Assembly Fastening Tool Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

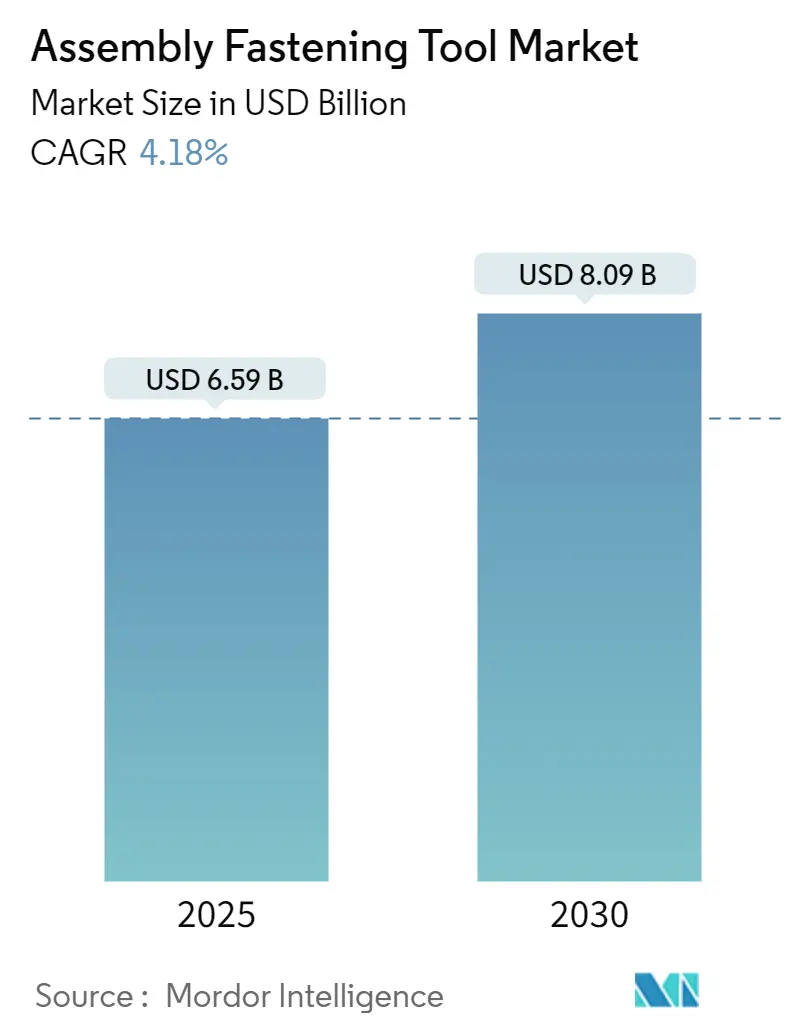

| Market Size (2025) | USD 6.59 Billion |

| Market Size (2030) | USD 8.09 Billion |

| Growth Rate (2025 - 2030) | 4.18% CAGR |

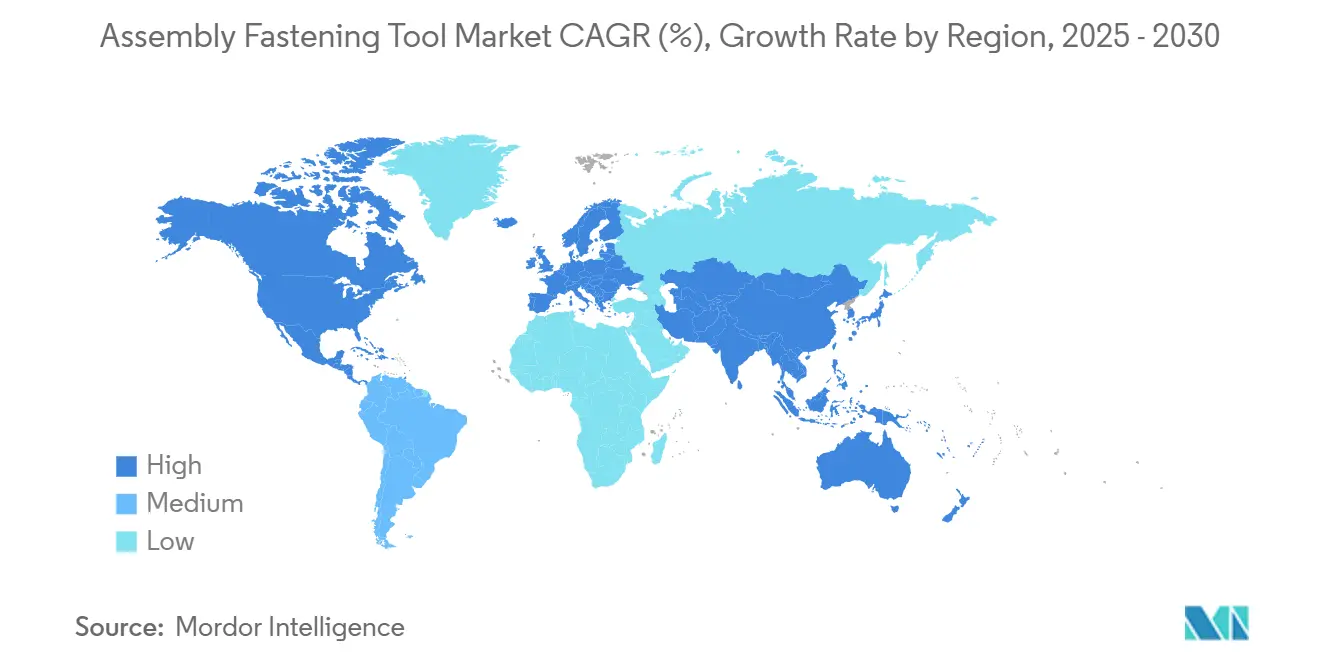

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Assembly Fastening Tool Market Analysis by Mordor Intelligence

The assembly fastening tool market size stood at USD 6.59 billion in 2025 and is forecast to reach USD 8.90 billion by 2030, advancing at a 4.18% CAGR. This outlook reflects steady demand growth as factories accelerate Industrial 4.0 programs and shift from pneumatic toward electric architectures. Investments in collaborative robots, data-rich tightening platforms, and sustainability-driven electrification underpin revenue expansion, while mature plants continue to upgrade legacy tools to meet stricter quality regimes. Competitive differentiation now leans on software, energy efficiency, and application-specific design rather than headline torque figures, giving established vendors scope to defend share without aggressive price cuts. Opportunities cluster around Asia Pacific capacity additions, precision electronics assembly, and lightweight-material joining in transportation manufacturing. Raw-material price swings and a widening skills gap temper growth but also motivate automation spending that favors digitally enabled fastening solutions.

Key Report Takeaways

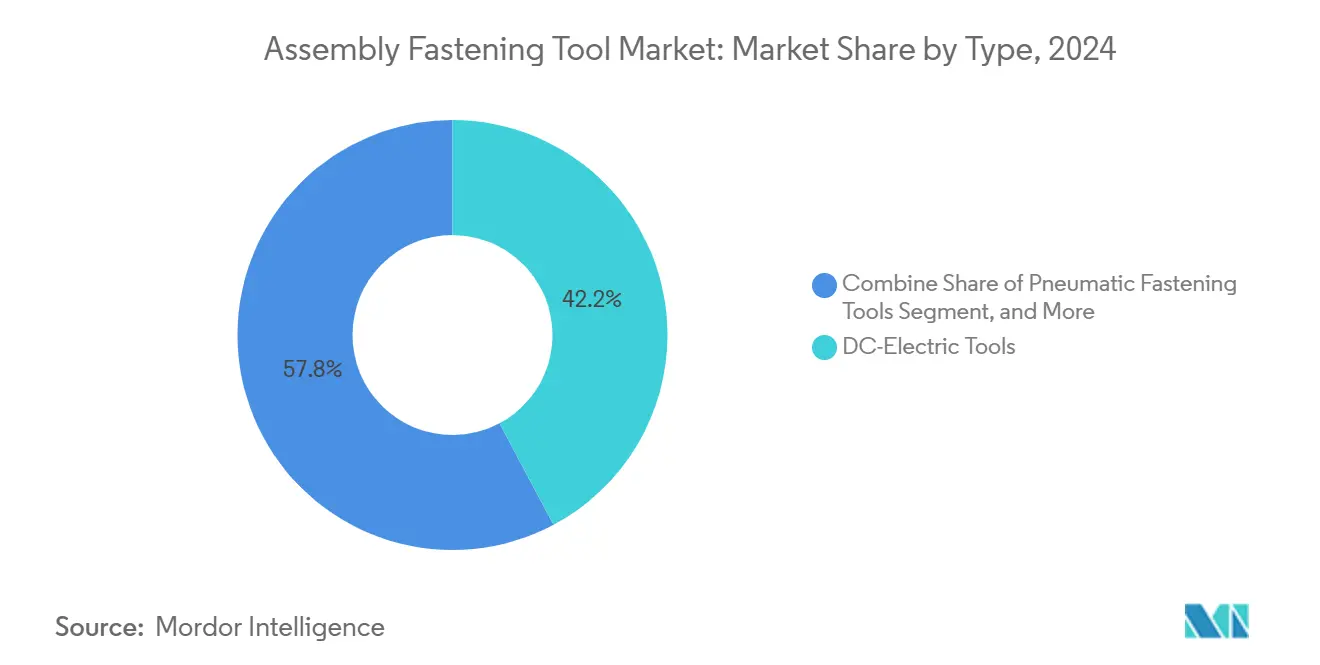

- By technology, DC-electric tools led with 42.21% of assembly fastening tool market share in 2024. Battery-electric tools are projected to post the fastest 4.29% CAGR through 2030.

- By automation level, manual hand-held platforms accounted for 55.67% of the assembly fastening tool market size in 2024. Fully automated/robotic are poised to expand at a 4.31% CAGR between 2025-2030.

- By end-use, automotive captured 37.23% revenue share in 2024; electronics and semiconductor equipment is set to grow at a 4.27% CAGR to 2030.

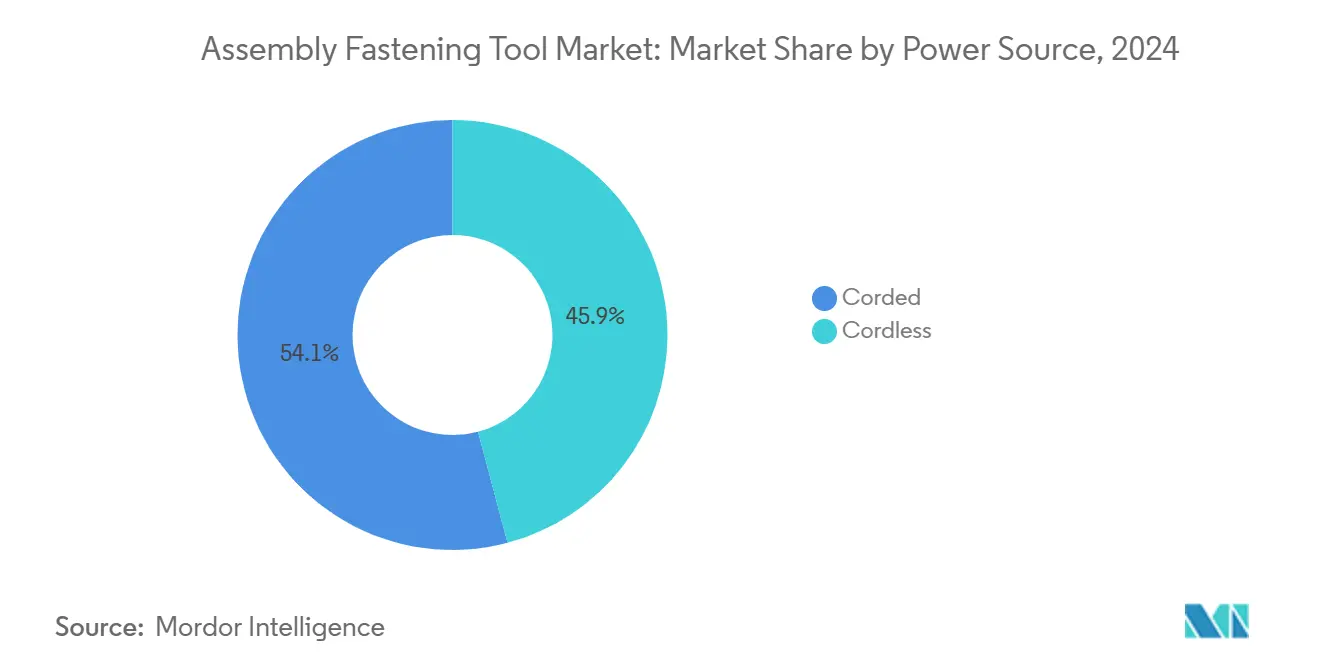

- By power source, corded captured 54.11% revenue share in 2024; cordless is set to grow at a 4.91% CAGR to 2030.

- By region, North America held 38.41% of the assembly fastening tool market size in 2024, while Asia Pacific shows the highest 4.98% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Assembly Fastening Tool Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing automation and Industry 4.0 integration | +1.2% | Global with APAC leading adoption | Medium term (2-4 years) |

| Shift from pneumatic to electric/battery-powered tools | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Rising demand for lightweight materials | +0.5% | Aerospace regions, global automotive | Long term (≥ 4 years) |

| Increasing integration with collaborative robots | +0.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Growing emphasis on precision, quality and compliance | +0.6% | Global aerospace and automotive | Long term (≥ 4 years) |

| Demand for sustainable and energy-efficient tools | +0.4% | Europe leading, North America following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Automation and Industry 4.0 Integration

Manufacturing plants are embedding smart tools that stream real-time torque, angle, and cycle-time data directly into MES and ERP stacks, enabling closed-loop quality control and predictive maintenance. Atlas Copco’s Alture deployment at CNH Industrial’s Austrian site demonstrated defect reduction after parameter optimization. Machine-learning models trained on fastening signatures now adjust sequences automatically, preventing cross-threading and stripping events. China leads roll-outs; 53% of factory managers there expect largely autonomous operations by 2040. This data-centric ecosystem is becoming a procurement prerequisite, especially among aerospace tier-ones that demand electronic traceability for every critical joint.

Shift from Pneumatic to Electric/Battery-Powered Tools

Electric drives eliminate the latent energy losses of compressed-air networks, cutting total cost of ownership while boosting throughput. Pneumatic systems typically waste 60-80% of input energy through leaks and pressure drops.[1]Atlas Copco, “Make the Switch from Pneumatic to Electric Tools,” atlascopco.com Battery packs built on high-capacity lithium-ion cells now sustain high-torque output across full shifts; Bosch’s Nexo cordless nutrunner delivers repeatable torque from 2-50 Nm with integrated error-proofing. Air-hose removal mitigates foreign-object-debris risks in aircraft final assembly and simplifies workstation reconfiguration in automotive body-in-white lines. Stanley Black & Decker measured 60% CO₂e reduction on sites adopting its DEWALT POWERSHIFT cordless platform.

Rising Demand for Lightweight Materials

Broader use of carbon-fiber reinforced thermoplastics and mixed-metal body structures raises joint-integrity challenges. CFRTs deliver 40% faster cycle times versus metallic panels but require tools with tighter torque accuracy and thermal monitoring.[2]Advanced Materials, “Carbon Fiber Reinforced Thermoplastics: From Materials to Manufacturing and Applications,” onlinelibrary.wiley.com Battery-electric vehicle packs marry aluminum housings to steel crash frames, demanding adaptive torque algorithms that avoid galvanic corrosion. DEPRAG’s screwdriving modules for EV battery lines compensate for stack-up tolerances by capturing clamping-force data every cycle. Electronics assemblers likewise need low-reactive force spindles to protect wafer-level components.

Growing Emphasis on Precision, Quality and Compliance Requirements

Aerospace primes require full traceability for every critical fastener; Boeing’s D6-82479 Rev C standard drives suppliers toward ISO 9001 and AS9100 certified toolchains. Automotive OEMs impose zero-defect mandates for high-voltage EV assemblies, triggering demand for error-proofing and joint-verification software baked into tightening controllers. Electronics manufacturers rely on statistical-process-control dashboards that flag torque outliers in real time, preventing costly board scrap.

Restraints Impact Analysis of Assembly Fastening Tool Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw material prices | -0.9% | Global, emerging markets most affected | Short term (≤ 2 years) |

| Shortage of skilled labor | -0.7% | North America and Europe | Medium term (2-4 years) |

| Increasing pricing pressure and margin compression | -0.4% | Global competitive markets | Short term (≤ 2 years) |

| Integration complexity with existing systems | -0.3% | Developed markets with legacy infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices

Large vendors hedge with multiyear contracts and diversified sourcing while smaller producers, constrained by working-capital limits, absorb input shocks or raise prices, eroding competitiveness. Profit compression can delay R and D investment and lengthen replacement cycles for industrial buyers.

Shortage of Skilled Labor

Plants counter by procuring self-diagnosing tools that require minimal operator expertise, though this shifts the shortage toward maintenance technologists. Training partnerships and augmented-reality work instructions help onboarding but add upfront costs that smaller plants may forgo.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Assembly Fastening Tool Market Segment Analysis

By Type:

Electric Tools Drive Market EvolutionDC-electric platforms captured 42.21% assembly fastening tool market share in 2024, validating their position in high-precision assembly where repeatability and audit trails trump raw speed. Pneumatic systems remain cost-effective for legacy lines yet face retrofits as energy costs rise. Battery-electric models deliver the fastest 4.29% CAGR, propelled by lighter high-energy cells and integrated controllers that log every tightening for traceability. Hydraulic and other specialty formats occupy niches requiring ultra-high torque or hazardous-area safety compliance.

The transition reflects broader electrification trends across factories. Bosch introduced 30 brushless models in 2024 to widen its 18 V ecosystem.[3]Bosch Power Tools, “Launches Over 30 New Tools Expanding 18V Platform,” bosch-press.comAutomotive OEMs equip BIW stations with one-button programming guns that auto-populate torque curves from central servers, shrinking operator training times. Aerospace tier-ones deploy cordless angle nutrunners to eliminate hose-related foreign-object damage.

By Automation Level:

Manual Operations Persist Despite Robotic GrowthManual hand-held devices comprised 55.67% of assembly fastening tool market size in 2024, evidence that human dexterity remains irreplaceable for complex geometries and mixed-model stations. Semi-automated fixtured systems add precision without fully removing the operator, using guided-sequence lights and auto-shutoff clutches to prevent skipped bolts. Fully automated/robotic show the briskest 4.31% CAGR, empowered by safer cobot architectures and simplified programming tools.

Hybrid workcells dominate investment, marrying robotic repeatability to human adaptability. A European white-goods plant couples three UR5e arms with vision-guided screwdrivers, lifting throughput while letting operators handle inspection. This incremental pathway fits budget constraints and labor realities better than lights-out plans.

By Power Source:

Cordless Revolution AcceleratesCorded solutions maintained 54.11% share in 2024 owing to unlimited runtime in fixed stations; however, cordless models enjoy a 4.91% CAGR through 2030. Modern batteries sustain shift-length life while embedded connectivity relays torque data over Wi-Fi. Aerospace assembly favors cordless to avoid tether hazards, and construction managers expect fully electrified jobsites within two years.

DEWALT’s 2025 survey found 66% of site managers view battery platforms as critical to productivity. Similar sentiment spreads to general manufacturing as reconfigurable lines replace traditional conveyor-paced layouts.

By End-use Industry:

Electronics Surge Reshapes Demand PatternsAutomotive led revenue with 37.23% share, sustained by platform refresh cycles and EV driveline rollouts that mandate torque-traceable joints. Electronics and semiconductor equipment is on course for a 4.27% CAGR, driven by AI accelerator boards and flexible PCBs requiring sub-0.1 Nm accuracy and minimal downward force. Aerospace and defense rely on certified tightening systems meeting AS9100 documentation, while off-highway machinery rides infrastructure spending spurts.

Rapid semiconductor investment alters vendor roadmaps: tool makers now integrate vacuum-compatible spindles and clean-room-compliant housings. MKS Instruments cited strong vacuum-product sales in Q1 2025 as chip fabs expand capacity.

Geography Analysis

APAC Assembly Fastening Tool Market

Asia Pacific’s 4.98% CAGR through 2030 outpaces all regions as China, India, and Southeast Asia add EV, electronics, and machinery capacity. Chinese OEMs such as BYD continue building regional assembly plants, and India’s production-linked incentive scheme pulls tool suppliers closer to local customers. These investments expand the assembly fastening tool market size across APAC plants that demand digitally integrated fastening ecosystems to satisfy export quality benchmarks.

North America Assembly Fastening Tool Market

North America controlled 38.41% revenue in 2024, anchored by automotive retooling for electrification and aerospace programs that require stringent joint-traceability. U.S. Tier-1 suppliers accelerate tool fleet renewal to satisfy OEM defect-per-vehicle targets. Growth moderates relative to emerging regions as base penetration is high, yet software upgrades and cobot retrofits sustain replacement cycles. Federal tax incentives for energy-efficient equipment spur migration from air tools to DC-electric platforms, supporting the assembly fastening tool market.

Europe and Middle East Assembly Fastening Tool Market

Europe balances mature automotive hubs with renewable-energy equipment manufacturing. Tight carbon-reduction mandates make the region an early adopter of cordless and energy-optimized fastening systems. German machine builders specify integrated controller protocols that feed torque data into plant-wide MES environments, driving demand for open-architecture electric tools. Eastern Europe and the Middle East provide incremental upside as infrastructure projects and industrial diversification stimulate fresh tool orders.

Competitive Landscape

The assembly fastening tool market features moderate fragmentation with technology, service, and channel breadth defining leadership. Atlas Copco, Stanley Black & Decker, and Bosch collectively accounted for just over one-third of global sales in 2024, leveraging extensive product portfolios and worldwide calibration-service networks. Atlas Copco extended its lead by acquiring automated bolt-feeding specialists, broadening turnkey line-integration capabilities. Stanley Black & Decker emphasized sustainability credentials, citing emission cuts from its cordless equipment when replacing small gasoline engines.

Mid-tier contenders focus on niche strengths: Hilti excels in construction, Ingersoll Rand expands via hydraulic and pump acquisitions, and DEPRAG targets EV battery assembly modules. Software vendors collaborate with hardware majors to embed cloud analytics, aligning with customer demand for uptime-based service contracts. Competition therefore pivots on ecosystem support rather than tool alone, raising barriers for new entrants unless they offer differentiated digital value or specialized application know-how.

Pricing competition remains limited; customers prioritize lifetime cost and compliance over upfront tool expense. However, commodity inflation and labor shortages squeeze margins, pushing vendors toward subscription-based software and service bundles that smooth revenue and lock in customers. Market concentration may increase as leading brands deploy cash to acquire smaller innovators, consolidating technology while extending coverage in high-growth regions.

Assembly Fastening Tool Industry Leaders

Atlas Copco Group

Stanley Black & Decker, Inc.

Robert Bosch GmbH

Ingersoll Rand Inc.

Hilti Group

- *Disclaimer: Major Players sorted in no particular order

Assembly Fastening Tool Market Companies Covered in this Report

- Atlas Copco Group

- Stanley Black & Decker, Inc.

- Robert Bosch GmbH

- Ingersoll Rand Inc.

- Hilti Group

- Makita Corporation

- Pace Assembly Tools

- Apex Tool Group, LLC

- Snap-on Incorporated

- Panasonic Holdings Corporation

- Mountz Inc.

- Estic Corporation

- WEBER Schraubautomaten GmbH

- Sumake Industrial Co., Ltd.

- Kolver Srl

- FEC Inc.

- Uryu Seisaku, Ltd.

- Kilews Industrial Co., Ltd.

- Applifast Inc.

- Rotabroach. Ltd.

Recent Industry Developments in Assembly Fastening Tool Market

- March 2025: Robert Bosch GmbH, a provider of technology and services, has unveiled its latest range of Hand Tools tailored for professionals and artisans. Alongside these, Bosch introduced advanced Industrial Tools aimed at streamlining assembly line operations.

- October 2024: Makita Inc., a tool manufacturer, released a new 40V max XGT 9-inch power cutter designed to deliver more power and less vibration than previous models. The tool caters to masons, general contractors, hardscape contractors, fire and rescue professionals, and other industry professionals.

- January 2024: Hilti North America, a provider innovative tools, technology, software, and services to the commercial construction industry, announced the launch new cordless tools on the 22V Nuron battery platform to fill out the portfolio and offer greater value through its subscription tool service, Fleet Management.

Global Assembly Fastening Tool Market Report Scope

Segmentation Overview

| Pneumatic Fastening Tools |

| DC-Electric Tools |

| Battery-Electric Tools |

| Hydraulic / Other Specialty Tools |

| Manual Hand-Held |

| Semi-Automated Fixtured |

| Fully-Automated / Robotic |

| Corded |

| Cordless |

| Automotive |

| Aerospace and Defense |

| Electronics and Semiconductor Equipment |

| Heavy Machinery and Off-Highway |

| Construction and MRO |

| Other End-use Industries (includes Marine, Energy, and Telecommunication) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Type | Pneumatic Fastening Tools | |

| DC-Electric Tools | ||

| Battery-Electric Tools | ||

| Hydraulic / Other Specialty Tools | ||

| By Automation Level | Manual Hand-Held | |

| Semi-Automated Fixtured | ||

| Fully-Automated / Robotic | ||

| By Power Source | Corded | |

| Cordless | ||

| By End-use Industry | Automotive | |

| Aerospace and Defense | ||

| Electronics and Semiconductor Equipment | ||

| Heavy Machinery and Off-Highway | ||

| Construction and MRO | ||

| Other End-use Industries (includes Marine, Energy, and Telecommunication) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the assembly fastening tool market by 2030?

The market is forecast to reach USD 8.90 billion by 2030, reflecting a 4.18% CAGR from 2025.

Which technology segment is growing fastest within assembly fastening tools?

Battery-electric tools show the highest 4.29% CAGR as factories adopt cordless, energy-efficient platforms.

Why is Asia Pacific considered the most promising region for assembly fastening tool suppliers?

Rapid capacity additions in electric vehicle, electronics, and general manufacturing plants drive a 4.98% regional CAGR and growing demand for digital fastening solutions.

How are sustainability goals influencing tool selection?

Buyers prefer DC-electric and cordless tools that cut energy consumption up to 80% versus pneumatics and reduce operational CO₂e emissions by 60%.

What factors are pushing factories toward fully automated fastening cells?

Skilled-labor shortages and the need for traceable, zero-defect joints encourage investments in collaborative-robot workcells that lift throughput and quality.

Page last updated on: