Pneumatic Cylinder Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

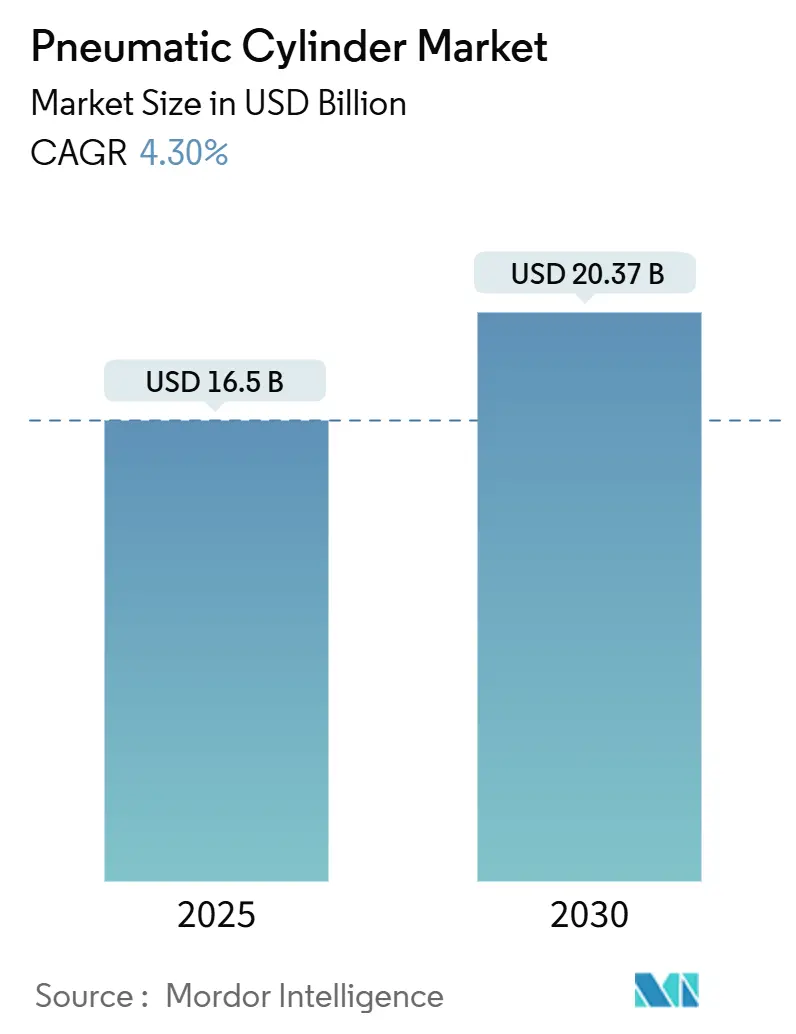

| Market Size (2025) | USD 16.5 Billion |

| Market Size (2030) | USD 20.37 Billion |

| Growth Rate (2025 - 2030) | 4.30% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pneumatic Cylinder Market Analysis by Mordor Intelligence

The pneumatic cylinder market size stands at USD 16.5 billion in 2025 and is forecast to reach USD 20.37 billion by 2030, reflecting a 4.30% CAGR over the period. Robust investment in low-cost factory automation, retrofitting of brown-field plants, and the transition to energy-efficient compressed-air systems underpin this outlook. The Asia-Pacific region leads demand, while North America’s reshoring programs drive the fastest regional growth. Double-acting products keep volume leadership, yet smart cylinders with integrated sensors outpace all other categories. Moderate industry consolidation and sustained research and development spending by leading brands signal an innovation-led competitive environment.

Key Report Takeaways

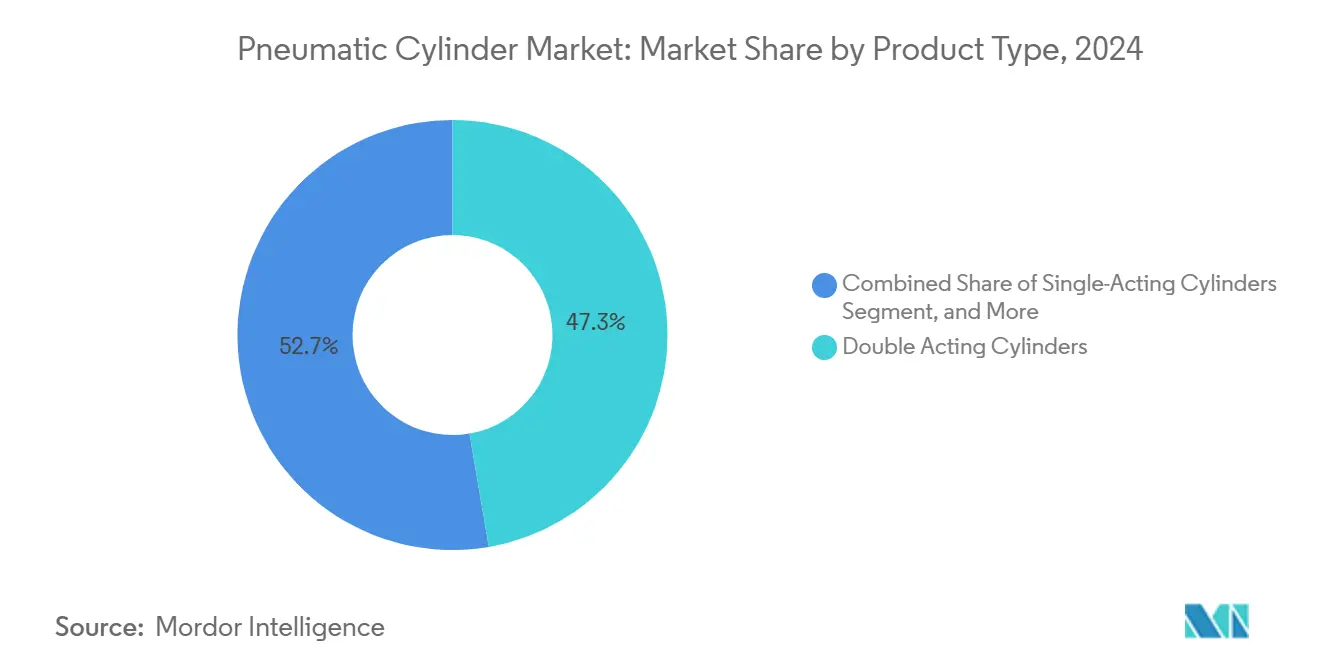

- By product category, double-acting units accounted for 47.3% of pneumatic cylinder market share in 2024, whereas smart/integrated-sensor cylinders are projected to expand at a 4.5% CAGR through 2030.

- By motion type, linear designs accounted for 82.3% of the pneumatic cylinder market size in 2024, and rotary variants are forecast to register a 5.1% CAGR between 2025 and 2030.

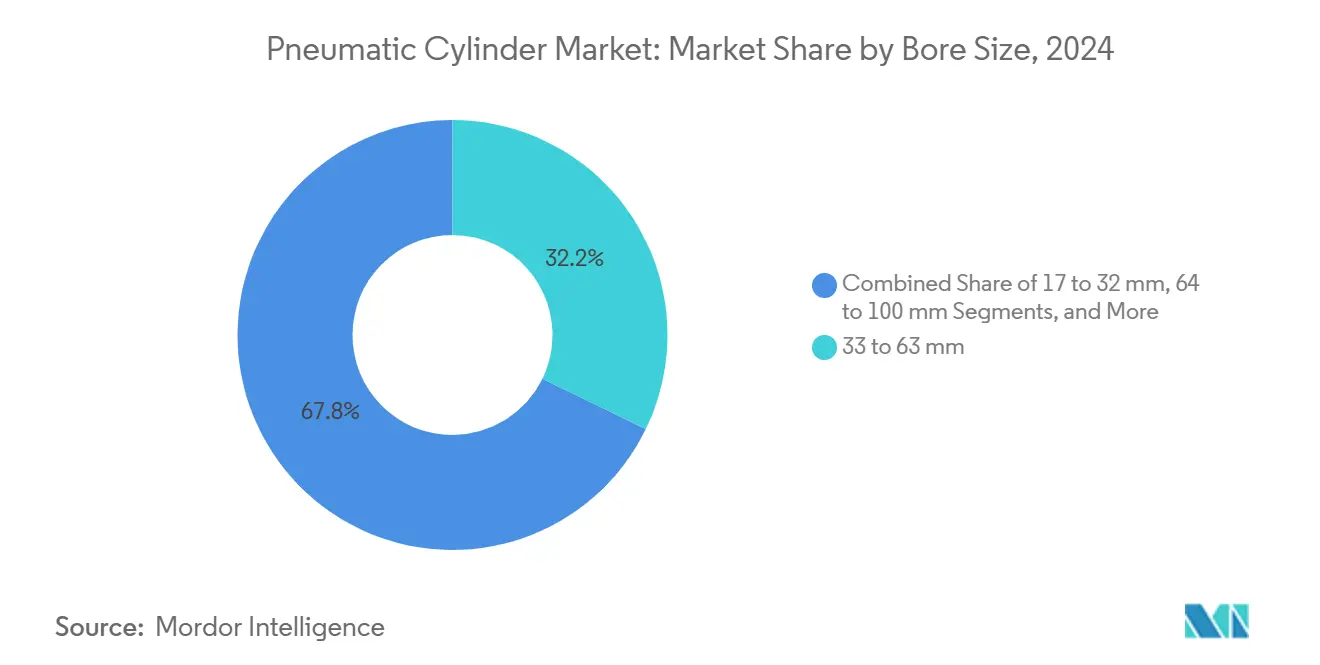

- By bore size, the 33–63 mm class held a 32.2% revenue share in 2024; micro cylinders (≤16 mm) represent the fastest-growing tier, with a 5.2% CAGR to 2030.

- By end-user industry, industrial automation and machinery led with a 25.6% share of the pneumatic cylinder market size in 2024, while the food and beverage processing sector posted the highest 5.8% CAGR through 2030.

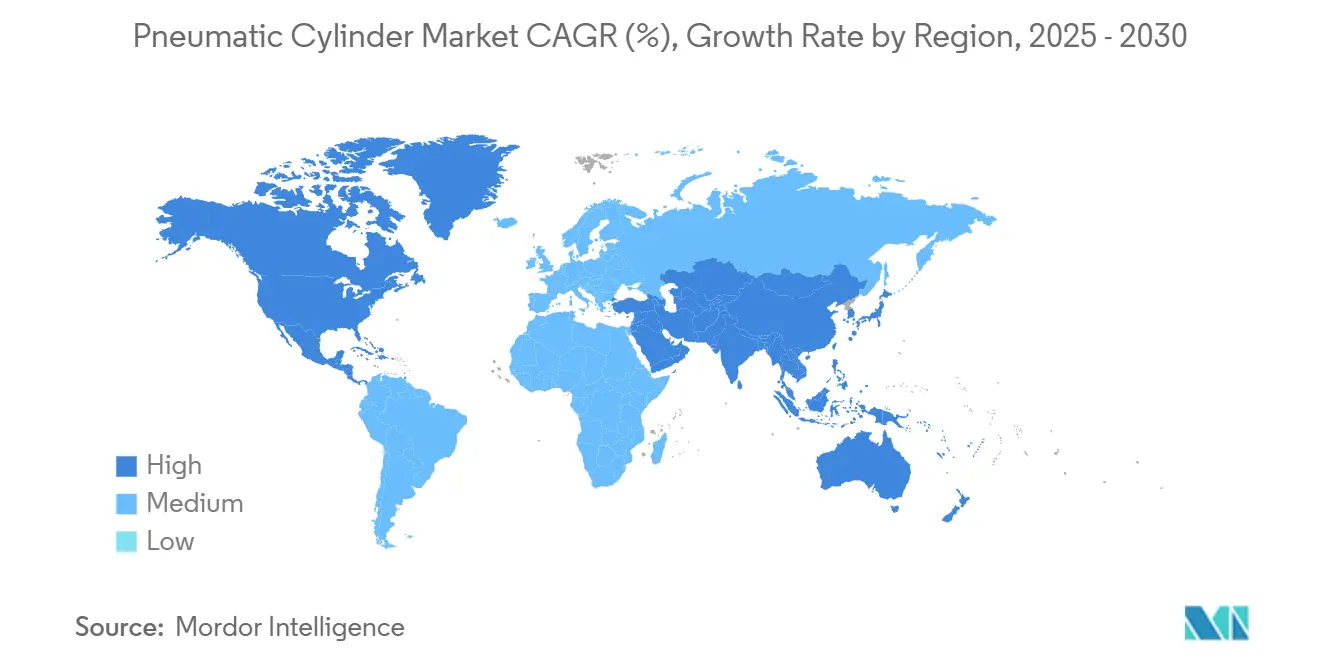

- By geography, Asia-Pacific retained a 39.30% share in 2024; North America is set to grow at a 6.10% CAGR over 2025-2030.

Global Pneumatic Cylinder Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in Low-Cost, High-Speed Factory Automation Projects | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Energy-Efficient Compressed-Air Systems Lowering Lifetime TCO | +0.8% | North America, Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Retrofitting Demand in Brown-Field Smart-Factory Upgrades | +0.7% | Europe, North America, and selective Asia-Pacific | Medium term (2-4 years) |

| Rapid Expansion of E-Commerce Fulfilment Centres | +0.6% | Global, led by North America and China | Short term (≤ 2 years) |

| Miniaturisation Enabling New Medical-Device Use-Cases | +0.4% | North America, Europe, premium Asia-Pacific | Long term (≥ 4 years) |

| Emergence of Oil-free Cylinders for Clean-Room Operations | +0.3% | Pharmaceutical and food hubs worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Low-Cost, High-Speed Factory Automation Projects

Affordable robotics kits and modular conveyors let small and midsize manufacturers automate packaging, palletizing, and pick-and-place workstations at previously unattainable price points. Pneumatic cylinders remain the preferred drive element for rapid, repetitive strokes where force requirements are moderate, and cycle times are measured in milliseconds. Their lightweight design eases robot arm payload limits, while simple maintenance suits resource-constrained factories. Vendors such as SMC forecast heightened demand for palletizing and machine-tending applications as AI-driven vision systems coordinate higher-speed manipulation tasks.[1]Source: SMC Corporation of America, “Company,” smcusa.com The democratization of automation, therefore, sustains baseline growth in both developed and emerging economies.

Energy-Efficient Compressed-Air Systems Lowering Lifetime TCO

Compressed air often accounts for 10-15% of a plant’s total electricity bill, making efficiency upgrades financially compelling. Intelligent air-management modules now capture pressure, flow, and temperature data in real time, feeding analytics that pre-empt leaks and load mismatches. IMI Norgren reports 50% energy savings with integrated valve-actuator packages versus conventional plumbing.[2]Source: IMI Norgren, “IVAC Cylinders,” norgren.com As corporate net-zero pledges intensify, the resulting drop in total cost of ownership keeps pneumatics in capital-equipment budgets even when electric rivals promise higher precision.

Retrofitting Demand in Brown-Field Smart-Factory Upgrades

Legacy plants rely on existing compressor networks yet still seek data visibility and closed-loop control. IO-Link sensors embedded in cylinders relay stroke counts, velocity, and internal pressure without disturbing the core mechanical layout. Festo’s adoption of PLCnext Technology embeds cybersecurity-ready controllers inside valve terminals, delivering deterministic control plus cloud connectivity for predictive maintenance.[3]Source: Phoenix Contact, “PLCnext Technology Partnership,” phoenixcontact.comPhased retrofits, therefore, help manufacturers de-risk digitalization and stretch asset life.

Rapid Expansion of E-Commerce Fulfilment Centres

Surging parcel volumes push warehouse operators to install automated sorters, AMRs, and high-throughput packaging lines. Cylinders, power pusher arms, case erectors, and flap folders are used because of their high speed and tolerance for dusty environments. Flow-optimized valve manifolds paired with vision systems now achieve up to 300 cartons per minute on compact footprints, supporting the just-in-time logistics model. Short project cycles in e-commerce favor proven pneumatics that scale quickly with minimal commissioning time.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatility in Industrial Compressed-Air Energy Prices | -0.6% | Global; acute in power-cost-sensitive regions | Short term (≤ 2 years) |

| Competition from Electro-Mechanical Actuators in Precision Tasks | -0.9% | North America, Europe, premium Asia-Pacific | Long term (≥ 4 years) |

| Supply-Chain Tightness in High-Grade Aluminium and Seals | -0.4% | Major manufacturing hubs | Medium term (2-4 years) |

| Ambient-Noise Regulations Limiting Plant Pneumatic Adoption | -0.3% | Urban industrial zones in North America and the Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Industrial Compressed-Air Energy Prices

Spot electricity rates rose sharply in 2024-2025, exposing energy-intensive plants to margin risk and delaying some capex for new pneumatic lines. In California, compressors consumed over 12% of statewide manufacturing electricity, magnifying exposure to rate swings. Metal-price inflation for cylinder tubes and end caps compounded cost pressures. OEMs replied with higher-efficiency compressors and leak-detection audits, yet budget uncertainty constrained near-term order cycles.

Competition from Electro-Mechanical Actuators in Precision Tasks

Electric linear actuators, aided by falling motor prices and servo drives, now dominate micrometre-level positioning. Their power-on-demand architecture lowers consumption and allows energy recovery, aligning with decarbonization targets. Hybrid systems that pair electric axes for fine moves with pneumatic stages for rapid approach partially mitigate share loss, but pure-electric competition intensifies in premium segments such as semiconductor assembly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Cylinders Drive Innovation

Double-acting units generated 47.3% of 2024 revenue, reinforcing their role as the workhorse of the pneumatic cylinder market. Smart cylinders, although representing a smaller base, are projected to clock a 4.5% CAGR to 2030 as embedded sensors feed PLCs and MES layers for closed-loop quality control. The pneumatic cylinder market size attached to smart variants will therefore expand faster than any other product category through enhanced OEE and predictive-maintenance returns. Single-acting and rodless designs continue to address specialty packaging and space-constrained conveyor duties, while tandem constructions cater to construction and mining, where peak force outweighs speed.

Sensorization transforms cylinders into edge-computing nodes, capturing stroke-by-stroke analytics that flag seal wear or misalignment well before unexpected downtime. IO-Link and Ethernet-APL interfaces now appear on mid-range product lines, democratizing access to condition data. Lubrication-free composite bushings reduce contamination risk in food zones and clean rooms.[4]Source: Bimba, “Original Line All Stainless Steel,” bimba.comAs cloud dashboards surface usage patterns across fleets, procurement departments recognize the lifecycle benefit despite higher upfront pricing, powering sustained demand for intelligent designs.

By Motion Type: Linear Dominance with Rotary Growth

Linear cylinders anchored 82.3% of the pneumatic cylinder market share in 2024 as push-pull motions remain ubiquitous in assembly, press-fitting, and clamping jobs. Nevertheless, rotary variants will outpace linear at a 5.1% CAGR thanks to robotics wrists, indexing tables, and medical-device actuators that rely on controlled rotation. For packaging OEMs, compact rotary drives simplify cap screwing and cartoning without external gearboxes, preserving layout flexibility. Soft-robotic grippers in rehabilitation devices adopt low-pressure rotary bellows that mimic human joints, evidencing growth in non-industrial niches.

Hybrid modules combining a linear slide with a 90-degree rotary clamp support multi-axis tasks on a single actuator, shrinking bill-of-material count. As cobots proliferate on mixed-model lines, designers specify rotary pneumatics for energy-absorbent, back-drivable joints that ensure intrinsic safety. This behavioural shift aligns with rising investments in collaborative automation across both advanced and developing economies.

By Bore Size: Miniaturization Drives Micro Segment

The 33–63 mm category contributed 32.2% to 2024 revenue, covering mainstream factory-automation force ranges. Yet micro cylinders ≤16 mm lead growth at 5.2% CAGR through 2030 as electronics and medical OEMs require precision in confined spaces. The pneumatic cylinder market size associated with the micro tier remains modest today, but its outsized expansion rate draws focused research and development investment. MEMS-fabricated microvalves achieve response times below 40 milliseconds, facilitating microfluidic dosing and lab-on-chip platforms.

Meanwhile, larger bore classes above 100 mm keep demand steady from mining, off-highway, and steel mills, where robust construction and tolerance of contaminants trump energy considerations. Manufacturers deploy nitrided piston rods and high-performance seals to extend service life under abrasive conditions, defending shares against hydraulics.

By End-User Industry: Food Processing Accelerates

Industrial automation and machinery retained 25.6% revenue in 2024, yet food and beverage plants will post the swiftest 5.8% CAGR as hygiene standards tighten. Stainless-steel cylinders with NSF-H1 grease and oil-free compressors avoid product contamination and withstand aggressive washdowns.[5]Source: Atlas Copco, “Oil-Free Air Compressors,” atlascopco.comThe pneumatic cylinder market size allocated to food lines, therefore, moves ahead of automotive, packaging, and metals. Automotive assembly continues to specify pneumatics for door handling and seat-press operations, but its mature capex cycle limits incremental unit growth.

Electronics clean rooms adopt oil-free, low-outgassing cylinders to protect wafers from particulate, sustaining share gains. Healthcare OEMs integrate micro pneumatics in rehabilitation exoskeletons and handheld surgical tools, an emerging but high-margin niche. Logistics and e-commerce hubs rely on compact slides and grippers in automated sortation equipment, reinforcing mid-term demand resilience.

Geography Analysis

The Asia-Pacific region held 39.30% of 2024 revenue, benefiting from established component supply chains in China and increasing capital expenditure in India and Southeast Asia. Government incentives for semiconductor fabrication in India and Vietnam further accelerate the adoption of oil-free and miniaturized cylinders.

North America is expected to register the fastest 6.10% CAGR from 2025 to 2030, driven by government grants and tax credits that encourage the domestic production of EV batteries, medical devices, and consumer goods. More than 300,000 manufacturing jobs were regained in 2022, and another 180,000 were added in the first half of 2023, strengthening the installed base for pneumatic equipment. High labor costs make automation indispensable, and pneumatics provide a proven and maintainable solution.

Europe continues stable growth amid aggressive sustainability targets. OEMs emphasize energy-optimized valve terminals and CO₂-neutral operations; Festo plans to achieve full neutrality across its German sites by 2024. Automotive clusters in Germany, packaging machinery in Italy, and aerospace in France sustain cylinder demand. Meanwhile, political commitment to circular-economy principles nudges investments toward high-efficiency compressed-air platforms.

South America and the Middle East and Africa remain nascent but promising. Brazilian food processors upgrade lines to meet export standards, while Gulf petrochemical players favor heavy-duty, corrosion-resistant cylinders. Growth rates are smaller, but margin profiles often exceed global averages due to custom engineering requirements.

Competitive Landscape

The industry is moderately fragmented. Festo recorded EUR 3.65 billion (USD 4.1 billion) turnover in 2023 and allocates over 7% of revenue to research and development, underscoring a technology-led strategy. Parker-Hannifin reported USD 19.9 billion in sales for fiscal 2024, although North American industrial sales declined 8.6% as OEM destocking continued at the company.

Consolidation trends accelerated: Ingersoll Rand closed a USD 135 million trio of bolt-on deals, adding hydraulic and pneumatic product lines that deliver USD 50 million extra annual revenue and expand specialty-cylinder breadth. Emerson targets packaging and robotics niches with the AVENTICS Series XV valve system featuring up to 350 NL/min flow in slim footprints. Competitive differentiation now centers on integrated diagnostics, cloud visibility, and lower energy footprints rather than mechanical dimensions alone. Rising demand for miniature and oil-free designs creates pockets for specialists, yet high tooling costs and certification barriers deter new entrants.

Pneumatic Cylinder Industry Leaders

SMC Corporation

Festo SE & Co. KG

Parker-Hannifin Corporation

Norgren Limited (IMI plc)

Aventics GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Festo marked its centenary, reaffirming commitments to AI-enabled pneumatics and cross-industry sustainability.

- October 2024: Ingersoll Rand finalized three acquisitions worth USD 135 million, adding APSCO, Blutek, and UT Pumps to its portfolio.

- August 2024: Emerson introduced AVENTICS Series XV valves with multi-protocol fieldbus and online configurator support.

- July 2024: SMC granted its Sustainability in Automation Award to Hypertherm Associates, spotlighting eco-friendly design advances.

Global Pneumatic Cylinder Market Report Scope

| Single-Acting Cylinders |

| Double-Acting Cylinders |

| Rodless Cylinders |

| Tandem and Multi-Stage Cylinders |

| Smart/Integrated-Sensor Cylinders |

| Linear |

| Rotary |

| ≤16 mm (Micro) |

| 17–32 mm |

| 33–63 mm |

| 64–100 mm |

| >100 mm (Heavy-Duty) |

| Automotive and Transportation |

| Food and Beverage Processing |

| Packaging and Logistics |

| Electronics and Semiconductor |

| Healthcare and Medical Devices |

| Metals and Machinery |

| Others End-User Industry (Textiles, Pulp and Paper) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Single-Acting Cylinders | ||

| Double-Acting Cylinders | |||

| Rodless Cylinders | |||

| Tandem and Multi-Stage Cylinders | |||

| Smart/Integrated-Sensor Cylinders | |||

| By Motion Type | Linear | ||

| Rotary | |||

| By Bore Size | ≤16 mm (Micro) | ||

| 17–32 mm | |||

| 33–63 mm | |||

| 64–100 mm | |||

| >100 mm (Heavy-Duty) | |||

| By End-User Industry | Automotive and Transportation | ||

| Food and Beverage Processing | |||

| Packaging and Logistics | |||

| Electronics and Semiconductor | |||

| Healthcare and Medical Devices | |||

| Metals and Machinery | |||

| Others End-User Industry (Textiles, Pulp and Paper) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving growth in the pneumatic cylinder industry?

The pneumatic cylinder market is primarily driven by low-cost factory automation projects (+1.2% CAGR impact), energy-efficient compressed air systems (+0.8%), brownfield smart-factory retrofits (+0.7%), and e-commerce fulfillment center expansion (+0.6%). The market is projected to grow from USD 16.5 billion in 2025 to USD 20.37 billion by 2030 at a 4.3% CAGR.

Which pneumatic cylinder types are most popular?

Double-acting cylinders dominate with 47.3% market share due to their versatility in bidirectional movement applications. However, smart cylinders with integrated sensors are growing fastest at a 4.5% CAGR through 2030 as manufacturers seek data-driven maintenance and performance optimization capabilities.

How are pneumatic cylinders used in food processing?

Food processing represents the fastest-growing end-user segment (5.8% CAGR) for pneumatic cylinders. The industry uses stainless steel cylinders with NSF-H1 food-grade lubricants and oil-free compressed air systems to prevent contamination. These specialized cylinders withstand aggressive washdown procedures while meeting strict hygiene standards required for food safety compliance.

Where is pneumatic cylinder demand strongest globally?

Asia-Pacific leads with 39.3% market share in 2024, leveraging established manufacturing infrastructure in China and growing automation in India and Southeast Asia. However, North America shows the fastest growth at 6.1% CAGR (2025-2030), driven by reshoring initiatives that created over 480,000 manufacturing jobs between 2022-2023.

Page last updated on: