems, resulting in a surge for hydroxyethyl cellulose and polyquaternium conditioners.

Amid rising crude prices, oil and gas operators are amplifying polymer flooding volumes to enhance recovery, consequently boosting the segment’s share in the water-soluble polymer market. Pulp and paper mills are adopting cationic starch and polyacrylamide as retention aids, aiming to curtail fiber loss and minimize water usage. While agrochemical adoption of PVA pouch technology is on the rise, it grapples with challenges stemming from China's draft restrictions on non-biodegradable polyacrylamide for soil conditioning. In India, the Production-Linked Incentive scheme is fast-tracking local excipient capacity, bolstering domestic self-sufficiency and amplifying the pharmaceutical sector's demand for the water-soluble polymer industry.

Geography Analysis

Asia-Pacific held 50.17% of global value in 2025 and will advance at a 4.74% CAGR through 2031. This growth is bolstered by substantial investments in wastewater management in China and India's comprehensive rural water initiative. Countries like Japan, South Korea, and various Southeast Asian nations are amplifying demand by enhancing their pharmaceutical excipient capacities and wastewater infrastructures. Given its leading role in both the production and consumption of water-soluble polymers, the Asia-Pacific region solidifies its dominance in the market.

North America is witnessing a resurgence, driven by stabilizing shale-gas activities and the EPA's stringent zero-discharge regulations, which have compelled coal plants to transition to advanced polymers. Canada is at the forefront, experimenting with amphoteric polyacrylamides for oil-sands tailings. Meanwhile, Mexico is channeling funds into upgrading wastewater systems in its major metropolitan areas. These diverse initiatives underscore North America's significant standing in the water-soluble polymer market.

Europe is reshaping its product offerings in response to its push for phosphorus-free effluents and stringent microplastic regulations. This shift is steering the market towards high-charge-density polyacrylamides and eco-friendly alternatives. With numerous municipal plants in need of tertiary upgrades, there's an anticipated demand surge for polymers. While Nordic countries champion natural hydrocolloids due to biodegradability mandates, projects in Russia's Volga Basin are spurring growth in Eastern Europe.

South America is capitalizing on Brazil's ambitious sanitation initiative, Argentina's experimental polymer seed-coating, and mining endeavors in the Andes to boost regional consumption. In the Middle-East and Africa, efforts to expand desalination capacities and modernize wastewater facilities in South Africa are bolstering the demand for scale inhibitors and flocculants, further diversifying the global water-soluble polymer landscape.

Competitive Landscape

The water-soluble polymers market is moderately fragmented. Western leaders migrate toward specialized grades such as amphoteric polyacrylamides for tailings and ultra-low-residual-monomer excipients. Chinese firms added new capacity during 2024-2026 to meet municipal and mining demand. Bio-manufacturing startups leverage synthetic biology to cut fermentation costs for xanthan and gellan, challenging incumbents on both price and sustainability credentials. ISO 9001 and ISO 14001 certifications are increasingly mandatory in municipal tenders, favoring producers with multinational quality systems and transparency.

Water-soluble Polymer Industry Leaders

SNF Group

BASF SE

Ashland

Kemira

Kuraray Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mitsubishi Chemical secured ISCC PLUS certification for specialty PVOH grades including GOHSENX and Nichigo G-Polymer.

- June 2024: Kuraray unveiled ready-to-use water-based PVA solutions that cut customer heating energy and lower carbon footprints at its Frankfurt site.

Global Water-soluble Polymer Market Report Scope

Water-soluble polymers are large molecules composed of repeating units that can dissolve or disperse in water. These polymers possess hydrophilic groups or side chains that interact with water molecules, allowing them to dissolve and form solutions or colloidal suspensions. They can range from natural polymers like cellulose derivatives, starch, and proteins to synthetic polymers. Water-soluble polymers have extensive use in various industries because they can modify the properties of water, enhance product performance, and facilitate processes such as thickening, stabilization, adhesion, and drug delivery.

The water-soluble polymer market is segmented by type, end-user industry, and geography. By type, the market is segmented into polyacrylamide, polyvinyl alcohol, guar gum, gelatin, xanthan gum, polyacrylic acid, polyethylene glycol, and other types (cellulose ethers, pectin, and starch). Based on the end-user industry, the market is segmented into water treatment, food and beverage, personal care and hygiene, oil and gas, pulp and paper, pharmaceutical, and other end-user industries (agrochemicals). The report also covers the market sizes and forecasts for the water-soluble polymer market in 22 countries across the major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Polyacrylamide |

| Polyvinyl Alcohol |

| Guar Gum |

| Gelatin |

| Xanthan Gum |

| Polyacrylic Acid |

| Polyethylene Glycol |

| Other Types (Cellulose Ethers, Pectin, and Starch) |

| Water Treatment |

| Food and Beverage |

| Personal Care and Hygiene |

| Oil and Gas |

| Pulp and Paper |

| Pharmaceutical |

| Other End-user Industries (Agrochemicals) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Polyacrylamide | |

| Polyvinyl Alcohol | ||

| Guar Gum | ||

| Gelatin | ||

| Xanthan Gum | ||

| Polyacrylic Acid | ||

| Polyethylene Glycol | ||

| Other Types (Cellulose Ethers, Pectin, and Starch) | ||

| By End-User Industry | Water Treatment | |

| Food and Beverage | ||

| Personal Care and Hygiene | ||

| Oil and Gas | ||

| Pulp and Paper | ||

| Pharmaceutical | ||

| Other End-user Industries (Agrochemicals) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the water-soluble polymer market?

The water-soluble polymer market size stands at USD 39.22 billion in 2026, tracking the 4.57% CAGR, reaching USD 49.04 billion by 2031.

Which polymer type holds the leading position?

Polyacrylamide leads with a 24.48% share in 2025, buoyed by global wastewater treatment upgrades and oilfield adoption.

Why is Asia-Pacific so dominant?

Regional investments in wastewater infrastructure and robust pharmaceutical capacity expansions lift Asia-Pacific to 50.17% of global value.

What is the fastest-growing end-user segment?

Pharmaceutical manufacturing shows the fastest trajectory at 5.02% CAGR through 2031 as biologics and controlled-release drugs expand.

Page last updated on: