Plastic Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 30.41 Billion |

| Market Size (2031) | USD 38.28 Billion |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Additives Market Analysis by Mordor Intelligence

The Plastic Additives Market size is projected to be USD 29.05 billion in 2025, USD 30.41 billion in 2026, and reach USD 38.28 billion by 2031, growing at a CAGR of 4.71% from 2026 to 2031. Robust demand for higher-performance formulations that answer lightweight-vehicle, compostable-packaging, and antimicrobial-surface requirements is steering value creation from commodity volume toward specialty grades. Electric-vehicle makers are specifying heat-stable, flame-retardant additive packages that tolerate 150 °C operating environments, driving price realization that outpaces resin cost inflation. Meanwhile, compostable-packaging mandates in the European Union and California are lifting bio-derived masterbatch demand, where 20%–30% price premiums over titanium-dioxide blends remain defendable. Post-pandemic hygiene protocols have permanently embedded silver-ion and copper-infused synergists into food-contact and healthcare plastics, expanding what were niche categories before 2024. Competitive intensity is accelerating as integrated petrochemical players leverage feedstock control to squeeze independent formulators, prompting a race for acquisitions and patents in non-fluoropolymer processing aids ahead of looming PFAS curbs.

Key Report Takeaways

- By application, packaging led with 42.76% revenue share in 2025, while consumer goods are forecast to advance at a 5.15% CAGR through 2031.

- By form, masterbatch captured 55.78% of the plastics additives market share in 2025; liquid concentrates are projected to grow at a 4.91% CAGR to 2031.

- By type, colorants accounted for 45.87% value in 2025; the dedicated processing aids segment itself is predicted to expand at 4.78% CAGR through 2031.

- By plastic type, polyethylene dominated with 17.87% of the plastics additives market size in 2025, whereas polystyrene is poised to register the quickest 4.66% CAGR during the forecast period.

- By geography, Asia-Pacific commanded 53.12% of global value in 2025 and is expected to grow at a 5.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plastic Additives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight-EV Components Boosting High-Performance Additives | +0.8% | China, the EU, and North America | Medium term (2–4 years) |

| Plastics Replacing Metals Across Uses | +0.9% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Asia-Pacific Urbanisation Expanding Packaging Demand | +0.7% | Core Asia-Pacific, spill-over to Middle East | Short term (≤ 2 years) |

| Mandatory Compostable-Packaging Laws | +0.6% | EU, California, Canada, emerging India | Medium term (2–4 years) |

| Rapid Adoption of Antimicrobial Surfaces | +0.5% | North America, Europe, Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lightweight-EV Components Boosting High-Performance Additives

Battery-electric platforms demand polymer parts that tolerate temperatures above 150 °C without adding weight. Polyamide and polycarbonate housings for power electronics now require heat stabilizers and impact modifiers that preserve tensile and flammability performance at elevated service temperatures. Lubricant formulators are introducing fluorinated and silicone chemistries that cut injection-molding cycle times by 8%–12% while improving surface finish. Tesla’s 2025 supplier code mandates UL 94 V-0 compliance using halogen-free solutions, inflating specialty-package selling prices by up to 35%. Producers with integrated research and development are consequently securing long-term supply contracts, shielding margins from raw-material swings. As automakers publish stricter sustainability scorecards, additive suppliers that can certify low-VOC and recyclability credentials are positioned to capture a disproportionate share of incremental volume in the plastics additives market.

Plastics Replacing Metals Across Consumer and Industrial Uses

Corrosion resistance, lightweighting, and shape versatility are accelerating the substitution of metals with reinforced plastics in pump housings, valve bodies, and appliance components. Appliance OEMs that swapped zinc die-casts for impact-modified ABS achieved 40% cost savings and reduced component and part count through mold-in design freedom. The European Union’s Ecodesign Regulation, effective 2025, assigns higher circularity scores to mono-material goods, catalyzing single-polymer assemblies that rely on advanced additive packages for mechanical strength[1]European Commission, “Ecodesign for Sustainable Products Regulation,” ec.europa.eu. As design engineers pursue ever-thinner wall sections, nucleating agents and long-term heat stabilizers gain favor, elevating formulation complexity. This dynamic widens the capability gap between global formulators and regionally focused blenders, reinforcing consolidation trends inside the plastics additives market.

Asia-Pacific Urbanisation Expanding Packaging Demand

Rapid urban migration across India, China, and Southeast Asia is lifting packaged-goods consumption—and with it, demand for barrier, slip, and antiblock packages inside multilayer films[2]World Bank, “Urban Population Data,” worldbank.org . India added 35 million urban residents between 2023 and 2025, spurring flexible-film volume that incorporates EVA masterbatch to maintain low-temperature impact strength. China’s cold-chain warehouse footprint rose 18% in 2025, requiring polyethylene films infused with antifog and moisture-barrier additives to preserve visual clarity at sub-zero storage. Southeast Asian converters are co-developing oxygen-scavenger blends that triple shelf life for shelf-stable meals, highlighting the market’s shift toward collaborative product-development agreements. These trends firmly support continued 5%-plus regional growth in the plastics additives market through 2031.

Mandatory Compostable-Packaging Laws Lifting Bio-Additive Masterbatch

The EU Packaging and Packaging Waste Regulation finalized in 2024 mandates that all single-use food-service articles be compostable by 2027, accelerating demand for PLA and PHA masterbatch fortified with bio-derived plasticizers and nucleators. California’s SB 1046 bans petroleum-based additives in compostable articles from 2026 onward, forcing reformulators to adopt plant-wax matrices that retain melt flow without compromising biodegradability. India’s updated EPR credits incentivize brands adopting bio-masterbatch, unlocking subsidized credits that lower payback periods for new production lines. Announced global capacity additions of 45,000 t/y underline the momentum. Price differentials remain 25% above conventional masterbatch, yet brands accept the premium to pre-empt future landfill fees, underscoring a growing profit pool within the plastics additives market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tin and Phosphorus Feedstock Volatility Compressing Margins | -0.4% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Phthalate Plasticiser Phase-Out in United States and Europe | -0.5% | North America, Europe | Medium term (2–4 years) |

| PFAS-Based Processing-Aid Restrictions Curbing Adoption | -0.3% | Europe, North America, pending Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Tin and Phosphorus Feedstock Volatility Compressing Margins

Indonesia cut its tin export quota by 15% in 2025, driving LME spot prices from USD 25,000/ton to USD 30,500/ton by year-end. Concurrently, Myanmar’s political turbulence disrupted phosphorus pentoxide shipments, forcing European stabilizer makers to source from Morocco at 22% premiums. Organotin stabilizers remain indispensable for rigid PVC pipe, yet calcium-zinc alternatives need 30% higher dosages, undermining converter economics. Margin squeeze is most acute for mid-tier formulators lacking long-term contracts, compelling exit or diversification. The plastics additives market, therefore, confronts short-run cost volatility that discourages capital deployment in tin-intensive product lines.

Phthalate Plasticiser Phase-Out in United States and Europe Shrinking Addressable Volume

The U.S. EPA restricted DEHP, DBP, and BBP in December 2024, requiring phase-out by January 2027 across consumer goods. ECHA added four more phthalates to REACH Annex XIV in 2025, effectively banning their use without authorization in medical devices and food-contact articles. Replacement adipate and citrate esters require 10%–15% higher loadings and offer weaker low-temperature flexibility, raising costs while trimming elasticity of demand. Global phthalate consumption is set to fall by 180,000 tons annually, suppressing overall growth potential in the plastics additives market until performance-neutral substitutes emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Processing Aids Lead Innovation Race

Processing aids captured the fastest 4.78% CAGR outlook between 2026 and 2031 as converters prioritize melt-flow improvements that do not migrate to part surfaces. Fluoropolymer-based aids, historically entrenched in PVC, now grapple with PFAS scrutiny that has accelerated the rise of acrylic and silicone replacements delivering 90% comparable performance. The plastics additives market size for lubricants, slip, and antistatic agents, collectively grouped under “other types,” reached the largest value pool in 2025 due to their ubiquity in polyethylene film and molded packaging. As extrusion lines target 5%–8% shorter cycles, flow improvers specifically enable thinner polypropylene panels for vehicle interiors, a direct contribution to OEM lightweight targets.

In 2025, colorants held a 45.87% share of the plastic additives market, driven by demand for aesthetic differentiation, branding, and functional coloration in packaging, construction, and mobility. The adoption of recycled polymer-compatible masterbatches and innovations in heat-stable, UV-resistant, and food-contact-compliant pigments are boosting usage. Advanced colorants for high recycled-content films and molded parts further expand their applications, cementing their key role in the market.

By Plastic Type: Polyethylene Dominates, Polystyrene Accelerates

Polyethylene commanded 17.87% of the global plastics additives market share in 2025 thanks to expansive use in films, agricultural wraps, and blow-molded containers that rely on slip and UV systems for shelf integrity. Demand for polyethylene continues to build as recycled content targets advance, necessitating additive packages that re-establish melt viscosity and IR barrier performance. Polystyrene, particularly in its expanded form, is expected to post a 4.66% CAGR through 2031 after flame-retardant innovations enabled code-compliant absence of halogens in building insulation.

Polypropylene benefits from electric-vehicle interior applications where talc-filled grades need coupling agents to maintain ductility below –20 °C, underpinning mid-single-digit growth in plastics additives market size across Asia-Pacific. Polyvinyl chloride’s ongoing dependence on heat stabilizers faces headwinds from phthalate withdrawals, yet rigid-pipe demand in infrastructure projects supports baseline volume. Polyethylene terephthalate, transitioning toward high-PCR blends, uses chain extenders and acetaldehyde scavengers to restore mechanical properties. Polycarbonate and polyamide serve high-value niches in under-hood components and industrial machinery, where premium additive packages enable 150 °C dimensional stability and UL 94 V-0 compliance, locking in superior margin opportunities for suppliers in the plastics additives market.

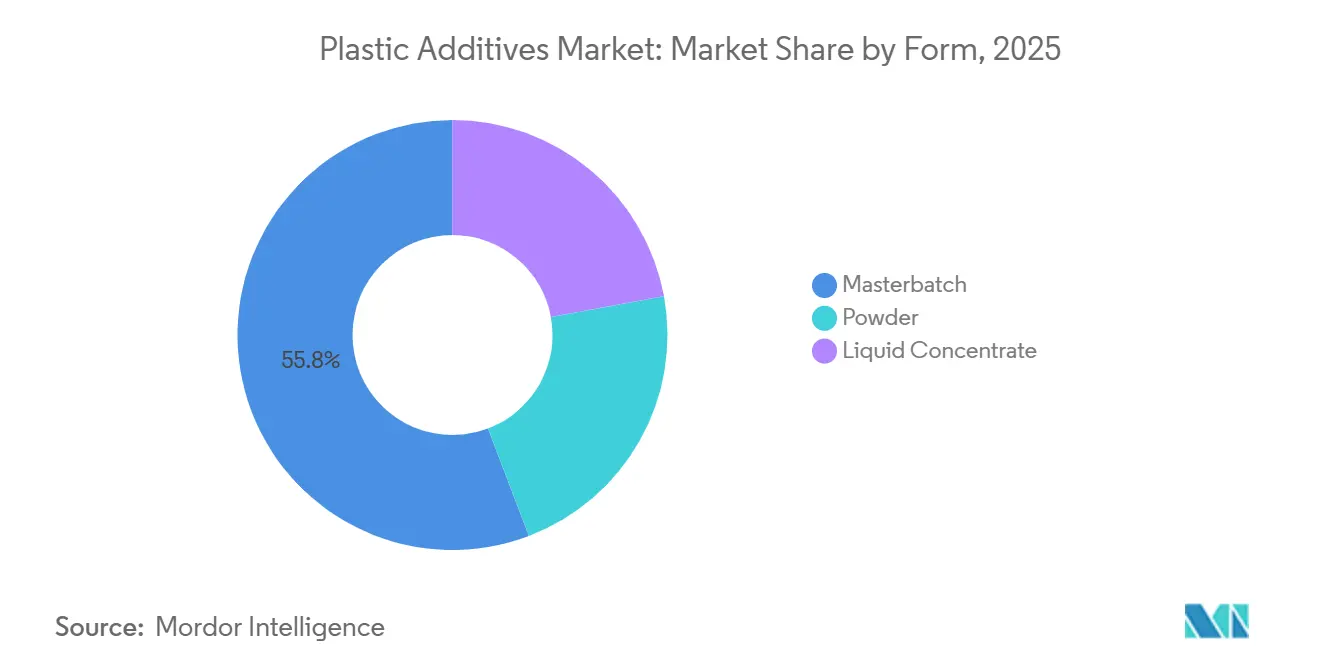

By Form: Masterbatch Holds Share, Liquids Gain Efficiency Edge

Masterbatch remained the preferred form at 55.78% in 2025, favored for handling convenience, accurate dosing, and global compounding infrastructure compatibility. However, liquid concentrates are predicted to grow 4.91% annually as processors install gravimetric feeders capable of metering fluids directly into extruder throats, eliminating an entire pre-compounding step and lowering holding costs by up to 18%. Liquid systems also minimize REACH reporting burdens by consolidating substance tracking into single-component solutions.

In response, masterbatch providers are commercializing ultra-high-concentration pellets with carrier-resin content reduced to 20%, compressing the cost gap with liquids. Powder additives, though smallest in volume, still dominate dry-blend PVC and thermoset workflows, where liquid carriers interfere with cure kinetics. The plastics additives market is therefore bifurcating: large processors favor efficient liquid systems, while small-to-mid converters continue to prefer ready-to-use masterbatch granules.

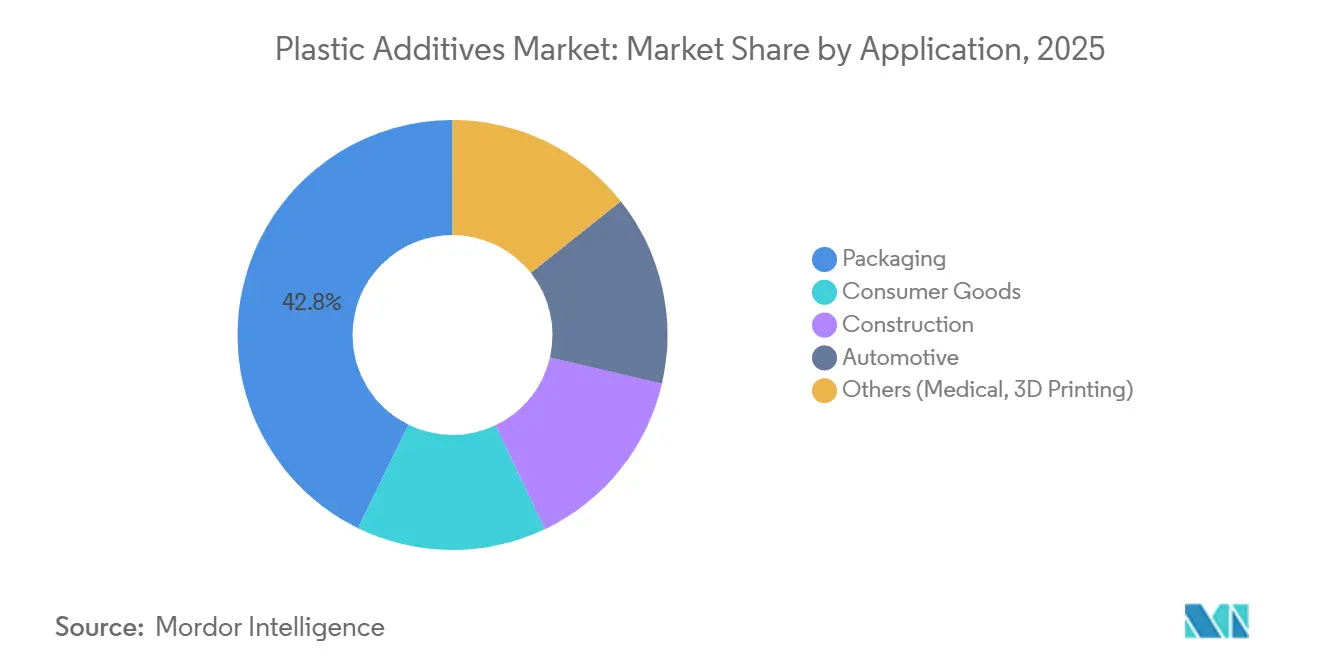

By Application: Consumer Goods Outpaces Packaging

Although packaging retained 42.76% revenue in 2025, consumer goods are forecast to exhibit the quickest 5.15% CAGR, propelled by antimicrobial, color, and tactile-enhancing additives injected into personal-care and houseware components. Automotive demand is pivoting from interior trim toward structural battery plastics that call for flame-retardant and impact-modifier packages. Construction remains reliant on rigid PVC profiles fortified by heat-stabilizer and impact-modifier systems that assure multi-decade weatherability.

Medical devices and additive-manufacturing uses, grouped under “others,” provide double-digit growth albeit from a small base, thanks to ISO 10993-certified stabilizers and flame-retardant powders formulated for layer-by-layer printing. This broadening of end-use diversity reduces cyclicality and safeguards revenue streams across the plastics additives market, particularly as housing starts and packaging volumes fluctuate with macroeconomic cycles.

Geography Analysis

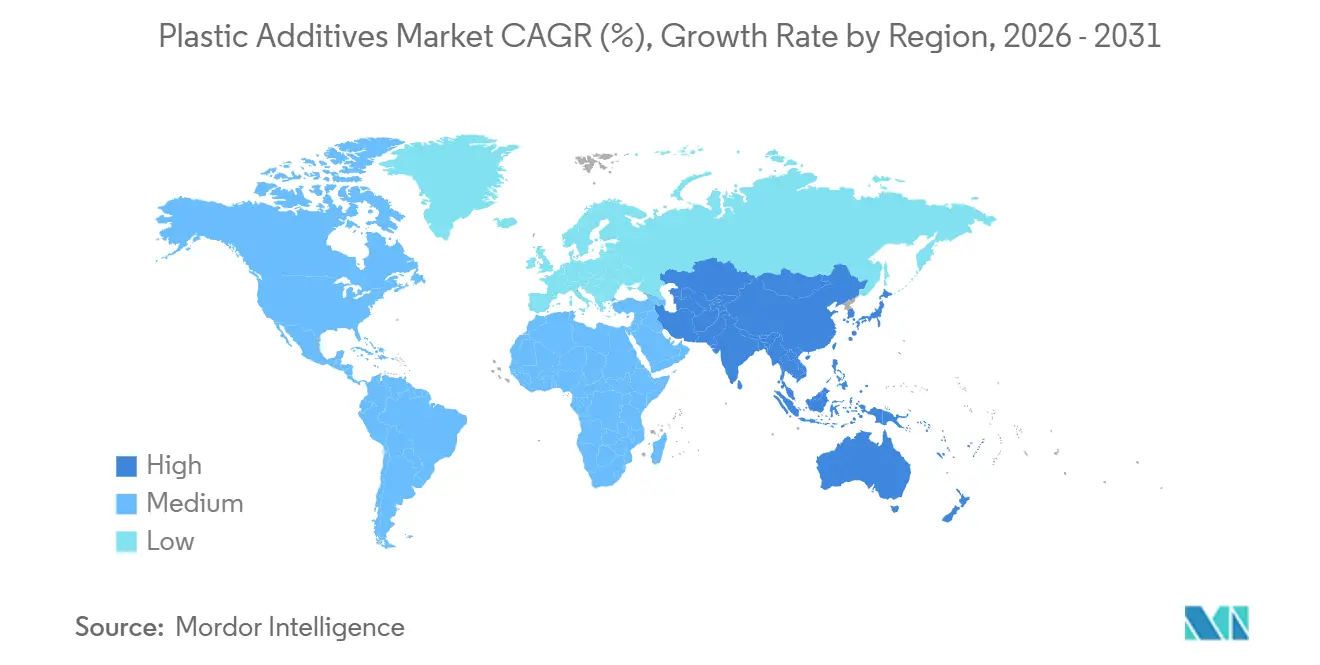

Asia-Pacific held 53.12% of the plastics additives market share in 2025 and is projected to expand at a 5.27% CAGR through 2031. China’s dual-circulation agenda steers compounders toward local additive suppliers, supporting rapid capacity additions in Shandong and Zhejiang provinces that logged 12% new polypropylene throughput in 2025. India’s Production-Linked Incentive disbursed USD 1.2 billion to advanced-chemistry investors, catalyzing projects that will add 85,000 ton/year of additive output by 2028. Japan sustains specialty demand for engineering resin additives despite flat volume, while South Korea’s electronics majors specify halogen-free flame systems, lifting local consumption growth to the mid-single digits.

North America benefits from reshoring and the Inflation Reduction Act, which underwrites domestic specialty-chemical lines in Texas and Louisiana, slated to total 40,000 tons/year by 2026. Canada aligns its phthalate bans with U.S. policy, accelerating citrate adoption, whereas Mexico’s vehicle exports stimulate polypropylene modifier use in bumper fascia and dashboards. Europe’s circular-economy laws prioritize mono-material designs, pushing demand for high-function additive packages that replace metal-plastic hybrids. Germany, France, and Italy lead bio-masterbatch penetration for compostable packaging, while Scandinavia mandates halogen-free flame retardants in construction panels, securing premium opportunities for specialized formulators.

South America’s growth is led by Brazil, where a 4.5 million-hectare expansion in planted area during 2025 increased agricultural-film demand that employs UV and light-diffusion systems. Argentina’s auto-parts exports propel incremental polypropylene and polyamide additive uptake, although currency volatility tempers capital spending. The Middle East invests downstream via Saudi Arabia’s local compounding push, opening a nascent plastics additives market centered on processing aids for newly commissioned PE and PP lines. South Africa’s retailers specify antimicrobial packages for extended shelf life, marking early adoption in a region still constrained by cold-chain limitations.

Value Chain Analysis

The plastic additives value chain begins with feedstocks and intermediates (petrochemical and bio-based) used to produce stabilizers, plasticizers, pigments, processing aids, and other functional packages. Integrated chemical producers and specialty formulators manufacture these products and deliver them as powders, liquids, and masterbatches to compounders and converters, which dose them into PE, PP, PVC, PET, PS, and engineering resins for packaging, automotive, construction, and other end uses. In 2026, supply-chain risk management remains a visible operating requirement, as regionalization pushes buyers to qualify multi-region sources and carry higher inventories amid longer lead times for chemical intermediates and energy-cost volatility.

Distribution typically covers both direct sales to large processors and regional distribution for small and mid-sized converters. Technical service and compliance documentation increasingly move into the sales process. Regulatory-driven substitution is also influencing procurement and qualification workflows, with PFAS scrutiny and phthalate restrictions accelerating development and adoption of acrylic, silicone, and bio-based alternatives, which raises testing burden for food-contact and recycled-content applications. Named approvals show how product qualification and regulatory clearance can act as gating steps for time-to-market and supplier selection across the chain, including Clariant securing EU Commission approval in February 2026 for renewable rice bran wax additives for food-contact plastics.

Competitive Landscape

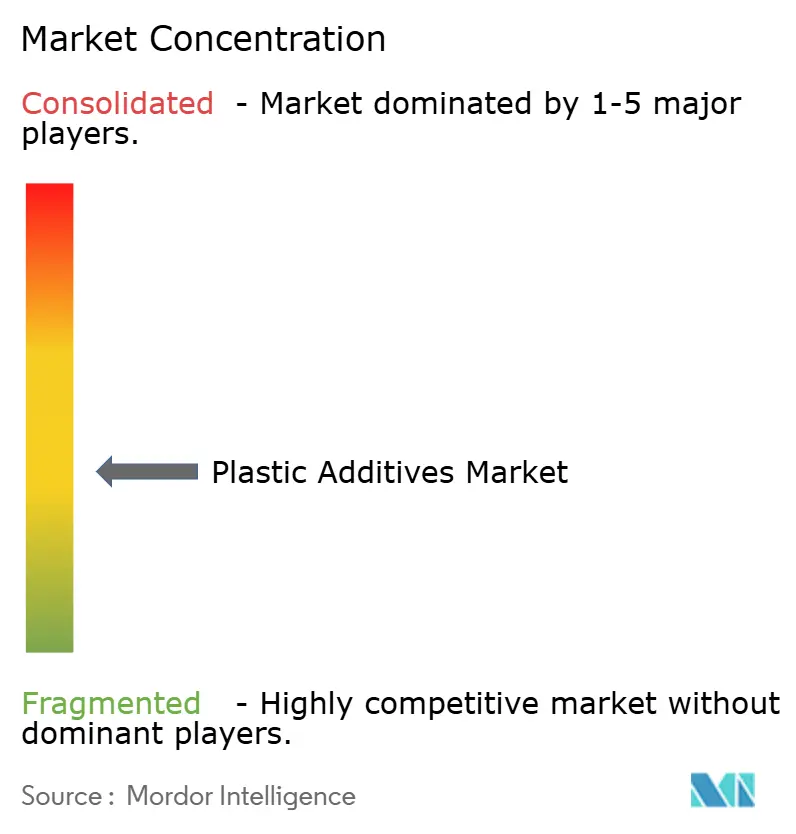

The plastics additives market is moderately fragmented, with a meaningful share for regional players. Integrated petrochemical majors such as BASF, Dow, and Evonik leverage feedstock control to underwrite cost leadership in commodity stabilizers and plasticizers, while specialty houses like Clariant and Avient differentiate through rapid formulation services tailored to local converters. Patent filings for non-fluoropolymer processing aids surged 40% during 2024-2025, signaling a scramble to replace PFAS ahead of regulatory cutoffs. Technology investments focus on high-throughput pilot extruders and AI-driven formulation engines that cut lab cycles by one-third, boosting speed-to-market for customer-specific blends. Small-to-mid players lacking capital for compliance testing and global technical service are consolidating or exiting, evidenced by three European mid-size formulators being absorbed in 2025. White-space remains in bio-based plasticizers, antimicrobial masterbatches, and polycarbonate-compatible flame retardants where regulatory pull meets limited industrial-scale capacity. Companies able to scale fermentation or bio-refining processes will likely capture a disproportionate share as sustainability metrics tighten across end markets, reinforcing the strategic imperative for capacity realignment inside the plastics additives market.

Plastic Additives Industry Leaders

BASF

Evonik Industries AG

Clariant

Dow

Songwon Industrial Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunities concentrate in additive systems that enable higher recycled and circular polymer use while meeting tightening chemical and product-compliance requirements. Europe offers a specific pull, with the European Commission implementing REACH Annex XVII restrictions in May 2026 covering key phthalates (DEHP, DBP, BBP) and a PFAS-based surfactant. That framework is pushing reformulation activity toward phthalate-free plasticizers and non-fluorinated processing aids, and the June 2026 introduction of Regulation (EU) 2026/1168 to clarify derogations for synthetic polymer microparticles under REACH (effective 2028) increases the value of additives that can deliver performance without creating microplastics compliance complications.

A second focus is sustainability-credentialed and renewable-input additives that help brand owners and converters document reduced footprint without sacrificing throughput. Company actions in 2026 highlight commercialization momentum, including Songwon Industrial announcing commercial availability of an RSPO-certified SONGNOX 1076 antioxidant in July 2026 and BASF expanding standard HALS and NOR HALS capacity in April 2026 for plasticulture and other UV-demanding end uses. Demand-side programs around compostable and food-contact applications also support bio-based processing aids and lubricants, alongside Clariant's renewable rice bran wax additive approvals in 2026. Meanwhile, investments in circular feedstock upgrading, such as Evonik's impurity-removal approach for pyrolysis oil, create a route for additive suppliers to target recycling value chains rather than only virgin polymer conversion.

Recent Industry Developments

- June 2026: Evonik launched the Purocel product line aimed at facilitating chemical recycling by removing impurities such as chlorine from plastic-waste-derived pyrolysis oil. Improving pyrolysis oil quality supports steam cracker integration, expanding the addressable market for additive and catalyst solutions tied to circular feedstock use.

- June 2025: Clariant launched PFAS-free polymer processing aids for more sustainable polyolefin extrusion. The move directly targets substitution demand created by PFAS scrutiny, and it strengthens supplier positioning with converters seeking comparable processing performance without fluoropolymer-based aids.

- May 2024: Clariant introduced new solutions at NPE 2024 aimed at reducing the environmental impact of plastics, including offerings linked to circularity and improved processing efficiency. These launches align additive portfolios with brand and converter requirements around recyclability and lower-impact formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The plastic additive market is defined as revenues from additives sold for blending into plastics to improve processing, durability, and performance. This includes formats such as liquids, powders, and masterbatches, and it covers major polymer families and end uses.

Scope exclusions: Base resin sales are excluded, and pure pigment-only color concentrates are excluded when they are sold as pigments rather than functional additives.

Segmentation Overview

- By Type

- Lubricants

- Processing Aids (Fluro-polymer-based)

- Flow Improvers

- Slip Additives

- Antistatic Additives

- Pigment Wetting Agents

- Colorants

- Antifog Additives

- Plasticizers

- Other Types (Filler Dispersants, Blowing Agent, Anti-blocking Agents, Coupling agents, etc.)

- By Plastic Type

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Polyethylene Terephthalate (PET)

- Polycarbonate (PC)

- Polyamides (PA)

- Other Plastic Types

- By Form

- Masterbatch

- Powder

- Liquid Concentrate

- By Application

- Packaging

- Consumer Goods

- Construction

- Automotive

- Others (Medical, 3D Printing)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by locking down the demand and supply signals that can be checked in public data before any model is finalized. We relied on OECD and national statistics offices for industrial production and chemicals indices, UN Comtrade for trade flows of relevant chemicals, and World Bank and IMF series for macro and currency context.

To keep inputs connected to real polymer activity, we also reviewed open publications from plastics and chemicals associations, regulatory documents from agencies such as the US EPA and the European Commission for phase-outs and compliance timing, and peer-reviewed polymer science and processing papers that describe typical additive loading ranges. Company annual reports, investor presentations, and press releases were used to interpret product mix changes and pricing tone, while a paid subscription for company financials and a patent database helped validate innovation intensity and supplier positioning. These sources are not exhaustive, and we reviewed additional public documents to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test desk assumptions on additive loading, pricing movement, and where substitutions were actually showing up in customer specifications. We spoke with participants across the value chain, including additive suppliers, compounders, converters, and procurement or technical roles at major end-use manufacturers. We also ensured coverage across APAC, EMEA, and the Americas, so regional polymer mix and regulation differences were not missed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 20% | APAC: 47% |

| Mid tier: 55% | Functional/Unit leaders: 30% | EMEA: 30% |

| Smaller Players: 20% | Managers: 50% | Americas: 23% |

Market-Sizing & Forecasting

Market sizing was built using top-down and bottom-up logic. The top-down path is anchored on polymer production and trade indicators that reconstruct the addressable consumption pool by resin family and region. Those demand pools are then translated into additive value using realistic loading factors and average selling price bands adjusted for form factor, performance grade, and regional mix.

Key inputs in the plastic additive model included polypropylene and PVC output trends, packaging film and rigid packaging demand signals, construction activity tied to pipes and profiles, shifts in automotive lightweighting and EV content, and regulatory timelines that influence stabilizer and flame-retardant choices. Because pricing can move differently than volume in specialty chemistries, we modeled price progression with scenario analysis and cross-checked direction with what interviewees said about contract resets and premium shifts.

Selective bottom-up approximations were used to corroborate totals. For example, we rolled up sampled supplier revenues where disclosures were available and validated implied volumes using typical additive treat rates. Where country or additive type disclosures were limited, we handled gaps using proxy resin demand, trade substitution checks, and regional average pricing, then reviewed the outputs against expert feedback before finalizing.

Data Validation & Update Cycle

Validation was done through several checks so the model does not drift away from real market signals. We compared outputs against independent indicators such as polymer output trends, trade movements for key additive chemistries, and observed pricing direction. Any large variances were investigated before sign-off.

Anomalies were flagged when growth rates broke away from end-use demand patterns, or when implied additive intensity looked inconsistent with known processing norms. In those cases, assumptions were revisited, and when needed, experts were re-contacted to confirm whether the change was structural or temporary. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the latest updated view.

Mordor Intelligence's Plastic Additive Market Size Compared Against Other Published Estimates

Published market values for plastic additives can differ by a wide margin, and it usually comes down to what is counted, how pricing is treated, and which year is used as the anchor. Even when the topic sounds similar, the definition of additives versus adjacent chemical revenues can change the total quickly.

The main gap comes from scope choices, especially whether base resin value or pigment-only color concentrates get blended into the number, and how ex-factory pricing is converted across regions and years. Some estimates also lean more heavily on broad chemical market ratios without checking resin-specific loading factors, while others apply aggressive price escalation assumptions that can inflate value even when polymer volumes are steady. Because the model here ties additive demand to polymer output, resin mix, and realistic loading, the spread narrows to explainable drivers, which is consistent with the approach used by Mordor Intelligence in this market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.05 B (2025) | |

| Global Consultancy A | USD 51.40 B (2024) | Uses a larger stated total that appears to reflect a broader additive scope and a different base year, and the value can also be lifted by applying generalized pricing growth across regions without resin-specific loading checks. |

| Industry Publisher B | USD 58.90 B (2023) | The estimate is anchored to an earlier base year and is presented at a higher level across product and end-use baskets, which can embed adjacent chemical revenues and blended price assumptions that are not always traceable to polymer demand indicators. |

Taken together, the table shows that year selection and what gets included as an additive drive most of the difference, and pricing treatment tends to amplify it. By keeping the scope tied to additive revenues and checking the implied demand against polymer activity and realistic treat rates, we can explain the final value through steps that can be repeated and reviewed.

Key Questions Answered in the Report

What is the global value of the plastics additives market?

The global plastics additives market is estimated at USD 30.41 billion in 2026 and is forecast to rise to USD 38.28 billion by 2031.

Which region drives most demand for plastics additives?

Asia-Pacific led with 53.12% value share in 2025 and is projected to grow at a 5.27% CAGR through 2031.

Why are liquid concentrates gaining popularity over masterbatch?

Automated gravimetric feeders allow direct dosing, cutting inventory costs by up to 18% and supporting a projected 4.91% CAGR for liquids.

How will PFAS regulation affect additives suppliers?

Planned restrictions in Europe and North America force the development of acrylic and silicone alternatives, subtracting 0.3 percentage points from the overall CAGR.

Which additive type is growing fastest?

Processing aids, helped by EV lightweighting and thin-wall packaging, are set to expand at 4.78% per year through 2031.

What opportunities exist in bio-based additives?

Compostable-packaging laws in the EU, California, and India are triggering investments that will add 45,000 ton/year of bio-masterbatch capacity by 2027.

Page last updated on: