Tire Cord Fabrics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

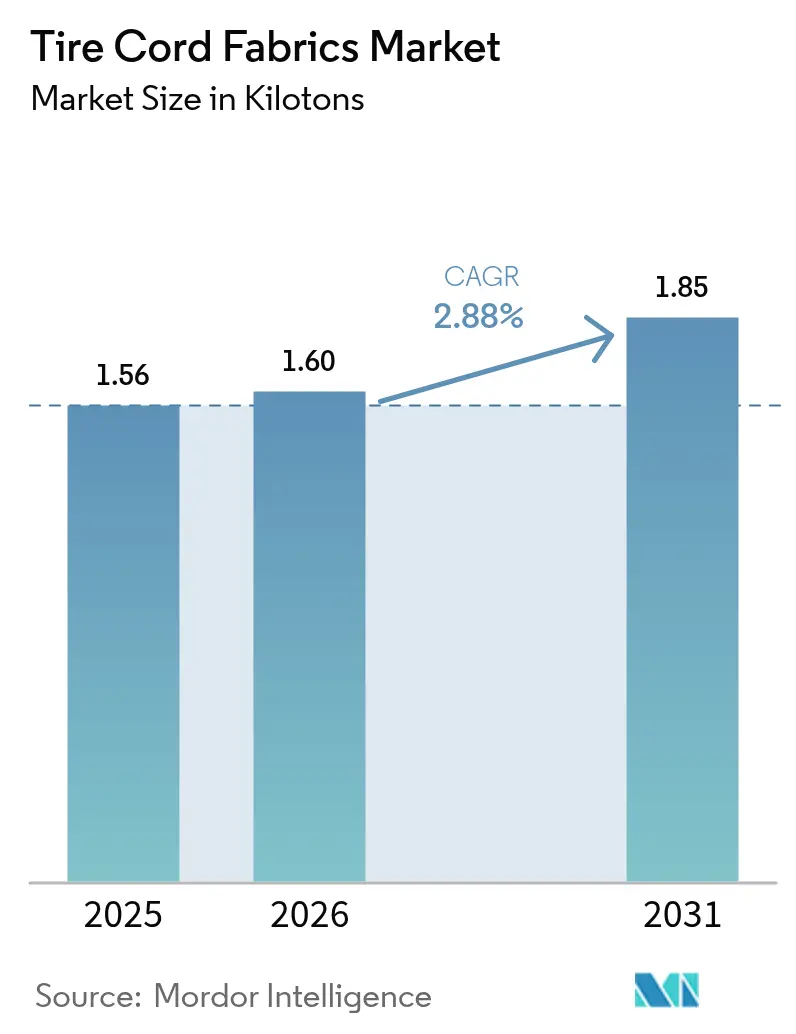

| Market Volume (2026) | 1.6 kilotons |

| Market Volume (2031) | 1.85 kilotons |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tire Cord Fabrics Market Analysis by Mordor Intelligence

The Tire Cord Fabrics Market size was valued at 1.56 kilotons in 2025 and estimated to grow from 1.6 kilotons in 2026 to reach 1.85 kilotons by 2031, at a CAGR of 2.88% during the forecast period (2026-2031). This moderate growth reflects rising replacement demand driven by electric-vehicle (EV) adoption, regulatory pressure for lower rolling resistance, and steady expansion of commercial vehicle fleets. Polyester retains dominance because it balances cost and performance, while aramid advances fastest on the back of premium tire applications that require superior heat resistance. Asia-Pacific leads consumption thanks to integrated manufacturing ecosystems and expanding vehicle ownership, whereas the Middle East and Africa records the quickest regional growth as governments invest in automotive capacity. Competitive dynamics favor vertically integrated suppliers that can offer HMLS polyester, hybrid cords, and resorcinol-formaldehyde-free (RFF) adhesion systems that help tire makers meet tightening sustainability rules. Raw-material cost swings, auto-production cycles, and early-stage airless tire concepts temper the near-term growth outlook for the tire cord fabrics market.

Key Report Takeaways

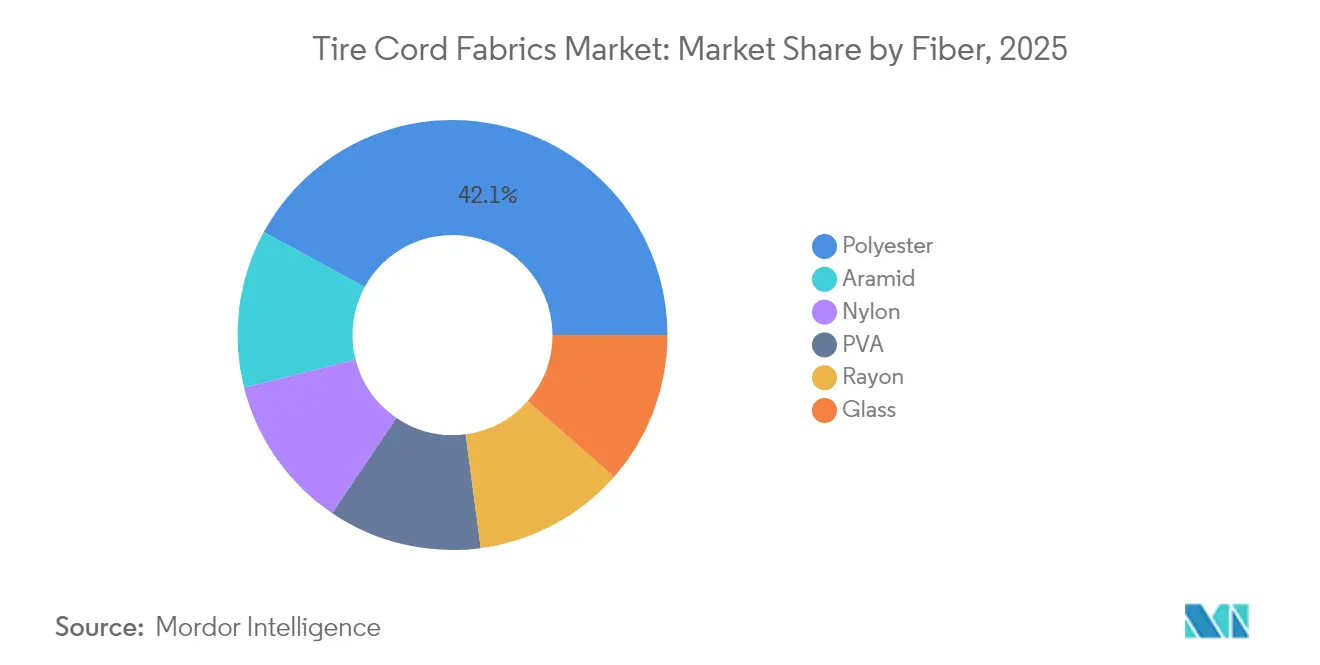

- By fiber, polyester held 42.05% of tire cord fabrics market share in 2025, while aramid is forecast to post a 3.14% CAGR to 2031.

- By tire type, radial construction commanded 67.65% of tire cord fabrics market share in 2025; semi-radial variants are projected to grow at a 3.05% CAGR through 2031.

- By vehicle type, automotive applications captured 70.80% of the tire cord fabrics market size in 2025, whereas aircraft tires are expected to expand at a 3.08% CAGR to 2031.

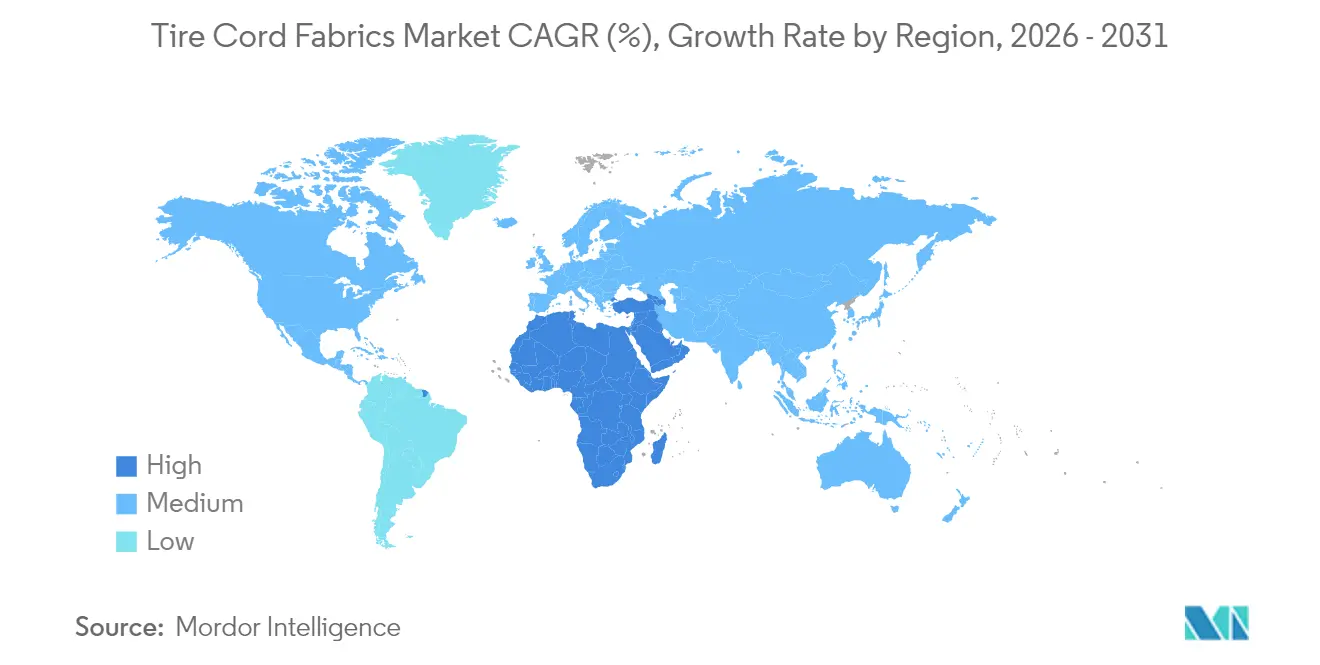

- By geography, Asia-Pacific led with 48.10% revenue share in 2025, while the Middle-East and Africa region is poised for the fastest 2.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tire Cord Fabrics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global vehicle production and parc expansion | +0.8% | Global (APAC strongest) | Medium term (2-4 years) |

| Rapid radial-tire adoption in emerging markets | +0.6% | APAC core, MEA spill-over | Long term (≥ 4 years) |

| Higher EV-related tire-replacement frequency | +0.5% | North America and Europe, spreading to APAC | Short term (≤ 2 years) |

| Lightweight HMLS and hybrid-cord demand for lower rolling resistance | +0.4% | Global premium focus | Medium term (2-4 years) |

| Adoption of RFF “green” adhesion chemistries | +0.2% | EU-led, global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Production and Parc Expansion

Industry-wide vehicle output recovery is driving bulk orders for reinforcement textiles as tire factories rebuild inventories that ran down during recent supply-chain disruptions. Heavy-duty trucks, buses, and trailers consume greater quantities of cord fabric per tire than passenger cars, magnifying demand gains. A steadily expanding global vehicle parc sustains replacement volumes, especially in emerging economies where ownership rates continue to climb despite macroeconomic headwinds. Electrification programs in logistics fleets add incremental pull because electric trucks require stiffer carcasses and higher cord density. Parallel capacity additions at leading tire makers create a synchronized upswing that underpins medium-term growth for the tire cord fabrics market.

Rapid Radial-Tire Adoption in Emerging Markets

Across India and Southeast Asia, bias-ply tires are giving way to radial designs that need roughly 40% more cord fabric per unit. Government fuel-efficiency mandates and user demand for longer service life accelerate the changeover. Farm-equipment segments amplify the effect because IF and VF radial technologies require stronger carcasses built with high-tensile cords. The conversion progresses through 2030, producing a durable volume tailwind that compensates for mature demand profiles in North America and Europe. Suppliers capable of ramping polyester and nylon output near local tire clusters are best placed to capture this share.

Lightweight HMLS and Hybrid-Cord Demand for Lower Rolling Resistance

Fuel-economy and CO₂-emission regulations push tire makers toward low-rolling-resistance designs. HMLS polyester offers high modulus with minimal shrinkage, cutting energy loss in the sidewall without sacrificing durability. Hybrid constructions that blend polyester with aramid or glass allow engineers to fine-tune stiffness and belt strength for ultra-high-performance tires. As labeling rules tighten in the European Union and other regions, premium technologies migrate into mainstream price tiers, broadening the addressable base for advanced cords[1]European Tyre & Rubber Manufacturers Association, “EU Tire Labeling Regulation Update 2024,” etrma.org.

Adoption of RFF “Green” Adhesion Chemistries

Regulators are phasing out formaldehyde emissions, prompting a shift to RFF dips that bond fabric to rubber without traditional resorcinol–formaldehyde resins. Early adopters in Europe and Japan have validated performance parity, and global roll-out accelerates between 2026-2027 as mandatory rules take effect. Cord producers that invested ahead of the curve can command pricing premiums during the transition, reinforcing the competitive importance of sustainable process capabilities[2]European Chemicals Agency, “Formaldehyde Restriction Proposal,” echa.europa.eu.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | -0.3% | Global, APAC manufacturing hubs | Short term (≤ 2 years) |

| Cyclical over-/under-capacity in auto production | -0.2% | Global, regionally uneven | Medium term (2-4 years) |

| Rise of airless/non-pneumatic tire concepts | -0.1% | North America and Europe early pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Price Volatility

Polyester and nylon rely on paraxylene, adipic acid, and caprolactam, all of which fluctuate with crude-oil cycles. Sudden surges compress margins for cord weavers, while sharp declines discourage upstream investment, creating supply-security risks. China’s dominant position in fiber intermediates means regional outages or trade tensions can translate quickly into global price swings. Although large tire companies can hedge, smaller fabric producers face working-capital stress that may constrain near-term supply.

Cyclical Over-/Under-Capacity in Auto Production

Automotive build rates remain sensitive to GDP shifts, interest rates, and policy incentives. Periods of under-utilized capacity in China and Europe reduce cord fabric pull-through, whereas rapid recoveries can trigger short-lived shortages that push up spot prices. The capital intensity of weaving and dipping lines makes it difficult for suppliers to flex capacity quickly, creating mismatches that ripple through the tire cord fabrics market. Consolidation and regional diversification strategies aim to blunt future shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber: Polyester Dominance with Aramid Momentum

Polyester retained 42.05% of tire cord fabrics market share in 2025 owing to its cost-to-performance balance across passenger and commercial tires. The segment’s favorable economics, abundant feedstock, and compatibility with automated weaving underpin its leadership. Aramid, while accounting for a smaller volume base, records a 3.14% CAGR through 2031, powered by EV and ultra-high-performance fitments that demand heat resistance and tensile strength beyond polyester’s ceiling. Nylon sustains relevance in bias constructions and specialty off-road tires but confronts gradual volume erosion as radial penetration rises. Rayon continues to retreat because of supply constraints and shorter fatigue life, whereas glass and PVA cord niches stay stable in industrial and aircraft applications. Sustainability imperatives encourage trials of bio-derived polyesters and recycled monomer streams, positioning innovators to redefine fiber hierarchies later in the decade.

Polyester’s HMLS grades help leading producers lock in long-term contracts with global tire OEMs, cushioning them against raw-material swings. Aramid suppliers command premium margins and often integrate backward into fiber precursor chemistries to secure supply. Hybrid cords combining polyester with aramid or glass enable tailored stiffness for fine-tuned ride comfort, offering an avenue for differentiated growth.

By Tire Type: Radial Supremacy with Semi-Radial Resilience

Radial tires accounted for 67.65% of the tire cord fabrics market size in 2025 thanks to superior heat dissipation, tread life, and fuel savings. Mass adoption across passenger cars and on-highway trucks normalized manufacturing economies, narrowing cost gaps to older designs. Even with maturity in developed regions, ongoing radial conversion in agriculture and mining ensures steady incremental demand.

Semi-radial constructions—combining radial belts with bias plies—are expanding at a 3.05% CAGR where fleets value balanced cost and durability, notably in heavy haulage and buses. Bias ply remains entrenched in certain off-road settings that prioritize sidewall toughness and easy repair, but its share continues to edge downward.

By Vehicle Type: Automotive Bulk under Aircraft Upswing

Automotive applications captured 70.80% of the tire cord fabrics market in 2025, underpinned by steady replacement cycles and rising EV penetration that inflates cord consumption per mile traveled. Light trucks in North America and China prolong the segment’s dominance because they employ larger tires with higher cord counts. Aircraft tires, although small in volume, post the swiftest 3.08% CAGR as global passenger traffic rebounds and defense budgets climb. Aramid-reinforced carcasses that tolerate multiple landings at elevated loads fetch unit prices far above automotive equivalents, lifting market value. Industrial vehicles such as loaders, graders, and port equipment supply a dependable base, while emerging segments, electric scooters, recreational ATVs, and last-mile robot, unlock boutique demand for specialized cords.

Regulatory scrutiny of tire abrasion particulates and microplastics could distort future vehicle-type demand patterns, compelling fabric producers to develop new chemistries that limit fiber shedding. This regulatory tailwind for innovation further differentiates suppliers with strong research and development pipelines within the tire cord fabrics industry.

Geography Analysis

Asia-Pacific’s 48.10% share in 2025 reflects production clusters that co-locate petrochemical feedstocks, high-speed weaving mills, and major tire plants. China combines scale with rising competency in HMLS polyester and RFF dipping, while India’s automotive growth adds a deep domestic consumption layer. Southeast Asian economies such as Thailand and Indonesia extend the supply chain with export-oriented tire plants, helping the region anchor the tire cord fabrics market.

The Middle East and Africa records a 2.96% CAGR, the fastest worldwide. Governments channel oil revenue into diversification programs that include tire and component production. Saudi Arabia’s industrial zones attract foreign joint ventures, while Morocco leverages trade pacts with the EU and the United States to become a North-African export base. Turkey and South Africa, with established auto sectors, provide additional anchor points for growth.

North America and Europe remain innovation hubs where regulatory pressure for low-rolling-resistance and sustainable materials drives demand for advanced cord solutions. High adoption of EVs, stringent fuel-economy standards, and early trials of airless tires shape premium specifications that ripple back through global supply chains. Latin America grows steadily on agricultural equipment demand, but currency volatility and economic cycles inject periodic softness. Overall, shifting geographic footprints prompt cord suppliers to balance low-cost manufacturing with proximity to high-spec customers, ensuring the tire cord fabrics market keeps diversifying regionally.

Competitive Landscape

The market landscape is moderately fragmented. Bekaert, Hyosung, Teijin, and Kolon control significant capacity, while a second tier of regional specialists focuses on nylon or rayon niches. Strategic investment clusters around HMLS polyester capacity, RFF dipping lines, and regional diversification to offset trade barriers. Hyosung expanded polyester cord output in Vietnam, aligning supply with Southeast Asian tire exports. Teijin focuses on aramid upgrades to support EV tire programs in Europe. Technology partnerships grow in importance: cord producers are collaborating with rubber-chemistry specialists to co-develop low-energy-cure adhesives, and with recyclers to pilot depolymerization routes for end-of-life cords.

Tire Cord Fabrics Industry Leaders

HYOSUNG ADVANCED MATERIALS

Indorama Ventures Public Company Limited

Kolon Industries Inc.

KORDRNA Plus a.s.

SRF Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kolon Industries committed USD 20.5 million to expand tire-cord output in Vietnam, targeting start-up in 2027, thus expanding its tire cord fabric production.

- January 2023: Century Enka began commercial production of nylon tire cord fabric made from 100% recycled nylon waste, with Apollo Tyres adopting the material in select product lines.

Global Tire Cord Fabrics Market Report Scope

The tire cord fabrics market report includes:

| Nylon |

| Polyester |

| Rayon |

| Aramid |

| Glass |

| PVA |

| Bias / Diagonal |

| Semi-Radial |

| Radial |

| Automotive |

| Aircrafts |

| Industrial Products |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Turkey | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fiber | Nylon | |

| Polyester | ||

| Rayon | ||

| Aramid | ||

| Glass | ||

| PVA | ||

| By Tire Type | Bias / Diagonal | |

| Semi-Radial | ||

| Radial | ||

| By Vehicle Type | Automotive | |

| Aircrafts | ||

| Industrial Products | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Turkey | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current volume of the tire cord fabrics market?

The market stands at 1.6 kilotons in 2026 and is projected to reach 1.85 kilotons by 2031.

Which fiber type leads demand?

Polyester leads with 42.05% share, thanks to its cost-performance balance and compatibility with high-speed weaving.

Why are EVs important for cord fabric suppliers?

EV tires wear faster and require cords with higher heat resistance, lifting both replacement frequency and demand for premium fibers such as aramid.

Which region is growing fastest?

The Middle East and Africa is forecast to grow at 2.96% CAGR through 2031 due to industrial diversification and infrastructure spending.

How are sustainability rules influencing product development?

Regulations are accelerating the shift to RFF adhesion chemistries and recycled or bio-based fibers, rewarding suppliers that invest early in green processes.

Page last updated on: