Pneumatic Tire Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

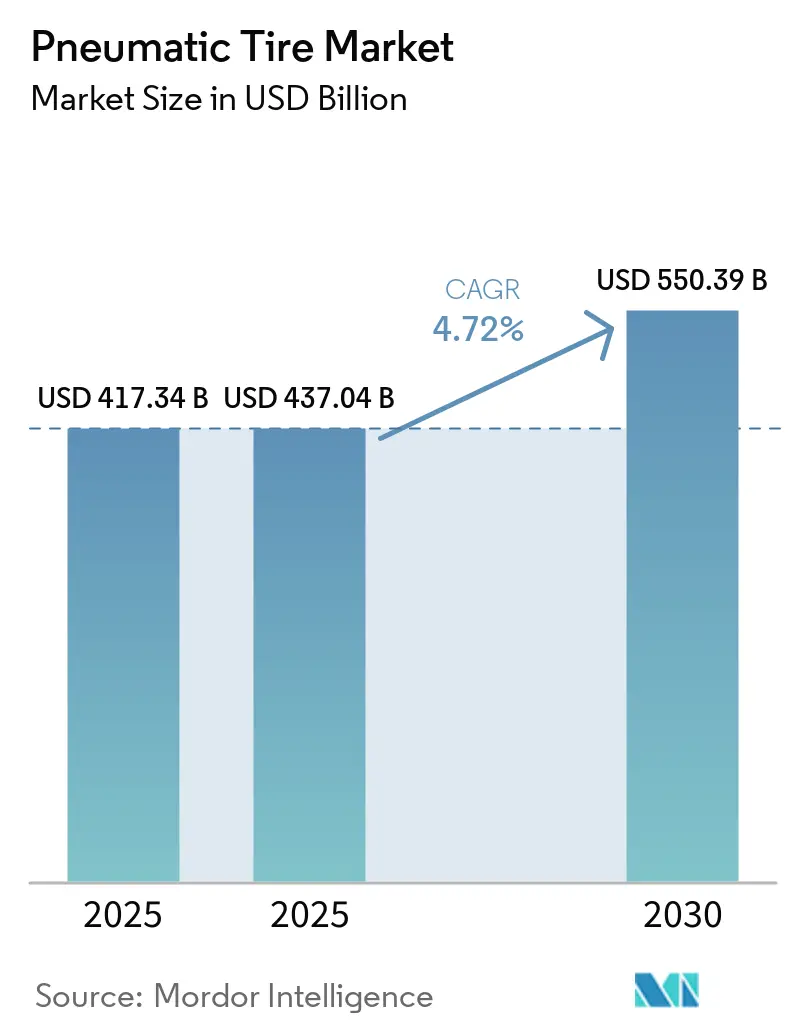

| Market Size (2025) | USD 437.04 Billion |

| Market Size (2030) | USD 550.39 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

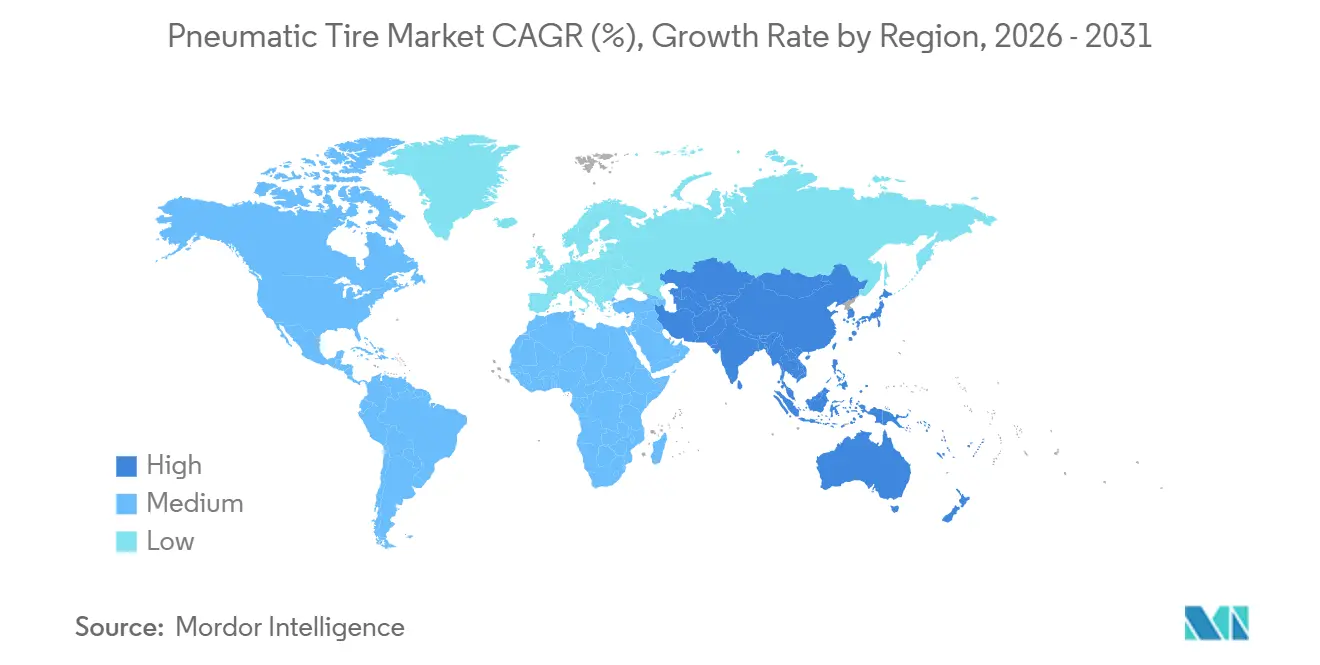

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pneumatic Tire Market Analysis by Mordor Intelligence

The Pneumatic Tire Market size is projected to expand from USD 417.34 billion in 2025 and USD 437.04 billion in 2025 to USD 550.39 billion by 2030, registering a CAGR of 4.72% between 2025 to 2030. Market growth is transitioning from a focus on volume to higher-margin radial designs, electric vehicle (EV)-compatible compounds, and sensor-enabled products, which are increasing average selling prices in both original equipment and replacement channels. Regulatory restrictions on rolling resistance and particulate abrasion are encouraging manufacturers in the Asia-Pacific region to phase out legacy bias-ply production. Meanwhile, fleets in North America and Europe are emphasizing fuel efficiency and predictive maintenance integration. Challenges such as counterfeit products and environmental compliance are increasing cost pressures. However, strategic investments in smart-factory automation and greenfield facilities are helping maintain supply flexibility and protect margins in the pneumatic tire market.

Key Report Takeaways

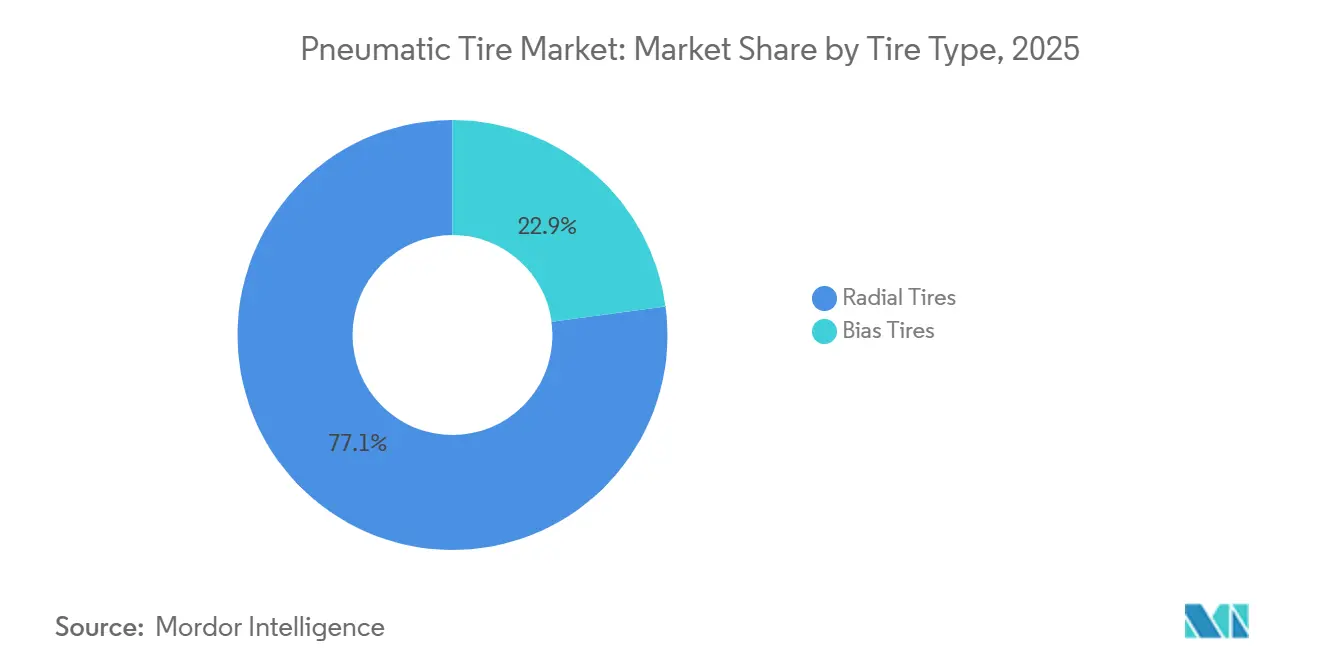

- By tire type, radial tires led with 77.12% of the pneumatic tire market share in 2025, while bias tires are forecast to post a 5.15% CAGR through 2031.

- By distribution channel, the aftermarket captured 60.45% of revenue in 2025 and is advancing at a 5.33% CAGR to 2031.

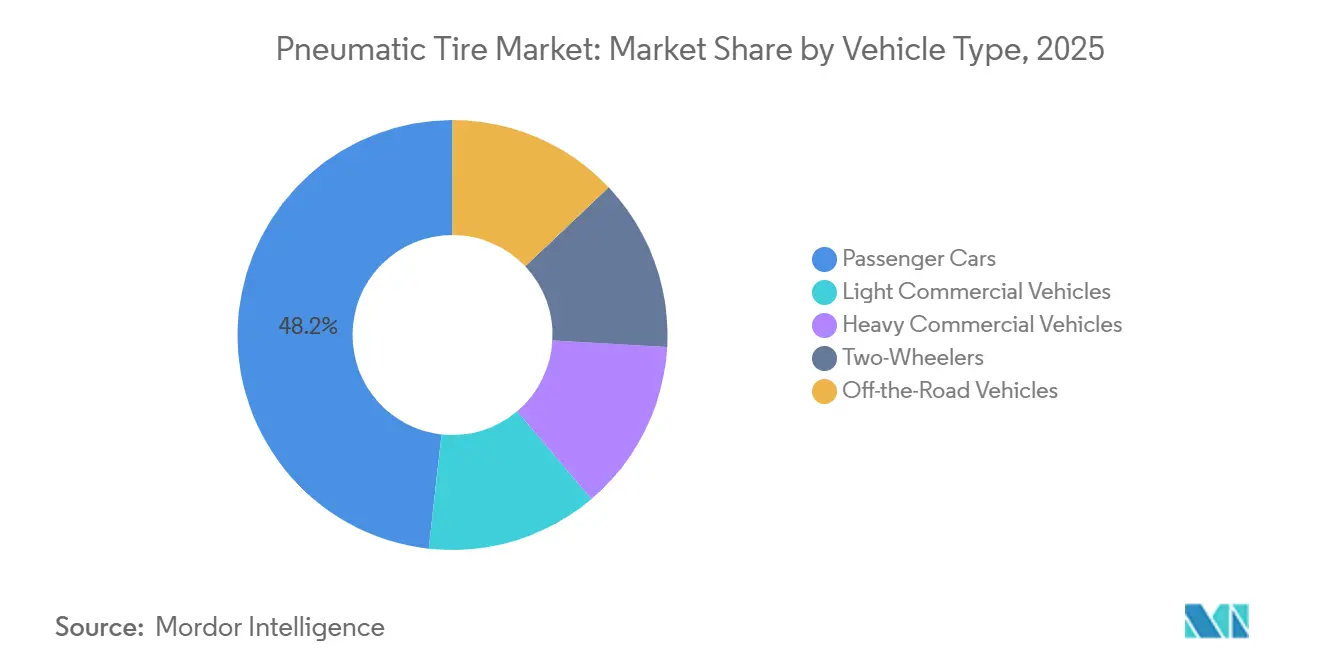

- By vehicle type, heavy commercial vehicles are projected to expand at a 5.27% CAGR from 2026-2031, outpacing passenger cars that held 48.23% volume in 2025.

- By geography, Asia-Pacific commanded 44.15% of value in 2025 and is forecast to grow at 5.49% through 2031, the fastest regional rate in the pneumatic tire market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pneumatic Tire Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Fuel-Efficient and High-Performance Tires | +1.2% | Global, with North America and the EU leading adoption | Medium term (2-4 years) |

| Expansion of E-Commerce and Logistics Fleets | +0.9% | Global, concentrated in North America, China, and India | Short term (≤ 2 years) |

| Accelerated Aftermarket Demand from Ageing Vehicle Parc | +0.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Stringent Tire-Efficiency and Labelling Regulations | +0.7% | EU, North America, China, South Korea | Medium term (2-4 years) |

| Integration of Smart-Tire Sensors for Predictive Maintenance | +0.5% | North America, the EU, and premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Fuel-Efficient and High-Performance Tires

Fleet operators are focusing on reducing rolling resistance to comply with the Corporate Average Fuel Economy (CAFE) standards, which will become stricter starting with model-year 2027[1]National Highway Traffic Safety Administration, “Corporate Average Fuel Economy Standards for Model Year 2027,” nhtsa.gov. This has led to the use of silica-rich tread compounds and bio-based oils that lower hysteresis without affecting wet grip, as noted by the National Highway Traffic Safety Administration (NHTSA). Products such as Continental EcoContact and Michelin e.Primacy, which holds A-ratings for European Union (EU) fuel-efficiency labels, demonstrates that high performance can align with safety requirements. Additionally, the increased torque of electric vehicles (EVs) raises tire wear rates by approximately 20%, prompting original equipment manufacturers (OEMs) to require reinforced sidewalls and optimized tread patterns to extend tire service life. These advancements enable suppliers to maintain price premiums in the pneumatic tire market. Technological innovation continues to drive growth in high-performance tire segments, outpacing overall replacement market growth.

Expansion of E-Commerce and Logistics Fleets

The United States Postal Service (USPS) plans to deploy 106,000 next-generation delivery vehicles by 2028, with 66,000 of these being battery-electric vehicles. This shift highlights the increasing urban delivery mileage. Goodyear’s USD 320 million upgrade to its Lawton facility aims to expand production capacity for low-noise tires with reinforced sidewalls, specifically designed for residential delivery routes. In markets like India and Indonesia, the rapid growth of online shopping is driving light-commercial fleets to transition from bias-ply to radial tires, which are better suited for managing heat during frequent stop-start cycles. As parcel volumes increase, fleet managers are adopting data-enabled tires that integrate with telematics systems, thereby increasing switching costs. These trends collectively contribute to incremental revenue growth in the pneumatic tire market.

Accelerated Aftermarket Demand from Ageing Vehicle Parc

In 2025, the average age of passenger cars in the United States reached 14 years, while light trucks averaged 11 years. This aging vehicle fleet has extended replacement cycles and influenced consumer preferences toward premium touring tires, which typically include 60,000-mile warranties. In the same year, there were 21.1 million new commercial-tire replacements and 16.9 million retreads, generating USD 20.4 billion in revenue. The increasing complexity of tire fitment and bundled service offerings has improved dealer margins compared to Original Equipment Manufacturer (OEM) contracts. Retreading now accounts for approximately 44% of the United States truck-tire market, sustaining demand for premium casings even as new-tire unit growth slows. This trend supports a stable revenue base and strengthens profitability in the pneumatic tire market.

Stringent Tire-Efficiency and Labeling Regulations

European Union (EU) Regulation 2020/740 mandates QR-coded labels that provide information on fuel efficiency, wet grip, and external noise levels, enhancing transparency throughout the supply chain. Additionally, the Euro 7 standards, set to take effect in July 2028, will introduce the world’s first particulate-emission caps of 3 milligrams per kilometer (mg/km) for passenger tires. These regulations will necessitate compound reformulations and extensive abrasion testing, increasing research and development (R&D) expenditures. Countries like China and South Korea are aligning with these standards, creating global compliance challenges and excluding manufacturers unable to meet certification requirements. These capital-intensive regulations establish high entry barriers, benefiting established players with advanced technologies. Improved labeling also encourages consumers to choose premium low-rolling-resistance tires, supporting sustained value growth in the pneumatic tire market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter Environmental Rules on Disposal and Micro-Plastics | -0.4% | EU, California, expanding to APAC | Medium term (2-4 years) |

| Counterfeit and Low-Quality Tire Influx in Developing Markets | -0.3% | Africa, South Asia, Latin America | Short term (≤ 2 years) |

| Emergence of Airless and Solid Tires in Niche Uses | -0.2% | Urban mobility, last-mile delivery in North America, the EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tighter Environmental Rules on Disposal and Micro-Plastics

Euro 7 regulations introduce stricter particulate limits, with further tightening expected by 2032. Additionally, 24 United States (U.S.) states have implemented Extended Producer Responsibility (EPR) laws, transferring disposal costs to manufacturers[2]U.S. Environmental Protection Agency, “Extended Producer Responsibility for Tires,” epa.gov. The use of harder tread compounds, while addressing durability, can affect wet-grip performance, necessitating new investments in silica dispersion and polymer cross-linking technologies to maintain safety standards. According to the Pew Charitable Trusts, tire and brake wear is projected to account for 90% of road-transport particulates by 2050, leading to increased regulatory scrutiny. Compliance with these regulations is estimated to raise unit costs by 2%-4%, impacting price competitiveness, particularly for low-margin suppliers in the pneumatic tire market.

Counterfeit and Low-Quality Tire Influx in Developing Markets

The Organization for Economic Co-operation and Development (OECD) estimates that counterfeit tires represent up to 40% of replacement sales in certain African regions, resulting in an annual revenue loss of EUR 2.2 billion (USD 2.56 billion) for legitimate European Union (EU) businesses. In Malaysia, the MS 224 certification regime has reduced illicit imports but has also increased testing costs for smaller distributors. Michelin reports that 50,000-70,000 counterfeit truck tires enter Europe each year, increasing liability risks. The prevalence of counterfeit products affects consumer confidence and diverts sales from established brands in the pneumatic tire market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tire Type: Radial Dominance Masks Bias Resilience

Radial tires accounted for 77.12% of market value in 2025, driven by regulatory emphasis on fuel efficiency and high-speed safety. Bias tires are projected to grow at a compound annual growth rate (CAGR) of 5.15% through 2031, surpassing the overall pneumatic tire market CAGR. In India, with a two-wheeler base exceeding 220 million units, bias tires remain popular due to their puncture resistance and affordability, particularly among rural users. Similarly, in Sub-Saharan Africa, bias tires are preferred for light trucks and three-wheelers operating on unpaved roads. Radial tires continue to dominate revenue generation, especially in electric vehicles. Bridgestone’s JPY 27 billion (USD 0.17 billion) investment in Japan has expanded capacity for high-rigidity radial tires designed for heavier electric vehicle (EV) battery packs.

Bias tire manufacturers are also modernizing. Companies like Zhongce Rubber and Triangle Tire are enhancing their engineering tire lines to cater to the mining and construction sectors, where radial advantages are less pronounced. Meanwhile, Continental’s plant in Thailand focuses on motorcycle and EV radial tires, which improve ride quality and torque management. As manufacturers aim to balance performance and sustainability, they are diversifying their product portfolios to address varied use cases across the pneumatic tire market.

By Distribution Channel: Aftermarket Sustains Margin Leadership

Aftermarket sales accounted for 60.45% of revenue in 2025, offering 15%-25% higher gross margins compared to original equipment manufacturer (OEM) contracts due to value-added services such as balancing and road-hazard programs. The increasing average age of vehicles supports a projected CAGR of 5.33% through 2031. Seasonal promotions and loyalty programs further drive repeat purchases and strengthen dealer relationships. The aftermarket segment is expected to grow at a faster rate than OEM sales, highlighting its critical role in ensuring cash-flow stability.

OEM contracts benefit from the growth in EV production and smart-tire co-development. For instance, Yokohama’s new facility in China supplies domestic EV manufacturers and exports to North America, demonstrating how collaborative design secures long-term volumes. However, predefined pricing agreements in OEM contracts limit the ability to pass on raw material cost increases, such as those for butadiene and natural rubber, potentially compressing margins. Balancing the flexibility of the aftermarket with the stability of OEM contracts remains essential for maintaining profitability in the pneumatic tire market.

By Vehicle Type: Heavy Commercial Vehicles Lead Growth

While passenger cars accounted for 48.23% of shipments in 2025, heavy commercial vehicles are expected to grow at a CAGR of 5.27% through 2031, fueled by e-commerce expansion, infrastructure investments, and fleet electrification. North American Class 8 truck production is forecast to increase by 6.1% in 2026, while European heavy-truck output is projected to grow by 5.0%, both outpacing passenger car production. The pneumatic tire market for heavy trucks benefits from their intensive duty cycles, which typically range from 12 to 16 hours per day, leading to higher replacement rates.

Light commercial vehicles, which combine passenger-car comfort with load capacities of up to 1,500 kilograms, are gaining popularity in markets like India and Latin America. In South Asia, two-wheeler demand remains significant, though electrification trends may shift tire preferences toward low-rolling resistance radials by the end of the decade. Meanwhile, the mining and construction equipment segment faces cyclical challenges. For example, Goodyear sold its off-the-road (OTR) unit to Yokohama for USD 905 million in 2024 to focus on higher-margin categories. These trends underscore the importance of segment diversification within the pneumatic tire market.

Geography Analysis

Asia-Pacific accounted for 44.15% of the market value in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.49% through 2031. This growth is supported by China’s annual output of 840 million units, India’s transition to radial tires, and the expansion of commercial vehicle markets in ASEAN (Association of Southeast Asian Nations) countries. Linglong’s USD 750 million Anhui plant adds 14 million units to its capacity, while ZC Rubber’s 5G-enabled Hangzhou facility doubles its output to 20 million passenger radials. These developments address regional demand and enhance export capabilities, reinforcing Asia-Pacific’s role in the pneumatic tire market.

North America shows slower volume growth but benefits from higher per-unit values due to the increasing adoption of premium electric vehicle (EV) tires. The United States Tire Manufacturers Association (USTMA) projects 340.4 million shipments in 2025, reflecting a modest 0.9% volume growth. However, an improved price mix is expected to drive revenue. Goodyear’s USD 320 million expansion in Lawton and a CAD 575 million (USD 415.16 million) modernization project in Canada focus on producing sensor-ready, low-noise EV tires. Meanwhile, Europe faces cost challenges, with German production declining by 4.3% in 2024. Additionally, Continental closed its Malaysian Alor Setar plant to reduce high-cost capacity.

South America and the Middle East & Africa remain smaller markets but hold strategic importance. Linglong’s joint venture in Brazil circumvents anti-dumping tariffs and supplies tires to Mercosur assemblers. In the Middle East, infrastructure development in Saudi Arabia and the United Arab Emirates (UAE) drives demand, although currency volatility dampens investment enthusiasm. In Africa, counterfeit products account for up to 40% of replacement tire sales, posing challenges for legitimate players in the pneumatic tire market.

Competitive Landscape

The pneumatic tire market is moderately concentrated. The top companies are Bridgestone, Michelin, The Goodyear Tire and Rubber Company, Continental Aktiengesellschaft (AG), Hankook Tire and Technology, Pirelli, Yokohama, Maxxis, and Zhongce. The industry's technological focus has shifted from increasing production capacity to integrating smart-tire technology and developing electric vehicle (EV)-specific compounds. Examples of innovation include Continental’s ContiConnect 2.0 and Bridgestone’s AirFree concept, which strengthen ties with original equipment manufacturer (OEM) platforms and enable aftermarket data services.

Chinese manufacturers are utilizing fifth-generation (5G)-enabled smart factories to achieve production cycles of less than 24 hours, reducing quality disparities with premium competitors. Apollo Tyres has invested USD 642 million in its Indian expansion, adding daily production capacity for 10,500 passenger-car radials and 3,600 truck-bus radials, with a focus on exports to Europe and North America. Additionally, Madras Rubber Factory (MRF) has approved a USD 575 million greenfield project in Tamil Nadu, set to commence in March 2026.

Patent activity in tire-wear sensors and self-sealing tread compounds is increasing. For instance, Melexis’s MLX91805 sensor is designed to withstand extreme centrifugal forces, while Society of Automotive Engineers (SAE) J2657 data protocols facilitate cross-brand sensor integration. These advancements highlight the growing importance of digital capabilities alongside rubber chemistry in establishing competitive advantages within the pneumatic tire industry.

Pneumatic Tire Industry Leaders

Michelin

The Goodyear Tire & Rubber Company

Bridgestone

Continental AG

Hankook Tire & Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: MRF Tyres has announced a USD 575 million greenfield manufacturing plant in Tamil Nadu, India. This investment, the company's largest at a single site, will focus on the production of pneumatic tires, specifically passenger car radials and two-wheeler tires. These products are intended to cater to both domestic demand and export markets, aligning with the growing global and regional demand for pneumatic tires.

- February 2026: Apollo Tyres has allocated USD 642 million to expand its production capacity in India for pneumatic tires. This investment is focused on increasing the daily production of 10,500 passenger car radial tires and 3,600 truck-bus radial tires. The expansion will be implemented in phases, with a ramp-up planned through 2028.

Global Pneumatic Tire Market Report Scope

A pneumatic tire is a flexible rubber casing filled with compressed air, designed to provide cushioning between a vehicle and the ground. These tires rely on internal air pressure to absorb shocks, maintain traction, and support the vehicle's weight. They are used in applications ranging from bicycles and cars to heavy-duty forklifts, as they provide effective performance on uneven surfaces compared to solid tires.

The pneumatic tire market is segmented by tire type, distribution channel, vehicle type, and geography. By tire type, the market is segmented into radial tires and bias tires. By distribution channel, the market is segmented into OEM and aftermarket. By vehicle type, the market is segmented into passenger cars, light commercial vehicles, heavy commercial vehicles, two-wheelers, and off-the-road vehicles. The report also covers the market size and forecasts for pneumatic tires in 21 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Radial Tires |

| Bias Tires |

| OEM |

| Aftermarket |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers |

| Off-the-Road Vehicles |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Tire Type | Radial Tires | |

| Bias Tires | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| Off-the-Road Vehicles | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current market size of Pneumatic Tire Market?

The Pneumatic Tire Market size is projected to expand from USD 417.34 billion in 2025 and USD 437.04 billion in 2025 to USD 550.39 billion by 2030, registering a CAGR of 4.72% between 2025 to 2030.

How fast is the pneumatic tire market expected to grow between 2026 and 2031?

Revenue is projected to increase at a 4.72% CAGR over the period.

Which region is growing fastest in the pneumatic tire space?

Asia-Pacific is expected to post a 5.49% CAGR through 2031, the highest among all regions.

Why are smart-tire sensors gaining traction?

Fleet operators adopt sensors to predict failures weeks in advance, reducing roadside incidents by up to 30% and lowering maintenance costs.

Page last updated on: