Extruded Polystyrene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

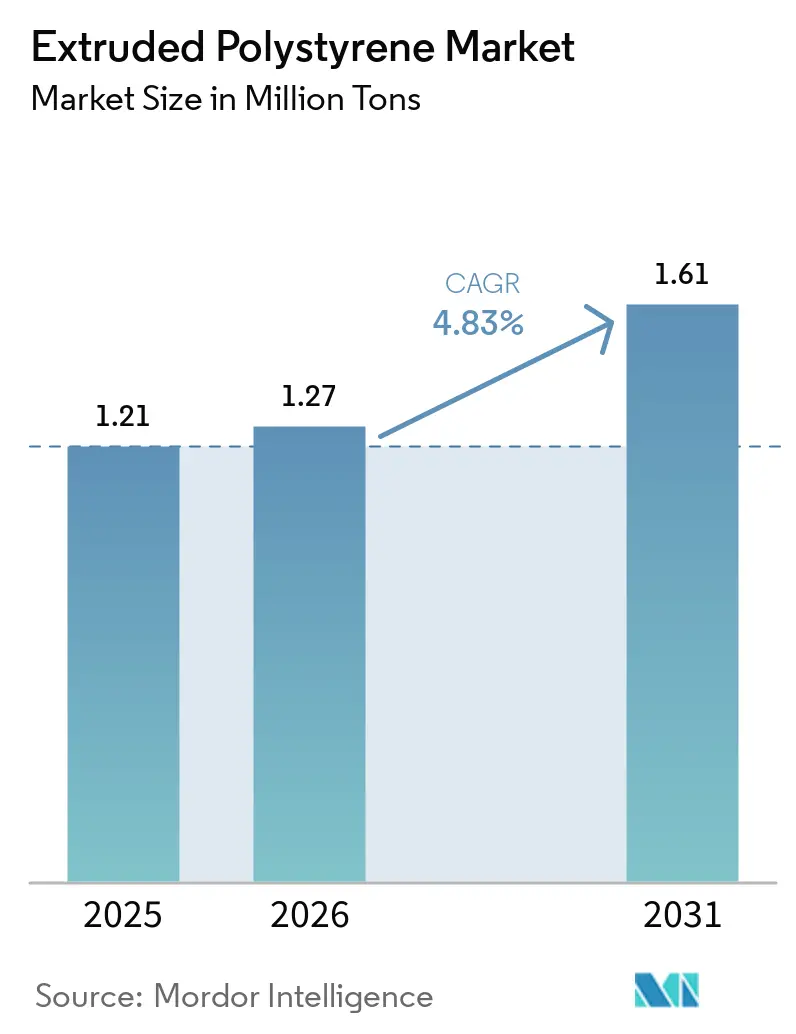

| Market Volume (2026) | 1.27 Million tons |

| Market Volume (2031) | 1.61 Million tons |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extruded Polystyrene Market Analysis by Mordor Intelligence

The Extruded Polystyrene Market size is projected to expand from 1.21 Million tons in 2025 and 1.27 Million tons in 2026 to 1.61 Million tons by 2031, registering a CAGR of 4.83% between 2026 to 2031. Rapidly tightening building‐energy regulations, a steep rise in carbon prices, and a synchronized boom in cold-chain warehousing are moving demand beyond the underlying pace of construction activity. Renovation mandates in the European Union, North America, and parts of Asia now treat thermal insulation as a statutory requirement rather than a discretionary upgrade, compressing the payback period for extruded polystyrene (XPS) retrofits to under three years in colder climates. At the same time, carbon pricing averaged EUR 64.74 per t CO₂ in 2024, lifting whole-life cost savings for owners and pushing energy-performance investments to the top of capital-allocation lists. Finally, large-scale expansions by global cold-storage operators are opening premium niches for high-compressive-strength extruded polystyrene (XPS) pipe sections able to withstand –30°C operating conditions.

Key Report Takeaways

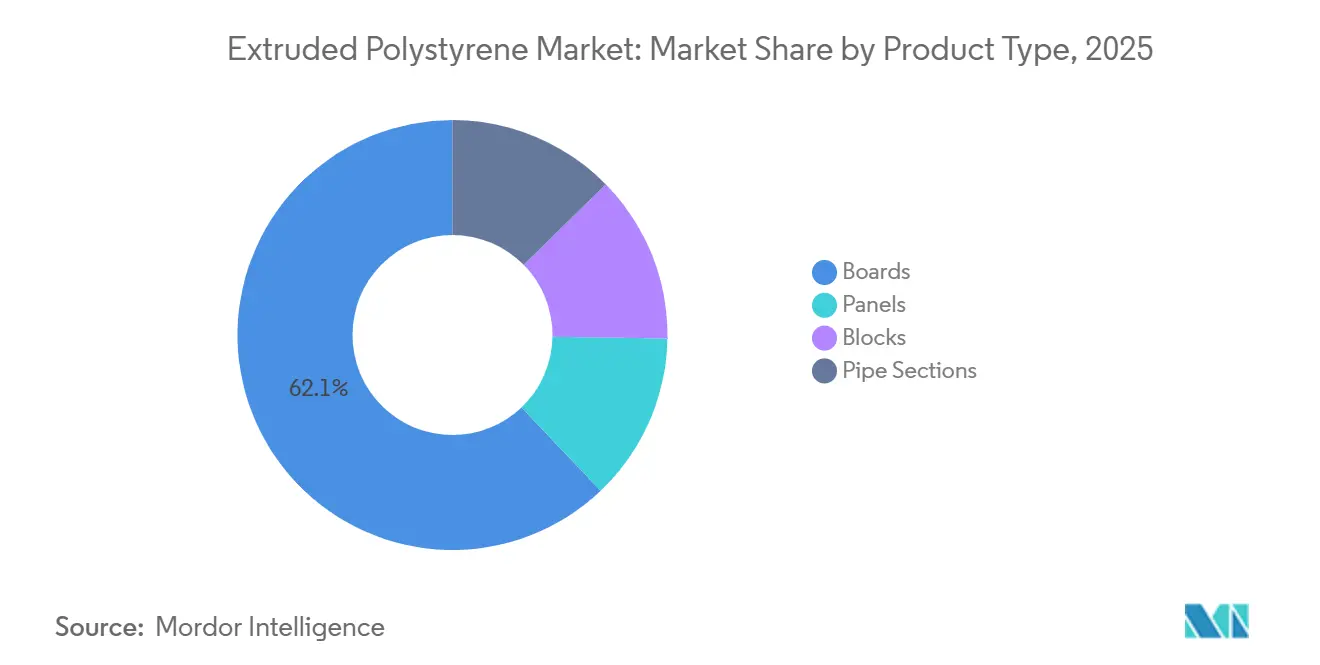

- By product type, boards captured 62.11% of the Extruded Polystyrene market share in 2025, and panels are projected to expand at a 4.89% CAGR during the forecast period (2026-2031).

- By application, roof insulation accounted for 41.12% of the Extruded Polystyrene market size in 2025, while wall insulation is forecast to post the fastest 4.99% CAGR during the forecast period (2026-2031).

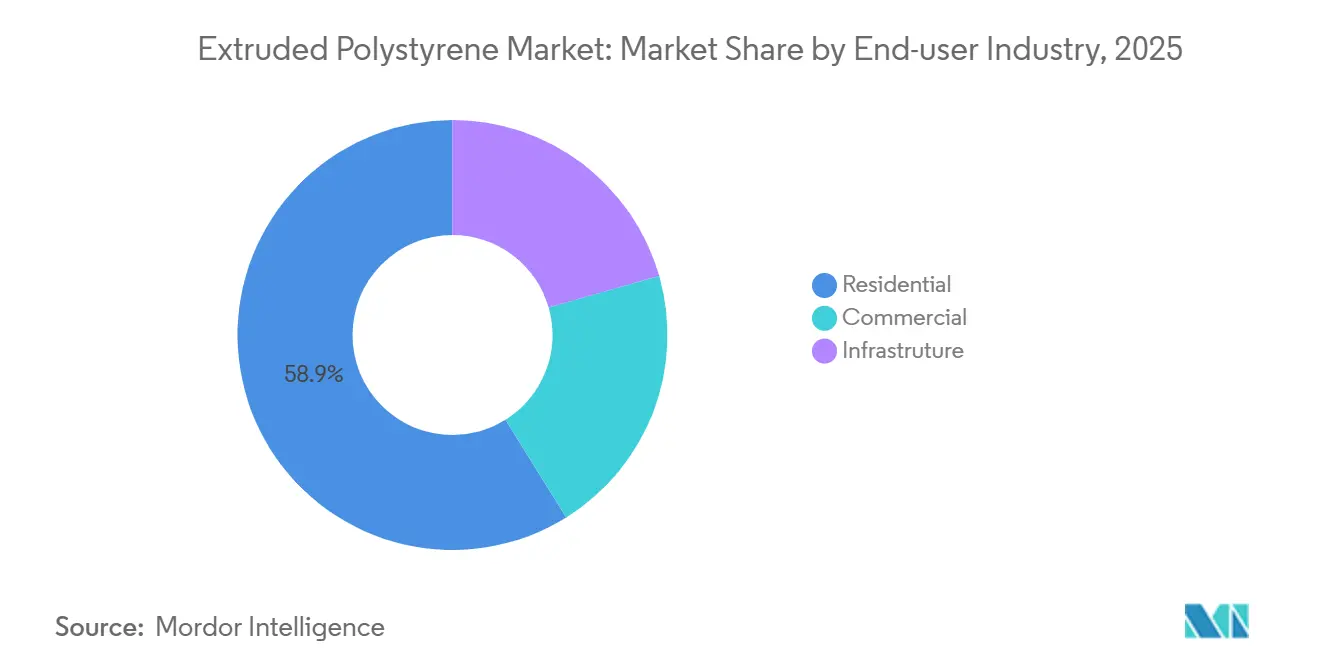

- By end-user industry, the residential segment held 58.87% of market volume in 2025 and is anticipated to advance at a 5.09% CAGR during the forecast period (2026-2031).

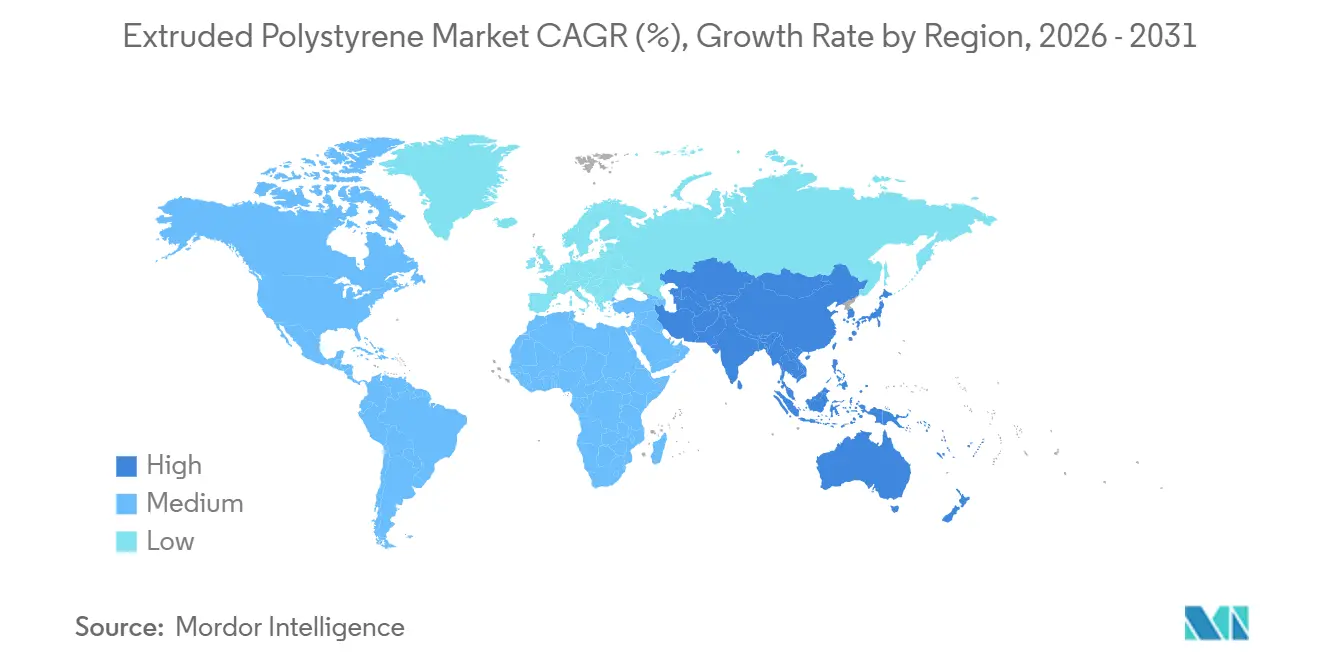

- By geography, Asia-Pacific dominated with 45.23% volume share in 2025 and is set to grow at a 4.98% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Extruded Polystyrene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and infrastructure expansion | +1.2% | APAC core (China, India), spill-over to Middle East | Medium term (2-4 years) |

| Stringent building codes mandating thermal insulation | +1.5% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Cold-chain warehousing boom for biologics and e-grocery | +0.8% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Carbon-pricing mechanisms boosting insulation payback | +0.9% | Europe (EU ETS), California, emerging in Canada | Medium term (2-4 years) |

| AI-enabled extrusion control raising throughput and cost-efficiency | +0.5% | Global, early adoption in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Infrastructure Expansion

Asia-Pacific’s urban population topped 55% in 2025, with China adding about 15 million new urban residents each year and India budgeting USD 1.4 trillion for smart-city infrastructure[1]Ministry of Housing and Urban Affairs, “Smart Cities Mission Progress 2025,” mohua.gov.in. Both countries now require thermal insulation in climate zones registering more than 2,000 heating- or cooling-degree-days, setting a floor under the Extruded Polystyrene market demand. In the Middle East, a USD 1.2 trillion construction pipeline anchored by Saudi Vision 2030 and the United Arab Emirates (UAE) hospitality projects embeds energy-efficiency criteria at the tender stage. Urban residential towers and transport hubs increasingly specify extruded polystyrene (XPS) for below-grade and roof assemblies, where compressive strength above 300 kPa blocks hydrostatic pressure. These specifications translate into recurring pull-through for the Extruded Polystyrene market as cities chase green-building certifications. Local extruders co-located near styrene crackers in China, India, and the Gulf are scaling capacity to shorten lead times and hedge feedstock swings.

Stringent Building Codes Mandating Thermal Insulation

The EU (European Union) Energy Performance of Buildings Directive 2024/1275 forces all new buildings to reach zero-emission status by 2030 and obliges renovations to lift energy ratings by at least two classes. Parallel moves in the United States, such as the 2024 update to Title 24 cool-roof requirements, push commercial roofs toward solar-reflective XPS-polyiso systems. Germany’s amended Gebäudeenergiegesetz set an exterior-wall U-value ceiling of 0.20 W/m²K, effectively locking in 120-150 mm of XPS on masonry walls. These codes raise third-party testing and Environmental Product Declaration costs, weeding out sub-scale importers. As more jurisdictions adopt ISO 29768 and ISO 29465 R-value thresholds, compliance-ready products capture the high-margin tier of the Extruded Polystyrene market.

Cold-Chain Warehousing Boom for Biologics and E-Grocery

Lineage Logistics earmarked USD 8 billion to add 50 million ft³ of temperature-controlled space by 2027, while Americold committed USD 1.5 billion to new sites in the US Southeast and Asia-Pacific. E-grocery penetration could reach 10% of total grocery sales by 2026, driving a wave of regional fulfillment centers that need blast-freezer walls certified to –30°C. The World Health Organization’s PQS standard demands insulation with thermal conductivity below 0.030 W/mK, a threshold XPS meets without the moisture-absorption risk of fibrous alternatives[2]World Health Organization, “PQS Performance Standards for Vaccine Cold Chain,” who.int. These warehouse investments form a premium niche inside the broader Extruded Polystyrene market, with pipe sections and perimeter boards priced 15-20% above commodity XPS. Contractors prefer XPS for its dimensional stability under thermal cycling, lowering maintenance costs over multi-decade asset lives.

Carbon-Pricing Mechanisms Boosting Insulation Payback

EU ETS (European Union Emissions Trading System) permits an averaged of EUR 64.74 per t CO₂ in 2024, cutting the payback on 100 mm of XPS roof insulation in northern Europe to about 2.7 years. California’s cap-and-trade price hit USD 35 per t CO₂, enough to justify continuous insulation for commercial owners facing Title 24 audits. A peer-reviewed 2024 study calculated that 100 mm of XPS can offset 1.2 t CO₂ per year in a mid-latitude home, equating to EUR 77 in avoided carbon fees. Canada’s federal price will climb to CAD 170 (USD 125) by 2030, reinforcing similar economics. As real estate funds adopt Scope 1 and 2 carbon disclosure under new IFRS (International Financial Reporting Standards) Sustainability rules, XPS insulation becomes a risk-mitigation line item rather than a discretionary spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material (styrene) price volatility | -0.6% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Kigali-driven HFC blowing-agent restrictions | -0.4% | Global, phased by income group | Medium term (2-4 years) |

| Extended Producer Responsibility (EPR) recycling burdens | -0.3% | Europe, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material (Styrene) Price Volatility

Styrene spot prices swung from USD 1,150 per ton in January 2024 to USD 1,520 in August before easing to USD 1,280 in December, a 32% intra-year range. Because contractors often lock in insulation prices six to twelve months ahead, sudden feedstock spikes compress operating margins across the Extruded Polystyrene market. Smaller Asian producers without hedging programs curtailed output when styrene topped USD 1,600, highlighting the vulnerability of non-integrated players. Forecast supply additions in China and the Middle East may narrow volatility by late 2026, yet geopolitical risk to naphtha remains. Vertical integration or long-term offtake agreements with styrene suppliers are emerging as a key defensive strategy for established XPS makers.

Kigali-Driven HFC Blowing-Agent Restrictions and EPR Burdens

The Kigali Amendment forced a January 2025 switch to blowing agents with a global-warming potential below 150, pushing manufacturers toward HFO-1234ze and HFO-1336mzz. The United States Environmental Protection Agency (EPA)’s SNAP (Significant New Alternatives Policy) Rule 24 bans HFC-134a in new XPS lines, and the EU’s Packaging and Packaging Waste Regulation 2025/40 adds EUR 15-25 per ton in Extended Producer Responsibility fees. Converting a single extrusion line can cost USD 2–5 million, a hurdle that accelerates consolidation inside the Extruded Polystyrene market. Margin compression of 200–300 basis points is common during the transition and favors players that can spread R&D (Research and Development) and capital costs across multiple plants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Boards Anchor the Base, Panels Accelerate

Boards represented 62.11% of 2025 shipments and underpinned the largest block of Extruded Polystyrene market share, owing to below-grade foundation and low-slope roof assemblies that demand compressive strength above 300 kPa. Panels, however, are forecast to rise at a 4.89% CAGR to 2031, the quickest pace among product types, as modular wall systems trim on-site labor by 30–40%. Blocks and pipe sections command 15–20% price premiums for niche uses such as green roofs and –40°C freezer lines. The new EN 13164:2024 standard tightened dimensional-tolerance tests, giving incumbents with in-house labs a durable compliance moat. Kingspan disclosed that insulated-panel sales grew 12% in 2024, outpacing board demand by four percentage points.

Panel adoption also mirrors a broader shift toward factory-finished façades in Europe and Japan, where seismic codes and labor shortages favor off-site construction. Japanese amendments to its Building Standard Law in 2024 elevated demand for XPS-core panels in retrofits that must keep dead-load additions to a minimum. Meanwhile, Gulf developers value metal-faced panels with XPS cores for high-albedo façades on hospitality projects aiming for LEED (Leadership in Energy and Environmental Design) Gold. As producers refine cell structure to work with HFO blowing agents, panels capitalize on thinner-core, higher-R-value layers that cut shipping weight and improve installer ergonomics across the Extruded Polystyrene market.

By Application: Roof Still Leads, Wall Insulation Gains Momentum

Roof insulation claimed 41.12% of 2025 demand, reflecting re-roof cycles and the United States Department of Energy cool-roof rules that specify minimum R-20 assemblies in most climate zones. Wall insulation is set to advance at a 4.99% CAGR during the forecast period (2026-2031), overtaking other applications as continuous insulation eliminates thermal bridges at steel studs and precast joints. Perimeter, floor, and below-grade uses added 18% of volume, with rising water tables in northern Europe driving XPS uptake for foundation protection. Continuous insulation mandates in Germany and France require 120–150 mm of XPS on masonry walls to meet a 0.20 W/m²K U-value cap. Codes add momentum by harmonizing R-value tables across the United States jurisdictions through the 2024 International Energy Conservation Code, simplifying contractor ordering for Extruded Polystyrene market participants.

The roof segment continues to favor XPS-polyiso composites that pair high compressive strength with solar-reflective surfaces. Data-center operators seek roof assemblies with thermal drift below 5% over 25 years to protect uptime guarantees, translating into premium pricing power. In wall systems, installers appreciate XPS panels that integrate drainage channels to meet new moisture-management clauses in the 2025 International Building Code. Perimeter insulation demand is strongest in Nordic countries, where designers must mitigate frost heave without adding costly geothermal loops, a dynamic that opens additional revenue streams for XPS producers.

By End-User Industry: Residential Leads, Commercial Adds Specialty Upside

Residential construction absorbed 58.87% of 2025 shipments, underpinned by single-family retrofits eligible for a 30% United States federal tax credit through 2032. The segment is set for a 5.09% CAGR during the forecast period (2026-2031) as Germany, France, and the United States enforce penalties for performance gaps between certified and actual energy use. Commercial buildings captured a substantial market volume, with data centers and cold-storage warehouses commanding above-average margins because designs routinely call for 150 mm XPS walls to maintain –30°C environments. Infrastructure applications, road base insulation, rail tunnels, and airport aprons' market share will grow due to climate-resilience budgets in Scandinavia and Japan.

Homeowners in northern Europe increasingly pick XPS for basement retrofits where moisture resistance is critical, extending the Extruded Polystyrene market size attached to do-it-yourself channels. By comparison, the commercial segment relies on pre-qualified supplier lists, letting incumbents leverage multi-year master-service agreements. Infrastructure bids often bundle insulation with drainage layers and geotextiles, nudging XPS makers to partner with civil-engineering firms. Although infrastructure volume is smaller, unit prices can run 25–30% above residential standards, offsetting lower replacement cycles and opening the door to public-private partnerships that lock in a guaranteed offtake.

Geography Analysis

Asia-Pacific carried 45.23% of 2025 shipments, and the region is tracking a 4.98% CAGR to 2031 as China’s green-building coverage hit 95% of new urban construction and India accelerated smart-city spending. Domestic extruders in China enjoy feedstock logistics advantages by locating near coastal styrene crackers, trimming delivery times for local builders. Japan’s updated efficiency rules, which cut allowable wall U-values below 0.87 W/m²K, sustain demand in a declining housing stock, while South Korea’s Carbon Neutrality Act pushes public buildings toward zero-energy status and mandates XPS cores for inverted roofs.

North America's market volume, fueled by the Inflation Reduction Act’s retrofit incentives, a multibillion-dollar cold-storage build-out, and persistent re-roof cycles across aging commercial assets. Extruded Polystyrene market size expansion is amplified by Title 24 updates in California and prescriptive continuous-insulation requirements embedded in the 2024 International Energy Conservation Code. Regional producers are investing in AI-enabled extrusion control to shrink scrap and defend margins against energy-price volatility, thereby stabilizing supply to contractors working on tight timelines.

Europe’s growth rate holds potential despite mature construction bases because the Energy Performance of Buildings Directive forces deep-renovation rates to triple by 2030. EU ETS carbon costs and the Packaging Waste Regulation’s EPR (Extended Producer Responsibility) fees simultaneously challenge margins, yet they also raise barriers for low-compliance imports, effectively protecting local capacity. In South America and the Middle East-Africa, Brazil’s Minha Casa Minha Vida program and Saudi Arabia’s Vision 2030 megaprojects underpin localized spikes, especially for pipe sections in refrigerated agri-export hubs and façade panels on hospitality towers.

Competitive Landscape

The Extruded Polystyrene market is moderately consolidated. Regional specialists, including TECHNONICOL and Synthos, are chipping away at share in Eastern Europe by co-locating extrusion lines near styrene hubs and promising 48-hour lead times. Mergers and acquisitions are likely to accelerate as EPR fees and blowing-agent conversion costs weigh on sub-100,000-ton plants. Private-equity funds are circling niche assets in ultra-low-temperature cold-storage insulation, betting that vaccine logistics and e-commerce grocery will remain secular growth engines.

Extruded Polystyrene Industry Leaders

DuPont

Saint-Gobain

Owens Corning

BASF

Kingspan Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: BEWI unveiled plans to set up a new XPS (extruded polystyrene) insulation facility in Sastamala, Finland, with production slated to commence in the first quarter of 2027.

- January 2025: BASF completed the sale of its Styrodur extruded polystyrene insulation business to Karl Bachl Kunststoffverarbeitung GmbH & Co. KG, to sharpen strategic focus on expandable polystyrene growth.

Global Extruded Polystyrene Market Report Scope

Extruded polystyrene (XPS) is a thermoplastic polymer known for its closed-cell structure, offering greater strength and superior mechanical performance compared to its close alternative, expanded polystyrene (EPS). Although more costly, XPS is commonly used as rigid foam insulation in residential floors, roofs, walls, ceilings, and balconies due to its high compressive strength and excellent moisture resistance.

The extruded polystyrene market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into boards, panels, blocks, and pipe sections. By application, the market is segmented into roof insulation, wall insulation, and others (floor, basement, cavity, and perimeter). By end-user industry, the market is segmented into residential, commercial, and infrastructure. The report also covers the market size and forecasts for Extruded Polystyrene in 15 countries across major regions. For each segment, market sizing and forecasts have been done based on volume (tons).

| Boards |

| Panels |

| Blocks |

| Pipe Sections |

| Roof Insulation |

| Wall Insulation |

| Others (Floor, Basement, Cavity and Perimeter) |

| Residential |

| Commercial |

| Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Boards | |

| Panels | ||

| Blocks | ||

| Pipe Sections | ||

| By Application | Roof Insulation | |

| Wall Insulation | ||

| Others (Floor, Basement, Cavity and Perimeter) | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for Extruded Polystyrene be by 2031?

Volume is forecast to reach 1.61 million tons by 2031, expanding at a 4.83% CAGR from 2026.

Which application is growing fastest within XPS insulation?

Wall insulation is projected to register the quickest 4.99% CAGR as continuous-insulation codes tighten worldwide.

Why are panels gaining share over traditional XPS boards?

Prefabricated panels cut on-site labor by up to 40% and align with modular construction trends, lifting their product-type CAGR to 4.89%.

How do carbon prices influence adoption of XPS insulation?

EU ETS and other schemes raise avoided-carbon savings, shortening retrofit payback to under three years in cold climates, which boosts specification rates.

What impact does the Kigali Amendment have on XPS producers?

It forces a shift to low-GWP blowing agents, requiring USD 2–5 million per extrusion line and raising compliance hurdles for smaller firms.

Page last updated on: