Micro Injection Molded Plastic Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

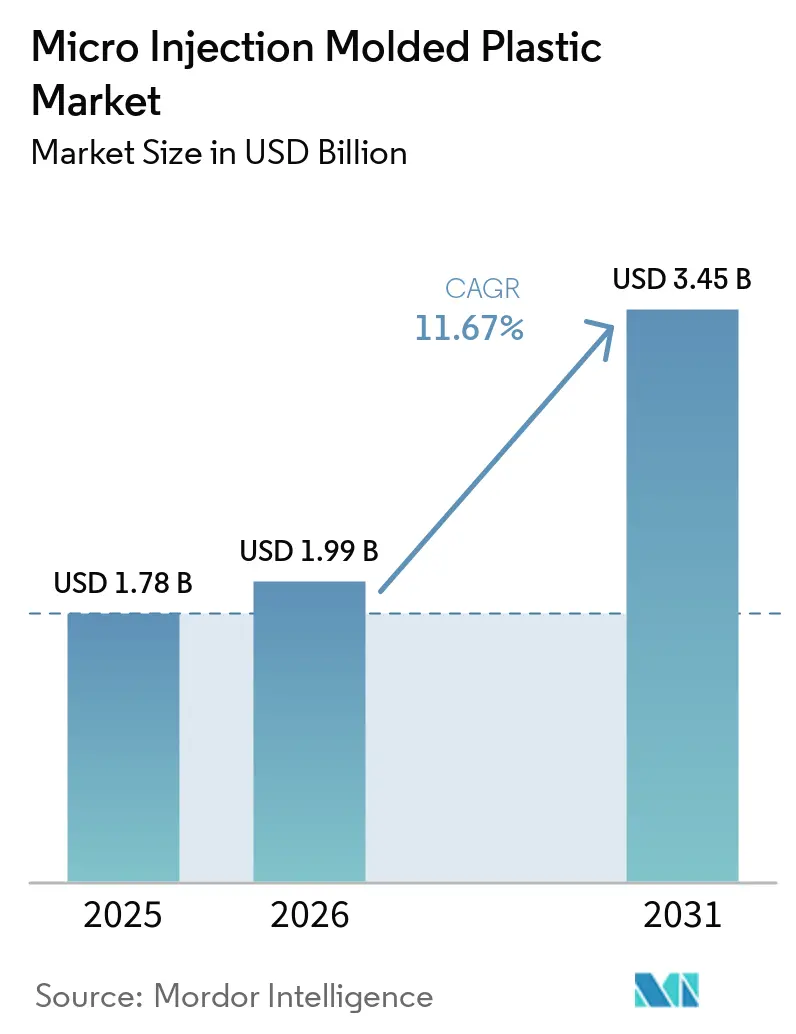

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 3.45 Billion |

| Growth Rate (2026 - 2031) | 11.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro Injection Molded Plastic Market Analysis by Mordor Intelligence

The Micro Injection Molded Plastic Market size is expected to increase from USD 1.78 billion in 2025 to USD 1.99 billion in 2026 and reach USD 3.45 billion by 2031, growing at a CAGR of 11.67% over 2026-2031. Demand is accelerating as automakers swap legacy silicon micro-electromechanical systems for high-temperature polymers that survive 150°C under-hood environments without exceeding a 0.2% scrap ceiling now enforced by AI-enabled in-line metrology. Liquid crystal polymers (LCPs) are gaining favor because their 0.002 loss tangent at 28 GHz supports mmWave antenna-in-package modules for 6G infrastructure, while their moisture uptake stays below 0.04%, preserving dimensional stability. Healthcare and diagnostics still dominate revenue, but wearable electronics are growing faster as stretchable polymer transistors yield 55,000 devices per square centimeter at 3 kHz switching speeds. Asia-Pacific leads volume growth thanks to China’s precision-mold output trajectory toward CNY 1 trillion by 2030, even though the region’s average tolerance of 0.03–0.05 mm lags Japan’s 0.01-0.02 mm benchmark.

Key Report Takeaways

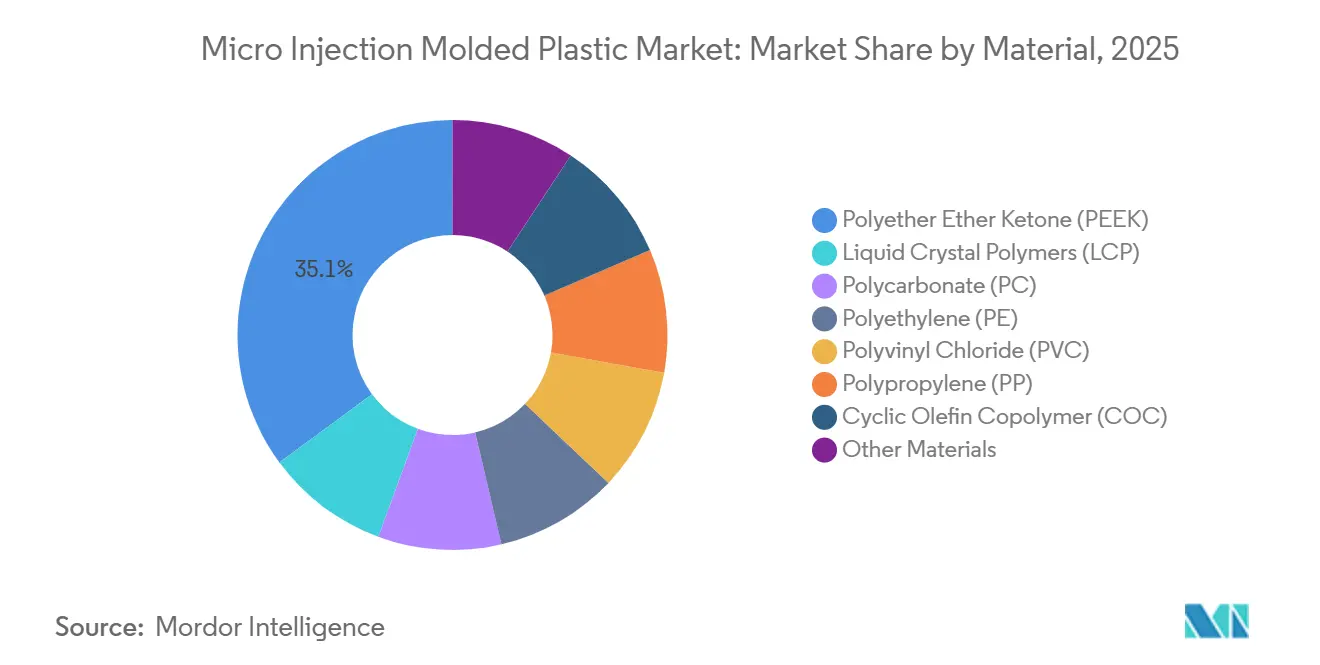

- By material, polyether ether ketone held the largest 35.11% micro injection molded plastic market share in 2025, while liquid crystal polymers are forecast to expand at a 12.10% CAGR through 2031.

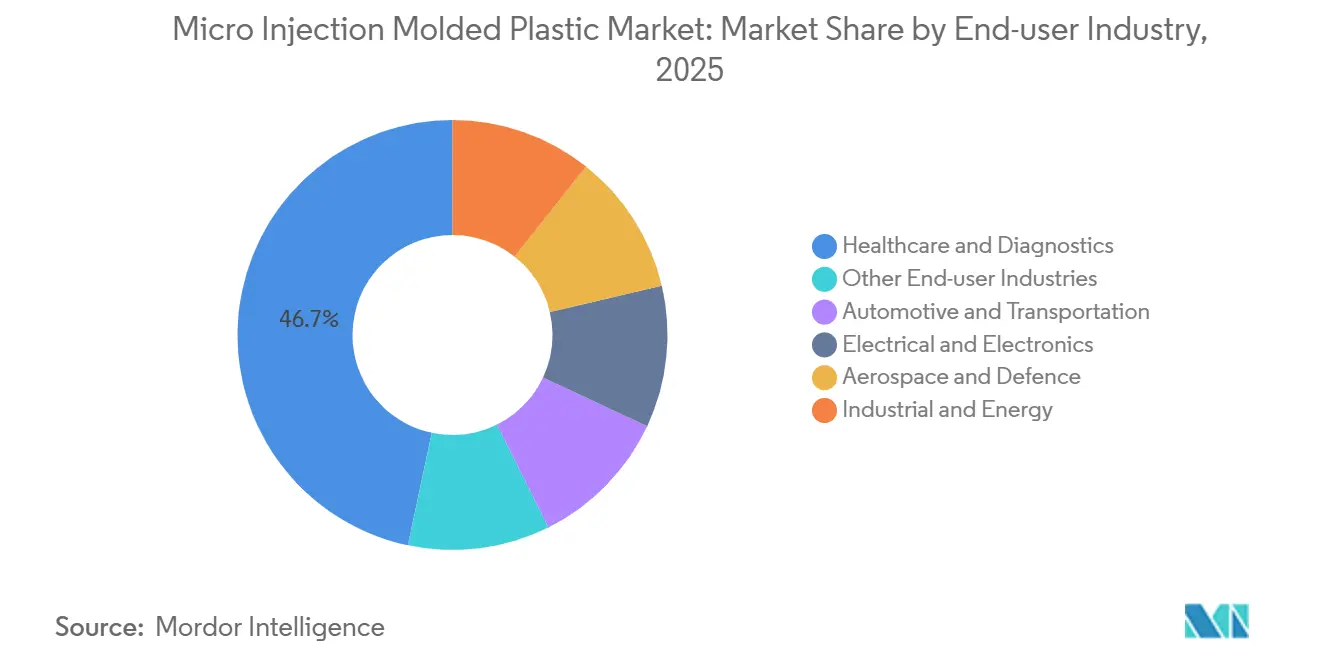

- By end-user industry, healthcare and diagnostics accounted for a 46.68% share of the micro injection molded plastic market size in 2025; electrical and electronics is advancing at a 12.68% CAGR to 2031.

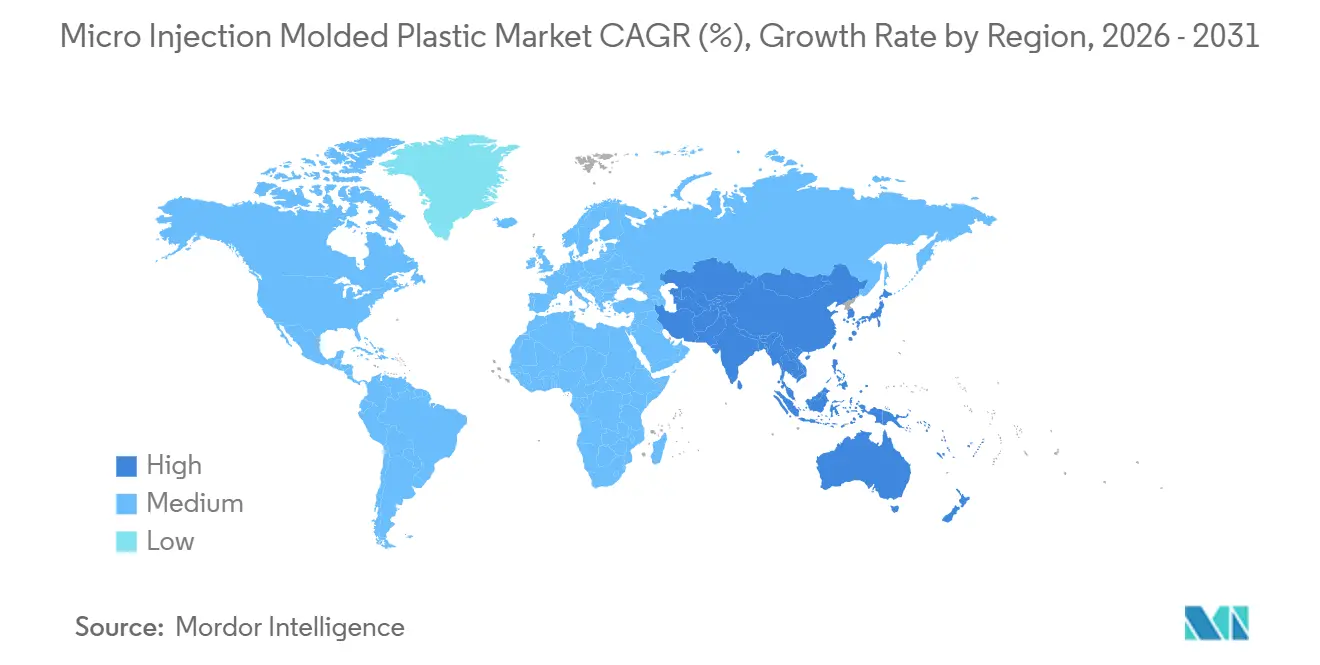

- By geography, Asia-Pacific captured 41.12% of 2025 revenue and is projected to grow at a 12.51% CAGR through 2031, outpacing all other regions over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Micro Injection Molded Plastic Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-plastic needs in automotive sensors | +2.8% | Germany, Japan, South Korea, U.S. Midwest | Medium term (2-4 years) |

| Migration from MEMS silicon to high-temperature polymers | +2.3% | China, Taiwan, South Korea, North America | Medium term (2-4 years) |

| Rising adoption of minimally-invasive drug-delivery systems | +3.1% | North America, EU, APAC | Long term (≥4 years) |

| AI-enabled in-line metrology cutting scrap below 0.2% | +1.9% | Global, led by Germany, Japan, U.S. hubs | Short term (≤2 years) |

| mmWave LCP connectors for 5G/6G antenna arrays | +1.6% | China, South Korea, Taiwan, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Precision-Plastic Needs in Automotive Sensors

Advanced driver-assistance vehicles contain up to 30 discrete sensors, each housed in polymer enclosures that tolerate -40°C to 150°C cycles without dimensional creep beyond 0.05 mm, eliminating aluminum die-castings that attenuate 77 GHz radar signals. PEEK and LCP radomes cut per-part costs 60% versus machined metal, and a 2024 polycarbonate roof-sensor module integrated seals and bosses in one 18-second shot, reducing warranty water-ingress claims by 40%[1]Covestro, “Polycarbonate Sensor Module Cuts Assembly Steps,” covestro.com. Automakers are redesigning toward centralized zone controllers, shrinking sensor footprints 30% by 2028, which requires wall thicknesses below 0.5 mm that only presses under 50 tons can repeatably mold.

Migration from MEMS Silicon to High-Temperature Polymers

Silicon micro-electromechanical dies cost USD 2-4 each and fracture above 1,500G, whereas molded polymers deliver similar performance for USD 0.80–1.20 per part and survive 2,000-hour 125 °C aging with less than 2% drift. LCP substrates, qualified by TSMC and Samsung in 2025, support antenna-in-package modules that remove discrete RF connectors and cut 28 GHz insertion loss by 0.8 dB[2]Advanced Industrial & Engineering Polymer Research, “Low-Loss LCP Substrates for 5G Packaging,” advancedpolymerresearch.com. By 2028, polymers are expected to carry 20% of advanced-node chiplets, though aerospace still favors radiation-hard silicon above 100 kilorads.

Rising Adoption of Minimally-Invasive Drug-Delivery Systems

Micro-molded parts for syringes, pens, and microneedle patches totaled 8 billion units in 2025 and are set to double by 2030 as self-administered biologics replace intravenous dosing. Polymer microneedles 0.5-1 mm long with 50 µm tips bypass nociceptors, raising adherence by 35% over hypodermic needles. The FDA cleared three microneedle-based products in 2025, while the EMA issued draft sterility guidance that aligns polymer patches with parenteral norms, accelerating European launches.

AI-Enabled In-Line Metrology Cutting Scrap Below 0.2%

Inline CT scanners now capture 10,000-point data clouds per shot and drive machine-learning loops that adjust velocity, pack pressure, and mold temperature within two-second cycles. Fraunhofer IPT’s SURFinloop system trimmed average scrap from 1.8% to 0.15% across 12 German Tier-1 facilities, saving EUR 4.2 million a year per 50-press plant. ISO 13485 auditors now accept AI-validated CpK ≥1.67, shortening medical-device submissions by up to 12 weeks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of ultra-precision toolmakers | −1.4% | North America, Europe, Japan | Medium term (2-4 years) |

| Limited global supply of implant-grade bio-absorbable polymers | −0.9% | U.S., EU, APAC | Long term (≥4 years) |

| Resin lot-to-lot variability triggering device re-validation | −0.7% | Global, with highest regulatory friction in U.S. & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Ultra-Precision Toolmakers

Fewer than 50 tool shops worldwide hold ±1 µm capability across 128-cavity molds, and 2025 lead times stretched to 22 weeks. Yuwa Corporation’s network covers only 12% of Asia-Pacific sub-0.1 g shot demand, while North American reshoring plans worth USD 800 million risk delays because 15% of senior machinists retire annually. LCP molds exacerbate capacity strain by needing 40% more machining hours than isotropic materials.

Limited Global Supply of Implant-Grade Bio-Absorbable Polymers

Only six producers operate certified reactors for over 99.5% purity of PCL, PLA, and PGA. Implant-grade PCL capacity was 4,200 tons in 2025 against a 12,000 tons requirement by 2030. Volatile lactide monomer prices swung ±35% in 2024, forcing OEMs into 18-month fixed-price contracts that shift commodity risk to molders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Performance Polymers Drive Premium Applications

Polyether ether ketone (PEEK) accounted for 35.11% of 2025 revenue, reflecting entrenched use in spinal implants and 150°C automotive sensors. Liquid crystal polymers’ 12.10% CAGR during 2026-2031 will reshape the micro injection molded plastic market size for high-frequency packages because their 0.002 loss tangent halves mmWave insertion loss versus polyimide. Polycarbonate holds ophthalmic devices owing to 89% transparency, although its 147°C Tg limits under-hood deployment. Cyclic olefin copolymer underpins point-of-care PCR plates that endure 100°C cycling without warpage, whereas polyethylene and polypropylene remain cost-driven choices for labware priced under USD 0.10 per part.

Equipment investments now pivot around closed-loop mold-temperature controllers and inline CT scanners that secure CpK greater than or equal to1.67 for PEEK and LCP geometries. That uptick in capital elevates barriers for mid-tier contract molders and will keep the micro injection molded plastic industry concentrated in fewer hands within material-intensive niches. Suppliers able to guarantee melt-temperature control within ±5°C are positioned to capture additional micro injection molded plastic market share from commodity molders.

By End-User Industry: Medical Dominates, Electronics Accelerates

Healthcare and diagnostics accounted for 46.68% of 2025 demand, anchored by pre-filled syringes, insulin pens, and microneedle patches. Electrical and electronics is projected to be the fastest riser at 12.68% CAGR through 2031 as flexible sensors in wearables speed adoption of sub-0.1g LCP and COC parts. Automotive tracks the headline micro injection molded plastic market growth rate, but radar-radome shifts from polycarbonate to LCP sustains value over volume. Aerospace claims <5% revenue yet commands USD 8–15 per part due to AS9100 traceability norms.

ISO 13485 certification remains a gating factor; audit slots now run nine months, nudging OEMs to renew multiyear contracts with incumbent suppliers. Electronics buyers, meanwhile, demand halogen-free resins that meet UL 94 V-0 at 0.75 mm, adding USD 1.20–1.80/kg and nudging up the micro injection molded plastic market size for flame-retardant grades.

Geography Analysis

Asia-Pacific owned 41.12% of 2025 revenue and is forecast to expand at 12.51% CAGR during 2026-2031 as China’s precision-mold industry heads toward CNY 1 trillion output by 2030. Japanese toolmakers’ ±0.01 mm capability commands 15–20% premiums but remains essential for implants, while South Korea’s semiconductor packaging drives local LCP consumption. ASEAN nations attracted USD 31 billion in 2024 electronics FDI, positioning Vietnam and Malaysia as overflow hubs within China-plus-one strategies.

North America and Europe trail Asia-Pacific growth by 3-4 points. The United States hosts eight of the fifteen largest micro-molders, including Tessy Plastics with USD 460 million in 2025 sales, but a shortage of ultra-precision toolmakers has pushed new-mold lead times past 22 weeks. Germany’s Baden-Württemberg and Bavaria clusters leverage Fraunhofer IPT metrology to sustain scrap at 0.15% and enable economical 5,000-part runs. EU Medical Device Regulation traceability rules, fully enforced in 2024, tack on 8-12 weeks to first-time device filings, favoring incumbents with ISO 13485 pedigrees.

South America and Middle East-Africa are witnessing considerable market growth. Brazil’s 60% domestic-content rule for sensors, effective 2027, is forcing Tier-1s to pre-qualify three local molders. Saudi Arabia’s King Salman Medical City tenders specify domestic ISO 13485 suppliers, creating USD 120 million annual demand currently met 90% by imports. Currency volatility in Argentina pushes contracts toward euro denomination, while Egypt and Morocco pursue 40% local content in pre-filled syringes by 2028.

Competitive Landscape

The micro injection molded plastic market is moderately consolidated. Leaders operate Class 7/8 cleanrooms and maintain fleets of greater than or equal to 40 micro presses with ±0.5 µm metrology. Tessy Plastics illustrates this model, running 400 presses across 3.2 million ft² and holding 0.0005-inch tolerances. MTD Micro Molding doubled its floor space in 2024 to meet radar-radome and medical-device demand requiring ±0.02 mm repeatability.

Strategic focus is shifting from press count to process-engineering depth. Absolute Haitian’s HT-XTEND platform shaved mold-setup time from 16 hour to 4 hour via edge-AI, making sub-5,000-unit lots economical. Fraunhofer IPT’s SURFinloop predictive control trimmed scrap to 0.15%, delivering EUR 4.2 million annual savings per 50-press plant. New entrants deploy additive-manufactured inserts to cut design-to-first-article cycles by 40% and profitably address orders under 50,000 units, eroding incumbents’ scale advantage.

Micro Injection Molded Plastic Industry Leaders

Accu-Mold

Makuta, Inc.

MTD Micro Molding

SMC Ltd.

ARTEREX

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: MTD Micro Molding inaugurated an expanded facility that doubles manufacturing area and boosts capacity for ±0.02 mm automotive radar-radome and medical-device parts.

- February 2026: Accumold unveiled 0.004-inch wall cannula molding at MD&M West, achieving 40 million pieces annually in ISO 13485 suites.

Global Micro Injection Molded Plastic Market Report Scope

Micro injection molded plastic is the material designed to produce small, high-precision plastic components, typically weighing between 0.1 and 1 gram, with tolerances ranging from 10 to 100 microns. These components are essential for creating complex miniaturized parts used in industries such as medical, electronics, and automotive.

The micro injection molded plastics market is segmented by material, end-user industry, and geography. By material, the market is segmented into polyether ether ketone (PEEK), liquid crystal polymers (LCP), polycarbonate (PC), polyethylene (PE), polyvinyl chloride (PVC), polypropylene (PP), cyclic olefin copolymer (COC), and other materials. By end-user industry, the market is segmented into Healthcare and diagnostics, automotive and transportation, electrical and electronics, aerospace and defence, industrial and energy, and other end-user industries. The report also covers the market size and forecasts for the micro injection molded plastic market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Polyether Ether Ketone (PEEK) |

| Liquid Crystal Polymers (LCP) |

| Polycarbonate (PC) |

| Polyethylene (PE) |

| Polyvinyl Chloride (PVC) |

| Polypropylene (PP) |

| Cyclic Olefin Copolymer (COC) |

| Other Materials |

| Healthcare and Diagnostics |

| Automotive and Transportation |

| Electrical and Electronics |

| Aerospace and Defence |

| Industrial and Energy |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Polyether Ether Ketone (PEEK) | |

| Liquid Crystal Polymers (LCP) | ||

| Polycarbonate (PC) | ||

| Polyethylene (PE) | ||

| Polyvinyl Chloride (PVC) | ||

| Polypropylene (PP) | ||

| Cyclic Olefin Copolymer (COC) | ||

| Other Materials | ||

| By End-user Industry | Healthcare and Diagnostics | |

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Aerospace and Defence | ||

| Industrial and Energy | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the micro injection molded plastic market by 2031?

Value is forecast to reach USD 3.45 billion, growing at an 11.67% CAGR over 2026-2031.

Which material holds the largest revenue share?

Polyether ether ketone led with 35.11% share in 2025, anchored by implants and high-temperature automotive sensors.

Which end-user segment is expanding the fastest through 2031?

Electrical and electronics applications are advancing at a 12.68% CAGR through 2031, driven by wearable devices that integrate high-density stretchable transistors.

Why are liquid crystal polymers preferred for 5G and 6G antenna-in-package modules?

LCPs combine a 0.002 loss tangent at 28 GHz with less than 0.04% moisture absorption, keeping insertion loss below 0.3 dB/cm and dimensional drift under ±0.01 mm.

Which region will post the highest growth rate during the forecast period?

Asia-Pacific is projected to expand at a 12.51% CAGR through 2031, propelled by China’s precision-mold investment and semiconductor packaging demand across South Korea and Japan.

What production technology is cutting scrap rates below 0.2%?

AI-enabled inline metrology platforms such as Fraunhofer IPT’s SURFinloop adjust molding parameters in real time, trimming average scrap to 0.15%.

Page last updated on: