Industrial Air Compressors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 41.26 Billion |

| Market Size (2031) | USD 50.61 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

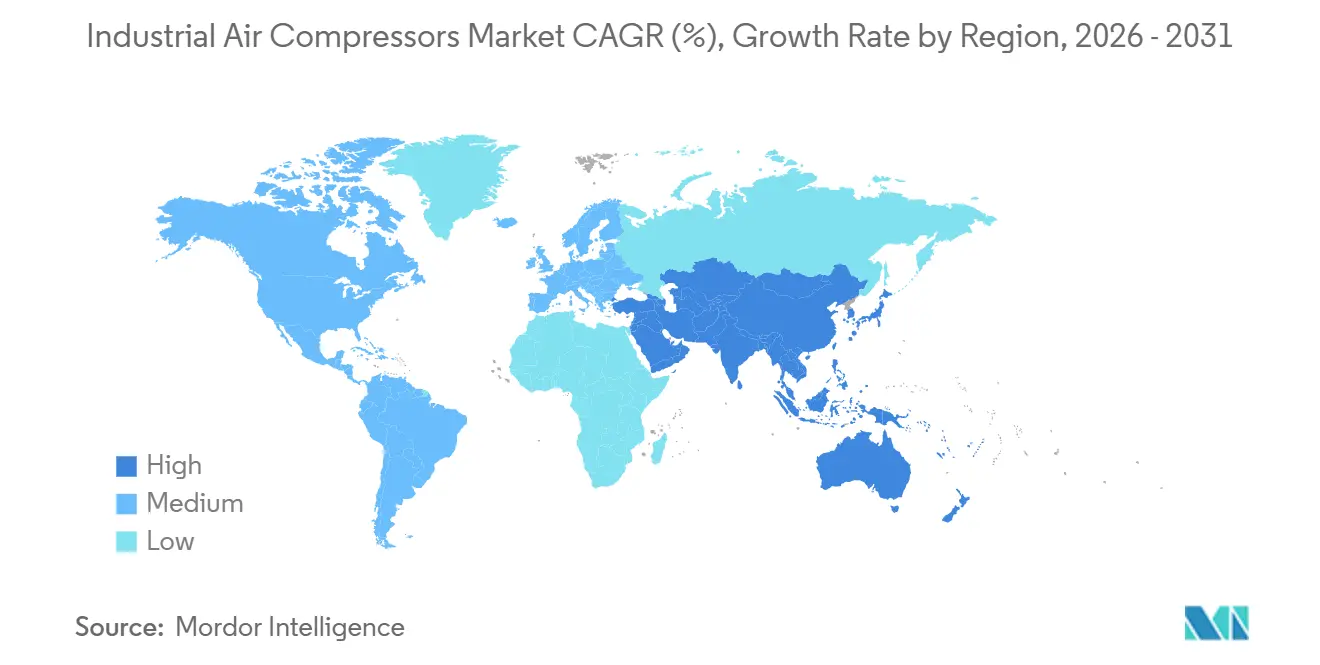

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Air Compressors Market Analysis by Mordor Intelligence

The industrial air compressors market size is expected to increase from USD 41.26 billion in 2026 to USD 50.61 billion by 2031, growing at a CAGR of 4.17% over 2026-2031. Manufacturers are modernizing plants with oil-free, variable-speed units that cut electricity use, satisfy ISO 8573-1 Class 0 purity rules, and integrate smart telemetry for predictive maintenance. Liquefied natural gas (LNG) export terminals and hydrogen refueling hubs are ordering centrifugal trains rated above 100 bar, while government rebates in the United States, Europe, and India accelerate replacement of fixed-speed, oil-flooded systems. Competitive intensity is rising as incumbents purchase niche specialists to secure technology and service adjacencies, and as regional challengers win entry-level share with localized production and aggressive pricing. Steel-price swings, noise-emission rules, and blower substitution in low-pressure duties temper near-term profitability but do not derail long-term growth prospects for high-efficiency, digitally connected compressors.

Key Report Takeaways

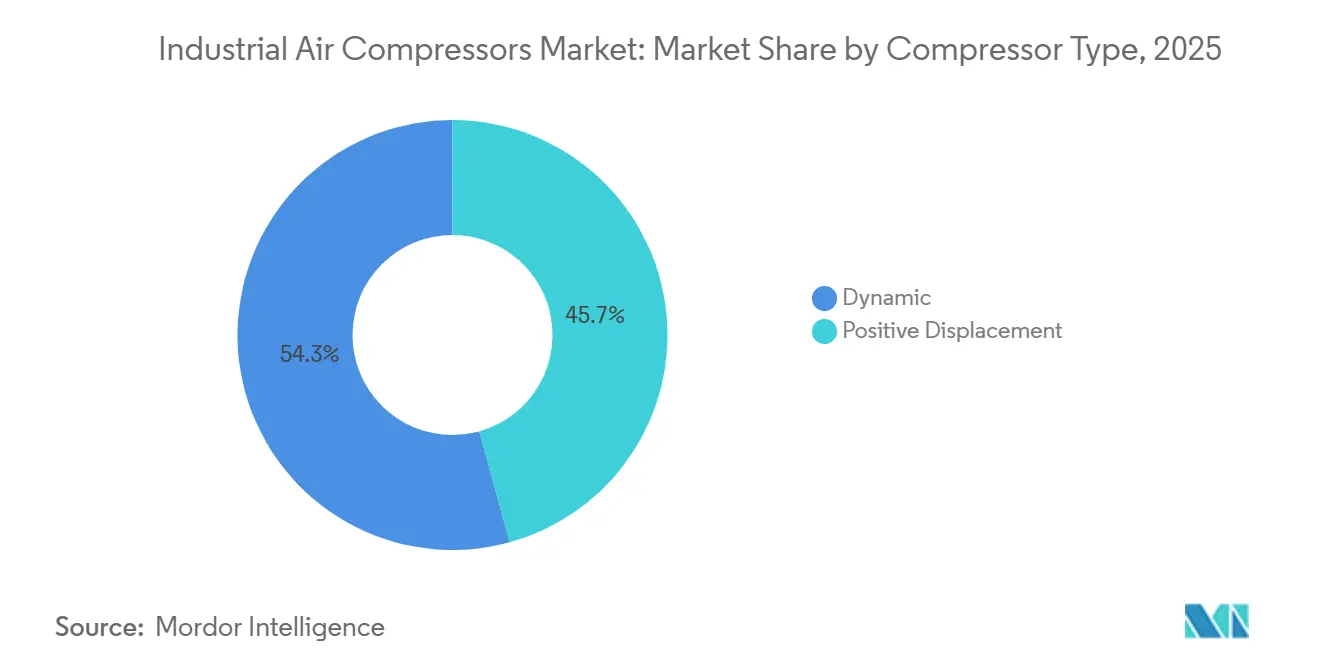

- By compressor type, positive displacement held 45.71% industrial air compressors market share in 2025, whereas dynamic units are the fastest growing at 4.55% CAGR through 2031.

- By lubrication, oil-flooded systems led with 53.48% share in 2025, while oil-free technology posts the highest 4.63% CAGR to 2031.

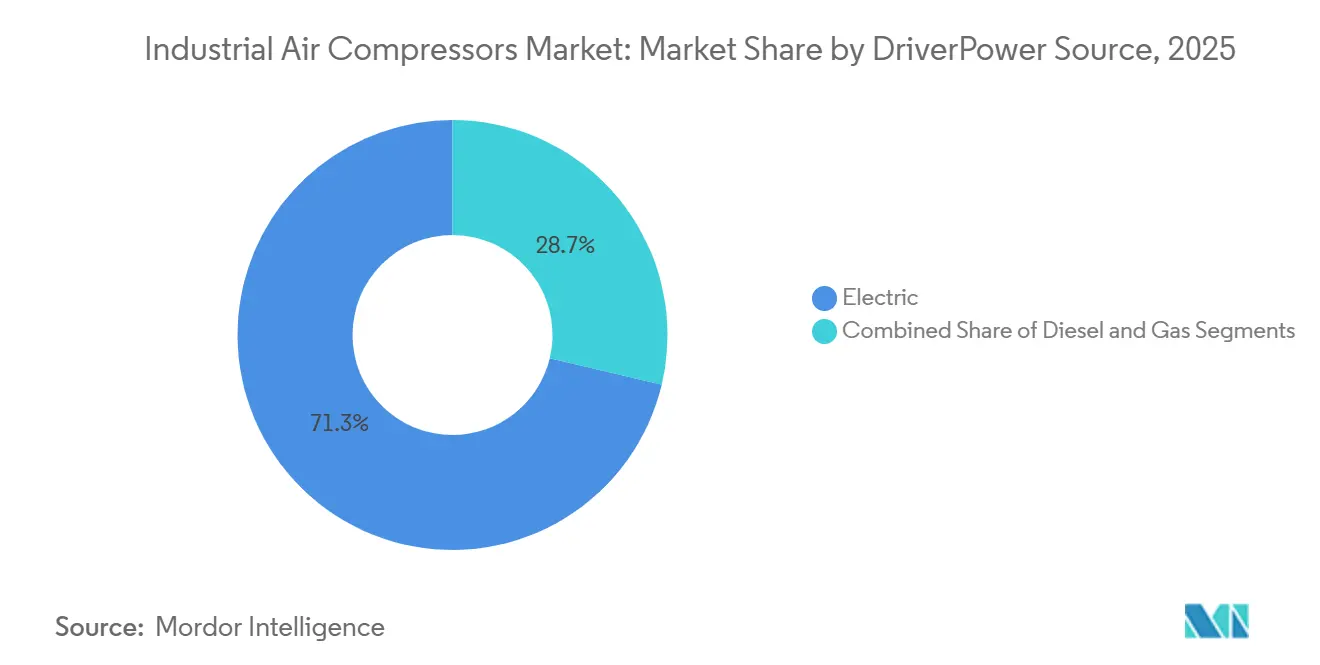

- By driver/power source, electric-powered units captured 71.28% share in 2025 and are advancing at 5.11% CAGR, outpacing diesel and gas alternatives.

- By end-use industry, manufacturing commanded 40.84% of demand in 2025; oil and gas is the quickest growing at 5.28% CAGR during 2026-2031.

- By geography, Asia-Pacific accounted for 42.58% of 2025 revenue and will expand at 5.44% CAGR, the strongest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Air Compressors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Energy-Efficient Manufacturing Facilities in Asia | +1.2% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Rising Demand for Oil-Free Compressors in Food and Beverage Processing | +0.8% | Global, with concentration in Europe and North America | Short term (≤ 2 years) |

| Surging Investments in LNG Infrastructure Requiring High-Pressure Compressors | +0.9% | North America, Middle East, Asia-Pacific (Australia, China) | Long term (≥ 4 years) |

| Government Incentives for Industrial Energy Audits Favoring Variable-Speed Compressors | +0.7% | North America and Europe, emerging in India | Short term (≤ 2 years) |

| Rapid Growth of EV Battery Gigafactories Utilizing Dry Screw Compressors | +0.6% | Asia-Pacific (China, South Korea), North America (United States) | Medium term (2-4 years) |

| Uptick in Brownfield Revamps of Petrochemical Plants in Middle East | +0.5% | Middle East (Saudi Arabia, United Arab Emirates, Qatar) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Energy-Efficient Manufacturing Facilities in Asia

Asian governments are linking power-tariff subsidies and soft loans to the deployment of variable-speed compressors that trim plant electricity bills by up to 35%. India’s ADEETIE program disbursed INR 1,000 crore (USD 122 million) in 2025, lowering payback periods to two years for small and midsize factories upgrading legacy equipment.[1]Ministry of Micro, Small and Medium Enterprises, Government of India, “ADEETIE Scheme Guidelines 2025,” msme.gov.in Multinationals responded: Mitsubishi Electric invested INR 2,100 crore (USD 256 million) in a new Chennai compressor plant, and SKF poured INR 653 crore (USD 80 million) into rotor-bearing output in Pune. These projects anchor a supply chain that favors high-efficiency, digitally monitored air systems. Parallel funding of INR 20,000 crore (USD 2.44 billion) for carbon capture infrastructure ensures long-run demand for ultra-high-pressure reciprocating units. As China’s steel appetite cools, South and Southeast Asian production of automobiles, electronics, and batteries is absorbing compressor capacity vacated elsewhere, sustaining momentum through the medium term.

Rising Demand for Oil-Free Compressors in Food and Beverage Processing

ISO 8573-1 Class 0 became the de facto quality benchmark in 2025, compelling processors to replace oil-flooded screws despite a 20-30% capital premium. Pharmaceutical lines add dew-point and particle sensors that interface with plant MES platforms, digitizing compliance evidence. Atlas Copco, Kaeser, and ELGi logged double-digit order growth for oil-free ranges, noting energy savings up to 30% when paired with variable-speed drives. Regulatory scrutiny from the United States Food and Drug Administration intensified documentation of compressed-air purity, prompting widespread retrofit campaigns. These dynamics elevate oil-free adoption from niche to mainstream across Europe and North America within the next two years.

Surging Investments in LNG Infrastructure Requiring High-Pressure Compressors

Contracts awarded in 2025 for Rio Grande, Commonwealth, and Alaska LNG terminals include multistage centrifugal trains that deliver flows above 10,000 m³ h⁻¹ at pressures over 40 bar. Middle Eastern megacomplexes such as Ras Laffan’s USD 6 billion ethylene project specify reciprocating units exceeding 100 bar for light-hydrocarbon separation. Suppliers leverage digital twins to optimize rotor dynamics and extend overhaul intervals to 48,000 hours, enhancing lifecycle value. As floating LNG and underground storage proliferate, demand for compact, weight-optimized packages capable of 345 bar and higher becomes a long-term growth pillar extending beyond 2030.

Government Incentives for Industrial Energy Audits Favoring Variable-Speed Compressors

United States utilities pay USD 25 per installed horsepower, trimming up-front costs by up to 25% and slashing payback periods from four to under two years. Europe’s Energy Efficiency Directive obliges enterprises to audit energy consumption every four years, after which compressed-air systems are routinely flagged among the top three saving opportunities.[2]European Commission, “Energy Efficiency Directive (Recast) 2025,” europa.eu Australia’s Instant Asset Write-Off accelerated purchasing of premium GA VSD+ units, with Atlas Copco reporting a 22% domestic order lift in 2025. Subsidies, coupled with rising carbon prices, make variable-speed drives the default specification in new capital projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel Prices Inflating Compressor BOM Cost Structures | -0.6% | Global, with acute pressure in Europe and North America | Short term (≤ 2 years) |

| Longer Payback Period Versus Blower Alternatives for Low-Pressure Applications | -0.4% | Global, concentrated in general manufacturing and construction | Medium term (2-4 years) |

| Stringent Noise Emission Norms Escalating Enclosure Costs in Europe | -0.3% | Europe, emerging in urban Asia-Pacific markets | Medium term (2-4 years) |

| Skilled Maintenance Labor Shortages Increasing Downtime in Emerging Markets | -0.3% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel Prices Inflating Compressor BOM Cost Structures

OECD data show 165 million t of new capacity entering service through 2027, amplifying price swings that squeeze gross margins.[3]EUROFER, “Economic and Steel Market Outlook 2025-2026,” eurofer.eu European mills running at 65% utilization confront both energy-cost inflation and weak demand, while Asian exporters discount surplus tonnage, creating a whiplash effect on specialty alloy surcharges. OEMs respond by dual-sourcing castings, redesigning housings for weight reduction, and hedging futures to stabilize quotations. Nevertheless, short-cycle project budgets remain vulnerable to 10-15% swings in casing and crankshaft input costs.

Longer Payback Period Versus Blower Alternatives for Low-Pressure Applications

Centrifugal blowers achieve similar flow at one-third the maintenance spend below 1 bar, trimming payback by up to 18 months. Contractors favor portable blower skids that weigh 30% less than reciprocating compressors, lowering transport fees. Where air quality is non-critical, Asian SMEs opt for locally made blowers priced 40-50% below imported screws. Global OEMs must either localize production or concede this low-pressure niche, capping growth in mature factory-air segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Compressor Type: Dynamic Units Extend High-Flow Reach

Positive displacement machines commanded 45.71% of the industrial air compressors market in 2025, anchored by rotary screws that dominate 7-13 bar duties in automotive, metalworking, and packaging plants. Their continuous operation, compact skid design, and variable-speed compatibility satisfy lean-manufacturing uptime targets. Reciprocating pistons remain indispensable for bottle blowing and CNG vehicle refueling but face maintenance-intensive duty cycles that limit widespread uptake. Scroll designs thrive in laboratories and hospitals where oil-free air, low noise, and minimal vibration outweigh their 2 m³ min⁻¹ flow ceiling.

Dynamic compressors, chiefly centrifugal, are projected to advance at 4.55% CAGR through 2031 as LNG, hydrogen, and petrochemical megaprojects demand flows above 10,000 m³ h⁻¹ and pressures beyond 40 bar. Siemens Energy and Baker Hughes both landed multi-train awards in 2025 that showcased digital-twin rotor optimization and predictive diagnostics. Axial stages remain niche in turbine air separation, limiting broader market penetration but underscoring dynamic technology’s edge in ultra-high-volume services where positive-displacement solutions become uneconomical.

By Lubrication: Oil-Free Purity Gains Critical Mass

Oil-flooded models retained 53.48% share in 2025 on lower capex and tolerance of dusty, high-temperature environments. Lubricated screws between 75 and 250 kW are plant utilities’ workhorse, with five-year service intervals and parts availability driving loyalty among maintenance managers. Conversely, oil-free installations are tracking a 4.63% CAGR, supported by ISO 8573-1 Class 0 mandates at pharmaceutical, semiconductor, and beverage sites. Gardner Denver lifted its oil-free ceiling to 290 kW, reporting 13% efficiency gains from new rotor coatings, while Atlas Copco telemetry shows 30% energy savings when oil-free screws pair with leak-tracking analytics.

Lifecycle cost math now favors oil-free where product contamination risks exceed USD 0.5 million per recall. Semiconductor fabs in Taiwan and South Korea specify oil-free screws exclusively, citing wafer yield protection. The industrial air compressors market size for oil-free segments is set to widen as Class 0 becomes the norm rather than the exception in critical-process industries.

By Driver/Power Source: Grid Electrification Accelerates

Electric-drive units dominated with 71.28% share in 2025, propelled by falling grid carbon intensity and rebates that offset variable-speed premiums. Programs from ComEd, Mass Save, and DTE slash capex by up to 25%, while U.S. federal incentives add USD 25 per horsepower, driving retrofit surges in food processing and metal fabrication. Diesel remains indispensable on remote mines and construction sites but is eroding as battery-powered portables like Atlas Copco’s B-Air 185-12 meet urban noise and emissions codes. Gas turbine-driven packages serve refineries that harness waste fuel but face decarbonization headwinds and capital complexity.

Battery-powered mobile compressors represent an emerging micro-segment, offering silent operation and overnight charging at off-peak tariffs that undercut diesel by 60%. As density improves, electric portables are expected to chip away at the 185-350 cfm rental class from 2028 onward, deepening electrification’s march across the industrial air compressors market.

By Pressure Rating: Ultra-High-Pressure Adoption Climbs

Units above 100 bar, though small in number, are tracking a 4.38% CAGR in hydrogen mobility, CNG stations, and carbon sequestration projects. HOERBIGER announced in October 2025 that it will supply three HCP 500 hydrogen compressor packages to the 105 MW Hamburg Green Hydrogen Hub, with each unit capable of compressing more than 250 kilograms per hour to pressures suitable for trailer filling and heavy-duty vehicle refueling.

European Union regulations mandate hydrogen refueling stations at urban nodes and every 200 kilometers along the Trans-European Transport Network by 2030, while the Fuel Cell and Hydrogen Energy Association projects that approximately 4,300 United States stations will be needed by 2030, creating sustained demand for high-pressure reciprocating and diaphragm compressors. Mid-range 21-100 bar machines service industrial gas plants and refrigeration loops with steady replacement demand but modest growth. Low-pressure 0-20 bar segments are being replaced by centrifugal blowers for aeration and conveying, constraining their long-term growth trajectory.

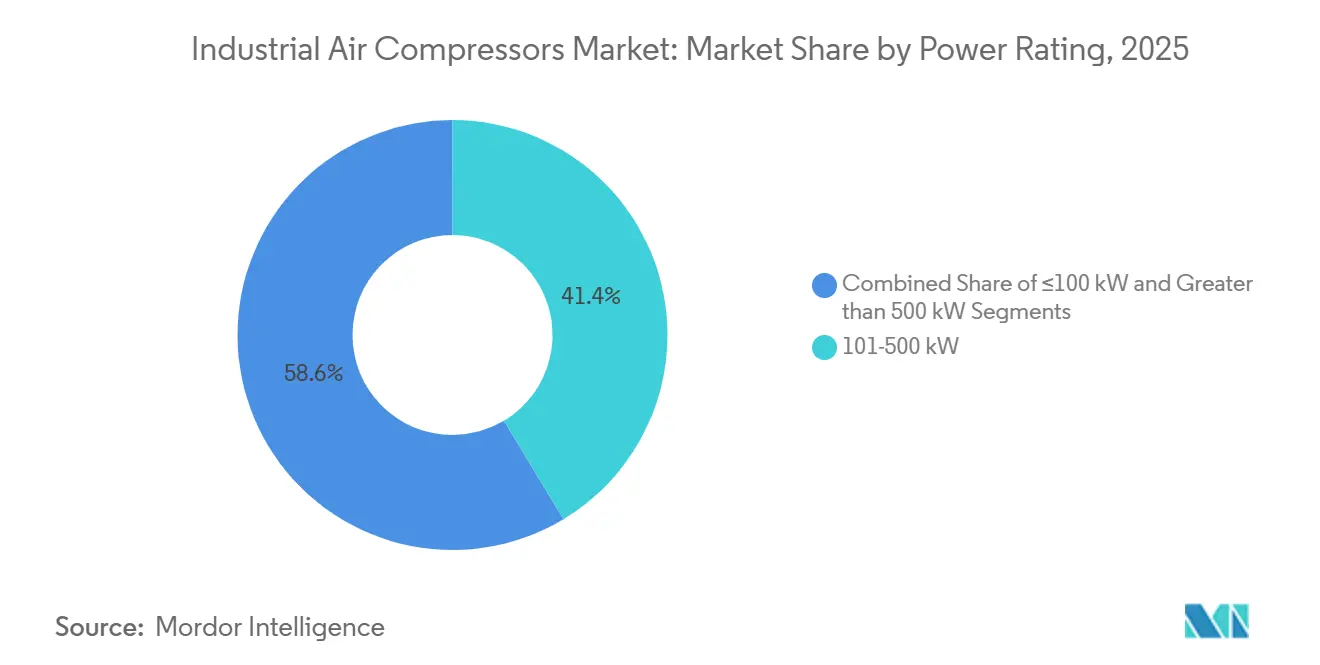

By Power Rating: Mega-Watt Classes Serve Data Centers and Hydrogen Hubs

Compressors over 500 kW advance at 4.85% CAGR, fuelled by data-center cooling and multi-megawatt electrolyzer complexes that inject hydrogen into pipelines. QatarEnergy’s Ras Laffan petrochemical megaproject will commission multi-MW reciprocating units by 2027, validating scale economics. Mid-range 51-250 kW machines, representing 41.37% of 2025 shipments, gain from mature variable-speed ecosystems that optimize part-load efficiency.

Compressors rated at 100 kW or less serve small workshops, automotive repair shops, and distributed manufacturing facilities, representing a fragmented, price-sensitive segment in which local suppliers compete on delivery speed and service responsiveness. This segment is mature in North America and Europe, with replacement demand driven by equipment age-out and regulatory mandates for energy-efficient models, yet it remains a growth opportunity in Asia-Pacific and South America, where industrialization is expanding the installed base

By End-Use Industry: Oil and Gas Emerges as Fastest Riser

Manufacturing retained 40.84% share in 2025 but inches forward as automation trims pneumatic tool counts. Electronics assembly boosts oil-free screws, yet cyclical semiconductor capex injects volatility. Oil and gas end-users are forecast to expand at 5.28% CAGR from 2026 to 2031, the fastest among all industries, propelled by upstream drilling activity in North American shale basins, midstream pipeline projects that compress natural gas for long-distance transport, and downstream refining and petrochemical brownfield revamps in the Middle East.

Food and beverage, pharmaceutical, and construction end-users represent stable, mature segments with steady replacement demand, yet their growth rates lag the overall market as efficiency gains reduce compressed air consumption per unit of output and as alternative technologies-such as electric actuators and hydraulic systems-displace pneumatic equipment in selected applications.

Geography Analysis

Asia-Pacific generated 42.58% of 2025 revenue and is projected to rise at 5.44% CAGR, bolstered by Indian and South Korean battery gigafactories and Chinese petrochemical expansions that specify oil-free, variable-speed systems. Government schemes disbursing more than USD 2.5 billion in concessional finance catalyze factory retrofits, while domestic vendors scale localized rotor casting and motor windings to shorten lead times. The industrial air compressors market size in the region also benefits from supply-chain shifts as electronics, textiles, and auto parts producers diversify away from coastal China, erecting new compressed-air infrastructure in inland China, Vietnam, and Indonesia.

North America rides LNG build-out and reshoring of durable-goods production. Federal and utility rebates slash retrofit paybacks, igniting a wave of fixed-speed replacements at Midwest metalformers and Southeast food processors. U.S. compressor OEMs record fuller order books for oil-free ranges as FDA monitoring rules tighten, while Canadian midstream operators expand CNG corridor networks that demand redundant reciprocating skids to guarantee 98% uptime. Mexico’s maquiladora sector is adopting electric portables to meet stricter urban emissions caps, nudging the region toward higher electrification rates.

Europe confronts steel-cost volatility and stringent noise codes that inflate enclosure spend, yet energy-audit mandates sustain investment in high-efficiency screws. German and Italian SMEs tap EU carbon-transition funds to upgrade 1990s-era machines, while Scandinavian pulp mills adopt centrifugal blowers for aeration, trimming lower-pressure compressor demand. Hydrogen-backed industrial decarbonization plans, anchored by projects such as Hamburg’s 100 MW hub, signal a coming uptick in ultra-high-pressure sales from 2027 onward.

Middle East and Africa gain momentum from petrochemical brownfield revamps in Saudi Arabia and the United Arab Emirates, coupled with emerging hydrogen exports that require 350-700 bar packages. South America remains fragmented; Brazil’s bio-CNG network fuels localized compressor demand, but currency volatility and skills shortages restrain advanced system adoption elsewhere.

Competitive Landscape

The industrial air compressors market is moderately concentrated: the top five vendors hold a considerable share of global revenue. Atlas Copco deepened its pump adjacency by acquiring LEWA and Geveke for EUR 294 million (USD 332 million) and strengthened Southeast U.S. service reach with the January 2026 purchase of Air Compressor Works. Ingersoll Rand executed seven takeovers from late 2024 to late 2025, most notably Italy’s TMIC and Adicomp for EUR 160 million (USD 181 million), securing renewable natural gas know-how. Kaeser emphasizes organic growth, expanding its Virginia plant by 80,000 ft² and debuting Stage V-compliant portables for mining and construction.

Digitalization differentiates incumbents. Atlas Copco’s SMARTLINK uploads five-minute interval data, promising 30% power savings and 3% uptime gains under Energy Performance contracts. Burckhardt Compression’s April 2025 Predictive Intelligence add-on to PROGNOST-NT applies machine learning to detect valve leakages before vibration thresholds spike, reducing unplanned outages. Meanwhile, regional challengers such as ELGi and Boge undercut premium brands by 15-25% through localized manufacturing in India and Eastern Europe, compelling multinationals to adopt dual-brand strategies.

White-space races center on hydrogen mobility and battery-electric portables. Siemens Energy secured January 2026 orders for two centrifugal hydrogen packages at Hamburg’s green hub, while HOERBIGER supplies three HCP 500 reciprocating units, each compressing 250 kg h⁻¹. Atlas Copco’s B-Air prototype targets the 185 cfm rental class with lithium-iron-phosphate batteries, staking an early claim on zero-emission urban construction. These innovations, alongside electrochemical metal-hydride concepts at TRL 6-7, hint at a shifting competitive rubric that weights lifecycle carbon and digital uptime over up-front price.

Industrial Air Compressors Industry Leaders

Ingersoll Rand Inc.

Atlas Copco Group

Gardner Denver Inc.

Kaeser Kompressoren SE

Doosan Portable Power

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Atlas Copco acquired Air Compressor Works, a Florida distributor with USD 16 million revenue and 50 staff, expanding its southeastern U.S. aftermarket reach.

- January 2026: Siemens Energy won a contract for two hydrogen compressor packages for the 100 MW Hamburg Green Hydrogen Hub, with startup set for 2H 2027.

- November 2025: Ingersoll Rand purchased Transvac Systems in the United Kingdom, adding ejector technology for vacuum and low-pressure niches.

- November 2025: Kaeser launched the M480 portable compressor, powered by a 343 kW Cummins diesel, aimed at heavy civil and mining contractors.

Global Industrial Air Compressors Market Report Scope

The Industrial Air Compressors Market refers to the market for compressors used in industrial applications to convert power into potential energy stored in pressurized air. These compressors are essential for various industries, including manufacturing, oil and gas, power generation, chemical and petrochemical, food and beverage, pharmaceutical, construction, and others.

The Industrial Air Compressors Market Report is Segmented by Compressor Type (Positive Displacement and Dynamic), Lubrication (Oil-Flooded and Oil-Free), Pressure Rating (0-20 bar, 21-100 bar, and Above 100 bar), Driver/Power Source (Electric, Diesel, Gas), Power Rating (≤100 kW, 101-500 kW, and Greater than 500 kW), End-use Industry (Manufacturing, Oil and Gas, Power Generation, Chemical and Petrochemical, Food and Beverage, Pharmaceutical, Construction, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Positive Displacement | Rotary Screw |

| Reciprocating (Piston) | |

| Scroll | |

| Dynamic | Centrifugal |

| Axial |

| Oil-Flooded |

| Oil-Free |

| 0-20 bar |

| 21-100 bar |

| Above 100 bar |

| Electric |

| Diesel |

| Gas |

| ≤100 kW |

| 101-500 kW |

| Greater than 500 kW |

| Manufacturing | General Manufacturing |

| Metal and Mining | |

| Electronics and Semiconductors | |

| Oil and Gas | Upstream |

| Midstream (Pipeline/LNG) | |

| Downstream (Refining) | |

| Power Generation | |

| Chemical and Petrochemical | |

| Food and Beverage | |

| Pharmaceutical | |

| Construction | |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Compressor Type | Positive Displacement | Rotary Screw |

| Reciprocating (Piston) | ||

| Scroll | ||

| Dynamic | Centrifugal | |

| Axial | ||

| By Lubrication | Oil-Flooded | |

| Oil-Free | ||

| By Pressure Rating | 0-20 bar | |

| 21-100 bar | ||

| Above 100 bar | ||

| By Driver/Power Source | Electric | |

| Diesel | ||

| Gas | ||

| By Power Rating | ≤100 kW | |

| 101-500 kW | ||

| Greater than 500 kW | ||

| By End-use Industry | Manufacturing | General Manufacturing |

| Metal and Mining | ||

| Electronics and Semiconductors | ||

| Oil and Gas | Upstream | |

| Midstream (Pipeline/LNG) | ||

| Downstream (Refining) | ||

| Power Generation | ||

| Chemical and Petrochemical | ||

| Food and Beverage | ||

| Pharmaceutical | ||

| Construction | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for industrial air compressors be by 2031?

The industrial air compressors market is forecast to reach USD 50.61 billion by 2031, expanding at a 4.17% CAGR from 2026.

Which compressor type is growing fastest?

Dynamic, primarily centrifugal units, post the strongest 4.55% CAGR through 2031 because LNG terminals and hydrogen hubs require high-flow, high-pressure capability.

Why are oil-free compressors gaining share in food and pharma plants?

ISO 8573-1 Class 0 purity rules and tighter FDA monitoring compel processors to eliminate hydrocarbon carryover, boosting oil-free demand despite higher capex.

Which region leads future growth?

Asia-Pacific advances at 5.44% CAGR as India, China, and South Korea add energy-efficient factories and battery gigafactories that specify oil-free, variable-speed systems.

Page last updated on: