Tire Bead Wire Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tire Bead Wire Market Analysis by Mordor Intelligence

The Tire Bead Wire Market size is expected to grow from USD 1.52 billion in 2025 to USD 1.58 billion in 2026 and is forecast to reach USD 1.94 billion by 2031 at a 4.21% CAGR over 2026-2031. The sector is moving from the capacity-expansion surge of the early-2020s into a steadier phase that prioritizes higher-grade specifications, closer proximity to tire plants, and lower embedded carbon. Growth hinges on three structural forces: slowing replacement cycles for passenger cars in mature economies, electrification-driven demand for lighter yet stronger wire grades, and continued rationalization of global wire-rod supply. Record global vehicle output of 92.5 million units in 2024 anchors baseline demand, with China and India contributing a combined 37.3 million units and exerting strong pull on regional bead-wire capacity. Yet demand is shifting beneath the surface as radial-tire penetration in India and Southeast Asia rises, aerospace tire specifications tighten for next-generation wide-bodies, and commercial EV fleets require bead assemblies that can withstand heavier static loads while delivering ultralow rolling resistance.

Key Report Takeaways

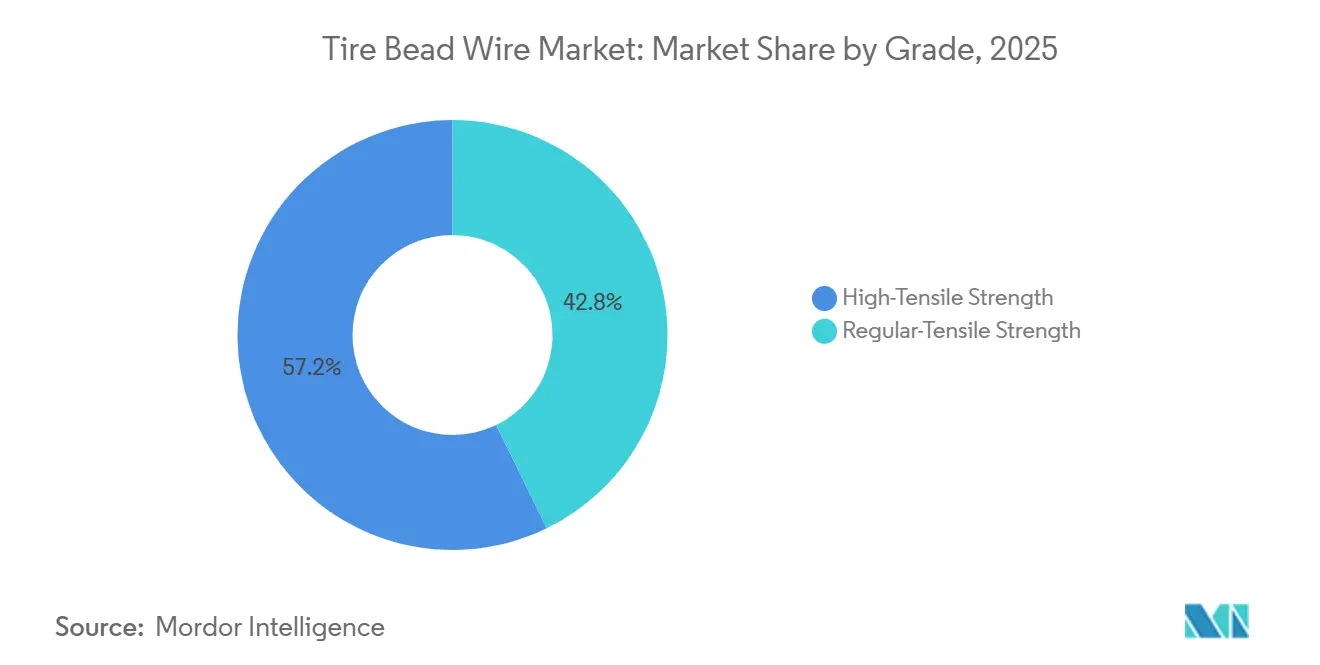

- By grade, high-tensile strength bead wire captured 57.22% of the tire bead wire market share in 2025; the same grade is projected to log the fastest 4.75% CAGR through 2031.

- By type, radial tyres commanded 81.31% share of the tire bead wire market size in 2025 and are forecast to expand at a 5.10% CAGR between 2026-2031.

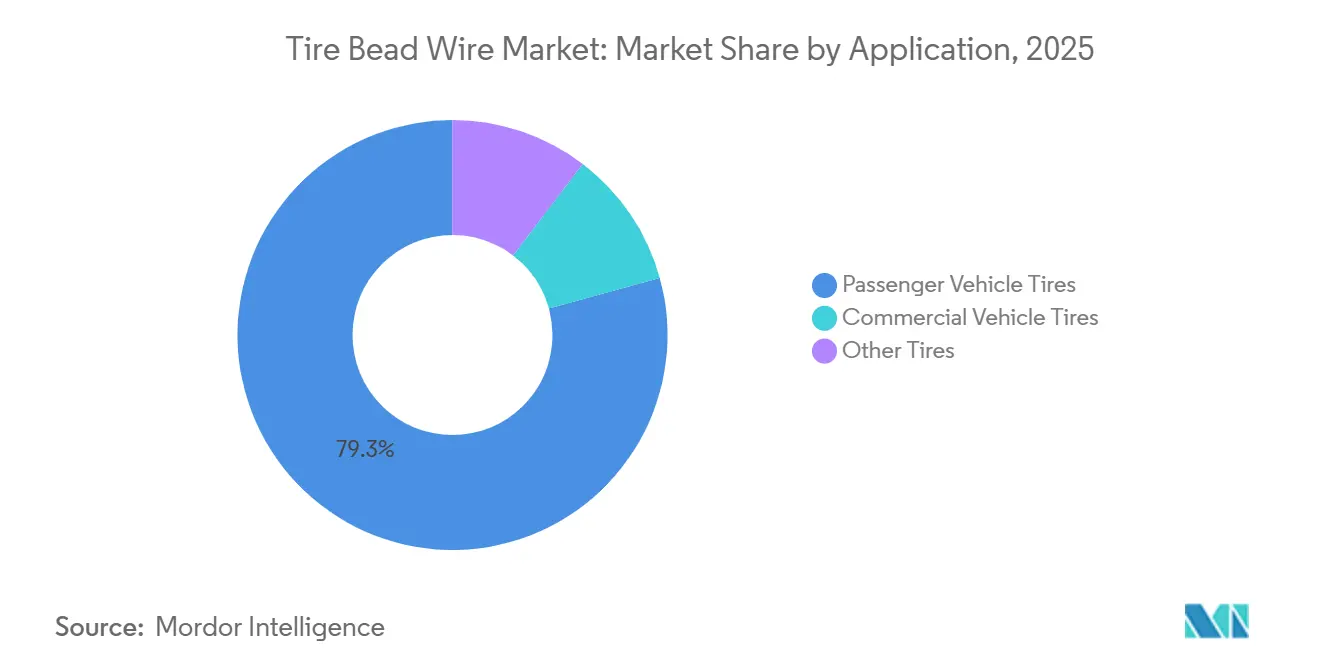

- By application, passenger-vehicle tires led with 79.27% revenue share in 2025, whereas commercial-vehicle bead-wire demand is advancing at a 5.29% CAGR to 2031.

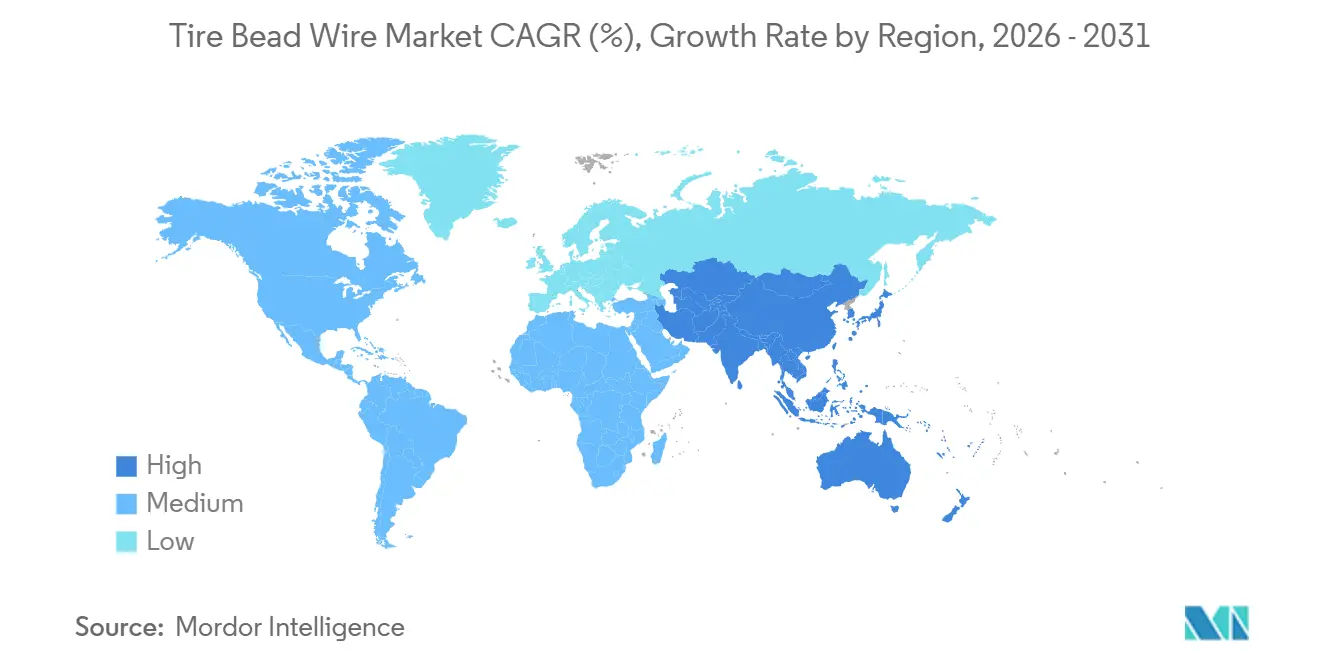

- By geography, Asia-Pacific held 40.40% of the tire bead wire market share in 2025; the same region posts the fastest 5.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tire Bead Wire Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global vehicle production | +0.8% | China, India, ASEAN | Medium term (2-4 years) |

| Rapid radial-tire penetration | +0.9% | India, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Expanding demand from aircraft tires | +0.3% | North America, Europe, Middle East | Long term (≥ 4 years) |

| EV-specific bead designs | +0.6% | China, Europe, North America | Medium term (2-4 years) |

| Lightweight micro-alloy wire for EV loads | +0.5% | Global early adopters (China, Germany, U.S.) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Production

Global light-vehicle output stabilized at 92.5 million units in 2024, but regional production shifted unmistakably toward Asia as Chinese and Indian automakers deepened local supply chains. Carmakers seek bead-wire suppliers that can deliver just-in-time within the same economic zone to reduce currency risk and freight costs. Apollo Tyres’ USD 700 million Andhra Pradesh expansion illustrates how new radial-tire lines are being co-located with bead-wire plants to capture this proximity premium. Suppliers lacking footprints in India, Vietnam, or Mexico face margin compression as fast-freight premiums erode.

Rapid Radial-Tire Penetration in Developing Economies

Although radial tires already represent 81.31% of global output, penetration in India’s truck-bus segment remains below 60% and below 40% for Indonesian motorcycles. Countervailing duties on Chinese tire imports through 2029 and India’s Automotive Mission Plan 2047 continue to spur domestic capacity additions that demand bead wire with tighter ±0.02 mm dimensional tolerances. Michelin’s 2025 Chennai ramp-up, focused on 16-22-inch premium radials, confirms OEM appetite for local, high-grade bead wire certified to ISO 4000-1:2024 HL classifications.

Expanding Demand from Aircraft & Aerospace Tires

More than 14,000 commercial aircraft on firm order through 2035 translates into a predictable bead-wire aftermarket insulated from automotive cyclicality. Aerospace-grade wire must achieve tensile strengths above 4,000 MPa and comply with AS9100D quality management. ArcelorMittal’s chromium-alloyed C90+Cr rod meets these specs at sub-0.2 mm diameters and earns 15–20% price premiums, creating a resilient niche that stabilizes revenue when automotive demand cools.

EV-Specific Bead Designs for Ultra-Low Rolling Resistance

Battery-electric vehicles impose conflicting demands for thicker load indices and thinner bead bundles to curb rolling resistance. Elyta ultra-tensile wire, launched by Bekaert in 2025, enables 15–20% strand-count reduction while sustaining 3,200-3,500 MPa strength, cutting bead mass by 8-12% and supporting OEM range targets[1]Bekaert, “Q1 2025 Trading Update,” bekaert.com. The surge in medium- and heavy-duty electric truck sales, up 136% year-over-year in H1 2025, magnifies this requirement.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel and copper prices | –0.4% | India, Southeast Asia, global importers | Short term (≤ 2 years) |

| Tightening emission norms | –0.3% | Europe, China, United States | Medium term (2-4 years) |

| Concentration risk in high-carbon rod supply | –0.2% | Global, heavily China-centric | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel and Copper Prices

High-carbon rod equals 65–70% of production cost, and single-quarter price swings hit 28% in 2024. Indian rod averaged USD 678 per tonne versus Chinese imports at USD 518 CFR, giving gray-market traders room to undercut local mills. Converters lacking hedging depth must pass costs through on 45–60-day lags, crimping margins when prices spike, whereas vertically integrated players enjoy 200–300 basis-point advantages.

Tightening Emission Norms for Wire-Drawing Operations

Europe’s Industrial Emissions Directive 2024/1785 obliges ferrous processors to install real-time monitors by 2027 and transformation plans by 2030, driving EUR 2–5 million retrofits per line[2]European Union, “Industrial Emissions Directive 2024/1785,” eur-lex.europa.eu. China’s MEE mirrors these limits, though unevenly enforced. Mid-tier European converters may exit rather than spend, shrinking capacity 8–12% by 2028 and pushing compliant suppliers’ utilization and prices higher.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: High-Tensile Strength Wire Leads Lightweighting Push

High-tensile grades held 57.22% of the 2025 tire bead wire market share and will advance at a 4.75% CAGR through 2031. Ultra-tensile wire above 3,200 MPa lets tire engineers use 12–15% fewer strands, cutting bead mass 8–10% and improving EV range by 1–2 km. The tire bead wire market size attributed to regular-tensile grades is eroding as bias-ply demand falls in South Asia and Africa. ArcelorMittal’s chromium-alloyed C90+Cr rod surpasses 4,000 MPa after drawing below 0.2 mm, allowing 0.85–0.95 mm bead diameters without compromising burst resistance, but commands a 10–15% premium. Suppliers verifying <5 particles/mm² inclusion density under ISO 16232 lock in multi-year EV contracts.

Affordability still matters in aftermarket two-wheelers and agricultural tires, preserving a residual niche for regular-tensile grades. Yet suppliers limited to these grades risk commoditization as Asian OEMs standardize high-tensile for all radial platforms from 2027 onward.

By Type: Radial Tires Cement Structural Dominance

Radial designs held 81.31% market share in 2025 and are on course for a 5.10% CAGR to 2031, accelerated by India and Brazil mandating bias-ply phase-outs for commercial vehicles by 2028. Radials deliver 8–10% lower rolling resistance and 15–20% longer tread life, making lifecycle economics decisive for fleets. The tire bead wire market size linked to bias-ply commercial truck tires will therefore shrink about 1.5% annually.

Precision demands tighten under radial construction: ±0.02 mm wire-diameter tolerance and ≥2,800 MPa strength are now baseline. Jiangsu Xingda’s 150,000 t steel-cord plus 80,000 t bead-wire phase-II expansion in Thailand exemplifies vertical integration aimed at Southeast Asian radial capacity that is scaling 8–10% per year.

By Application: Commercial-Vehicle Segment Scales Fastest

Passenger tires drove 79.27% of 2025 volume, but commercial-vehicle tires are projected to post the quickest 5.29% CAGR through 2031. Nearly 89,000 electric medium- and heavy-duty trucks sold in H1 2025, up 136% year-on-year, demand bead assemblies rated for HL loads and 200,000–700,000 km lifespans. Tire makers in China and the US are co-developing ultra-tensile bundles reaching 3,500 MPa to handle the extra axle weight imposed by 480–780 kWh battery packs.

“Other Tires,” covering two-wheelers, OTR, agricultural, and aircraft, delivers 15–18% of bead-wire volume but features high-margin niches. Aerospace wire claims 15–20% price premiums, while radial agricultural tires grow steadily as emerging-market mechanization advances.

Geography Analysis

Asia–Pacific led the tire bead wire market with 40.40% share in 2025 and is projected to climb at a 5.68% CAGR to 2031 as India, Vietnam, and Thailand commission new radial lines. China’s 31.28 million-unit vehicle output in 2024 kept tire plant utilization above 80%, and export tires to the US and Europe rose 20% year-over-year, sustaining regional bead-wire pull. India’s tire-sector revenue hit INR 100,000 crore (USD 12 billion) in FY 2025 and continues to grow 7–8%, underpinned by 50% replacement demand and record FY 2024 exports of INR 23,073 crore (USD 2.77 billion).

North American commercial-vehicle electrification offsets sluggish passenger-tire volumes, yet Europe confronts higher energy costs and the EU IED 2024/1785 retrofits that could shutter 8–12% of bead-wire capacity by 2028. Apollo Tyres will close its Dutch Enschede plant by summer 2026, citing cost inflation and low-priced imports. Bekaert’s EUR 60 million purchase of Bridgestone’s Shenyang and Rayong units underscores the strategic pivot to Asia.

In South America and the Middle East and Africa, Brazil’s legislative bias-ply phase-out by 2028 has spurred Linglong’s USD 1.2 billion Ponta Grossa greenfield, which will require 25,000–30,000 t of new bead-wire per year. Middle Eastern aviation hubs secure multi-year aerospace wire deals, while agricultural mechanization in Sub-Saharan Africa offers steady radial-tire growth albeit at higher working-capital intensity due to short payment terms.

Competitive Landscape

The Tire Bead Wire market is moderately consolidated. Technology and sustainability differentiate winners. Jiangsu Xingda targets 40% recycled content by 2030 and issued China’s first wire-sector digital product passport in 2022. Bekaert’s Elyta mega-tensile line captured Tire Tech Expo’s 2025 Material Innovation Award for enabling 15–20% fewer strands per bead. Indian challengers Rajratan and Aarti Steel pursue cost leadership, planning combined capacity of 240,000 t by 2027 and pricing commodity grades 8–12% below incumbents, forcing Western peers to chase premium niches: ultra-tensile EV wire, aerospace assemblies, and captive rod integration to dampen price swings.

Tire Bead Wire Industry Leaders

Bekaert

Jiangsu Xingda Steel Tyre Cord Co., Ltd.

Kiswire Ltd.

Rajratan Global Wire Limited

Shandong Daye Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Apollo Tyres unveiled an agricultural tire containing 75% sustainable materials, including recycled bead wire, advancing its goal of 40% sustainable raw input by 2030.

- November 2024: US EPA finalized stricter emissions rules for rubber-tire manufacturing, adding USD 13.3 million in annual compliance costs across bead-wire and rubber-mixing operations.

Global Tire Bead Wire Market Report Scope

Bead wire is a type of high-carbon bronze-coated steel wire that has been surface-plated with brass, copper, and other materials. It has high strength, excellent flexibility, and superior fatigue properties, and is primarily used in the tire bead as the framework material for reinforcement. It is frequently used in automobile tires, light truck tires, cargo truck tires, heavy equipment tires, and plane tires.

The Tire Bead Wire market is segmented by grades, type, application, and geography. By grades, the market is segmented into High Tensile Strength and Regular Tensile Strength. By type, the market is segmented into Radial tires and Bias tires. By application, the market is segmented into Automotive tires, Bicycle tires, Truck tires, and Others. The report also covers the market size and forecasts for the Tire Bead Wire market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| High-Tensile Strength |

| Regular-Tensile Strength |

| Radial Tyres |

| Bias Tyres |

| Passenger Vehicle Tires |

| Commercial Vehicle Tires |

| Other Tires |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Grade | High-Tensile Strength | |

| Regular-Tensile Strength | ||

| By Type | Radial Tyres | |

| Bias Tyres | ||

| By Application | Passenger Vehicle Tires | |

| Commercial Vehicle Tires | ||

| Other Tires | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the tire bead wire market in 2031?

The tire bead wire market is forecast to reach USD 1.94 billion by 2031.

How fast is the market expected to grow between 2026 and 2031?

It is projected to register a 4.19% CAGR over the period.

Which grade segment leads volume and growth?

High-tensile wire dominates with 57.22% share in 2025 and a projected 4.75% CAGR through 2031.

Why are commercial-vehicle tires a high-growth application?

E-commerce logistics and the surge in electric medium- and heavy-duty trucks are pushing a 5.29% CAGR in bead-wire demand for commercial tires

Which region is expected to post the fastest growth?

Asia–Pacific is set to expand at a 5.68% CAGR, driven by new tire capacity in India, Vietnam, and Thailand.

Page last updated on: