Market Overview

| Study Period | 2021 - 2031 |

|---|---|

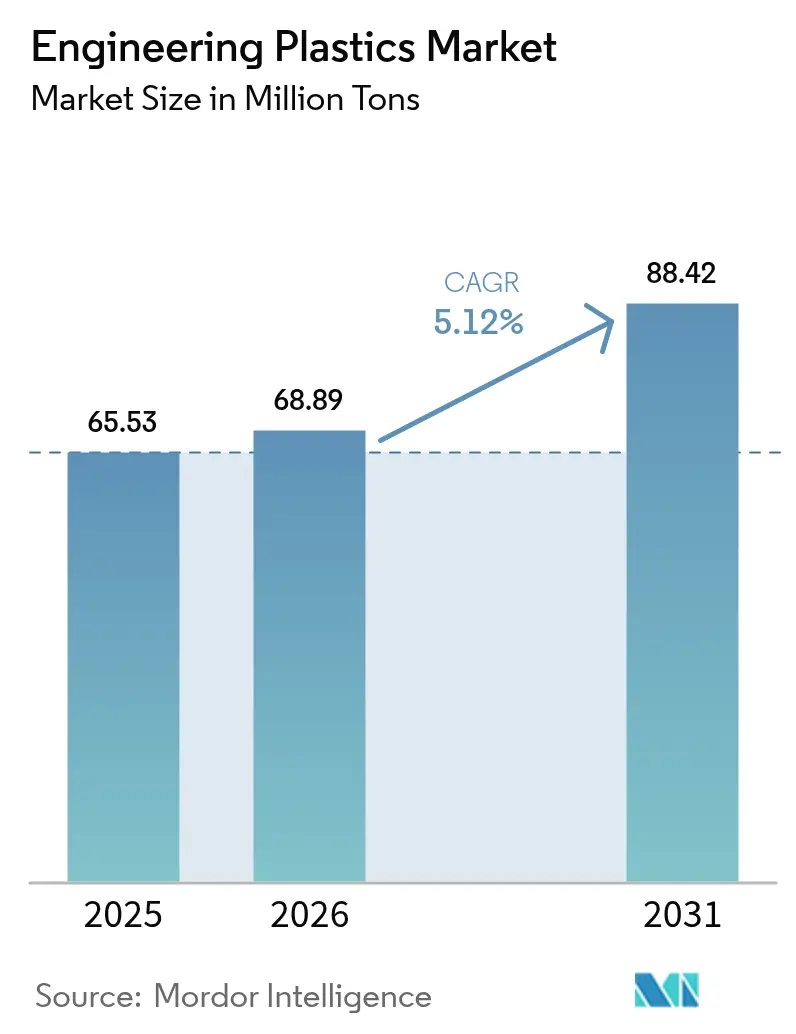

| Market Volume (2026) | 68.89 Million tons |

| Market Volume (2031) | 88.42 Million tons |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

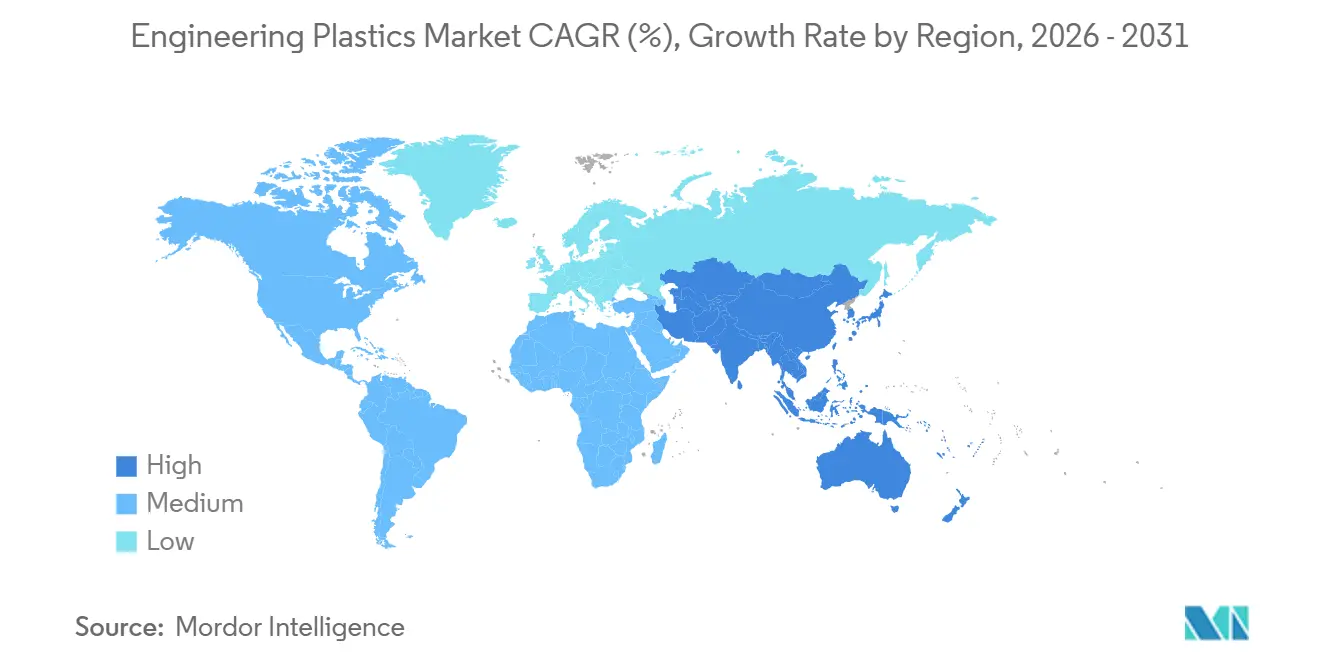

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Engineering Plastics Market Analysis by Mordor Intelligence

The Engineering Plastics Market size is projected to expand from 65.53 Million tons in 2025 and 68.89 Million tons in 2026 to 88.42 Million tons by 2031, registering a CAGR of 5.12% between 2026 to 2031. Rising demand from mobility lightweighting programs, electrified power-train architectures, and semiconductor-fabrication investments is steering resin substitution away from metals and commodity polymers. Battery-module housings increasingly specify flame-retardant polyamides and polycarbonates that shave mass while simplifying thermal management. Simultaneously, chemical-recycling start-ups are injecting recycled feedstock into polyester and polyamide streams, enabling brand owners to meet recycled-content pledges without compromising mechanical performance. Competitive intensity remains moderate as the top five suppliers control roughly 38% of global capacity, yet fresh capacity announcements in Asia-Pacific and the United States hint at a supply-side reshuffle. Regulatory moves—particularly Europe’s revised Packaging and Packaging Waste Regulation—are tightening virgin-resin use thresholds, pressuring converters to pivot toward circular grades.

Key Report Takeaways

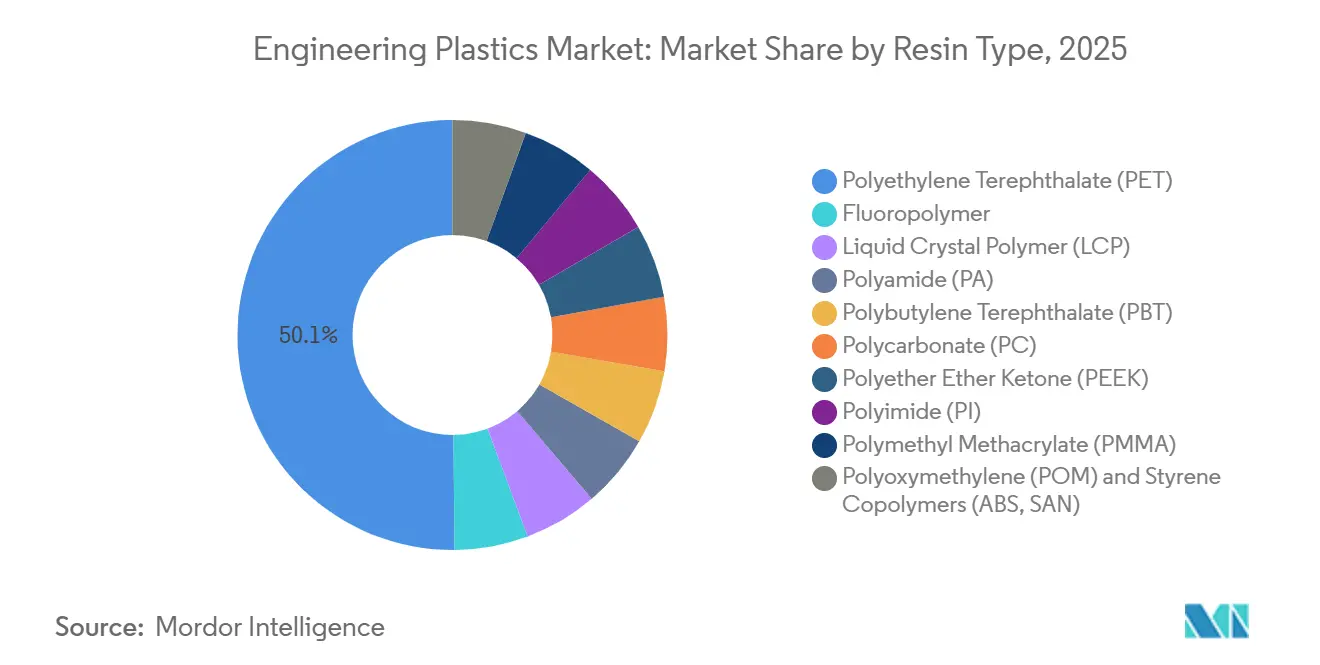

- By resin type, polyethylene terephthalate (PET) led with 50.15% of engineering plastics market share in 2025, while fluoropolymers are forecast to expand at a 7.45% CAGR through 2031.

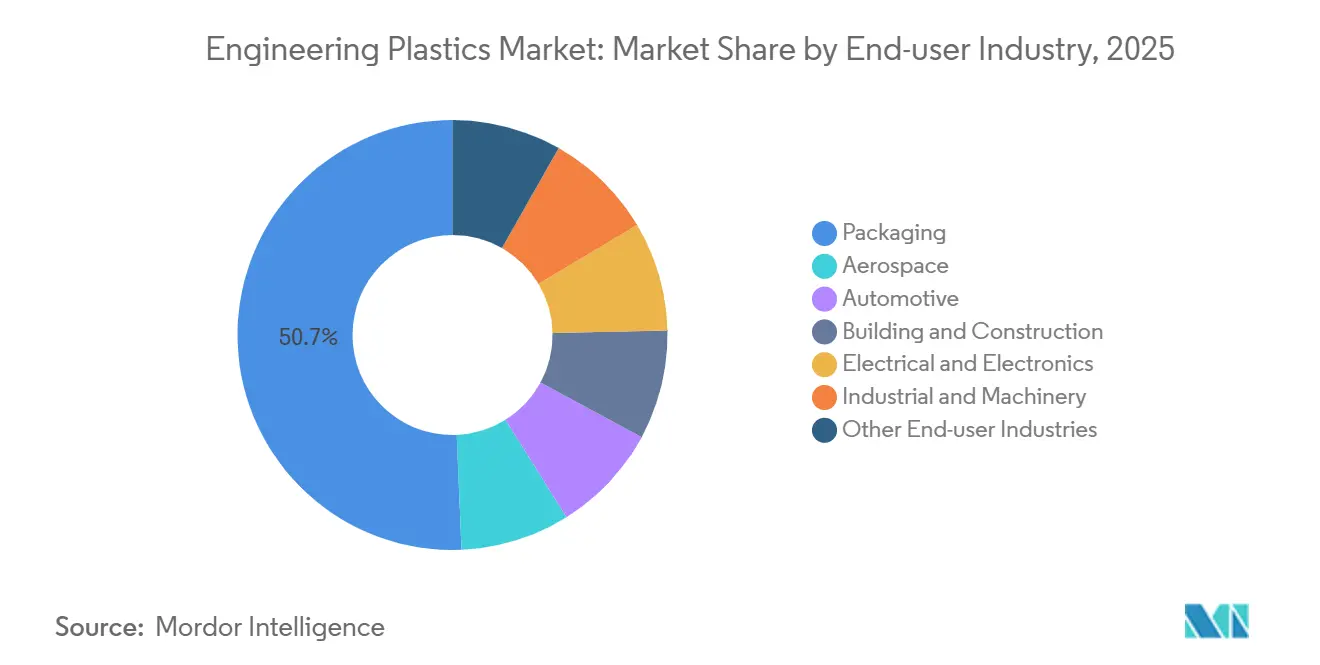

- By end-user industry, packaging captured 50.66% of the engineering plastics market size in 2025, while electrical and electronics are advancing at a 7.01% CAGR to 2031.

- By geography, Asia-Pacific accounted for 55.78% of 2025 volume, while it is projected to grow at a region-leading 5.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Engineering Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting Push in Mobility and Aerospace | +1.2% | Global, with concentration in North America, Europe, and China | Medium term (2-4 years) |

| Electrification-Led Demand Spike | +1.5% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Asia-Pacific Manufacturing Migration | +0.9% | APAC (China, India, ASEAN), with indirect effects in MEA | Long term (≥ 4 years) |

| EV Battery Module Housing Adoption | +0.8% | China, United States, Germany, South Korea | Medium term (2-4 years) |

| Chemical-Recycling Supply Boosts | +0.6% | North America and Europe, early pilots in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Push in Mobility and Aerospace

Weight-reduction mandates across automotive and aerospace fleets are accelerating substitution of steel and aluminum with high-performance thermoplastics. The U.S. EPA’s 2024 Corporate Average Fuel Economy revision compels light-duty vehicles to achieve 58 miles-per-gallon by 2032, giving automakers a direct incentive to deploy glass-fiber-reinforced polyamides for intake manifolds and polycarbonate glazing in sunroofs[1]U.S. Environmental Protection Agency, “Corporate Average Fuel Economy Standards Final Rule,” epa.gov . Boeing’s 787 program already employs polyetheretherketone fasteners and polysulfone ducting that collectively lower empty weight by 20%. Airbus extended the narrative in 2025 after EASA certified polyimide-film insulation for A350 electrical harnesses, slicing wire-bundle mass by 12%. Proven aerospace data packages shorten validation cycles in automotive programs, enabling rapid cross-sector diffusion. Component suppliers now quote 40-50% mass savings over metal while holding cost parity at production volumes surpassing 300,000 parts per year, confirming durable momentum behind the engineering plastics market.

Electrification-Led Demand Spike

Battery-electric vehicle output hit 14.2 million units worldwide in 2025, and each platform consumes 18-25 kg of engineering plastics in high-voltage connectors, cell separators, and thermal-interface plates. SABIC’s Noryl GTX resin, a polyphenylene-ether blend, won designs in GM’s Ultium and Volkswagen’s MEB packs, replacing stamped-aluminum trays and cutting module mass by 3.2 kg. Covestro’s Makrolon TC grade, launched in 2024 with 3 W/m-K thermal conductivity, enables injection-molded cooling plates that delete brazed aluminum heat exchangers and reduce assembly steps by 30%. China’s GB 38031 flame-retardancy rule for battery housings, effective January 2025, concentrated demand on phosphorus-based additive packages and lifted polyamide 6 shipments by 28% during 1H 2025. Thermal-runaway mitigation continues to open niche volume for polyetherimide films boasting limiting-oxygen indices above 47%, reinforcing the engineering plastics market trajectory.

Asia-Pacific Manufacturing Migration

Foreign direct investment worth USD 4.7 billion flowed into Southeast-Asian compounding ventures in 2025, as firms diversified supply chains out of single-country exposure. Thailand’s Board of Investment cleared 22 engineering-plastics plants totaling USD 890 million, including Mitsubishi Chemical’s 60,000 tpa polyamide line. Vietnam captured Hyosung’s USD 385 million PA-66 salt complex set for 2027 service. India’s Production-Linked Incentive scheme disbursed USD 1.2 billion to electronics assemblers, catalyzing 45,000 tpa incremental demand for polycarbonate and ABS. Japanese automakers shifted compounding capacity into Thailand and Indonesia, evidenced by a 19% drop in Japan-to-China polyamide exports in 2025. This manufacturing dispersion anchors supply security yet forces resin majors to deploy multi-country technical-service hubs, driving service-based differentiation inside the engineering plastics market.

EV Battery Module Housings Adoption

Thermoplastic enclosures are advancing on aluminum trays in mid-range and premium EVs. LyondellBasell’s Celstran long-fiber PA achieved a 35% weight reduction versus aluminum in a 75 kWh pack fielded by a European OEM in 2024 and now underpins three additional 2026-2027 vehicle launches. Teijin’s carbon-fiber-reinforced polycarbonate trays, produced under a 2024 JV with China Shipbuilding Industry Corp., cut module mass by 1.8 kg, an attractive delta for luxury brands. Regulatory divergence persists: South Korea’s MOLIT adopted UL 94 V-0 for housings in 2025, whereas China’s GB 38031 specifies a stricter vertical-burn rate, compelling dual formulations. Design integration remains a bonus; molded-in coolant channels remove brazed cold plates, trimming bill-of-material cost by USD 18-22 per module. Polyamide 6T/6I copolymers withstand 160 °C continuous exposure, supporting under-hood battery placement in hybrid architectures and extending the engineering plastics market envelope.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Monomer Price Volatility | -0.7% | Global, acute in Asia-Pacific due to feedstock concentration | Short term (≤ 2 years) |

| Packaging Regulations Tightening | -0.4% | Europe and North America, early adoption in select APAC markets | Medium term (2-4 years) |

| Fluorspar-Linked Fluoropolymer Shortage | -0.3% | Global semiconductor and aerospace supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Monomer Price Volatility

Feedstock swings undermine margin stability. Benzene spot quotes in Asia oscillated between USD 850 and USD 1,320 per t during 2025, mirroring refinery outages in South Korea and China’s styrene surges. Caprolactam fluctuated from USD 1,450 to USD 1,980 per t in Europe as natural-gas and ammonia supplies tightened amid regional conflicts. China commissioned 1.2 million t of adipic-acid capacity between 2023-2025, but demand lagged, driving prices down 18% and squeezing integrated PA-66 producers. Contract clauses now reset quarterly against naphtha benchmarks, yet smaller compounders lack hedging muscle, swallowing 8-12% margin erosion during rallies. Larger players such as BASF shelter behind captive adiponitrile and cyclohexane, further tilting competitive dynamics within the engineering plastics market.

Packaging Regulations Tightening

The EU’s 2024 Packaging and Packaging Waste Regulation mandates 30% recycled content in beverage containers by 2030, capping virgin-PET draw in bottles[2]European Commission, “Packaging and Packaging Waste Regulation 2024,” europa.eu . Germany’s deposit-return expansion lifted PET collection to 96% within six months, eliminating 85,000 tpa of virgin demand. California’s SB 54 imposes 25% PCR in single-use packaging by 2032, adding EPR fees that pull brand owners toward chemical recycling despite cost premiums. Food-grade rPET yields linger at 60-70% due to contamination, creating structural shortages and price inversions with virgin resin. Polycarbonate baby-bottle bans in several U.S. states diverted 12,000 tpa into durable goods, underscoring how health concerns can abruptly shift end-use patterns and moderate engineering plastics market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: PET Dominance Meets Fluoropolymer Surge

Polyethylene terephthalate captured 50.15% of 2025 volume, bolstered by bottle and fiber consumption that anchored the engineering plastics market size at 65.53 million tons. Deposit-return schemes and recycled-content mandates are set to temper virgin PET growth, yet chemical-recycling rollouts mitigate potential volume loss. Fluoropolymers will post the fastest expansion at 7.45% CAGR in the engineering plastics market size by 2031. EUV lithography tools incorporate 2.8 kg of PTFE seals per scanner, accumulating incremental demand by 2027. PVDF’s piezoelectricity spurs adoption in automotive ultrasonic sensors, with Arkema logging a 34% shipment rise in 2025. However, Europe’s proposed PFAS ban could fence off non-critical PTFE cable coatings, compelling formulators to pivot toward high-temperature polyamides. Bio-based PA-11 secures premium niches in sports gear where sustainability labels command margin upside. Polycarbonate advances in panoramic sunroofs after Covestro’s Makrolon Rx4 met ECE R43 transparency and impact standards, illustrating ongoing diversification within the engineering plastics market.

Continued demand for polyoxymethylene gears, polyimide films, and liquid-crystal-polymer connectors stabilizes the high-performance tier even as aggregate volume stays below 2%. DuPont’s Delrin 527UV moved exterior trim away from glass-filled PA, capturing a 12,000 t addressable window in 2025. Styrene copolymers maintain appliance and electronics relevance, with INEOS Styrolution’s 15,000 t ABS recycling line yielding food-contact pellets for refrigerator shells. The diversified resin mix cushions the engineering plastics industry against single-material regulatory shocks while encouraging multipronged R&D agendas.

By End-user Industry: Electronics Outpaces Packaging

Packaging absorbed 50.66% of 2025 demand, yet tightening European and Californian statutes cap virgin draw, slowing segment growth. Electrical and electronics is on course for a 7.01% CAGR through 2031, fortifying its share of the engineering plastics market size. Nvidia’s GB200 AI server dissipates 1,200 W per GPU and relies on polyamide 9T connectors tested to 180 °C. Liquid-crystal polymers, prized for stable dielectric constants above 60 GHz, grew 41% in telecom base-station connectors as Ericsson populated Southeast Asian networks with 28 GHz radios. Automotive is expanding as hybrid and full-electric models standardize polyamide 6T manifold covers and polycarbonate glazing.

Aerospace and defence drives material specification trends; 1,340 commercial-aircraft deliveries in 2025 consumed 300 kg of engineering plastics apiece. Building and construction is on the back of infrastructure stimulus in Italy and Spain, leveraging recycled-content PC panels that feed into smart-city guidelines. Industrial machinery’s automation wave keeps POM gears and PA bushings on a steady incline, while niche categories like medical devices and sports equipment harvest high-margin bio-based resins, underscoring the breadth of opportunity across the engineering plastics market.

Geography Analysis

Asia-Pacific anchored 55.78% of 2025 volume, powered by China’s 9.4 million-unit NEV output and India’s USD 1.2 billion electronics subsidy that together contributed 5.44% CAGR to regional growth. BYD alone consumed 42,000 t of in-house compounded polyamide and polycarbonate during 2025, signaling OEM vertical integration. Japan’s exports slipped 11% as capacity relocated to Thailand and Vietnam, aided by ASEAN incentives. South Korea held production flat, prioritizing specialty grades. FDI totaling USD 4.7 billion financed Thai and Vietnamese compounding nodes, reshaping intraregional trade.

North America is steady yet tempered by the United States’ 9.2% BEV sales penetration. Covestro’s USD 450 million Baytown PC expansion, slated for 2027, aligns with Inflation Reduction Act content thresholds and positions Gulf Coast producers for downstream EV and solar opportunities. Mexico’s 14% rise in automotive parts exports to the U.S. lifted PA and ABS throughput in Nuevo León clusters. Canada’s aerospace recovery, driven by Bombardier Global 7500 production, nudged national demand up 4.3%.

In Europe, high energy costs and REACH compliance dragged German polyamide usage lower in 2025. France benefited from Airbus ramp-ups, while the U.K. leveraged post-Brexit trade pacts to import Asian resins at reduced tariffs, prompting INEOS to idle Scottish ABS capacity. Italy and Spain enjoyed resilience on EU-funded infrastructure requiring recycled-content PC glazing. Sanction-hit Russia slid 5.4% as OEMs substituted premium imports with local PA and PC.

South America and the Middle-East and Africa combined for smaller share. Brazil’s 2.4 million vehicle build lifted regional PA demand, whereas Argentina contracted amid macro shocks. Saudi Arabia exported 140,000 t of PC and ABS into Europe and Asia, exploiting low-cost ethylene. The UAE’s Jebel Ali hub re-exported 95,000 t toward East Africa and South Asia, underlining Gulf logistics leverage. South Africa’s localized sourcing mandates lifted domestic engineering plastics market usage substantially.

Competitive Landscape

Global capacity remains low concentrated, with BASF, Covestro, DuPont, SABIC, and Celanese sharing 32%. Envalior, birthed from DSM and Lanxess in 2024, wields EUR 3.85 billion in sales and chases EUR 120 million cost synergies by 2027. BASF’s backward integration into adiponitrile and caprolactam insulated earnings during 2025’s feedstock turbulence and delivered a 140-basis-point gain in polyamide share. SABIC’s collaboration with Plastic Energy supplied 14,000 t of pyrolysis oil to European crackers, yielding certified-circular PC and ABS at 10-15% premiums. Arkema scaled bio-based PA-11 while Victrex earned AS9100D for PEEK filament, legitimizing aerospace additive manufacturing. Patent filings for halogen-free flame retardants rose 23% in 2025, pointing to future differentiation channels as environmental scrutiny intensifies across the engineering plastics industry. Smaller compounders continue to chase regional niches, yet rising compliance costs and feedstock volatility encourage consolidation or strategic alliances.

Engineering Plastics Industry Leaders

SABIC

BASF

DuPont

Covestro AG

Celanese Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Covestro AG launched new post-consumer recycled (PCR) polycarbonate products derived from end-of-life headlamps and expanded its range of low-carbon medical-grade polycarbonates under the Makrolon RE brand. The automotive-grade materials were certified by TÜV Rheinland.

- September 2024: LOTTE Chemical Corporation invested more than 300 billion KRW to establish Korea's largest single compounding plant in the Yulchon Industrial Complex, Jeollanam-do, with operations planned for 2026. The facility had an initial capacity of 500,000 tons, expandable to 700,000 tons, focusing on high-value Super Engineering Plastics (Super EP) such as PPS and LCP, catering to the automotive, IT, and home appliance markets.

Global Engineering Plastics Market Report Scope

Engineering plastics are high-performance thermoplastics characterized by superior mechanical, thermal, and chemical resistance compared to commodity plastics. They are designed for structural, long-term, and high-stress applications and are often used as substitutes for metal, glass, or ceramics due to their durability, strength, and reduced weight.

The engineering plastics market is segmented by resin type, end-user industry, and geography. By resin type, the market is segmented into polyethylene terephthalate (PET), fluoropolymer, liquid crystal polymer (LCP), polyamide (PA), polybutylene terephthalate (PBT), polycarbonate (PC), polyether ether ketone (PEEK), polyimide (PI), polymethyl methacrylate (PMMA), polyoxymethylene (POM), and styrene copolymers (ABS, SAN). By fluoropolymer, the market is further segmented into ethylenetetrafluoroethylene (ETFE), fluorinated ethylene-propylene (FEP), polytetrafluoroethylene (PTFE), polyvinylfluoride (PVF), polyvinylidene fluoride (PVDF), and other sub-resin types. By polyamide (PA), the market is further segmented into liquid crystal polymer (LCP), polyamide (PA), aramid, polyamide (PA) 6, polyamide (PA) 66, and polyphthalamide. By end-user industry, the market is segmented into packaging, aerospace, automotive, building and construction, electrical and electronics, industrial and machinery, and other end-user industries. The report also covers the market size and forecasts for engineering plastics in 20 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

By Resin Type

| Polyethylene Terephthalate (PET) | |

| Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinylfluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub Resin Types | |

| Liquid Crystal Polymer (LCP) | |

| Polyamide (PA) | Aramid |

| Polyamide (PA) 6 | |

| Polyamide (PA) 66 | |

| Polyphthalamide | |

| Polybutylene Terephthalate (PBT) | |

| Polycarbonate (PC) | |

| Polyether Ether Ketone (PEEK) | |

| Polyimide (PI) | |

| Polymethyl Methacrylate (PMMA) | |

| Polyoxymethylene (POM) | |

| Styrene Copolymers (ABS, SAN) |

By End-user Industry

| Packaging |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Resin Type | Polyethylene Terephthalate (PET) | |

| Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) | |

| Fluorinated Ethylene-propylene (FEP) | ||

| Polytetrafluoroethylene (PTFE) | ||

| Polyvinylfluoride (PVF) | ||

| Polyvinylidene Fluoride (PVDF) | ||

| Other Sub Resin Types | ||

| Liquid Crystal Polymer (LCP) | ||

| Polyamide (PA) | Aramid | |

| Polyamide (PA) 6 | ||

| Polyamide (PA) 66 | ||

| Polyphthalamide | ||

| Polybutylene Terephthalate (PBT) | ||

| Polycarbonate (PC) | ||

| Polyether Ether Ketone (PEEK) | ||

| Polyimide (PI) | ||

| Polymethyl Methacrylate (PMMA) | ||

| Polyoxymethylene (POM) | ||

| Styrene Copolymers (ABS, SAN) | ||

| By End-user Industry | Packaging | |

| Aerospace | ||

| Automotive | ||

| Building and Construction | ||

| Electrical and Electronics | ||

| Industrial and Machinery | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Market Definition

- End-user Industry - Packaging, Electrical & Electronics, Automotive, Building & Construction, and Others are the end-user industries considered under the engineering plastics market.

- Resin - Under the scope of the study, consumption of virgin resins like Fluoropolymer, Polycarbonate, Polyethylene Terephthalate, Polybutylene Terephthalate, Polyoxymethylene, Polymethyl Methacrylate, Styrene Copolymers, Liquid Crystal Polymer, Polyether Ether Ketone, Polyimide, and Polyamide in the primary forms are considered. Recycling has been provided separately under its individual chapter.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms