Hydraulic Cylinder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

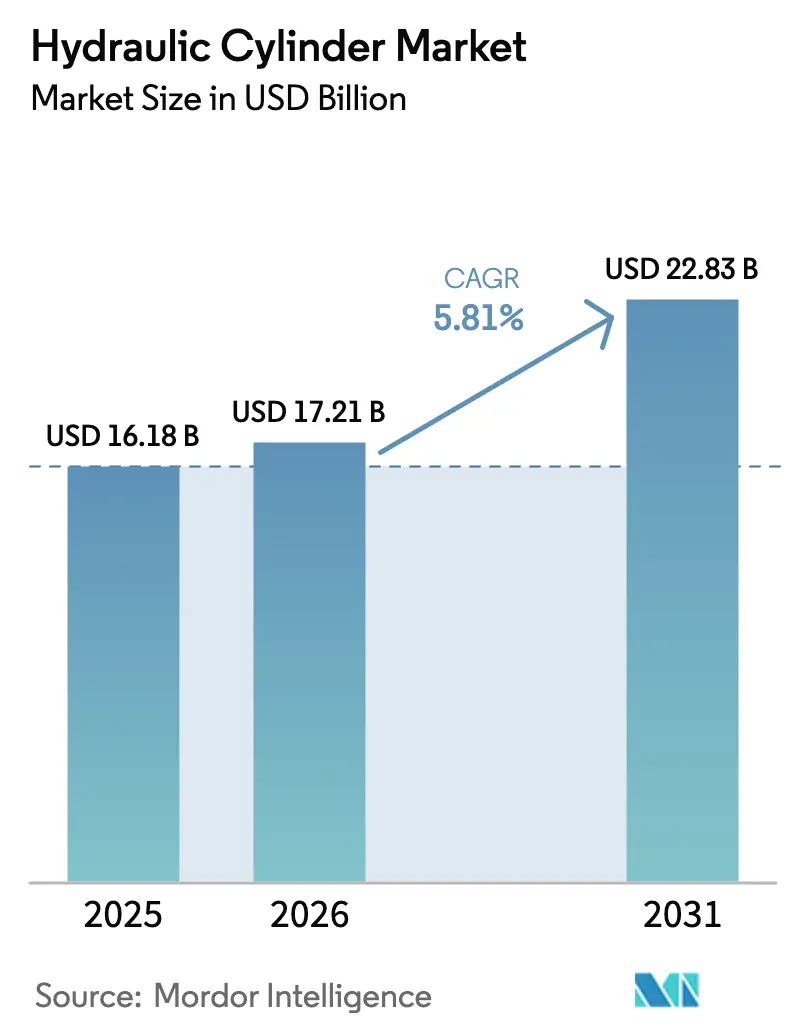

| Market Size (2026) | USD 17.21 Billion |

| Market Size (2031) | USD 22.83 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

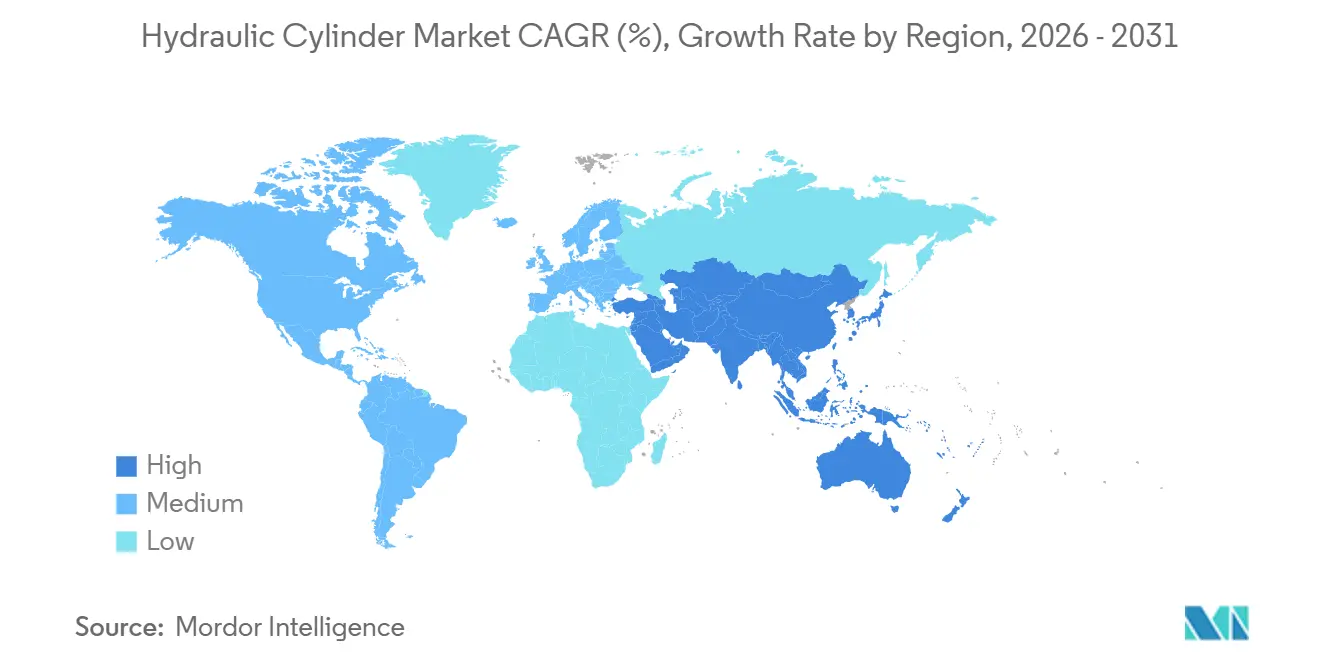

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydraulic Cylinder Market Analysis by Mordor Intelligence

The hydraulic cylinder market size is projected to expand from USD 16.18 billion in 2025 and USD 17.21 billion in 2026 to USD 22.83 billion by 2031, registering a CAGR of 5.81% between 2026 and 2031. Sustained public-works spending, farm mechanization across emerging economies, and e-commerce driven warehouse automation are the principal forces behind this trajectory. Double-acting cylinders dominate heavy-duty equipment, while single-acting designs are gaining traction in cost-sensitive material handlers. Warehouse operators are specifying compact cylinders that tolerate high duty cycles, and OEMs are shifting toward electro-hydraulic “smart” designs that bundle sensors and firmware for condition-based maintenance. Regional demand continues to pivot toward Asia Pacific, yet the Middle East is emerging as the fastest growing geography as Saudi Arabia and the UAE advance multi-billion-dollar infrastructure programs.

Key Report Takeaways

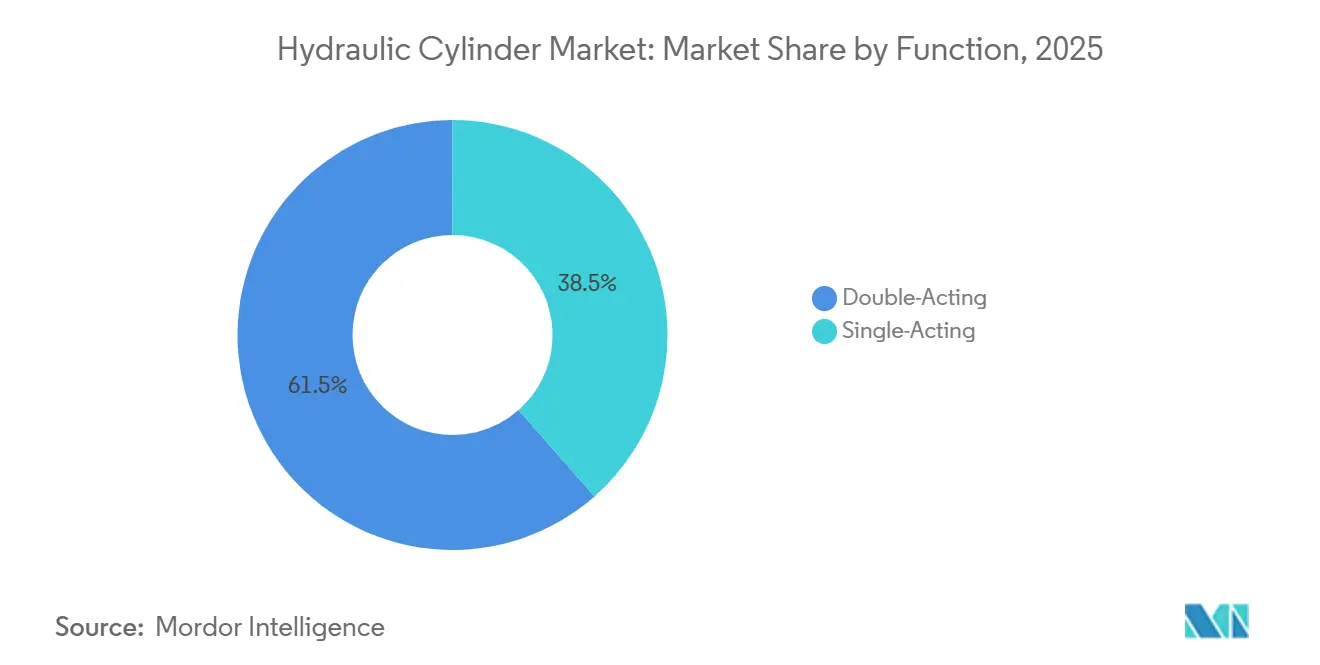

- By function, double-acting cylinders led with 61.48% of the hydraulic cylinder market share in 2025, whereas single-acting cylinders are forecast to advance at a 5.97% CAGR through 2031.

- By specification, welded cylinders held 47.92% revenue share in 2025, while telescopic designs are projected to expand at a 6.02% CAGR to 2031.

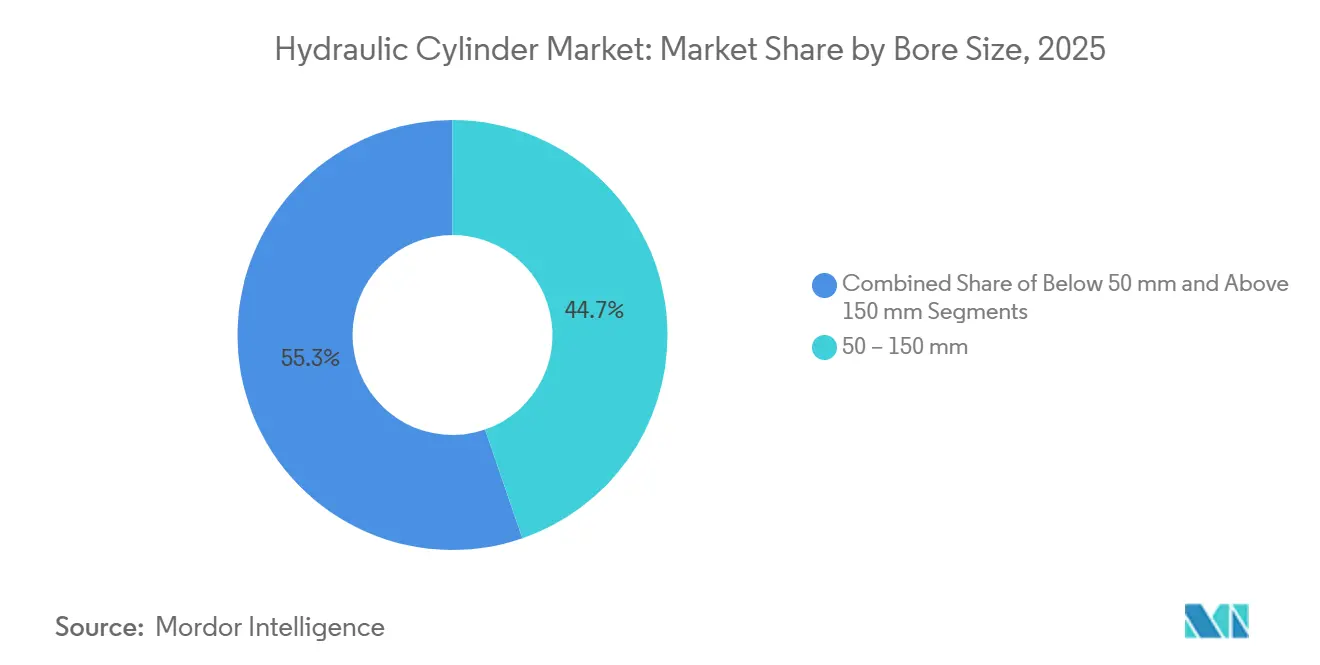

- By bore size, cylinders with 50-150 mm bores captured 44.73% share of the hydraulic cylinder market size in 2025, and units above 150 mm bores are forecast to rise at a 5.91% CAGR through 2031.

- By end-user industry, construction equipment accounted for 27.63% share in 2025, whereas industrial manufacturing is anticipated to record the highest CAGR at 6.12% up to 2031.

- By geography, Asia Pacific commanded 42.57% revenue share in 2025, but the Middle East is set to grow at a 6.18% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydraulic Cylinder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure and Construction-Equipment Boom | +1.8% | Global, with concentration in Asia Pacific (India, China) and Middle East (Saudi Arabia, UAE) | Medium term (2-4 years) |

| Rising Farm Mechanization in Developing Regions | +1.2% | Asia Pacific (India, Southeast Asia), South America (Brazil, Argentina), Africa | Long term (≥ 4 years) |

| E-Commerce-Led Surge in Warehouse Material-Handling Automation | +1.0% | North America, Europe, Asia Pacific (China, Japan) | Short term (≤ 2 years) |

| Shift Toward Electro-Hydraulic "Smart" Cylinders in Mobile Machinery | +0.9% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Growing Use Of Hydraulic Cylinders in Wind-Turbine Pitch Control | +0.6% | Europe (offshore wind), North America, Asia Pacific (China) | Long term (≥ 4 years) |

| Recovery of Aerospace and Defense Production Cycles | +0.4% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure and Construction-Equipment Boom

Government-led infrastructure programs are redefining cylinder demand across emerging markets, with India's construction equipment sector shipping 140,191 units in fiscal 2025- up from 107,624 units in fiscal 2023- driven by metro rail expansions, expressway construction, and urban housing schemes.[1]Indian Construction Equipment Manufacturers' Association, “Construction Equipment Industry Statistics,” icema.in China's Belt and Road Initiative awarded USD 70.7 billion in construction contracts during 2024, with transport infrastructure (rail USD 9.6 billion, roads USD 3.1 billion) and energy projects (USD 24.3 billion in oil and gas) requiring excavators, loaders, and cranes equipped with high-pressure welded cylinders. OEMs investing in local content, such as indigenous piston pump programs, shorten lead times and mitigate import costs. These trends collectively extend replacement cycles and enlarge the installed base of serviceable cylinders.

Rising farm mechanization in developing regions

Farm wages and labor shortages are accelerating the adoption of tractors and harvesters across India, Southeast Asia, and Sub-Saharan Africa. India's National Bank for Agriculture and Rural Development reported tractor sales exceeding 900,000 units annually, with hydraulic cylinders integral to front-end loaders, backhoe attachments, and three-point linkages.[2]National Bank for Agriculture and Rural Development, “Agricultural Finance Statistics,” nabard.orgSubsidies and microfinance packages are lowering capital barriers for smallholders, boosting penetration of bore sizes between 50 mm and 80 mm. Export-oriented Brazilian OEMs are adding ISO 6020-1 compliant tie-rod cylinders to sugarcane harvesters shipped across South America and Africa. Intensifying irrigation projects further raise cylinder demand in center-pivot systems that rely on automated valve and boom actuation.

E-Commerce-Led Surge in Warehouse Material-Handling Automation

Same-day delivery norms are prompting fulfillment centers to deploy automated storage and retrieval systems, narrow-aisle forklifts, and conveyor lifts that count on compact high-cycle cylinders. Mast cylinders conforming to ISO 6020-2 enable vertical reaches above 10 m in congested racking layouts, while down-safety valves remain a mandatory feature under ISO 10100. Modular electric PTO packages pairing battery drives with hydraulic cylinders let operators decouple from fixed hydraulic power units and extend shift runtimes. These solutions are scaling fastest in North America and Europe, and China’s parcel volume ensures Asia Pacific stays close behind.

Shift Toward Electro-Hydraulic Smart Cylinders in Mobile Machinery

OEMs are embedding sensors, edge processors, and wireless connectivity inside cylinder housings to harvest pressure, position, and temperature data. Smart cylinders interfacing with fleet telematics cut unplanned downtime by roughly a third, fostering interest among rental companies that monetize uptime guarantees. Suppliers with vertical integration across valves, pumps, and software are best placed to co-engineer full electro-hydraulic systems. New excavator and loader design cycles scheduled for 2026-2028 already list over-the-air firmware updates and predictive seal monitoring as core requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of Electric Actuators In Light-Duty Applications | -0.7% | Global, particularly North America and Europe in automotive and robotics | Short term (≤ 2 years) |

| Volatile Steel Prices Inflating Cylinder Cost Structure | -0.5% | Global, with acute impact in Europe and North America | Medium term (2-4 years) |

| Chronic Maintenance and Leakage Issues in Legacy Systems | -0.3% | Global, concentrated in aging fleets in North America and Europe | Long term (≥ 4 years) |

| Cyclical CAPEX In Mining and Oil And Gas Sectors | -0.4% | North America (shale), Middle East, Africa, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Electric Actuators in Light-Duty Applications

Automotive, electronics, and collaborative robot builders increasingly specify fully electric linear actuators for thrusts below 5 kN. These units eliminate fluid plumbing, trim energy bills, and simplify maintenance, allowing payback inside two years for high-cycle tasks. As electric vehicle assembly lines reduce hydraulic content, suppliers exposed to sub-50 mm bore single-acting cylinders face volume erosion. Nevertheless, applications that exceed 100 kN or demand shock-load absorption in dirt and debris filled environments continue to lean on hydraulic power.

Volatile Steel Prices Inflating Cylinder Cost Structure

Steel constitutes nearly half of a cylinder’s production cost, and price gyrations can erase margins on annual supply contracts. European Union steel consumption declined in 2024, yet prices remained elevated due to energy-cost inflation and capacity rationalization, compressing margins for cylinder manufacturers unable to pass costs through to OEM customers locked into annual supply agreements.[3]OECD Steel Committee, “Steel Market Developments,” oecd.org Welded cylinders that depend on thick seamless tubing suffer the sharpest cost swings. Manufacturers counter by qualifying high-strength alloys that shave wall thickness, integrating captive tube mills, and adopting finite element techniques to optimize material use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Bidirectional Designs Command Heavy Equipment

Double-acting cylinders retained 61.48% share of the hydraulic cylinder market in 2025 thanks to universal use across excavators, wheel loaders, and mining shovels. These units generate controlled push-pull forces for bucket curl, boom lift, and steering functions that dominate duty cycles in earthmoving fleets. The hydraulic cylinder market for single-acting units is expanding as cost-focused agricultural implements, dock levelers, and truck hoists leverage gravity or spring returns to simplify circuitry. OEM standardization on ISO 6020 mounting patterns keeps aftermarket interchangeability easy, and the integration of load-holding valves protects workers on elevated work platforms.

Manufacturers are pursuing coatings that lengthen rod life in abrasive soils, while blade-position cylinders in bulldozers add redundant seals to survive high shock loads. Wind-turbine builders now specify double-acting pitch cylinders with integrated position transducers, underscoring the design’s adaptability to smart control schemes.

By Specification: Welded Robustness Meets Telescopic Reach

Welded designs captured 47.92% share during 2025 and remain the default for equipment exposed to vibration, side loads, and dirt ingress. Eliminating tie rods allows slimmer barrels that fit tight machinery envelopes, and weld integrity supports pressures reaching 35 MPa. In parallel, telescopic cylinders are advancing at a 6.02% CAGR because urban construction demands long strokes inside compact machines. A five-stage telescopic model can extend 6 m while retracting to 1.5 m, enabling dump trucks to unload below pedestrian bridges without contact.

The hydraulic cylinder market size attributable to tie-rod units is steady in stationary presses and molding machines where fast seal swaps outweigh envelope constraints. Mill-type cylinders satisfy niche steel and paper mill roles that demand square heads and rugged guides. Suppliers now exploit finite element simulations to reduce stage overlap in telescopic models and trim weight, a critical factor as battery powered machinery gains share.

By Bore Size: Mid-Range Dominates, Large Bores Accelerate in Mining

Large-bore cylinders, defined as units with diameters above 150 mm, are expanding at a 5.91% CAGR through 2031 as ultra-class mining trucks, offshore drilling rigs, and utility-scale wind turbines demand higher thrust capacities. These heavy-duty cylinders feature thicker rod diameters, chrome-plated surfaces, and composite wipers that withstand abrasive dust and salt-spray exposure common at mine and offshore sites. Operators value the shock-load absorption and overload protection that hydraulic systems deliver when hauling 290-ton payloads or maneuvering blades on 15 MW wind turbines.

At the other end of the spectrum, compact cylinders below 50 mm are holding niche positions in precision agriculture, food processing, and mobile robotics where clean-room compatibility and repeatability matter more than raw force. This cohort’s vulnerability to electric actuators is prompting hydraulic vendors to integrate micro-sensors and low-leakage seals that boost efficiency and reduce oil mist. Across all size classes, OEMs increasingly specify ISO 3320 bore/rod combinations to streamline global sourcing and lower downtime. The widespread adoption of standard sizing simplifies aftermarket stocking and helps distributors keep critical spares close to remote mines and wind farms.

By End-User Industry: Construction Equipment Leads, Industrial Manufacturing Accelerates

Construction equipment accounted for 27.63% of the hydraulic cylinder market size in 2025, reflecting robust excavator, wheel loader, and bulldozer demand tied to road, rail, and metro projects across the Asia Pacific and the Middle East. High-pressure welded cylinders handle bucket curl, boom lift, and blade tilt cycles that can exceed 3,000 psi, so OEMs prioritize heat-treated rods and induction-hardened eyes to prevent fatigue failures on job sites. Government stimulus packages and public-private partnerships are lengthening order backlogs, while compact urban machinery is shifting toward telescopic stages that extend reach without exceeding transport height limits.

Industrial manufacturing is poised for the fastest expansion, with a 6.12% CAGR through 2031, as smart-factory investments drive the installation of hydraulic presses, injection-molding machines, and test rigs equipped with electro-hydraulic cylinders that report real-time stroke, pressure, and temperature data to plant MES platforms. Agriculture provides a steady, recurring demand for single-acting hitch, lift, and steering cylinders, though year-to-year swings in commodity prices influence OEM production schedules. Aerospace and defense are recovering, with aircraft build rates improving and military vehicle programs adding blast-resistant suspension cylinders. Marine and offshore oil applications require class-approved mill-type cylinders that resist corrosion and shock, yet spending remains selective in the face of volatile energy prices.

Geography Analysis

Asia-Pacific secured 40.62% of 2025 revenue and records an 6.73% CAGR, driven by megaprojects such as India’s high-speed rail corridors and China’s offshore wind build-out. Domestic champions like Hengli scale vertically integrated plants to replace imported high-end cylinders, trimming lead times and landed costs. Supplier proximity also aligns with just-in-time practices adopted by regional OEMs.

North America ranks second, buoyed by federal infrastructure spending that refreshes construction fleets and upgrades inland-port material-handling systems. Local producers differentiate through advanced metallurgy and digital integration, meeting end-user demand for data-rich equipment as predictive maintenance adoption rises.

Europe emphasizes sustainability and noise reduction, prompting the uptake of smart electro-hydraulic designs that curtail energy waste. OEMs receive legislative stimulus from EU Green Deal directives, spurring orders for cylinders with biodegradable fluids and leak-prevention technologies. The Middle East sees demand swings tied to oil-price cycles, but gas-processing expansion in Saudi Arabia revives large-bore cylinder orders for pipeline construction. Africa and Latin America benefit from agricultural mechanization subsidies and mining concessions, though currency volatility challenges importers. Across all regions, suppliers that offer localized service networks and rapid spare-parts fulfillment gain advantage in the hydraulic cylinder market.

Competitive Landscape

The hydraulic cylinder market is moderately fragmented: the top five vendors account for a considerable share of global revenue, leaving mid-tier specialists room to thrive. Parker-Hannifin, Bosch Rexroth, and Caterpillar offer full-stack motion-control portfolios encompassing cylinders, pumps, valves, and digital controllers, enabling OEMs to source integrated systems rather than discrete components. Acquisition pipelines illustrate this strategy: Bosch Rexroth’s purchase of HydraForce fuses compact-valve expertise with global manufacturing scale to accelerate smart-hydraulics rollouts.

Private-equity plays also reshape the field. Fortress Investment Group consolidated Texas Hydraulics, Hydromotion, and Oilgear to create a diversified platform spanning large-bore and high-precision niches, targeting industrial and energy customers seeking one-stop sourcing. Applied Industrial Technologies’ Hydradyne buy expands its technical-services footprint, positioning the distributor to bundle engineering support with components and thereby deepen customer stickiness.

Suppliers race to embed telematics and cloud APIs, converting cylinders into data nodes that feed uptime dashboards. First-movers can monetize subscription analytics, capturing aftermarket annuities that lift lifetime margins beyond the initial sale. Competition therefore pivots from price to life-cycle value, encouraging continuous investment in sensor fusion, edge computing, and materials science throughout the hydraulic cylinder market.

Hydraulic Cylinder Industry Leaders

Bosch Rexroth AG

Parker-Hannifin Corporation

Eaton Corporation plc

SMC Corporation

KYB Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Airbus delivered 766 aircraft in 2025, sustaining demand for flight-control and landing gear cylinders.

- January 2025: Boeing shipped 56 aircraft in December 2025, capping the year at 348 deliveries as 737 MAX production challenges linger.

- January 2026: GE Vernova disclosed plans to cut up to 900 onshore wind jobs, signaling slower pitch-control cylinder orders.

- February 2025: KYB dissolved its Indian concrete equipment joint venture, pivoting toward excavator and industrial cylinders.

Global Hydraulic Cylinder Market Report Scope

The Hydraulic Cylinder Market refers to the industry focused on the design, manufacturing, and application of hydraulic cylinders, which are mechanical actuators used to provide unidirectional force through a unidirectional stroke. These cylinders are widely utilized across various industries, including construction, agriculture, material handling, mining, industrial manufacturing, aerospace and defense, marine, and oil and gas, to perform tasks requiring heavy lifting, pushing, pulling, or other force-intensive operations.

The Hydraulic Cylinder Market Report is Segmented by Function (Single-Acting and Double-Acting), Specification (Welded, Tie-Rod, Telescopic, and Mill-Type), Bore Size (Below 50 mm, 50-150 mm, and Above 150 mm), End-User Industry (Construction Equipment, Agriculture, Material Handling and Forklifts, Mining, Industrial Manufacturing, Aerospace and Defense, Marine, and Oil and Gas), and Geography (North America, Europe, Asia Pacific, South America, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Single-Acting |

| Double-Acting |

| Welded |

| Tie-Rod |

| Telescopic |

| Mill-Type |

| Below 50 mm |

| 50 - 150 mm |

| Above 150 mm |

| Construction Equipment |

| Agriculture |

| Material Handling and Forklifts |

| Mining |

| Industrial Manufacturing |

| Aerospace and Defense |

| Marine |

| Oil and Gas |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Function | Single-Acting | |

| Double-Acting | ||

| By Specification | Welded | |

| Tie-Rod | ||

| Telescopic | ||

| Mill-Type | ||

| By Bore Size | Below 50 mm | |

| 50 - 150 mm | ||

| Above 150 mm | ||

| By End-User Industry | Construction Equipment | |

| Agriculture | ||

| Material Handling and Forklifts | ||

| Mining | ||

| Industrial Manufacturing | ||

| Aerospace and Defense | ||

| Marine | ||

| Oil and Gas | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the growth outlook for the hydraulic cylinder market through 2031?

Global revenue is projected to rise from USD 17.21 billion in 2026 to USD 22.83 billion by 2031 at a 5.81% CAGR.

Which cylinder function holds the largest share?

Double-acting cylinders commanded 61.48% of global revenue in 2025 due to widespread use in heavy construction equipment.

Which geography is expanding fastest?

The Middle East is forecast to record a 6.18% CAGR from 2026 to 2031, ahead of other regions.

How are smart cylinders changing equipment maintenance?

Embedded sensors enable condition monitoring that can cut unplanned downtime by roughly 30%.

Why are telescopic cylinders gaining popularity?

Urban job sites favor telescopic designs that deliver long strokes while fitting inside compact retracted lengths.

Page last updated on: