Plastics Injection Molding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

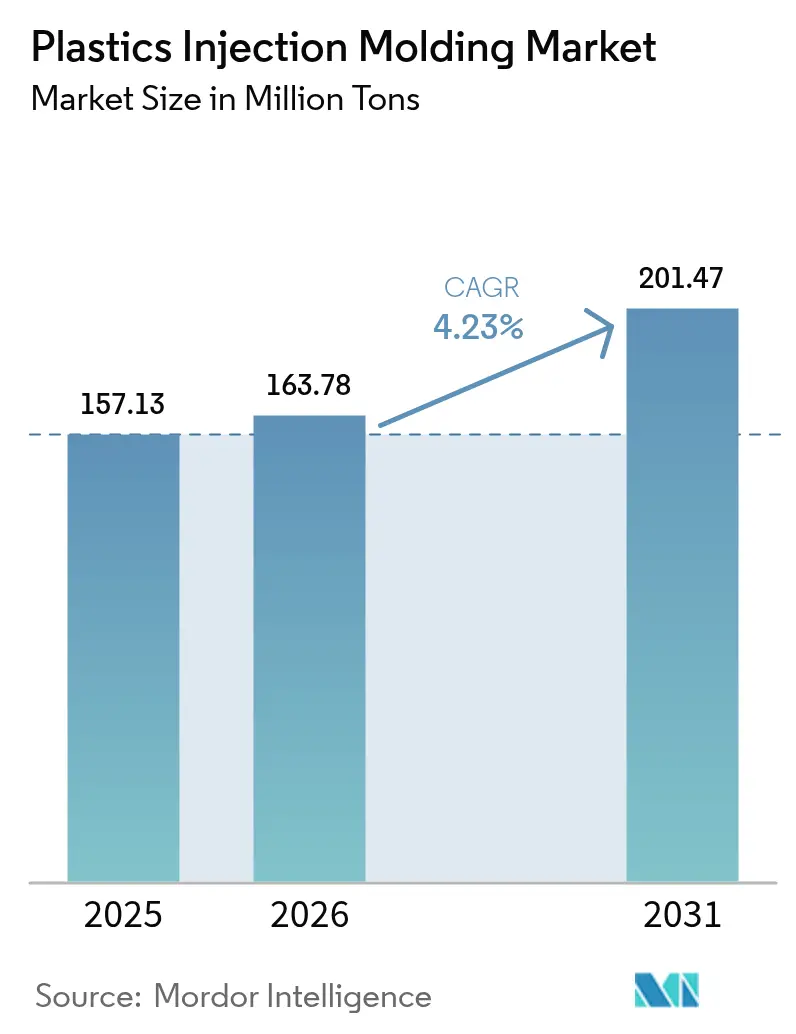

| Market Volume (2026) | 163.78 Million tons |

| Market Volume (2031) | 201.47 Million tons |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastics Injection Molding Market Analysis by Mordor Intelligence

The Plastics Injection Molding Market size was valued at USD 157.13 million tons in 2025 and estimated to grow from USD 163.78 million tons in 2026 to reach USD 201.47 million tons by 2031, at a CAGR of 4.23% during the forecast period (2026-2031). This sustained expansion underscores the technology’s centrality to cost-effective, large-volume manufacturing in packaging, automotive, electronics and medical devices. E-commerce growth, accelerating electric-vehicle (EV) production and regulatory pushes for circularity collectively widen the application base of the plastics injection molding market, while energy-efficient all-electric machines and advanced material formulations help producers offset rising input costs. Asia-Pacific’s growing electronics clusters, North American reshoring initiatives and Europe’s first-mover stance on recyclability regulations all amplify regional opportunities. At the same time, volatile crude-oil-linked resin pricing and tightening global anti-plastic rules temper profit margins and compel investments in recycled feedstocks, digital quality control and end-of-life traceability systems.

Key Report Takeaways

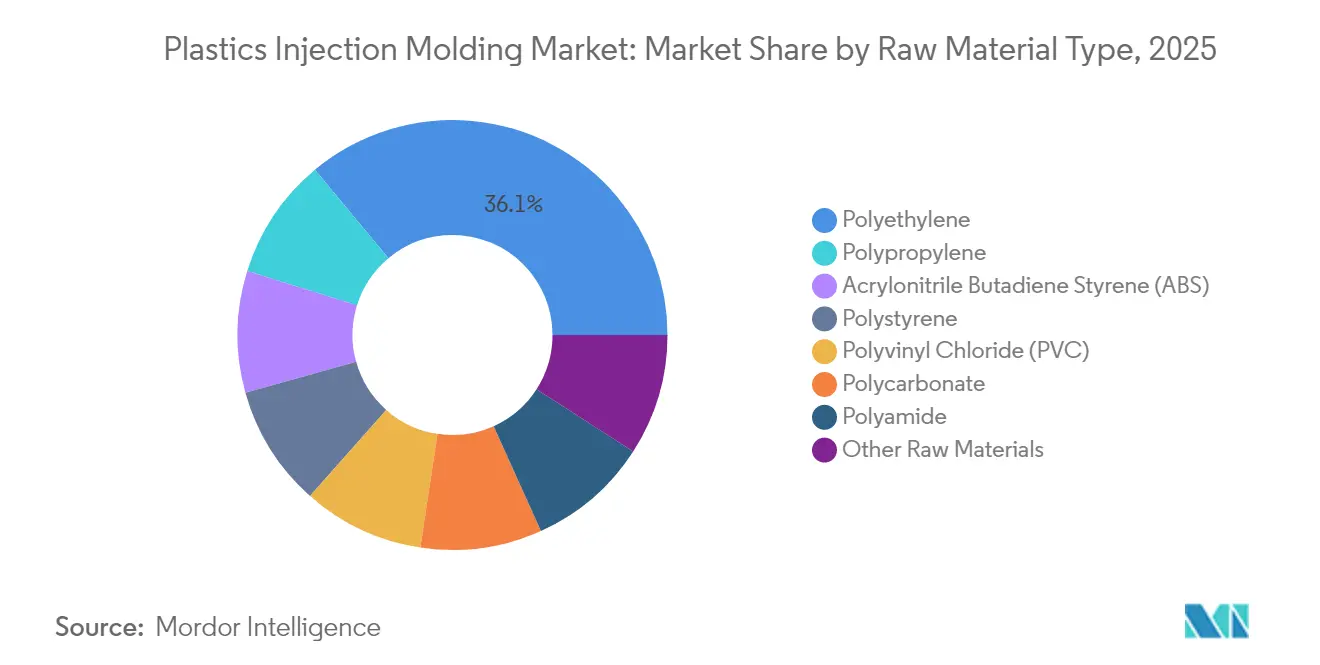

- By raw material, polyethylene captured 36.05% of plastics injection molding market share in 2025 and is projected to advance at a 5.02% CAGR through 2031.

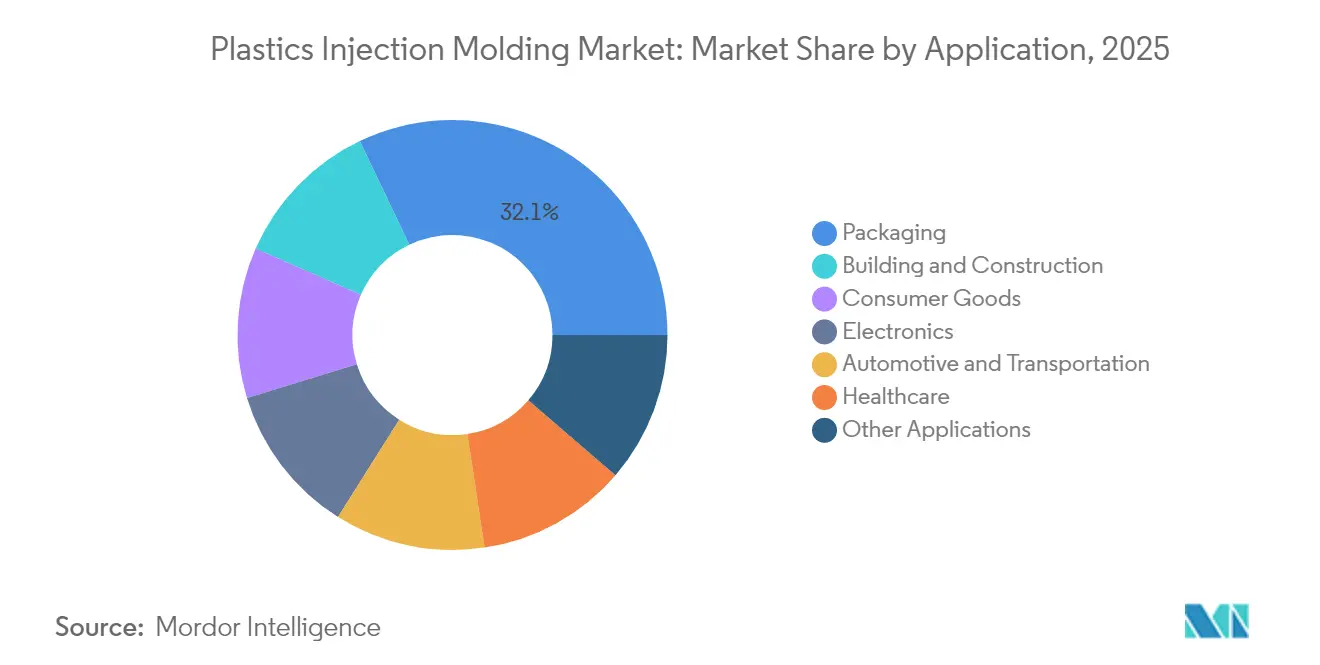

- By application, packaging accounted for 32.10% of the plastics injection molding market size in 2025, while automotive and transportation is set to expand the fastest at a 4.98% CAGR to 2031.

- By geography, Asia-Pacific commanded 34.10% share of the plastics injection molding market in 2025 and is growing at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastics Injection Molding Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce-driven packaging demand | +1.2% | Global; strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Lightweighting requirements in automotive and EVs | +0.9% | Europe and North America lead; global relevance | Long term (≥ 4 years) |

| Growing need for single-use medical disposables | +0.7% | Developed markets worldwide | Short term (≤ 2 years) |

| Industrialisation in APAC electronics manufacturing | +0.8% | Asia-Pacific core; spill-over to MEA | Medium term (2-4 years) |

| OEM adoption of injection-molded EV battery housings | +0.6% | Early adoption in China, Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce-Driven Packaging Demand

Explosive parcel volumes have heightened requirements for durable yet lightweight protective solutions, prompting brand owners to specify mono-material polyethylene and polypropylene packages that minimize material use without compromising strength. The EU Packaging and Packaging Waste Regulation (PPWR), effective 2025, mandates 30% recycled content in PET food packaging by 2030, accelerating redesign of tooling and process parameters to handle higher-recycled blends[1]Andrew Almack, “PPWR 2025: How the EU’s Packaging Waste Regulation Is Reshaping Sustainable Packaging,” Plastics for Change, plasticsforchange.org. U.S. Extended Producer Responsibility (EPR) fees across 14 states create an additional cost signal that rewards eco-modulated designs and favors converters with advanced resin reclamation lines. These converging mandates bolster volume growth in the plastics injection molding market, particularly in thin-wall container and closure segments where cycle-time reductions deliver material savings and higher throughput. Progressive molders are adopting in-mold labeling and digital watermarking to streamline sorting, increasing the likelihood of post-consumer resin availability and ensuring feedstock continuity.

Lightweighting Requirements in Automotive and EVs

Automotive OEMs have intensified plastics substitution to achieve stringent fleet-average CO₂ targets and maximize EV range. Tesla’s gigacasting strategy showcases how large aluminum castings reduce part counts, but it simultaneously expands demand for injection-molded interior and exterior trims that integrate with cast structures. Battery manufacturers are exploring thermoplastic housings with flame-retardant sandwich walls that cut up to 40 kg per vehicle compared with steel alternatives, a shift exemplified by Engel’s high-voltage battery enclosure prototype. ISO 14040 life-cycle assessments increasingly influence material choices, favoring recyclable resins over multi-material metal assemblies. These trends elevate engineering-grade polymers such as polyamide, polycarbonate and recycled polypropylene, widening the value pool of the plastics injection molding market through higher content per vehicle and sustained tooling demand for new EV platforms.

Growing Need for Single-Use Medical Disposables

Post-pandemic healthcare investment has driven hospitals to standardize on single-use syringes, pipettes and diagnostic cartridge systems, powering expansion of ISO 13485-certified molding capacity. DuPont’s USD 313 million acquisition of Donatelle Plastics typifies supplier consolidation aimed at capturing specialty device growth lanes. Equipment advances such as Husky’s ICHOR multi-cavity systems enable sub-two-second cycle times for drug-delivery components, boosting economies of scale. Precision resins like cyclic olefin copolymer (COC) meet optical clarity and chemical inertness requirements in infusion pumps, reinforcing the premium positioning of healthcare volumes within the plastics injection molding market. Demographic aging, elevated chronic-disease incidence and rising surgical procedures cement a long runway for single-use device expansion.

OEM Adoption of Injection-Molded EV Battery Housings

Vehicle makers are scrutinizing thermoplastic housings to reduce mass and improve crash energy absorption. BYD’s Yangwang U7 program employs two-platen presses to mold rear spoilers within ±0.3% weight tolerance, illustrating the precision achievable on large exterior panels. SABIC’s recycled polycarbonate-polybutylene-terephthalate blend offers UL 94 V-0 flame resistance without glass reinforcement, eliminating secondary finishing steps. Integrating structural ribs and cooling channels in a single molding cycle shortens assembly times and reduces part counts. Regulatory frameworks such as IATF 16949 enforce traceability and process control, raising qualification hurdles that protect incumbents positioned in this high-growth pocket of the plastics injection molding market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil-linked resin pricing | -1.1% | Worldwide; import-reliant economies hit hardest | Short term (≤ 2 years) |

| Tightening global anti-plastic regulations | -0.8% | Europe and developed markets spearhead | Medium term (2-4 years) |

| Cap-ex and skills gap for all-electric high-tonnage presses | -0.5% | Concentrated in emerging economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil-Linked Resin Pricing

Polyethylene and polypropylene spot prices rose as crude benchmarks responded to geopolitical disruptions. U.S. tariffs introduced in 2025 raised landed costs of some resin grades by 10-15%, while Chinese oversupply, estimated at an additional 5 million tons of capacity, depressed Asian quotes and widened inter-regional arbitrage spreads. Resin distributors cite unprecedented uncertainty, with 82% of converters pursuing multisourcing strategies to guard against price spikes. Margin volatility discourages long-term tooling commitments, raising the hurdle rate for capacity additions across the plastics injection molding market and nudging processors toward hedging instruments and formula-pricing contracts.

Tightening Global Anti-Plastic Regulations

The EU PPWR’s recyclability and minimum recycled content mandates, together with national single-use bans effective 2030, are compelling redesign of entire product portfolios. In the United States, EPR fees projected at USD 4.7 billion by 2026 act as de-facto material taxes, lifting total landed costs for conventional resins. Compliance demands investment in certification, track-and-trace systems and recycled-content verification, hitting smaller converters hardest and slowing new-product launches. These headwinds curb near-term expansion of the plastics injection molding market, though they concurrently spur innovation in bio-based blends and closed-loop logistics that may unlock longer-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material Type: Polyethylene Dominance Drives Sustainability Transition

Polyethylene secured a commanding 36.05% share of the plastics injection molding market in 2025 and is on track for a 5.02% CAGR through 2031 as recycled-content mandates reinforce its recyclability advantage. This leadership is fueled by thin-wall packaging, cap-and-closure systems and emerging automotive fuel-cell components that capitalize on the resin’s chemical resistance. Polypropylene follows closely in interior automotive trims, HVAC housings and appliance parts, leveraging high heat deflection and stiffness-to-weight ratios. Acrylonitrile butadiene styrene retains niche in consumer electronics casings, while polystyrene faces structural decline in single-use cutlery amid regulatory crackdowns.

Advanced recycling facilities capable of depolymerization and solvent-based purification are improving the quality of post-consumer polyethylene, enabling drop-in replacement for virgin resin and lowering scope-3 emissions for converters. Polycarbonate uptake advances steadily in headlamp lenses and transparent protective shields, with thin-gauge glazing options replacing heavier glass in certain automotive models. Bio-based polyamides produced from castor-bean oil are gaining interest in under-hood parts due to inherent flame retardancy and lower carbon intensity. These material-level shifts deepen the diversification of the plastics injection molding market while supporting clients’ environmental, social and governance (ESG) objectives.

By Application: Packaging Leadership Meets Automotive Innovation

Packaging retained 32.10% of the plastics injection molding market share in 2025 on the back of omnichannel retail expansion and heightened food-safety requirements. Mono-material closures, dispensing pumps and tamper-evident containers dominate new-product pipelines, reflecting retailers’ preference for fully recyclable formats. Concurrently, the automotive and transportation vertical is forecast to accelerate at 4.98% CAGR through 2031, buoyed by EV penetration and lightweighting mandates that elevate plastics content per unit.

Building and construction applications contribute steady volume through window profiles, electrical conduit and infrastructure fittings, particularly in emerging markets with rapid urbanization. Electronics demand gravitates toward high-precision micro-molding for camera modules and wearable devices, running ultra-fast cycles on all-electric presses. Healthcare maintains premium margins owing to stringent validation, with cyclic olefin copolymer and medical-grade polypropylene seeing robust offtake in single-use drug-delivery systems. These diverse end-uses collectively reinforce the resilience of the plastics injection molding market, enabling processors to balance cyclical sectors against more stable healthcare and packaging streams.

Geography Analysis

Asia-Pacific held 34.10% of the plastics injection molding market in 2025 and is expanding at a 5.24% CAGR to 2031 as China, India, and Southeast Asia scale electronics and automotive output. Government incentives, lower labor costs, and proximity to downstream assembly plants underpin capacity additions. Japan is leveraging digital twins and carbon-footprint dashboards across more than 80% of factories to heighten productivity and sustainability. North America benefits from reshoring and nearshoring, with Mexico securing USD 43.9 billion in FDI during 2023 that spurs tooling imports and turnkey cell installations for automotive interiors.

The United States’ USD 1.4 trillion reindustrialization plan supports semiconductor, EV battery and medical-device capacity that will boost domestic resin offtake. Canada’s mold-making clusters in Ontario continue to supply high-cavitation tools for consumer-packaging programs, though wage premiums encourage higher degrees of automation.

European converters are investing in depolymerization and solvent-based purification plants to meet PPWR requirements for 30% recycled content in PET packaging by 2030. Germany’s engineering prowess underpins advanced multi-component molding for premium vehicles, while France scales bio-based cosmetic packaging aligned with consumer eco-preferences. South America depends on Brazilian automotive demand, with localized content rules compelling higher domestic plastic part production.

The Middle East and Africa are expanding through Saudi Arabia’s polymer downstream investments and South Africa’s tooling grant scheme aimed at stimulating localized part production. These diverse regional dynamics collectively broaden the geographic footprint of the plastics injection molding market.

Competitive Landscape

The market is highly fragmented, with regional contract molders coexisting alongside global integrated players spanning resins, machines and finished parts. Contract molding sees roll-ups aimed at regulated niches: DuPont’s Donatelle deal targets ISO 13485 medical capabilities, while Berry’s acquisition of CMG Plastics strengthens short-run food-packaging programs. Sustainability credentials act as a competitive differentiator. Meanwhile, automation retrofits with smart auxiliaries are proliferating; cooling units with machine-learning-based flow balancing and material-handling robots with condition-monitoring cut unplanned downtime and standardize part quality.

Plastics Injection Molding Industry Leaders

ALPLA

Amcor PLC

AptarGroup, Inc.

Magna International Inc.

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SEKISUI CHEMICAL announced a sixth plant in Pune, India, for automotive injection-molded products, investing USD 3 million with operations slated for January 2026.

- January 2024: Arterex completed the acquisition of Micromold, broadening precision-component capacity for next-gen medical devices.

Global Plastics Injection Molding Market Report Scope

Injection molding plastics are produced to obtain molded products by injecting plastic materials molten by heat into a mold and then cooling and solidifying them. The plastics injection molding market is segmented by raw material, application, and geography. By raw material, the market is segmented into polypropylene, acrylonitrile butadiene styrene (ABS), polystyrene, polyethylene, polyvinyl chloride (PVC), polycarbonate, polyamide, and other raw materials. By application, the market is segmented into packaging, building and construction, consumer goods, electronics, automotive and transportation, healthcare, and other applications. The report also covers the market size and forecasts for plastics injection molding in 15 countries across major regions. The market sizing and forecasts are based on volume (kilotons) for each segment.

| Polypropylene |

| Acrylonitrile Butadiene Styrene (ABS) |

| Polystyrene |

| Polyethylene |

| Polyvinyl Chloride (PVC) |

| Polycarbonate |

| Polyamide |

| Other Raw Materials |

| Packaging |

| Building and Construction |

| Consumer Goods |

| Electronics |

| Automotive and Transportation |

| Healthcare |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material Type | Polypropylene | |

| Acrylonitrile Butadiene Styrene (ABS) | ||

| Polystyrene | ||

| Polyethylene | ||

| Polyvinyl Chloride (PVC) | ||

| Polycarbonate | ||

| Polyamide | ||

| Other Raw Materials | ||

| By Application | Packaging | |

| Building and Construction | ||

| Consumer Goods | ||

| Electronics | ||

| Automotive and Transportation | ||

| Healthcare | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the plastics injection molding market in 2026?

The market reached 163.78 million tons in 2026 and is projected to grow to 201.47 million tons by 2031.

What is the forecast CAGR for plastics injection molding through 2031?

Industry volumes are expected to expand at a 4.23% CAGR between 2026 and 2031.

Which region leads current demand?

Asia-Pacific holds 34.10% of global volume thanks to robust electronics and automotive manufacturing.

Which raw material has the highest growth outlook?

Polyethylene tops both volume (36.05% share) and growth (5.02% CAGR) due to recycling initiatives and packaging demand.

What end-use segment is growing the fastest?

Automotive and transportation parts are forecast to rise at a 4.98% CAGR through 2031, propelled by EV lightweighting needs.

Page last updated on: