Ball Valve Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.57 Billion |

| Market Size (2031) | USD 16.23 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

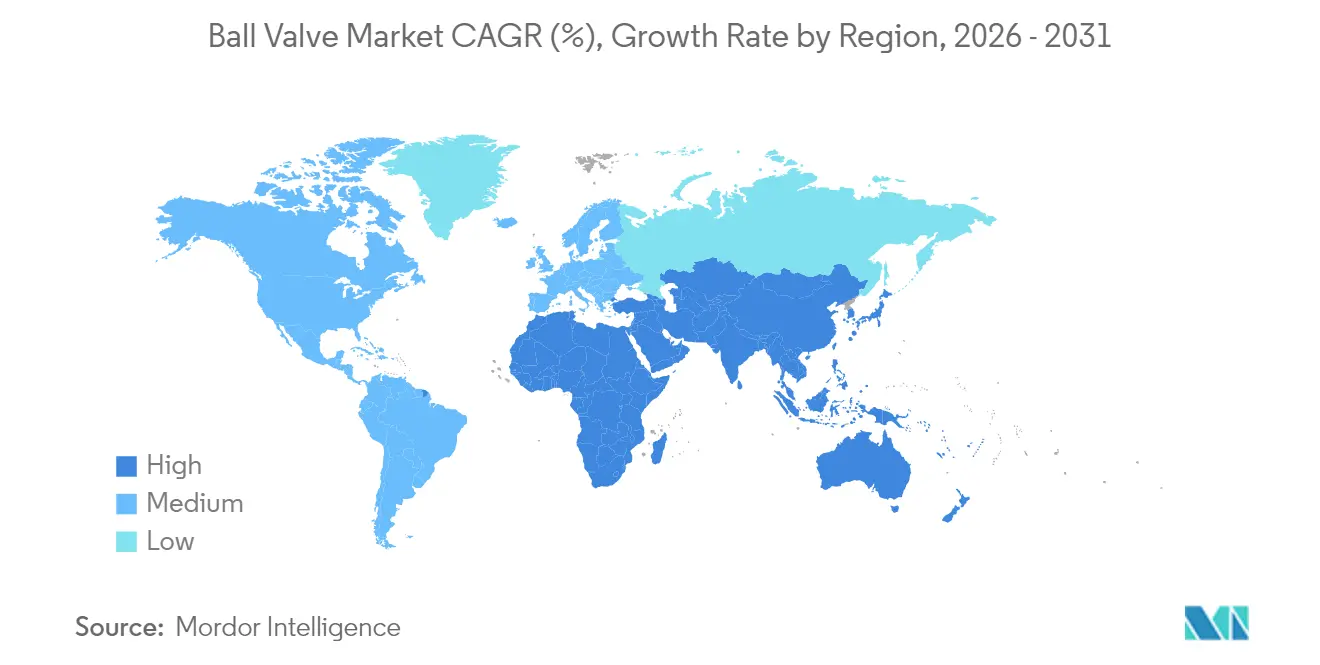

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ball Valve Market Analysis by Mordor Intelligence

The Ball valve market size was valued at USD 13.09 billion in 2025 and estimated to grow from USD 13.57 billion in 2026 to reach USD 16.23 billion by 2031, at a CAGR of 3.64% during the forecast period (2026-2031). The outlook confirms a steady, demand-backed expansion that mirrors the pace of global infrastructure upgrades rather than boom-cycle growth. Widespread liquefied natural gas (LNG) build-outs in Asia, regulatory pressure to cut fugitive emissions in hydrocarbon economies, and accelerated digitalization of water utilities are the principal forces reinforcing long-term valve demand. Project owners are prioritizing component integrity, safety compliance, and low lifetime emissions, which amplifies preference for premium ball valves over lower-cost substitutes. At the same time, supply-chain bottlenecks in specialty forgings and volatile stainless-steel prices are tempering near-term profit margins, especially for mid-tier Asian fabricators.

Key Report Takeaways

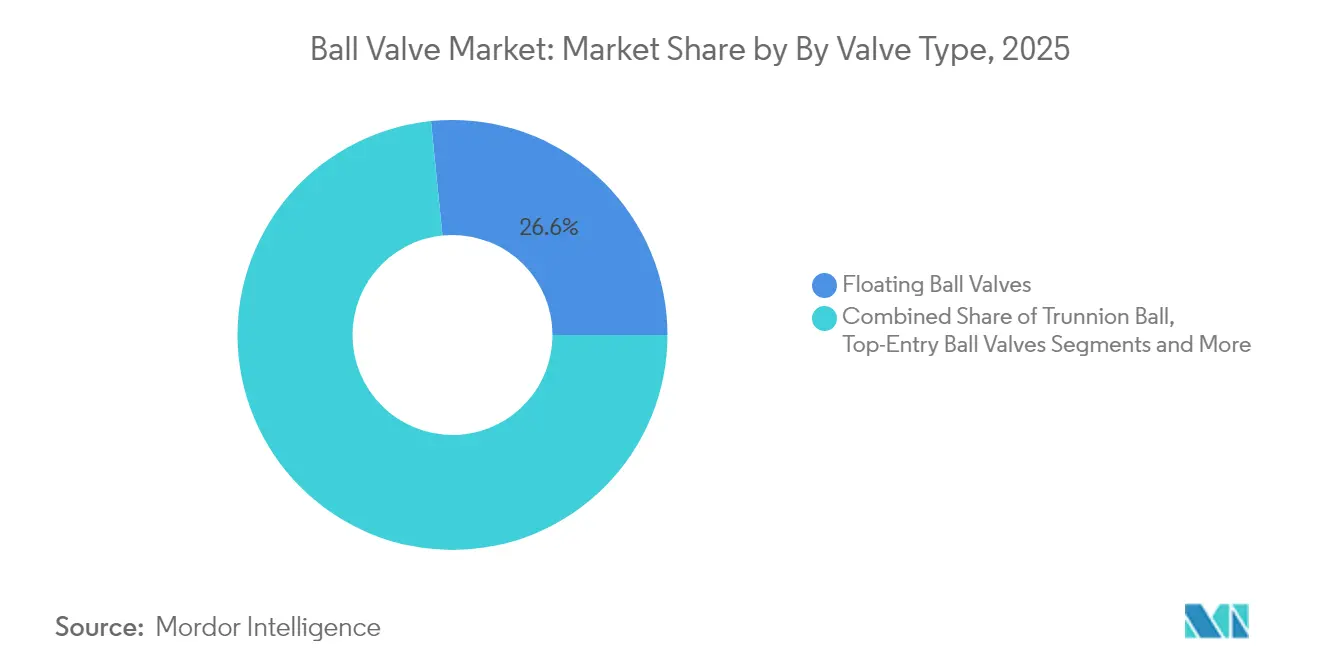

- By valve type, floating ball valves held 26.60% of Ball valve market share in 2025, while cryogenic designs are on course for a 6.12% CAGR to 2031.

- By material, carbon steel captured 31.50% of the Ball valve market share in 2025; alloy-based materials are expanding at a 5.07% CAGR through 2031.

- By valve size, the 1"–6" class led with 33.30% share of the Ball valve market size in 2025, whereas units above 50" are poised to grow 6.31% per year to 2031.

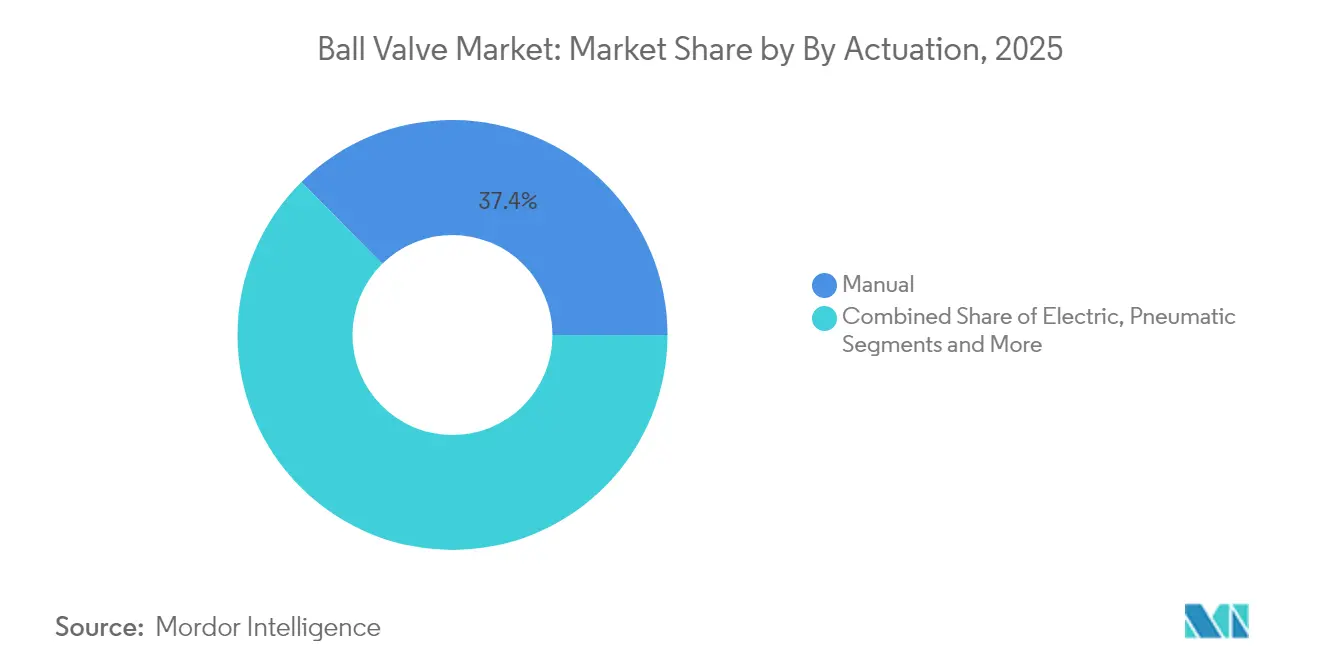

- By actuation, manual devices accounted for 37.40% share of the Ball valve market size in 2025; electric actuators represent the fastest track at a 6.02% CAGR.

- By end-user, oil and gas remained the biggest spender with 20.70% share in 2025; water and wastewater treatment is set to register a 5.83% CAGR to 2031.

- By region, Asia dominated the Ball valve market with 30.60% revenue in 2025; the Middle East is projected to pace growth at 4.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ball Valve Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated LNG Infrastructure Expansion in Emerging Asia Pacific | +0.8% | ASEAN core, spill-over to South Asia | Medium term (2-4 years) |

| Rising Adoption of Severe-Service Ball Valves in Hydrogen & CCS Projects across Europe | +0.6% | EU core, UK, Norway | Long term (≥ 4 years) |

| North American Mid-stream Asset Modernization Mandates Driving Replacement Demand | +0.5% | North America, selective Canadian provinces | Short term (≤ 2 years) |

| Rapid Digitalization of Water Utilities Spurs Smart Ball Valve Retrofit in Nordics | +0.3% | Nordic countries, selective EU markets | Medium term (2-4 years) |

| Surge in FPSO Deployments Boosting Cryogenic Ball Valve Uptake in Brazil & West Africa | +0.4% | Brazil, West Africa offshore | Medium term (2-4 years) |

| Regulatory Push for Low-Emission Valves in the Middle East | +0.2% | Middle East core, selective GCC states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated LNG Infrastructure Expansion in Emerging Asia Pacific

Asian governments view LNG as an immediate route to strengthen energy security and cut coal reliance. An 18% rise in global LNG export capacity in 2025, mainly aimed at Asian import terminals, magnifies demand for cryogenic ball valves rated to –162 °C. These units must guarantee methane-tight sealing throughout liquefaction, transport, and regasification duty, which favors vendors with deep metallurgical expertise and validated low-temperature testing records. Import-dependent markets such as Vietnam and the Philippines, lacking pipeline grids, are rolling out floating storage and regasification units that specify premium trunnion-mounted cryogenic valves. This requirement lifts average selling prices and insulates leading suppliers from substitution risk, reinforcing profitable growth for the Ball valve market.[1]Institute for Energy Economics and Financial Analysis, “Global LNG Outlook 2024-2028,” ieefa.org

Rising Adoption of Severe-Service Ball Valves in Hydrogen & CCS Projects across Europe

The EU’s plan to generate 10 million t of renewable hydrogen by 2030 requires pipelines and storage networks that can withstand pressures above 700 bar while avoiding hydrogen-induced cracking. Duplex and super-duplex alloys are moving into mainstream production to meet these mechanical demands and the corrosion challenges of supercritical CO₂ in carbon capture and storage (CCS) lines. Manufacturers that certify materials under evolving hydrogen standards enjoy a first-mover advantage, because plant owners seek proven safety documentation before awarding contracts. This trend cements Europe’s role as a technology test bed and enlarges the premium tier of the Ball valve market.

North American Mid-stream Asset Modernization Mandates Driving Replacement Demand

Pipelines built during the 1970s are approaching design end-life, and regulators now require upgraded valves that integrate real-time monitoring. Pipe, valve, and fitting (PVF) spend across the United States and Canada will climb to USD 42.5 billion in 2025. Operators emphasize reliability and superior sealing over unit price, which raises margins on replacement projects. Digital valve diagnostics, aligned with federal leak detection rules, form a core procurement criterion and push adoption of smart electric actuators deloitte.com. However, chronic forging shortages have stretched lead times past 30 weeks, prompting some projects to explore plug-valve alternatives in less-critical services.

Rapid Digitalization of Water Utilities Spurs Smart Ball Valve Retrofit in Nordics

Nordic utilities are using internet-of-things (IoT) retrofits to manage distribution losses. Scandinavian pilot programs show leakage ratios dropping from 30% to 10% after full automation, validating the value proposition for connected valves. Artificial-intelligence (AI) analytics embedded in supervisory control and data acquisition (SCADA) platforms predict wear patterns and schedule maintenance before failure, lowering operating costs. The economic case is strongest in high-labor-cost economies, where field inspections are expensive. The experience is influencing municipal utilities across continental Europe, scaling demand for retrofittable actuator kits that transform legacy ball valves into network assets.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Prolonged Lead-Times due to Global Forging Capacity Constraints | -0.4% | Global, acute in specialized alloys | Short term (≤ 2 years) |

| High Capital Outlay for Metal-Seated Valves in Abrasive Mining Applications | -0.2% | Mining-intensive regions globally | Medium term (2-4 years) |

| Increasing Preference for Plug & Butterfly Valves in Compact HVAC Systems | -0.3% | Global, concentrated in urban markets | Long term (≥ 4 years) |

| Volatile Stainless-Steel Prices Eroding Margins for Tier-2 Asian Manufacturers | -0.2% | Asia Pacific, selective emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prolonged Lead-Times due to Global Forging Capacity Constraints

A decade of supplier consolidation has left only a handful of open-die forges capable of producing large-diameter, nickel-alloy blanks. Simultaneous demand from aerospace and energy increases capacity strain, with delivery cycles stretching to 24–32 weeks versus the historical 12–16 week window. Project owners now embed buffer inventories or accept alternate valve styles if schedule risk outweighs technical benefit. Some OEMs pursue vertical integration, but capital needs and qualification timelines delay relief until late decade.[2]Supply House Times, “State of the industrial PVF market,” supplyht.com

High Capital Outlay for Metal-Seated Valves in Abrasive Mining Applications

Metal-seated ball valves using tungsten-carbide or ceramic inserts deliver long service life in slurry lines but can cost four times more than soft-seated versions. Many mines facing volatile commodity pricing choose lower-cost valves, accepting higher maintenance frequency. The trade-off restrains uptake in cash-constrained regions even though total cost of ownership favors premium designs in remote or deep-shaft operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Cryogenic Applications Drive Innovation

The Ball valve market size for floating designs logged 26.60% revenue in 2025, driven by their adaptability across refinery, water, and general-purpose services. Cryogenic ball valves, though niche, are rising at a 6.12% CAGR as LNG terminals and hydrogen export hubs demand guaranteed sealing down to –162 °C. End users emphasize zero-leakage seats and blow-out-proof stems validated by helium mass-spectrometer testing, a standard that raises entry barriers and sustains premium price realization.

Additive-manufactured flow paths, now field-proven in subsea pilots, reduce weight and pressure drop in fully welded bodies. Meanwhile, orbit and rising-stem variants preserve seat life where throttling duty would damage conventional floating valves. Together, these developments diversify product portfolios and extend the functional scope, preserving relevance of ball valves even in markets exploring butterfly or plug alternatives.

By Material: Alloy Innovation Meets Hydrogen Demands

Carbon steel held 31.50% share of the Ball valve market size in 2025 thanks to its favorable strength-to-cost ratio across pipelines and industrial utilities. Hydrogen projects now favor alloy-based bodies with super-duplex or austenitic grades to resist embrittlement, raising alloy demand at a 5.07% CAGR. Duplex grades also unlock higher allowable pressure ratings, enabling pipeline engineers to downsize schedules and shave capex.

Stainless-steel price volatility pushes OEMs to qualify dual-certified grades that meet both 304L and 316L requirements, streamlining procurement flexibility. Additive manufacturing introduces functionally graded materials where high-nickel matrices reinforce seat zones, while carbon-steel dominates outer shells, optimizing total cost.

By Valve Size: Large Bore Applications Command Premium

1"–6" valves delivered 33.30% of 2025 revenue yet face modest growth as industrial baseload demand stabilizes. Units above 50" show a 6.31% CAGR as LNG export trains and offshore risers scale diameter to move larger gas volumes. These valves require purpose-built machining centers and deep-hole boring, limiting global supply to fewer than 10 certified workshops.

Weight drives installation economics; thus, designers adopt forged bar sections with finite-element-optimized wall profiles that cut mass without lowering burst rating. Automated phased-array ultrasonic testing has become standard to assure defect-free forgings. The Ball valve market benefits through value-rich orders even if volumes are low compared with mid-size categories.

By Actuation: Electric Systems Gain Smart Integration

Manual gearboxes still dominate the Ball valve market, claiming 37.40% of 2025 shipments, because they suit applications with minimal cycling and on-site operator presence. Electric-actuated units are advancing at 6.02% CAGR as digital plant architectures require closed-loop control and predictive maintenance. Upgraded firmware now embeds HART, Modbus, and PROFINET in a single board, easing integration with distributed control systems.

Battery-backed solar kits broaden use in remote valve stations, while cloud analytics forecast stem torque trends that signal packing wear. Pneumatic drives retain a niche in explosion-hazard zones; hydraulic cylinders govern rapid-stroke emergency shut-down duty. The net result is a more heterogeneous actuation mix that deepens service revenue potential across the Ball valve industry.

By End-User Industry: Water Utilities Lead Growth Transition

Oil and gas contributed 20.70% of 2025 revenue but trails future growth as upstream budgets increasingly diversify into carbon-efficient ventures. Water and wastewater agencies will expand spend at 5.83% CAGR because regulatory targets for non-revenue water force utilities to modernize valves and telemetry. Evidence from Nordic pilot cities shows triple-offset leakage reductions, motivating capital allocations despite tight municipal budgets.

Chemical producers order high-alloy valves for corrosive streams; mining operations weigh premium metal seats against capex limits yet lean toward metal-seated upgrades in isolated sites where downtime is costly. Food, beverage, and pharmaceutical plants specify sanitary internals and traceable alloys, adding documentation-driven value to the Ball valve market.

Geography Analysis

Asia accounted for 30.60% of Ball valve market revenue in 2025, propelled by Chinese industrial growth and Southeast Asian LNG import terminals. Government policies that mandate cleaner energy mix underpin sustained valve procurement. India’s “Make in India” scheme fosters domestic valve production yet still relies on imported severe-service trims for hydrogen pilots. Japan and South Korea prioritize high-performance alloys for niche chemical processes, maintaining a technology premium in regional trade.

The Middle East is the fastest-growing cluster, projecting 4.94% CAGR to 2031 as operators retrofit low-emission valves in legacy fields and build green-field LNG mega-trains. Qatar’s North Field expansion alone calls for thousands of cryogenic units, while Saudi Aramco deploys smart actuators across gas gathering networks to satisfy methane-intensity goals. Turkey’s transit ambitions also translate into large-bore pipeline valve orders.

North America retains sizable share owing to mid-stream replacement mandates. Shale-gas gathering systems need high-pressure ball valves resistant to acid gases. Canadian oil sands lines demand hard-faced seats to manage bitumen abrasion. Mexico, opening its energy market, imports API 6D-certified valves for export-class pipelines. Climate regulation stimulates adoption of ISO-15848-1 certified products, adding incremental requirements that favor established brands.

Competitive Landscape

Industry structure is moderately concentrated. Emerson, Flowserve, and Schlumberger combine wide portfolios, aftermarket presence, and global service bases to anchor premium project awards. Technological differentiation now centers on digital valve twins, advanced alloys, and integrated severe-service packages rather than sheer manufacturing scale.

Acquisition activity reshapes product breadth. Flowserve’s USD 290 million purchase of MOGAS doubled its mining exposure, underscoring a strategy to absorb niche innovators rather than develop in-house flowserve.com. IMI plc secured North Sea anti-surge contracts by pairing additive-manufactured internals with proprietary drag-control trims, highlighting material and flow-path innovation as market levers.

Tier-2 Asian suppliers face cost headwinds because stainless-steel price surges cannot be passed through in fixed-price export tenders. Some move up the value chain by securing ISO-15848-1 certifications and forming alliances with actuator specialists to offer complete packages. Competitive pressure also arises from butterfly and plug manufacturers entering the Ball valve market with compact designs that address HVAC space constraints yet still meet moderate pressure needs.

Ball Valve Industry Leaders

Emerson Electric Co.

Flowserve Corporation

Schlumberger (Cameron)

IMI plc

Kitz Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Heap and Partners has designed and manufactured 12 of its Phase trunnion ball valves for a Serica Energy maintenance campaign this year at the Bruce Field facilities in the UK North Sea. The 16-inch valves were the largest produced by the company, weighing under four metric tons.

- February 2025: American Petroleum Institute released the 2025 API Standards International Usage Report highlighting 20% increase in global regulatory references to API standards, with 1,395 total references identified across international laws and regulations. This expansion indicates growing standardization in valve specifications and quality requirements across global markets.

- January 2025: American Petroleum Institute published first-edition standard API Recommended Practice 697 providing comprehensive guidance for pump inspection and repair, which includes related valve maintenance procedures. The standard aims to enhance safety, reduce emissions, and improve operations in oil and natural gas industry applications.

- November 2024: Emerson Electric reported 13% increase in net sales to USD 4,619 million for Q4 2024, with strong performance in Final Control segment that includes ball valve products. The company anticipates net sales growth of 3.5% to 5.5% for full year 2025, indicating continued momentum in automation solutions.

Global Ball Valve Market Report Scope

The ball valve is a spherical closure device that controls the flow and pressure of liquids and gases within a system. These quarter-turn valves use a hollow, perforated, and pivoting ball to control flow through it.

The ball valve market is segmented by material (cast iron, steel, alloy-based), end-user industry (oil and gas, chemicals, water and wastewater, power, food and beverage, pharmaceuticals), and geography (North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa).

The market sizes and predictions are provided in terms of value in USD for all the above segments.

| Floating Ball Valves |

| Trunnion-Mounted Ball Valves |

| Rising-Stem / Orbit Ball Valves |

| Top-Entry Ball Valves |

| Fully-Welded Ball Valves |

| Cryogenic Ball Valves |

| Carbon Steel |

| Stainless Steel |

| Cast Iron / Ductile Iron |

| Alloy-Based (Duplex, Inconel, Hastelloy) |

| Bronze and Brass |

| Other Materials |

| Up to 1" (DN 25) |

| 1" - 6" |

| 6 " - 25" |

| 25" - 50" |

| Above 50" |

| Manual |

| Electric |

| Pneumatic |

| Hydraulic |

| Electro-Hydraulic |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Water and Wastewater |

| Power Generation |

| Mining and Metals |

| Food and Beverage |

| Pharmaceuticals and Biotechnology |

| HVAC and Refrigeration |

| Pulp and Paper |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Valve Type | Floating Ball Valves | |

| Trunnion-Mounted Ball Valves | ||

| Rising-Stem / Orbit Ball Valves | ||

| Top-Entry Ball Valves | ||

| Fully-Welded Ball Valves | ||

| Cryogenic Ball Valves | ||

| By Material | Carbon Steel | |

| Stainless Steel | ||

| Cast Iron / Ductile Iron | ||

| Alloy-Based (Duplex, Inconel, Hastelloy) | ||

| Bronze and Brass | ||

| Other Materials | ||

| By Valve Size | Up to 1" (DN 25) | |

| 1" - 6" | ||

| 6 " - 25" | ||

| 25" - 50" | ||

| Above 50" | ||

| By Actuation | Manual | |

| Electric | ||

| Pneumatic | ||

| Hydraulic | ||

| Electro-Hydraulic | ||

| By End-User Industry | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Water and Wastewater | ||

| Power Generation | ||

| Mining and Metals | ||

| Food and Beverage | ||

| Pharmaceuticals and Biotechnology | ||

| HVAC and Refrigeration | ||

| Pulp and Paper | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Ball valve market size and projected growth?

The market stands at USD 13.57 billion in 2026 and is estimated to reach USD 16.23 billion by 2031, reflecting a 3.64% CAGR.

Which region leads the Ball valve market?

Asia accounts for 30.60% of 2025 revenue, supported by industrial expansion in China and new LNG terminals across Southeast Asia.

Which valve type is growing fastest?

Cryogenic ball valves show the highest growth trajectory at 6.12% CAGR through 2031 due to LNG and hydrogen demand.

Why are electric actuators gaining share?

Plant digitalization drives demand for remote monitoring and predictive maintenance, causing electric-actuated valves to expand at 6.02% CAGR.

How are forging shortages affecting the market?

Limited forging capacity has doubled delivery lead times for large-diameter and specialty-alloy valves, prompting some buyers to consider alternative valve types.

What is driving Ball valve adoption in water utilities?

Nordic utilities cut leakage rates by installing smart, IoT-enabled ball valves, stimulating global interest in digital retrofits that improve water-network efficiency.

Page last updated on: