Viscose Staple Fiber Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

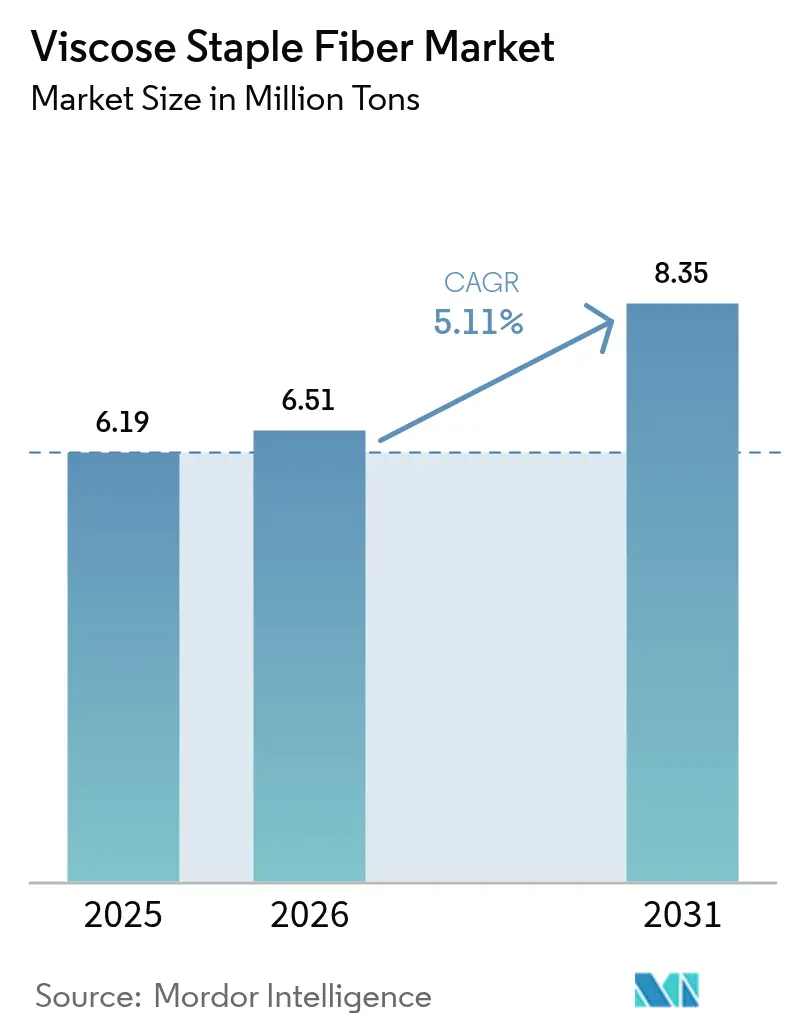

| Market Volume (2026) | 6.51 Million tons |

| Market Volume (2031) | 8.35 Million tons |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

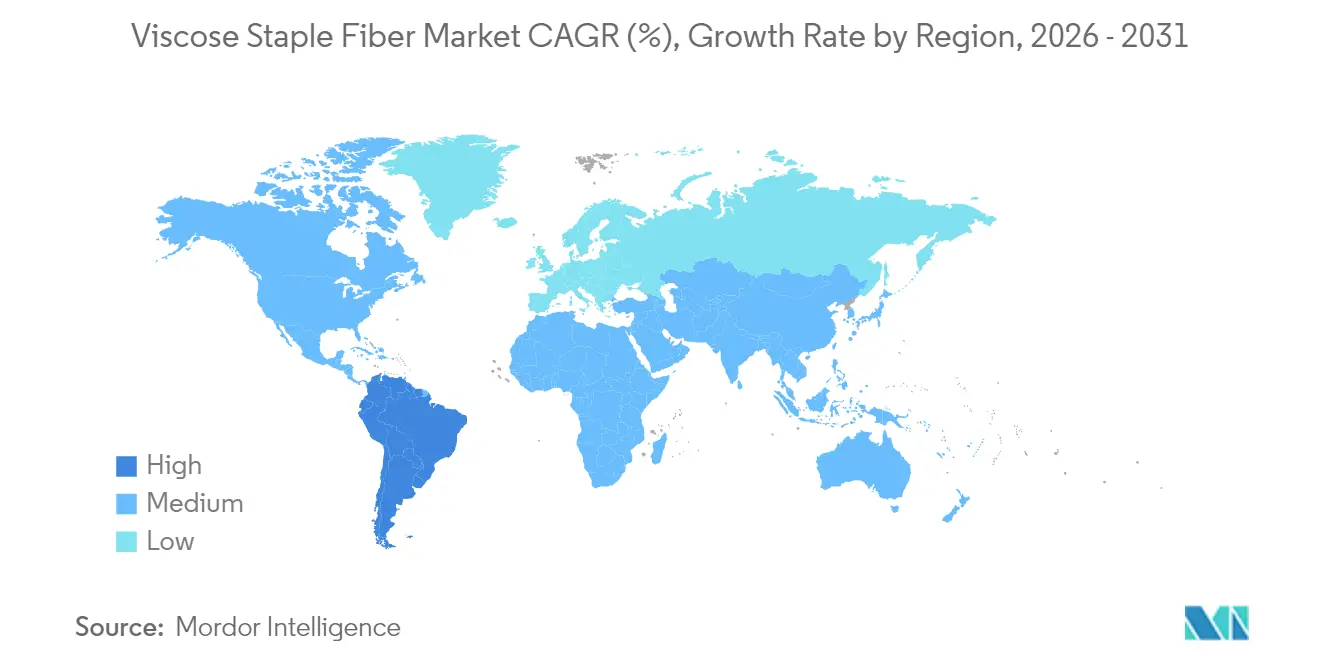

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Viscose Staple Fiber Market Analysis by Mordor Intelligence

The Viscose Staple Fiber Market size in 2026 is estimated at 6.51 million tons, growing from 2025 value of 6.19 million tons with 2031 projections showing 8.35 million tons, growing at 5.11% CAGR over 2026-2031. This growth trajectory reflects the sector’s ability to navigate dissolving-pulp price swings, capitalize on cotton volatility, and align with fast-fashion supply timelines. The viscose staple fibre market benefits from integrated Asian supply chains that pair proximate pulp sources with large spinning capacities, giving regional producers a structural cost edge. Demand resilience also stems from increased specialty fiber adoption in medical and hygiene products that offset cyclical apparel spending shifts. Intensifying sustainability mandates in North America and Europe reward closed-loop technologies, nudging premium buyers toward suppliers with certified low-emission operations.

Key Report Takeaways

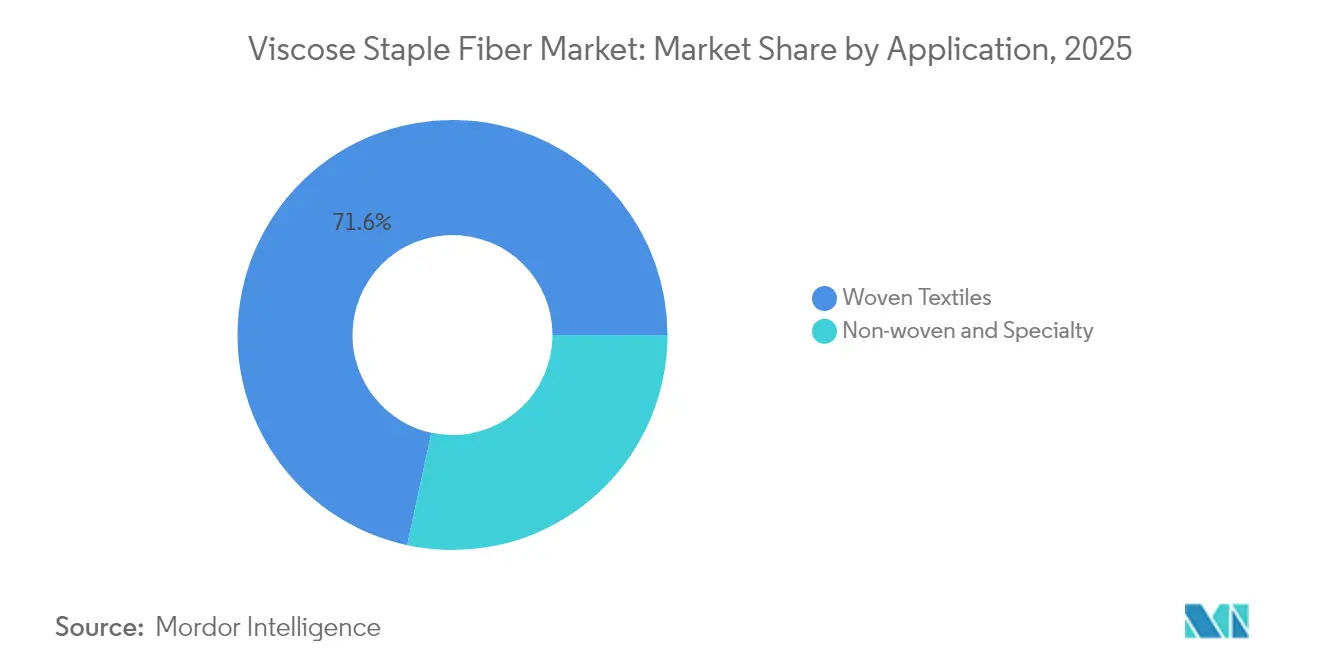

- By application, woven textiles led with 71.62% of the viscose staple fibre market share in 2025; non-woven and specialty applications are advancing at a 6.26% CAGR through 2031.

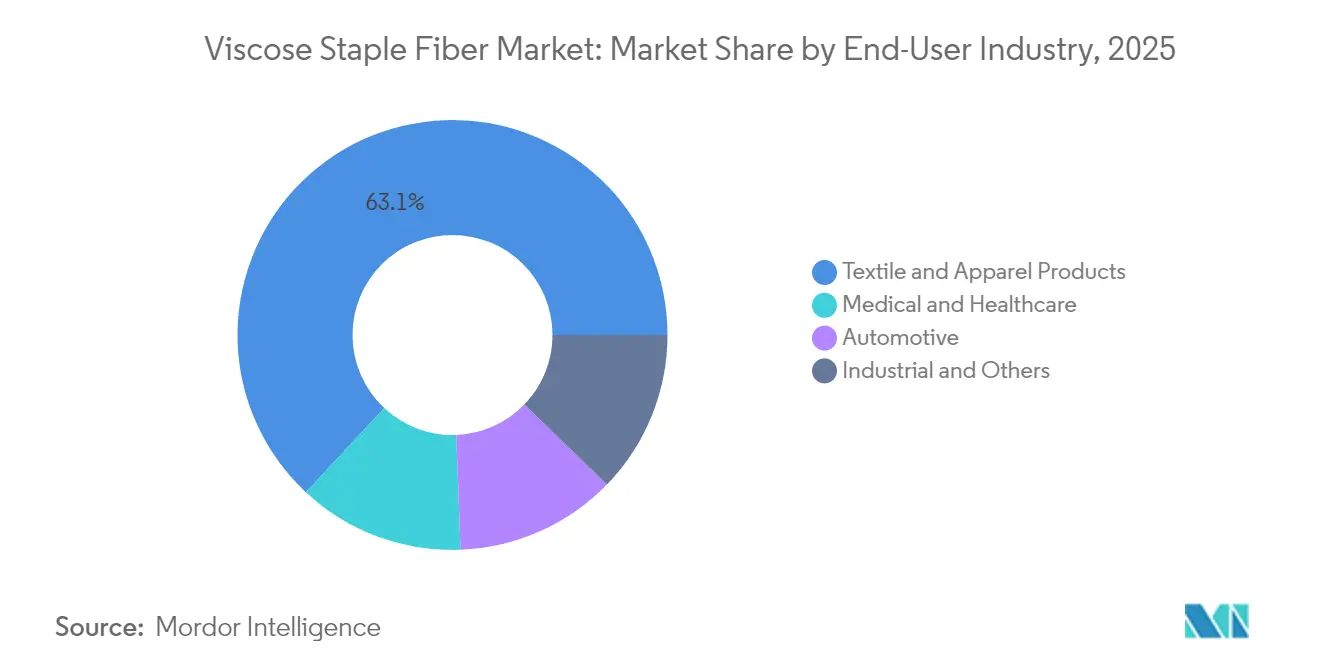

- By end-user industry, textile and apparel products held 63.05% of the viscose staple fibre market share in 2025, while medical and healthcare are projected to grow at a 6.79% CAGR through 2031.

- By geography, Asia-Pacific accounted for a 52.10% share of the viscose staple fibre market size in 2025, and South America is set to expand at a 6.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Viscose Staple Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for apparel and clothing | +1.8% | Global, APAC core | Medium term (2-4 years) |

| Cotton-price volatility favouring viscose | +1.2% | Global, price-sensitive markets | Short term (≤ 2 years) |

| Expansion of fast-fashion manufacturing in the Asia-Pacific | +0.9% | APAC, Southeast Asia spill-over | Medium term (2-4 years) |

| Surge in hygiene and wipes non-wovens blending | +0.7% | North America and EU lead | Long term (≥ 4 years) |

| Textile-to-pulp recycling enabling circular feedstock | +0.5% | EU and North America early, APAC scaling | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Apparel and Clothing

Global apparel consumption is still climbing, and viscose continues to win share from both cotton and synthetics. Retailers favor the fiber’s moisture management, drape, and dye uptake that help deliver premium aesthetics at mid-tier price points. Fast-fashion chains leverage viscose to replicate natural-fiber looks inside compressed design-to-shelf cycles. Limited U.S. spinning capacity redirected incremental volumes toward Asian mills, underscoring regional supply imbalances. Consumers newly focused on comfort and affordability increasingly choose viscose-rich blends, sustaining baseline demand even as discretionary spending ebbs.

Cotton-Price Volatility Favouring Viscose

Cotton prices swung sharply during 2024. Such volatility complicates seasonal cost planning and pushes mills toward the relative stability of wood-based viscose staple fibre market contracts. Concurrent dissolving-pulp price relief has widened viscose’s cost advantage, encouraging mills to lock in longer-term supply. Weather risks, land-use competition, and policy shifts continue to inject uncertainty into cotton supply, strengthening viscose’s hedge role in fiber portfolios.

Expansion of Fast-Fashion Manufacturing in the Asia-Pacific

Asia-Pacific’s fast-fashion network now couples design hubs, fabric mills, and garment factories within tightly integrated clusters that can ship new styles in weeks. Investments like Syre’s upcoming textile-to-textile recycling plant in Vietnam illustrate capital inflows that deepen the region’s vertical breadth[1]Syre, “Syre Raises USD 100 Million Series A,” syre.com. China’s Xinjiang smart-spinning complex, backed by CNY 2 billion, enhances local throughput and automation efficiency. These capabilities cement APAC’s primacy in the viscose staple fibre market by shortening lead times and concentrating capacity close to feedstock sources.

Surge in Hygiene and Wipes Non-Wovens Blending

Rising consumer demand for plastic-free personal-care products accelerates viscose substitution in wipes, diapers, and feminine-care pads. Lenzing’s LENZING Lyocell Dry fiber achieves a water contact angle above 100° after one hour, enabling hydrophobic acquisition layers that rival polypropylene[2]Lenzing, “Lenzing Expands LENZING™ Lyocell Dry Fiber Portfolio,” lenzing.com. EU Single-Use Plastics rules and North American retailer packaging targets boost acceptance of biodegradable cellulosic fibers. Medical textile makers also prize viscose for its inherent softness and microbial resistance, supporting growth in specialized wound dressings and surgical drapes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from synthetics | -0.8% | Global, price-sensitive segments | Medium term (2-4 years) |

| Stricter CS₂ emission regulations | -0.6% | EU and North America lead | Long term (≥ 4 years) |

| Dissolving pulp supply bottlenecks | -0.4% | Global, regional variance | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from Synthetics

Polyester and spandex producers discount aggressively to defend mass-market shares, and recycled PET yarns now carry sustainability labels that challenge viscose’s natural image. The spandex segment is growing, reflecting synthetics’ ability to tap niche performance niches. Established hydrocarbon feedstock chains lend price stability that resonates with value retailers, although environmental scrutiny of microplastics tempers the advantage.

Stricter CS₂ Emission Regulations

EU Best Available Techniques for sulfur emissions oblige viscose mills to install closed-loop systems or risk market exclusion. Birla Cellulose’s compliance blueprint demonstrates the capex burden required to align with the upcoming norms. Smaller standalone mills face disproportionate costs that could trigger capacity rationalization, especially in regions adopting EU-linked environmental trade standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Woven Textiles Anchor Volumes While Specialty Segments Accelerate

The woven textiles segment accounted for 71.62% of the viscose staple fiber market volume in 2025, reflecting entrenched apparel and home-textile processing capacity across the Asia-Pacific. Strong drape, breathability, and vibrant dye profiles keep viscose woven fabrics central to shirts, dresses, and bed linens. Although overall apparel demand normalizes, cost-conscious brands still specify viscose blends to manage ticket prices and maintain premium aesthetics.

Although smaller today, specialty non-woven uses post a 6.26% CAGR as hygiene and medical grades gain traction. Hydrophobic viscose innovations allow diaper acquisition layers and fem-care topsheets once dominated by polypropylene. Medical device firms adopt viscose for absorbent wound pads and single-use surgical covers where biodegradability and skin compatibility outweigh slightly higher costs. Over the forecast horizon, non-wovens’ faster growth gradually chips away at woven’s share but does not displace its volumetric leadership.

By End-User Industry: Healthcare Growth Outpaces Traditional Apparel Dominance

Textile and apparel retained 63.05% of the viscose staple fiber market share in 2025, buoyed by fast-fashion reorder cycles and value-tier brand expansions. Integrated Asian clusters supply mass-market retailers in compressed lead times, reinforcing viscose as a fixture of global apparel sourcing matrices.

Conversely, medical and healthcare demand expands at 6.79% CAGR as hospitals and wound-care brands seek fibers meeting stringent purity and biocompatibility benchmarks. Aging populations in the U.S., EU, and Japan, alongside rising care standards in emerging regions, raise volumes of disposable medical drapes, gauzes, and hygiene wipes that rely on high-purity viscose. Producers targeting this niche secure higher margins through specialty grade certifications, partially insulating revenue from apparel’s cyclical swings.

Geography Analysis

Asia-Pacific commanded 52.10% of global volume in 2025, anchored by China’s integrated pulp-to-fiber complexes and deep downstream weaving and garment industries. Domestic viscose output tops the global capacity, providing local converters with predictable access to fiber and enabling aggressive export pricing. Southeast Asian nations such as Indonesia and Vietnam add incremental scale, with Vietnam’s planned recycling facilities signaling a shift toward circular supply within the bloc. Robust logistics corridors and government support for textile hubs sustain APAC’s primacy through 2031.

While representing a smaller base, South America delivers the fastest regional CAGR at 6.12% through 2031. Brazil’s expanding knitwear mills and improved intra-regional trade pacts underpin capacity additions. Rising disposable income prompts domestic substitution of cotton with viscose in value apparel segments. Although still dependent on imported pulp and fiber, local stakeholders explore joint ventures to reduce freight costs and hedge currency volatility.

North America and Europe display mature, steady demand profiles, yet their regulatory environment wields outsized influence on global production standards. EU carbon and emission rules compel mills worldwide to invest in scrubbers, solvent recovery, and certified sustainable forestry. North American brand sustainability scorecards increasingly mandate traceability for pulp origin and closed-loop processing. These expectations elevate the competitive standing of technologically advanced mills even if absolute consumption grows modestly.

Competitive Landscape

The viscose staple fibre industry is moderately fragmented, with integrated producers using scale and technology to sustain leadership. Asian incumbents continue expanding; Sinopec Yizheng’s 3 million t PTA complex in Jiangsu strengthens upstream integration for regional viscose yarn producers. Competitive intensity increasingly hinges on sustainability credentials rather than pure tonnage. Mills demonstrating low CS₂ emissions, FSC-certified wood sourcing, and recycled feedstock capacities enjoy preferential access to European and North American brands. Conversely, smaller standalone facilities without solvent-recovery upgrades face margin compression or potential shutdowns as regulatory thresholds tighten.

Viscose Staple Fiber Industry Leaders

Lenzing AG

Grasim Industries Limited (Aditya Birla Group)

Sateri

Tangshan Sanyou Xingda Chemical Fiber CO.,Ltd

Xinjiang Zhongtai Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Jilin Chemical Fibre Group launched commercial-scale production of Reboocel, a staple fiber made from 70% FSC-certified bamboo and 30% recycled bamboo, targeting 30,000 tons annually as part of its push for sustainable man-made cellulosic fibre (MMCF) solutions. Furthermore, the company will enhance the output of Jirecell, its viscose filament yarn, which is made of 70% FSC-certified wood and 30% recycled cotton Circulose pulp, targeting an annual production capacity of 10,000 tons.

- February 2024: Tangshan Sanyou Xingda Chemical Fiber CO., Ltd’s three viscose staple fiber plants have once again passed the EU BAT audit, confirming their compliance with top-tier environmental standards and reinforcing the company’s commitment to clean production and sustainable MMCF practices.

Global Viscose Staple Fiber Market Report Scope

A viscous fiber is a type of fiber that has a high resistance to flow. This fiber is often used in textiles and clothing to provide comfort and breathability. Viscous fibers are also known for wicking moisture away from the skin, which can help keep the wearer cool and comfortable. Viscose staple fibers are biodegradable cotton-like fibers. They are made from wood pulp and cotton pulp. The viscose staple fiber market is segmented by application and geography. By application, the market is segmented into woven and non-woven and specialty. The report also covers the market sizes and forecasts for the viscose staple fiber market in 13 countries across the central regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Woven Textiles |

| Non-woven and Specialty |

| Textile and Apparel Products |

| Medical and Healthcare |

| Automotive |

| Industrial and Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Woven Textiles | |

| Non-woven and Specialty | ||

| By End-user Industry | Textile and Apparel Products | |

| Medical and Healthcare | ||

| Automotive | ||

| Industrial and Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global volume for viscose staple fibre by 2031?

Global demand is forecast to reach 8.35 million tons by 2031, expanding at a 5.11% CAGR from 2026 to 2031.

Which region currently dominates viscose staple fibre consumption?

Asia-Pacific leads with 52.10% of global volume from integrated pulp-to-garment supply chains.

Why are hygiene non-wovens a high-growth outlet for viscose?

Regulatory pressure against single-use plastics and innovations like hydrophobic Lyocell Dry fibers are boosting adoption in wipes and diapers.

How do dissolving pulp price movements influence fiber economics?

A slide from USD 740 to USD 590 per ton in 2024 lowered input costs, strengthening viscose staple fibre margins relative to cotton.

What sustainability measures differentiate leading viscose producers?

Technologies that capture and recycle CS₂, use certified wood sources, and incorporate textile-waste feedstock secure preferential access to brands and regulators.

Page last updated on: