Automotive Plastic Compounding Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

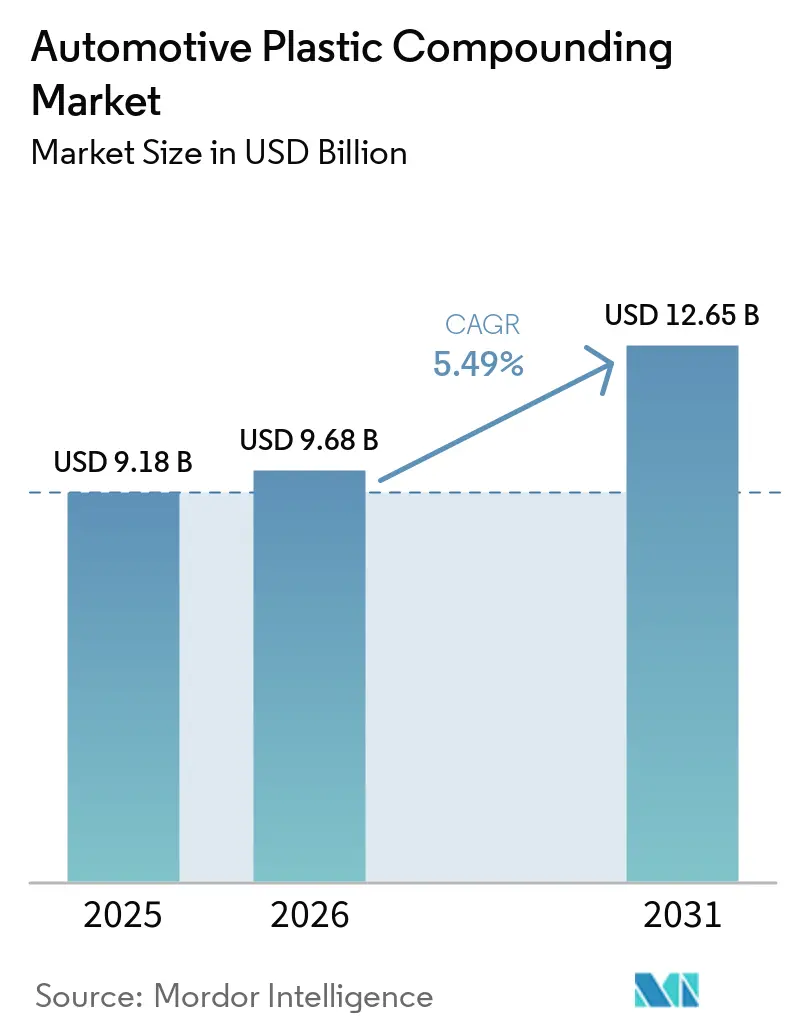

| Market Size (2026) | USD 9.68 Billion |

| Market Size (2031) | USD 12.65 Billion |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Plastic Compounding Market Analysis by Mordor Intelligence

The Automotive Plastic Compounding Market size is projected to be USD 9.18 billion in 2025, USD 9.68 billion in 2026, and reach USD 12.65 billion by 2031, growing at a CAGR of 5.49% from 2026 to 2031. As metal parts increasingly give way to engineered polymers and electrification drives demand for flame-retardant grades, the automotive plastic compounding market is experiencing steady growth. While polypropylene compounds serve as the sector's economic backbone, bio-based and recycled compounds are gaining traction. This shift is largely due to regulations targeting lower carbon emissions and requirements for recycled content, both of which favor environmentally friendly inputs. Glass-fiber reinforcements continue to lead in load-bearing applications, but carbon-fiber and long-fiber variants are carving out a presence in high-end battery-electric platforms. The competitive landscape is evolving: integrated petrochemical giants are intensifying their backward integration efforts, while niche specialist compounders focus on hydrolysis-resistant, laser-weldable, and mono-material solutions. Although margins face near-term pressures from crude-linked resin fluctuations, a strategic pivot towards recycled and bio-based feedstocks hints at a broader move towards circular supply chains.

Key Report Takeaways

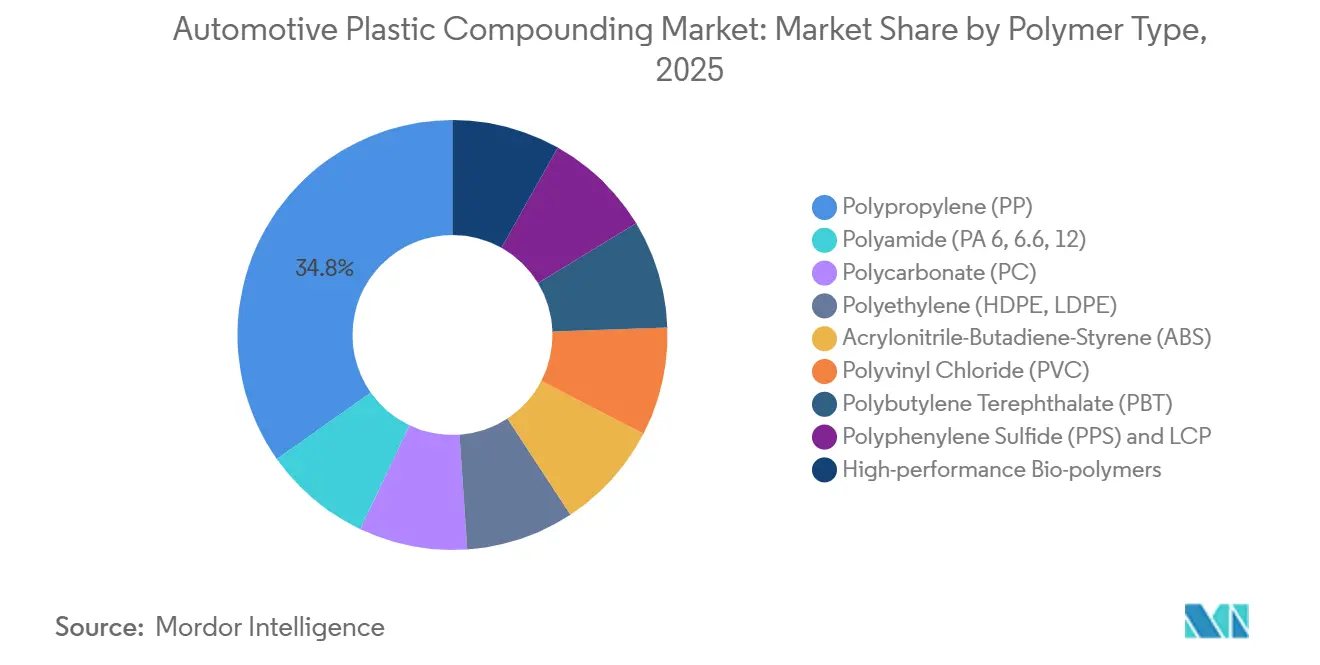

- By polymer type, polypropylene compounds led with 34.87% of the Automotive plastic compounding market share in 2025, whereas bio-polymers are projected to expand at a 6.11% CAGR over 2026-2031.

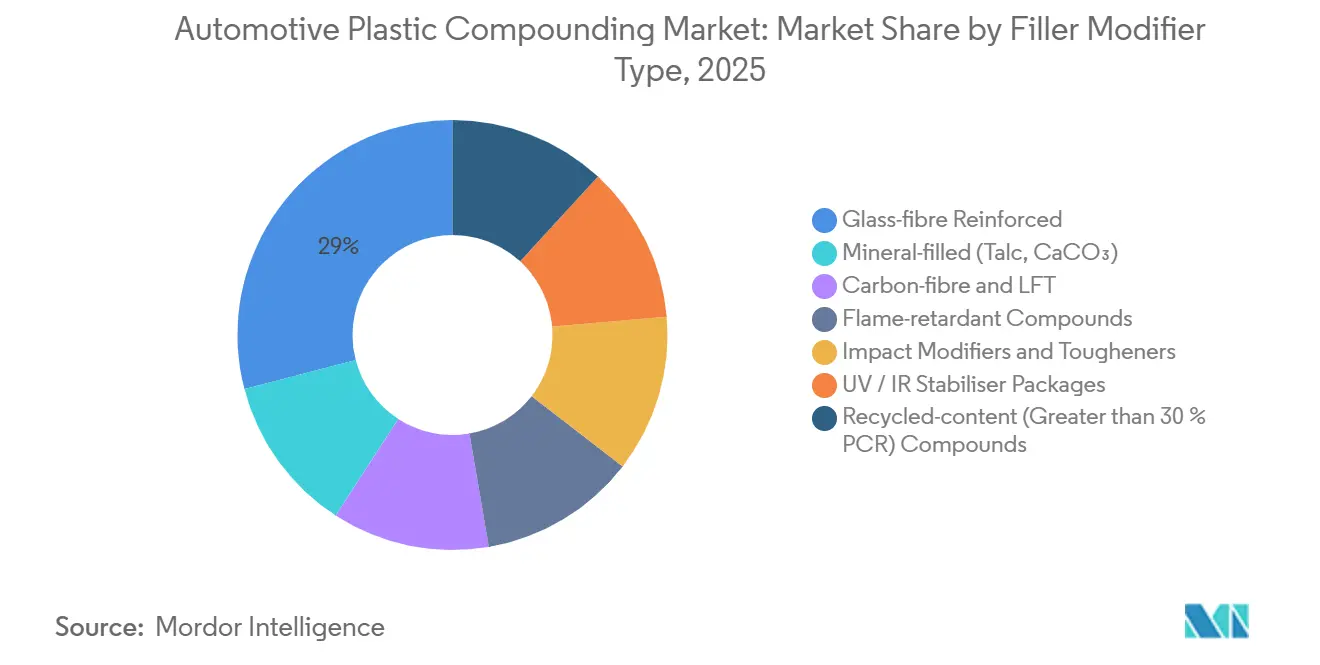

- By filler category, glass-fiber reinforced grades accounted for 29.04% of the Automotive plastic compounding market size in 2025, while the segment itself is advancing at a 5.89% CAGR over 2026-2031.

- By application, interior components captured 32.89% revenue share in 2025, yet battery-enclosure compounds are forecast to post the fastest 6.33% CAGR over 2026-2031.

- By vehicle type, passenger cars held 60.83% of the automotive plastic compounding market share in 2025, whereas battery-electric and hybrid platforms are growing at a 6.29% CAGR over 2026-2031.

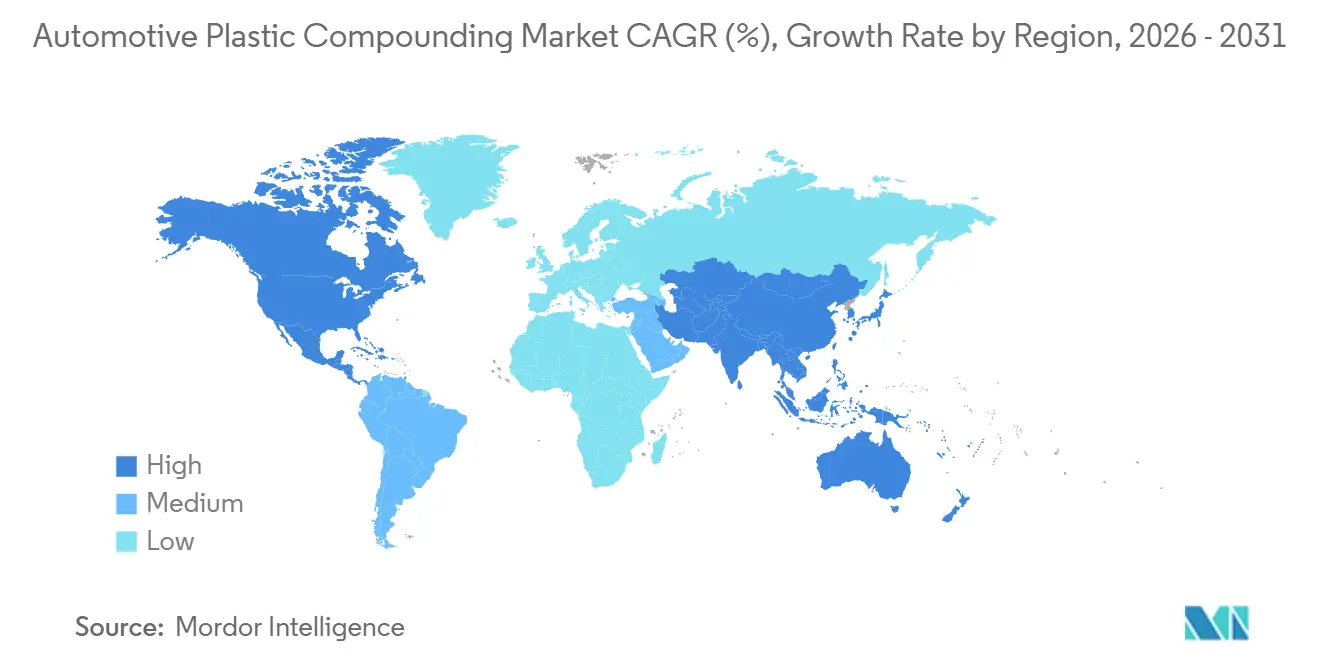

- By geography, Asia-Pacific captured 47.18% of the 2025 value and is leading regional expansion at a 6.45% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Plastic Compounding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM lightweighting mandates | +1.20% | Global, with EU and China leading compliance enforcement | Medium term (2-4 years) |

| Rapid EV rollout needs heat- and flame-resistant compounds | +1.50% | APAC core (China, South Korea), spill-over to North America and EU | Short term (≤ 2 years) |

| Global vehicle production rebound post-2025 | +0.90% | Global, with strongest recovery in ASEAN and India | Short term (≤ 2 years) |

| Laser-weldable polyolefin compounds for modular lighting | +0.60% | North America and EU, early adoption in premium segments | Medium term (2-4 years) |

| Mono-material bumper systems enabling recyclability | +0.80% | EU and Japan, driven by extended producer responsibility frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Lightweighting Mandates

In response to mandates for reduced fleet-average carbon dioxide emissions, automakers are transitioning from traditional stamped steel to advanced materials like glass-fiber polypropylene and polyamide. These new materials significantly reduce weight while maintaining stiffness. Long-glass-fiber polypropylene is already a foundational element in front-end modules for next-generation battery platforms. Additionally, weight savings showcased in concept vehicles hint at the potential for deeper integration of these materials. Such lightweight structures are pivotal in counterbalancing the additional weight of batteries in electric vehicles, directly impacting their range. Suppliers who combine weight reduction with recycled or bio-based content enjoy a significant compliance edge. Consequently, engineered polyolefins are set to dominate the semi-structural parts segment, solidifying their central role in the automotive plastic compounding market in the near future.

Rapid EV Rollout Needs Heat- and Flame-Resistant Compounds

In recent years, production of battery-electric vehicles has experienced a significant surge. Today, every pack, inverter, and charging port is designed with compounds that can withstand high-temperature continuous use, all while meeting stringent safety ratings for flammability[1]BASF, “Hydrolysis-Resistant Ultramid for eMobility,” basf.com. Hydrolysis-resistant polyamides significantly enhance the lifespan of parts in humid, fast-charge conditions. Meanwhile, blends of polyphenylene sulfide further improve performance under high-temperature conditions, though they are associated with higher costs. In Europe and North America, flame-retardant additives have transitioned to halogen-free chemistries, simplifying end-of-life recovery processes. As a result, battery enclosures have emerged as the fastest-growing application in the automotive plastic compounding market, driving specialty thermoplastics into broader adoption. Vendors with proprietary flame-retardant formulations benefit from premium pricing and extended customer qualification cycles.

Global Vehicle Production Rebound Post-2025

By the latter part of the decade, easing semiconductor bottlenecks is expected to enhance global light-vehicle production, reinstating demand for dashboard, bumper, and under-hood compounds. Expansions in final assembly across Southeast Asia and localization initiatives in India gain significance as cost-conscious original equipment manufacturers shift to high-fill polypropylene grades, balancing performance and cost. China's increase in production capacity for polyether polyols and other intermediates highlights a positive outlook on sustained demand for interior components. Although Europe and North America face challenges from higher energy and labor costs, strategic near-shoring to Mexico, supported by trade agreements, is helping to stabilize volumes in North America. This market recovery presents an opportunity for compounders to improve margins, provided they manage feedstock price fluctuations effectively.

Laser-Weldable Polyolefin Compounds for Modular Lighting

Automotive lighting modules now utilize laser welding to seamlessly integrate lenses, housings, and light-emitting diode arrays. This process requires infrared-transparent outer layers and absorber-pigmented inner layers. By employing polybutylene terephthalate and laser-transparent polycarbonate compounds, manufacturers can significantly reduce assembly times and achieve hermetic seals without the need for adhesives. While premium electric vehicle brands in North America and Europe have been the early adopters, there is an anticipated shift towards mid-segment penetration as tooling costs are amortized. Compounders that provide both transparent and absorber grades from a single source are securing platform-wide supply awards, enhancing customer loyalty. Looking ahead, this trend is poised to create a valuable new avenue for specialty polyolefins in the automotive plastic compounding market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-linked resin price volatility | -0.70% | Global, acute in import-dependent India and Southeast Asia | Short term (≤ 2 years) |

| Recycling infrastructure deficit for mixed-filler streams | -0.50% | North America, ASEAN, MEA | Medium term (2-4 years) |

| Heat-soak and EMI limits in e-powertrains | -0.40% | Global, high-voltage applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-Linked Resin Price Volatility

In early 2026, a single quarter experienced a significant increase in polypropylene prices, which tightened the margins for compounders. This fluctuation in polypropylene, along with shifts in prices for polyamide and polycarbonate feedstocks, closely mirrored the trends in crude oil and natural gas prices[2]Plastics News, “Resin Prices Surge in 2026,” plasticsnews.com . Premiums for polyamide 6.6 have increased due to disruptions in adiponitrile supply, while polycarbonate costs have risen because of restrictions related to phosgene. Producers with integrated operations mitigate risks through upstream assets, whereas independent producers face challenges from mismatched contracts. Bio-based polyamides provide some protection against market volatility but are associated with higher costs.

Recycling Infrastructure Deficit for Mixed-Filler Streams

Reprocessing glass-fiber and mineral-filled scraps poses challenges: fiber attrition diminishes mechanical properties, and mixed streams compromise melt purity. Chemical recycling plants capable of depolymerizing filled compounds are limited in availability outside of Western Europe. As a result, most markets rely on waste generated during manufacturing processes. Manufacturers' commitments to using recycled content are putting pressure on the available supply. This has led to recycled compounds being allocated to less critical applications, a situation expected to continue until the necessary infrastructure is further developed. This ongoing gap is likely to restrict the growth of recycled grades with high filler content over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Polypropylene Dominance with Bio-Based Upside

Polypropylene compounds delivered 34.87% of the automotive plastic compounding market share in 2025 on the strength of cost-effective glass-filled grades for bumpers, door modules, and dashboards. The Automotive plastic compounding market size for bio-polymers, though smaller, is projected to expand at 6.11% CAGR between 2026 and 2031, catalyzed by OEM net-zero agendas and renewable-content credits.

Flanking polypropylene’s footprint, hydrolysis-resistant polyamides secure under-hood and battery-enclosure real estate, polycarbonate offers optical clarity for glazing, and ABS persists in high-finish interior parts. Bio-based polyamides derived from castor oil combine temperature resistance with renewable feedstock, signaling an emerging premium niche. The resulting material matrix confirms a gradual but noticeable tilt toward low-carbon chemistries within the broader Automotive plastic compounding market.

By Filler / Modifier Type: Glass-Fiber Reinforcement Sets the Pace

Glass-fiber reinforcements contributed 29.04% to 2025 revenue and will climb at a 5.89% CAGR over 2026 to 2031. Long-fiber thermoplastics are increasingly being used in semi-structural battery trays and front-end carriers. While carbon-fiber grades enhance the stiffness-to-weight ratios for premium electric vehicles, their significantly higher cost limits widespread adoption.

Mineral fillers, like talc, help reduce costs for wheel-arch liners and under-body shields. Meanwhile, flame-retardant packages are transitioning to halogen-free systems, ensuring compliance with UL 94 V-0 standards and facilitating recycling. In Europe, recycled-content modifiers are witnessing the fastest growth, driven by mandatory thresholds. These choices in filler technology underscore the importance of property tailoring in capturing value within the automotive plastic compounding market.

By Application: Interiors Lead, Battery Enclosures Accelerate

Interiors absorbed 32.89% of demand in 2025, reflecting steady production of instrument panels and door trims around the world. Conversely, battery-enclosure compounds show the sharpest trajectory at 6.33% CAGR through 2026 to 2031. OEMs now demand flame-retardant polymers with certifications for extended life cycles.

For reasons of weight and cost, exterior panels are increasingly shifting to long-glass-fiber polypropylene. Meanwhile, modular lighting is adopting laser-weldable polybutylene terephthalate and polycarbonate. As internal combustion engines downsize, leading to heightened under-bonnet temperatures, under-hood fluid systems are turning to blends of high-heat polyamide and polybutylene terephthalate. These industry shifts are expanding the functional scope of the automotive plastic compounding market.

By Vehicle Type: Electrified Platforms Re-Shape Volume Mix

Passenger cars dominated with 60.83% share in 2025, but battery-electric and hybrid vehicles will be the primary growth lever, rising at 6.29% through 2026 to 2031. In electric vehicles, the use of packaged plastics per vehicle has significantly increased due to components like the battery cage, thermal plates, and orange-cable connectors, even as fuel-system components experience a decline.

Light commercial vehicles are now using abrasion-resistant polypropylene for bed-liners, while heavy trucks are relying on high-temperature polyamide and polyphenylene sulfide in their emission-control modules. As buses and delivery fleets transition towards electrification, there is a noticeable shift in volume towards flame-retardant grades. These trends highlight the pivotal role of electrification in shaping the automotive plastic compounding market.

Geography Analysis

Asia-Pacific held the largest 47.18% share of the Automotive plastic compounding market size in 2025 and is also projected to post the quickest 6.45% CAGR over 2026-2031, highlighting the region's leadership in both scale and momentum. China stands out, commanding a significant portion of the regional demand. This dominance is bolstered by China's impressive vehicle production and its aggressive dual-credit policies, which are fast-tracking the adoption of electric vehicles. Meanwhile, in India, government incentives and a surge in sport utility vehicle sales are driving market expansion. Notably, polypropylene compounds have captured a considerable share of the local demand, underscoring a trend towards cost-focused part specifications. Japan is shifting its focus towards mono-material bumper programs and is increasingly utilizing recycled polypropylene grades. South Korea's large family-owned business groups are ramping up polyamide capacity, catering to domestic battery-electric plants, which have shown substantial growth.

North America holds a substantial stake, accounting for a notable share of the global automotive plastic compounding market. Trade regulations are channeling assembly and compounding activities into Mexico. A testament to this shift is Husco International's acquisition of Mayfair Plastics, which brought in numerous injection lines with sourcing compliant to tariffs. Meanwhile, the United States Inflation Reduction Act is igniting a surge in domestic production of flame-retardant polyamide and polypropylene grades, crucial for battery enclosures. Both BASF and Covestro have scheduled their production start-ups. In a strategic move, LyondellBasell and Sipchem are conducting feasibility studies on a mixed-feed cracker in Saudi Arabia, signaling a push for upstream integration in the Middle-East, targeting North American clients downstream.

Despite grappling with high energy costs, Europe continues to wield significant influence in innovation and regulation. The revised End-of-Life Vehicle regulations, which mandate a specific percentage of recycled content by a future date, are driving investments from industry players. Companies like Borealis, Trinseo, and MBA Polymers are pivoting towards circular-ready polypropylene and polycarbonate compounds. Borealis is making a significant investment in its Schwechat line, focusing on glass-fiber and flame-retardant grades tailored for European electric vehicles. On a larger scale, Mutares has bolstered its regional presence with the acquisition of SABIC's engineering thermoplastics division. In South America, Brazil's vehicle assembly footprint remains the focal point. Meanwhile, in the Middle-East and Africa, demand is still in its infancy but on an upward trajectory. Saudi Arabia is ramping up its polymer capacity, and South Africa is making strides to address its energy challenges.

Competitive Landscape

The automotive plastic compounding market is moderately fragmented. The pace of acquisitions has picked up. Mutares made headlines by acquiring SABIC’s engineering thermoplastics unit, a move that added substantial compounding capacity, with a notable portion earmarked for automotive use. This acquisition catapulted Mutares into the ranks of the world's second-tier players. Borealis, making a strategic move, invested heavily in high-recycled and flame-retardant polypropylene facilities in Austria and Germany. This investment signals a strong bet on the European Union's recycled-content mandates. Furthermore, Orinko's acquisition of a majority stake in the Italian compounder Omikron and Polyram's investment in LAPO highlight a trend: Asian firms are keenly eyeing European companies, seeking a foothold in the premium segment.

Automotive Plastic Compounding Industry Leaders

LyondellBasell Industries Holdings B.V.

BASF SE

SABIC

Covestro AG

Celanese Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Husco International will acquire Mayfair Plastics, seamlessly integrating 77 injection machines. This strategic move will bolster the Automotive Plastic Compounding Market, amplifying production capacity and ensuring sourcing aligns with USMCA standards. Such compliance is paramount for catering to the demands of automakers in Detroit.

- September 2025: Borealis inaugurated a new polypropylene compounding facility in Austria, with an investment exceeding EUR 100 million. This state-of-the-art facility, featuring twin-screw lines, is strategically positioned to drive innovations in the Automotive Plastic Compounding Market. Its primary focus is to cater to the rising demand for glass-fiber and flame-retardant grades, especially in the realm of electric vehicles. Additionally, in a nod to sustainability, the facility processes up to 50% recycled feed.

Global Automotive Plastic Compounding Market Report Scope

Automotive Plastic Compounding is the process of blending base polymers with fillers, reinforcements, and additives to create customized materials tailored for vehicle applications. This enhances properties such as strength, durability, heat resistance, and recyclability. Compounded plastics are widely used in interiors, exteriors, under-hood systems, and electric vehicle components, supporting lightweight design, sustainability, and performance improvements across the automotive industry.

The Automotive plastic compounding market is segmented by polymer type, filler/modifier type, application, vehicle type, and geography. By polymer type, the market is segmented into polypropylene (PP), polyamide (PA 6, 6.6, 12), polycarbonate (PC), polyethylene (HDPE, LDPE), acrylonitrile-butadiene-styrene (ABS), polyvinyl chloride (PVC), polybutylene terephthalate (PBT), polyphenylene sulfide (PPS), LCP, and high-performance bio-polymers. By filler/modifier type, the market is segmented into mineral-filled (talc, CaCO₃), glass-fiber reinforced, carbon-fibre and LFT, flame-retardant compounds, impact modifiers and tougheners, UV/IR stabilizer packages, and recycled-content (>30% PCR) compounds. By application, the market is segmented into interior components, exterior panels and trim, under-hood/power-electronics, lighting systems and lens housings, high-voltage battery enclosures, and fuel- and fluid-contact systems. By vehicle type, the market is segmented into passenger cars, light commercial vehicles, heavy trucks and buses, and battery-electric and hybrid vehicles. The report also covers the market size and forecasts for the Automotive Plastic Compounding Market in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Polypropylene (PP) |

| Polyamide (PA 6, 6.6, 12) |

| Polycarbonate (PC) |

| Polyethylene (HDPE, LDPE) |

| Acrylonitrile-Butadiene-Styrene (ABS) |

| Polyvinyl Chloride (PVC) |

| Polybutylene Terephthalate (PBT) |

| Polyphenylene Sulfide (PPS) and LCP |

| High-performance Bio-polymers |

| Mineral-filled (Talc, CaCO₃) |

| Glass-fibre Reinforced |

| Carbon-fibre and LFT |

| Flame-retardant Compounds |

| Impact Modifiers and Tougheners |

| UV / IR Stabiliser Packages |

| Recycled-content (>30 % PCR) Compounds |

| Interior Components |

| Exterior Panels and Trim |

| Under-hood / Power-electronics |

| Lighting Systems and Lens Housings |

| High-voltage Battery Enclosures |

| Fuel- and Fluid-contact Systems |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Trucks and Buses |

| Battery-Electric and Hybrid Vehicles |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Polymer Type | Polypropylene (PP) | |

| Polyamide (PA 6, 6.6, 12) | ||

| Polycarbonate (PC) | ||

| Polyethylene (HDPE, LDPE) | ||

| Acrylonitrile-Butadiene-Styrene (ABS) | ||

| Polyvinyl Chloride (PVC) | ||

| Polybutylene Terephthalate (PBT) | ||

| Polyphenylene Sulfide (PPS) and LCP | ||

| High-performance Bio-polymers | ||

| By Filler / Modifier Type | Mineral-filled (Talc, CaCO₃) | |

| Glass-fibre Reinforced | ||

| Carbon-fibre and LFT | ||

| Flame-retardant Compounds | ||

| Impact Modifiers and Tougheners | ||

| UV / IR Stabiliser Packages | ||

| Recycled-content (>30 % PCR) Compounds | ||

| By Application | Interior Components | |

| Exterior Panels and Trim | ||

| Under-hood / Power-electronics | ||

| Lighting Systems and Lens Housings | ||

| High-voltage Battery Enclosures | ||

| Fuel- and Fluid-contact Systems | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Trucks and Buses | ||

| Battery-Electric and Hybrid Vehicles | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Automotive plastic compounding market?

The sector is valued at USD 9.68 billion in 2026 and is poised to reach USD 12.65 billion by 2031.

Which polymer commands the largest share in global automotive compounding?

Polypropylene compounds held 34.87% of the global share in 2025, reflecting their cost and performance balance.

Which application will grow fastest to 2031?

High-voltage battery-enclosure compounds are forecast to advance at a 6.33% CAGR on the back of accelerating EV adoption.

How do recycled-content mandates influence material choices?

EU rules requiring 25% recycled content by 2030 push OEMs toward mono-material bumper systems and certified post-consumer polypropylene blends.

Page last updated on: