Pressure Control Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.31 Billion |

| Market Size (2031) | USD 11.46 Billion |

| Growth Rate (2026 - 2031) | 2.12% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

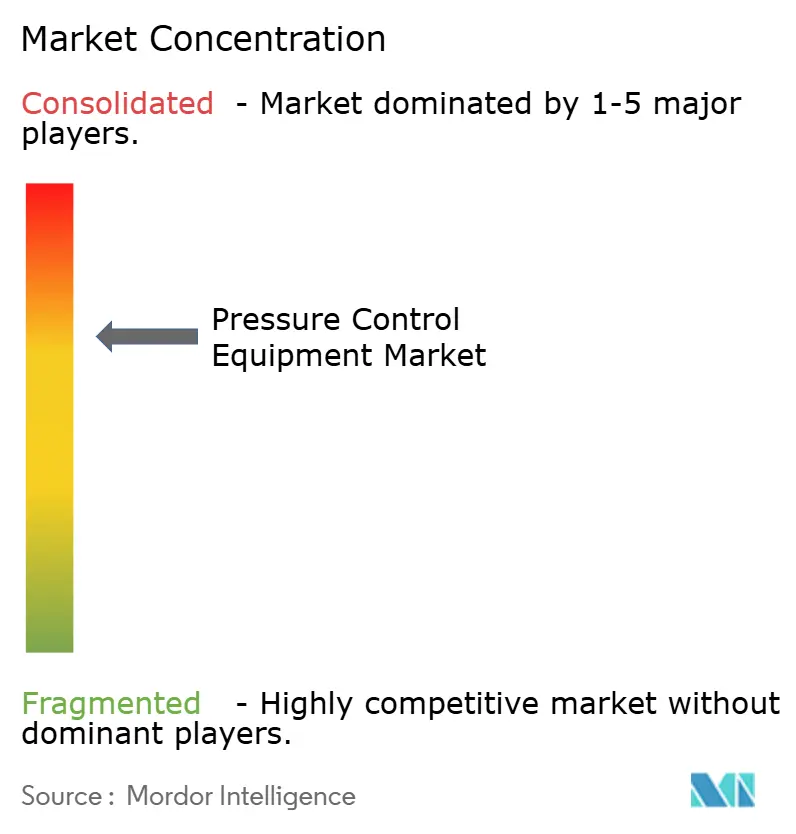

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pressure Control Equipment Market Analysis by Mordor Intelligence

The pressure control equipment market size is expected to grow from USD 10.1 billion in 2025 to USD 10.31 billion in 2026 and is forecast to reach USD 11.46 billion by 2031 at 2.12% CAGR over 2026-2031. Growth is propelled by deep- and ultra-deepwater drilling campaigns in South America, rapid adoption of managed pressure drilling technologies, and stricter safety regulations that shorten replacement cycles for aging systems. North American shale programs and North Sea brownfield projects sustain baseline demand, while ultra-high-pressure (20 kpsi+) systems unlock frontier reservoirs. Digital valve diagnostics, electrification, and AI-enabled predictive maintenance further stimulate equipment upgrades as operators pursue operational integrity and lower emissions. Meanwhile, crude-price volatility and a thriving rental model temper capital spending on new builds, driving suppliers to balance fleet investments with traditional sales channels.

Key Report Takeaways

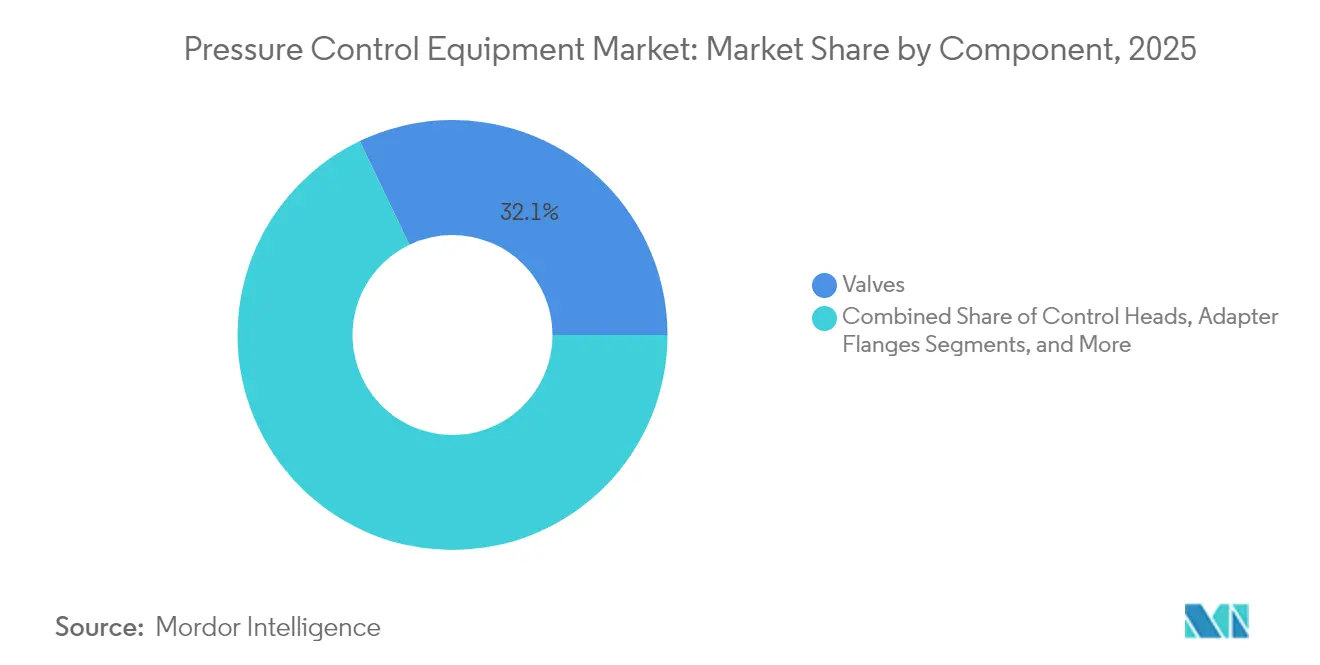

- By component, valves led with 32.10% revenue share in 2025; blowout preventers are forecast to expand at an 2.44% CAGR through 2031.

- By pressure rating, high-pressure systems held 56.55% of pressure control equipment market share in 2025, while ultra-high-pressure systems are projected to grow at 3.28% CAGR between 2026-2031.

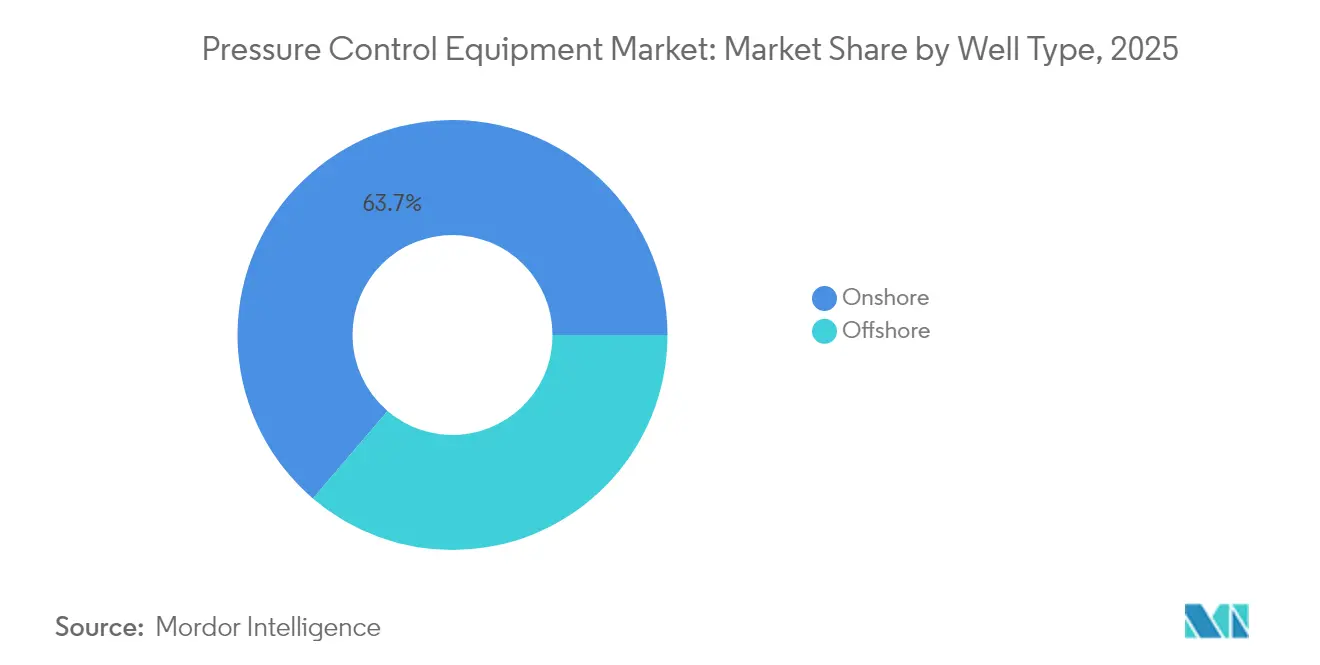

- By well type, onshore operations commanded 63.75% of the pressure control equipment market size in 2025; ultra-deepwater offshore wells are advancing at a 2.58% CAGR to 2031.

- By operation phase, drilling accounted for 46.20% share of the pressure control equipment market size in 2025, whereas intervention services exhibit a 3.06% CAGR to 2031.

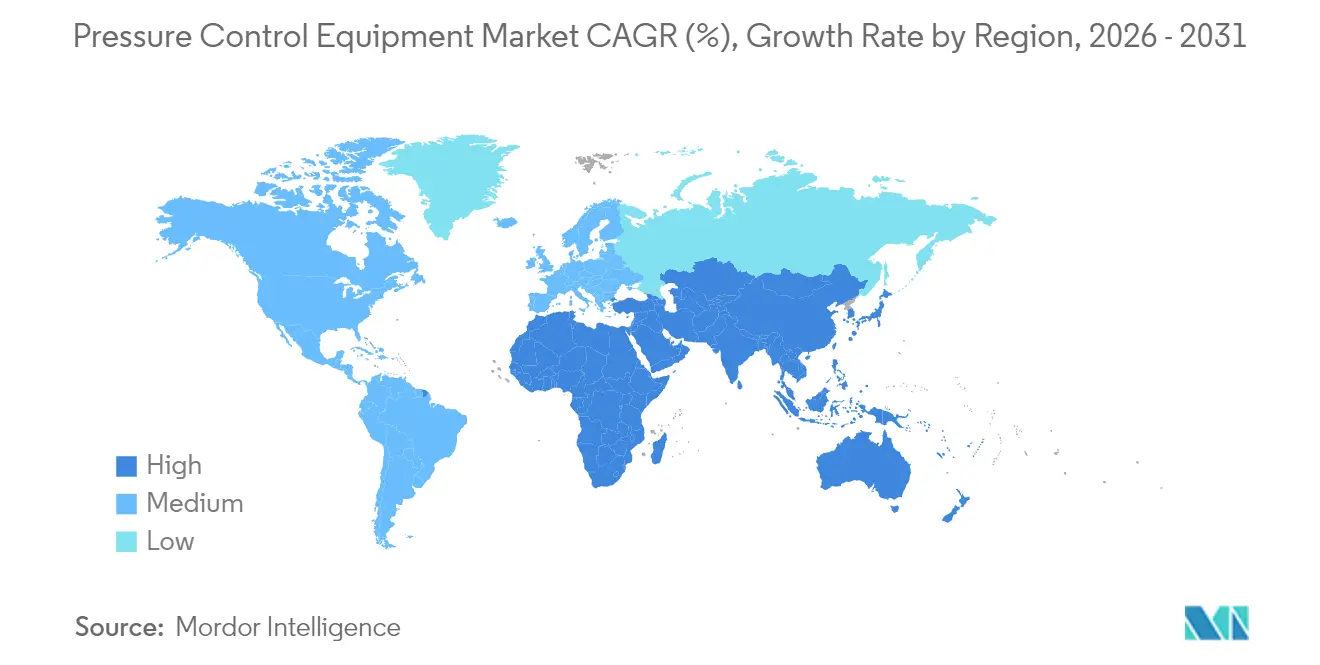

- By geography, North America captured 38.55% of the pressure control equipment market share in 2025; the Middle East records the highest regional CAGR at 2.58% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pressure Control Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Deep- & Ultra-Deepwater Drilling Campaigns in South America | +0.7% | South America, with spillover to Gulf of Mexico | Medium term (2-4 years) |

| Adoption of Managed Pressure Drilling Requiring Advanced Control Heads | +0.5% | Global, with early adoption in North America & North Sea | Short term (≤ 2 years) |

| Stringent Safety Regulations Driving Replacement Cycles in North American Shale | +0.4% | North America, particularly Permian Basin | Short term (≤ 2 years) |

| North Sea Brownfield Life-Extension Retrofits | +0.3% | Europe, primarily UK & Norwegian sectors | Medium term (2-4 years) |

| Digital Valve Diagnostics Minimising NPT in Middle-East Offshore Assets | +0.2% | Middle East, expanding to Asia-Pacific | Long term (≥ 4 years) |

| LNG Import-Terminal Expansion in Asia Boosting High-Pressure Transfer Valves | +0.2% | Asia-Pacific, with concentration in China & South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Deep- & Ultra-Deepwater Drilling Campaigns in South America

South America’s deepwater renaissance demands pressure control equipment that withstands extreme pressures, high CO₂ content, and corrosive fluids. SLB’s USD 800 million contract with Petrobras covers more than 100 wells in Brazil’s pre-salt basins, integrating high-spec safety valves and AI-enabled monitoring. Woodside Energy’s Trion project relies on 20 kpsi subsea systems for 18 ultra-deepwater wells at 2,500 m water depth. Flexible pipe supplied by Baker Hughes uses corrosion-resistant alloys to mitigate CO₂-induced cracking. Integrated hardware-plus-service packages spur aftermarket revenue as operators seek single-throat accountability for life-of-field support.[1]SLB, “SLB awarded integrated services contract for all Petrobras’ offshore fields in Brazil,” slb.com

Adoption of Managed Pressure Drilling Requiring Advanced Control Heads

Managed pressure drilling (MPD) has moved from deepwater niche to mainstream technique. Halliburton and Sekal deployed the first automated on-bottom drilling system integrating LOGIX automation and Drilltronics for real-time pressure control. Weatherford’s Victus Intelligent MPD suite won projects with Saudi Aramco and Petroleum Development Oman, illustrating onshore uptake. Field results show MPD cutting non-productive time by 92 hours and trimming total drilling time by 7.4 days. AI algorithms embedded in control heads predict influx or loss events, boosting safety and lowering well costs.[2]Offshore Magazine, “Halliburton, Sekal partner on automated on-bottom drilling system for Equinor North Sea project,” offshore-mag.com

Stringent Safety Regulations Driving Replacement Cycles in North American Shale

Updated blowout-preventer test intervals and pressure vessel inspection requirements shorten replacement cycles, enlarging the installed-base opportunity. The US Bureau of Safety and Environmental Enforcement underscores MPD as a compliant control method for high-pressure wells. Baker Hughes’ all-electric SureCONTROL Plus valves and Hummingbird cementing unit meet new reliability metrics while slashing maintenance. Operators adopting advanced systems report up to 75% fewer well-control incidents compared with legacy equipment.

North Sea Brownfield Life-Extension Retrofits

More than half of North Sea installations exceed 20 years of service. Next-generation subsea controls for Tordis and Vigdis fields restore bandwidth while eliminating obsolete electronics. Shell’s thermoplastic composite risers deliver a 50% lower CO₂ footprint than steel and remove continuous chemical dosing. Modular retrofit kits reduce capex by 70% versus wholesale replacement and align with UK carbon-reduction targets.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Crude-Oil Price Volatility Delaying Offshore CAPEX | -0.7% | Global, with highest impact on deepwater projects | Short term (≤ 2 years) |

| Rental Pressure-Control Packages Dampening New-Build Sales | -0.3% | North America & North Sea, expanding globally | Medium term (2-4 years) |

| Forged-Alloy Component Supply Bottlenecks Post-Ukraine Conflict | -0.2% | Global, with acute impact in Europe & North America | Short term (≤ 2 years) |

| Skilled-Labour Shortage for 20k-psi Equipment Maintenance in Emerging Markets | -0.1% | Asia-Pacific, Middle East, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility Delaying Offshore CAPEX

Brent is expected to average USD 74/bbl in 2025, but bearish views place downside at USD 65/bbl amid oversupply and tepid Chinese demand. Operators defer final investment decisions, pushing deepwater recovery to 2026+ as FPSO lead times stretch three-plus years. US E&Ps cut 2024 capex to USD 61.7-65.4 billion, underscoring disciplined spend. Equipment orders slow, especially for new ultra-deepwater rigs.

Rental Pressure-Control Packages Dampening New-Build Sales

Operators favor opex-based rentals that flex with rig utilization. Service firms grow fleets to secure recurring revenue but must maintain high uptime to offset lower capital turnover. Demand for latest-generation BOP stacks via rental boosts aftermarket services but tempers OEM sales pipelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Valves Sustain Leadership while Blowout Preventers Accelerate

Valves generated 32.10% of 2025 revenue as every drilling, completion, and production phase depends on ball, gate, and choke variants for fail-safe isolation. Incremental gains arise from digital positioners that provide real-time health data. Blowout preventers expand at an 2.44% CAGR to 2031, propelled by mandatory 20 kpsi capability for ultra-deepwater basins. Control heads enjoy growing share as MPD moves onshore; annular designs with elastomer enhancements reduce routine seal changes by 30%. Complementary items like adapter flanges and quick unions capture steady demand as rig owners standardize interfaces.

Supplier innovation spans beyond oil and gas: Emerson’s TESCOM HV-7000 hydrogen regulator signals cross-sector diversification. Christmas trees, particularly subsea vertical monobore styles, command premium price due to higher metallurgy and sensor density. OEM gross margins on subsea variants exceed 25% versus 17-19% on comparable surface trees. Integrated packages bundling valves, manifolds, and digital twins strengthen customer lock-in and open service-contract annuities.

By Pressure Rating: Ultra-High-Pressure Solutions Unlock Frontier Plays

High-pressure (10–20 kpsi) systems controlled 56.55% of pressure control equipment market share in 2025, anchored by 15 kpsi stacks deployed on deepwater floaters. The pressure control equipment market size tied to this rating tier will expand in low-single digits as adoption plateaus. Conversely, ultra-high-pressure (>20 kpsi) solutions outpace all categories at 3.28% CAGR to 2031, driven by Chevron’s Anchor and BP’s 20 kpsi projects.

OEMs are redesigning rams with tungsten-carbide inserts and maraging-steel housings to meet fatigue targets. Maximator’s 8,000-bar test rigs accelerate qualification of next-gen alloys. Low-pressure (<10 kpsi) equipment retains relevance in legacy land wells yet faces pricing pressure due to oversupply. Regional split shows North America skewing toward higher pressures, while parts of Middle East still deploy 10 kpsi systems on conventional fields.

By Well Type: Offshore Ultra-Deepwater Growth Surpasses Onshore Baseline

Onshore wells accounted for 63.75% of 2025 revenue thanks to resilient shale programs and conventional land rigs across the Middle East and China. Mature basin re-fracturing sustains valve demand, but growth moderates. Ultra-deepwater wells rise at 2.58% CAGR as Petrobras, Woodside, and Shell sanction projects requiring 2,500-3,000 m water-depth capability.

The pressure control equipment market size attached to ultra-deepwater could double by 2030, reflecting hardware unit cost multiples of 3-4× versus land equivalents. Subsea trees engineered for 15–20 kpsi and –18 °C to 176 °C temperature range enable safe production from high-pressure, high-temperature formations. Shallow-water and deepwater projects maintain steady demand through tie-backs and life-extension drilling near existing hubs.

By Operation Phase: Intervention Services Drive Fastest Upside

Drilling remained the largest phase with 46.20% share in 2025, underpinned by around 600 active US land rigs and 200 offshore rigs worldwide. However, intervention and work-over exhibit 3.06% CAGR as operators stretch asset life. AI-enabled chemical optimization platforms such as Baker Hughes’ InjectRT prolong equipment run life and drive chemical savings up to 30%.

Growing adoption of thru-tubing services and coiled-tubing-conveyed MPD tools boosts control-head utilization. Completion operations seek compact, all-electric wellhead systems that reduce topside footprint and emissions, aligning with decarbonization goals. Continuous production activities generate predictable aftermarket revenue for choke valves, wellhead sensing, and emergency-shutdown systems.

Geography Analysis

North America captured 38.55% of 2025 revenue, led by Permian Basin shale drilling and Gulf of Mexico subsea developments. Rig activity averages 600 land and 25 floating rigs, sustaining steady call-off orders for BOP spares and valve refurbishments. Canada adds incremental growth through oil-sands sustaining projects and Montney gas drilling, with rig counts expected to rise 4-5% annually, while Mexico’s Trion project brings new ultra-deepwater demand.

The Middle East is the fastest-growing region at 2.58% CAGR. Saudi Aramco, ADNOC, and PDO raise rig count from 412 in 2024 to a forecast 618 by 2028, spurring orders for high-pressure BOP stacks and digital choke manifolds. Real-time valve diagnostics installed on offshore platforms cut non-productive time by 18%, encouraging broader deployment. Israel and Turkey add to regional momentum through gas development.

Asia-Pacific shows diversified drivers: China’s shale gas and LNG terminal build-out, India’s exploration push lifting rigs from 111 to 142 by 2028, and South Korea’s new regas terminals that specify 15 kpsi actuated valves. Regional buyers demand local content, prompting OEMs to expand joint ventures and assembly lines. Australia maintains investment in Northwest Shelf tie-backs, while Southeast Asian national oil companies focus on marginal-field redevelopment.

Europe’s North Sea leverages brownfield retrofits and life-extension to sustain equipment upgrades. Electrification and composite risers reduce platform emissions, dovetailing with EU carbon objectives. Latin America beyond Brazil gains support from Argentina’s Vaca Muerta shale pilots and Guyana’s deepwater ramp-up. Africa remains mixed: Angola and Namibia attract exploration budgets, whereas Nigeria grapples with fiscal uncertainties.

Competitive Landscape

The market displays moderate concentration: top five suppliers account for roughly 68% of global revenue. SLB, Baker Hughes, Halliburton, Weatherford, and NOV leverage integrated portfolios and global service networks. SLB’s acquisition of ChampionX, awaiting final clearances, will unlock USD 400 million synergies and deepen production-chemical integration. Baker Hughes and Cactus formed a surface pressure-control joint venture granting Cactus 65% ownership, consolidating wellhead positions and broadening international reach.

Technology leadership pivots on AI-driven automation, electrification, and materials science. Halliburton’s LOGIX automated drilling and SLB’s Ora intelligent testing deliver data-rich insights that inform pressure-control parameters. White-space entrants such as Innovex International target niche downhole tools, while Maximator supplies ultra-high-pressure test equipment critical for 20 kpsi certification. OEMs race to patent fail-safe valve actuation and remote condition-monitoring algorithms, creating defensible IP and aftermarket pull.

Customers favor bundled hardware-software-service contracts reducing interface risk and enabling performance-based KPIs. Suppliers respond by expanding digital twins and remote operations centers that supervise drilling and production pressure envelopes. Skilled-labor shortages in emerging markets elevate value propositions around autonomous systems. Sustainability also influences buying: all-electric wellheads and composite risers command premiums as operators strive for lower Scope 1 and Scope 2 emissions.

Pressure Control Equipment Industry Leaders

-

Baker Hughes (A GE Company)

-

Schlumberger, Ltd.

-

Weatherford International, PLC

-

National Oilwell Varco, Inc.

-

Halliburton Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Baker Hughes and Cactus completed their joint venture for surface pressure control services, with Cactus owning 65% and operating Baker Hughes' surface pressure control product line. The partnership aims to enhance technological innovation while maintaining leadership in international markets for surface wellhead and production tree systems, with the transaction subject to regulatory approvals expected to close in the second half of 2025.

- April 2025: SLB announced it can legally close its acquisition of ChampionX after all waiting periods under US antitrust law expired. The acquisition includes a definitive agreement to sell ChampionX's equity interests in US Synthetic Corporation to a third party while SLB retains its MegaDiamond business for polycrystalline diamond compact cutters, with the transaction still under antitrust review in Norway.

- April 2025: Baker Hughes launched three electrification technologies for onshore and offshore operations, including the Hummingbird all-electric land cementing unit, SureCONTROL Plus interval control valves for electrical remote operations, and an all-electric subsea production system designed to reduce installation complexity and carbon footprint.

- March 2025: SLB was awarded a major drilling contract by Woodside Energy for the ultra-deepwater Trion development offshore Mexico, encompassing 18 wells over three years with AI-enabled drilling capabilities. The project will utilize digital directional drilling, logging while drilling, and cementing services, with operations beginning in early 2026 and first production targeted for 2028.

Global Pressure Control Equipment Market Report Scope

The pressure control equipment market is segmented by component (valves, control head, wellhead flange), application (offshore, onshore), type (high pressure (above 10,000 PSI), low pressure (below 10,000 PSI), and geography.

| Valves | Ball Valves |

| Gate Valves | |

| Choke Valves | |

| Check Valves | |

| Blowout Preventers | Annular BOP |

| Ram BOP | |

| Control Heads | |

| Adapter Flanges | |

| Quick Unions | |

| Christmas Tree / Flow Tee | |

| Others (Pack-offs, Lubricators) |

| Low Pressure (less than 10 000 psi) |

| High Pressure (10 000-20 000 psi) |

| Ultra-High Pressure (greater than 20 000 psi) |

| Onshore | Conventional Land Rigs |

| Shale and Tight Formations | |

| Offshore | Shallow-Water |

| Deepwater | |

| Ultra-Deepwater |

| Drilling |

| Completion |

| Intervention / Work-over |

| Production |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Valves | Ball Valves |

| Gate Valves | ||

| Choke Valves | ||

| Check Valves | ||

| Blowout Preventers | Annular BOP | |

| Ram BOP | ||

| Control Heads | ||

| Adapter Flanges | ||

| Quick Unions | ||

| Christmas Tree / Flow Tee | ||

| Others (Pack-offs, Lubricators) | ||

| By Pressure Rating | Low Pressure (less than 10 000 psi) | |

| High Pressure (10 000-20 000 psi) | ||

| Ultra-High Pressure (greater than 20 000 psi) | ||

| By Well Type | Onshore | Conventional Land Rigs |

| Shale and Tight Formations | ||

| Offshore | Shallow-Water | |

| Deepwater | ||

| Ultra-Deepwater | ||

| By Operation Phase | Drilling | |

| Completion | ||

| Intervention / Work-over | ||

| Production | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the pressure control equipment market?

The market is valued at USD 10.31 billion in 2026 and is forecast to reach USD 11.46 billion by 2031.

Which region holds the largest pressure control equipment market share?

North America leads with 38.55% share in 2025 owing to robust shale drilling and Gulf of Mexico projects.

What segment is growing fastest within the market?

Ultra-high-pressure systems (>20 kpsi) are expanding at 3.28% CAGR as deepwater operators target frontier reservoirs.

How are managed pressure drilling technologies influencing demand?

MPD adoption drives control-head sales and replacement cycles by enabling precise bottomhole pressure control and reducing non-productive time.

Why are valves still the largest component segment?

Valves are integral at every well phase; their 32.10% revenue share stems from ubiquity, rapid shutoff capability, and the shift toward smart, self-diagnosing designs.

How does crude-oil price volatility affect equipment purchases?

Low price scenarios delay offshore capex, slowing new-build orders, although replacement and rental demand cushion the impact by keeping existing rigs compliant.

Page last updated on: