Plasterboard Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

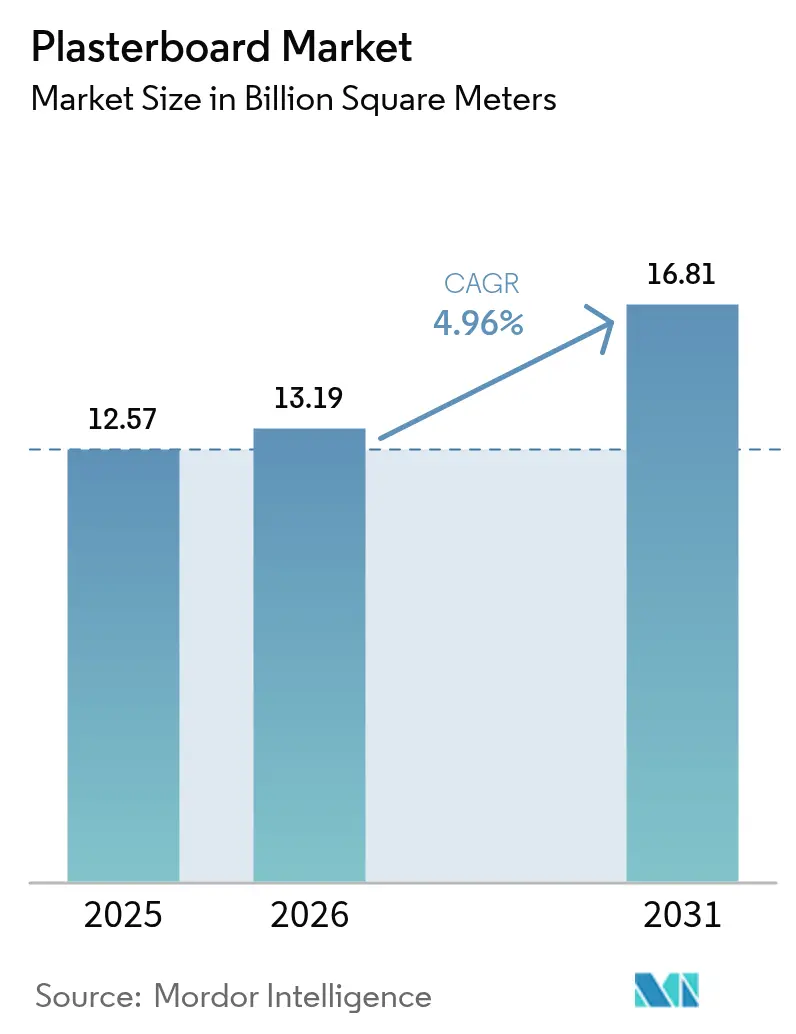

| Market Volume (2026) | 13.19 Billion square meters |

| Market Volume (2031) | 16.81 Billion square meters |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

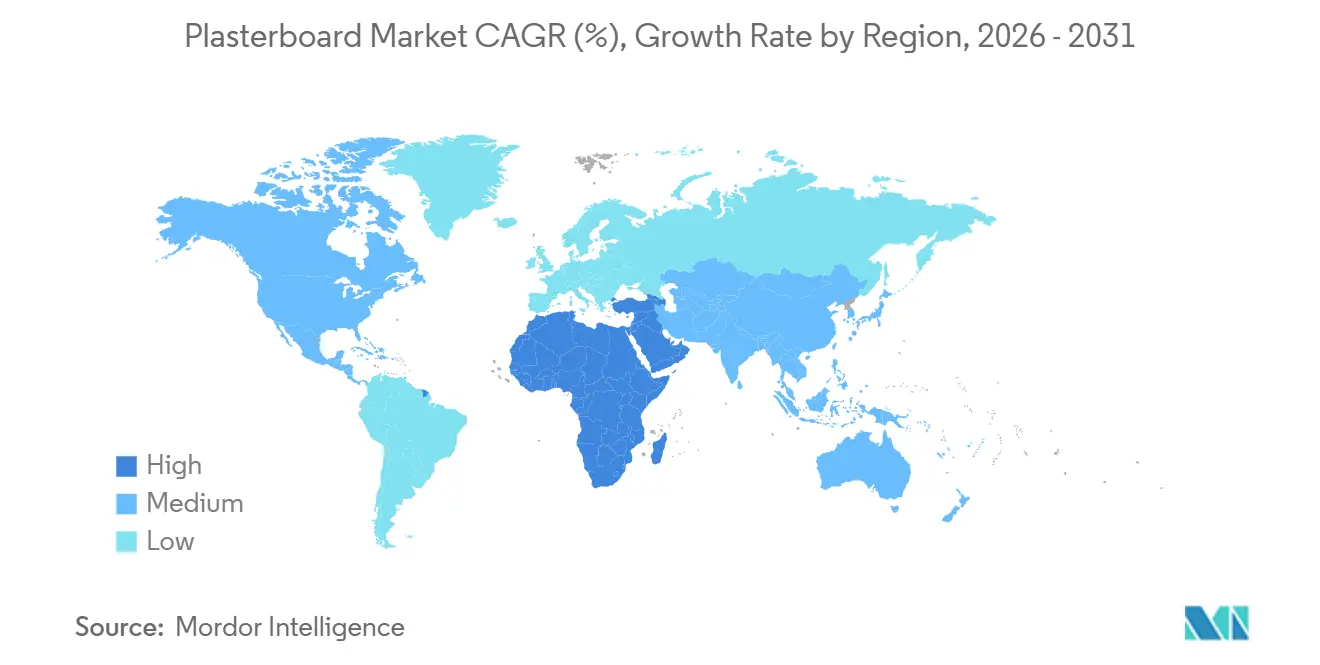

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plasterboard Market Analysis by Mordor Intelligence

The Plasterboard Market size is expected to increase from 12.57 billion square meters in 2025 to 13.19 billion square meters in 2026 and reach 16.81 billion square meters by 2031, growing at a CAGR of 4.96% over 2026-2031. Momentum is coming from the accelerating switch to dry-construction systems that cut on-site cycle times, stringent green-building codes that reward low-VOC and high-recycled-content panels, and regionally specific housing mega-projects that lock in long-term volume. Asia-Pacific anchored 46.11% of global demand in 2025 as China’s affordable-housing targets and India’s Pradhan Mantri Awas Yojana boosted wallboard consumption, while the Middle East and Africa registered the fastest growth at a 5.27% CAGR, propelled by Saudi Arabia’s USD 500 billion NEOM program and parallel Gulf developments. Competitive strategies now converge on lightweight formulations, circular-economy sourcing, and digital-jobsite enablement that helps contractors lower total installed cost, securing specification loyalty in both residential and non-residential build cycles.

Key Report Takeaways

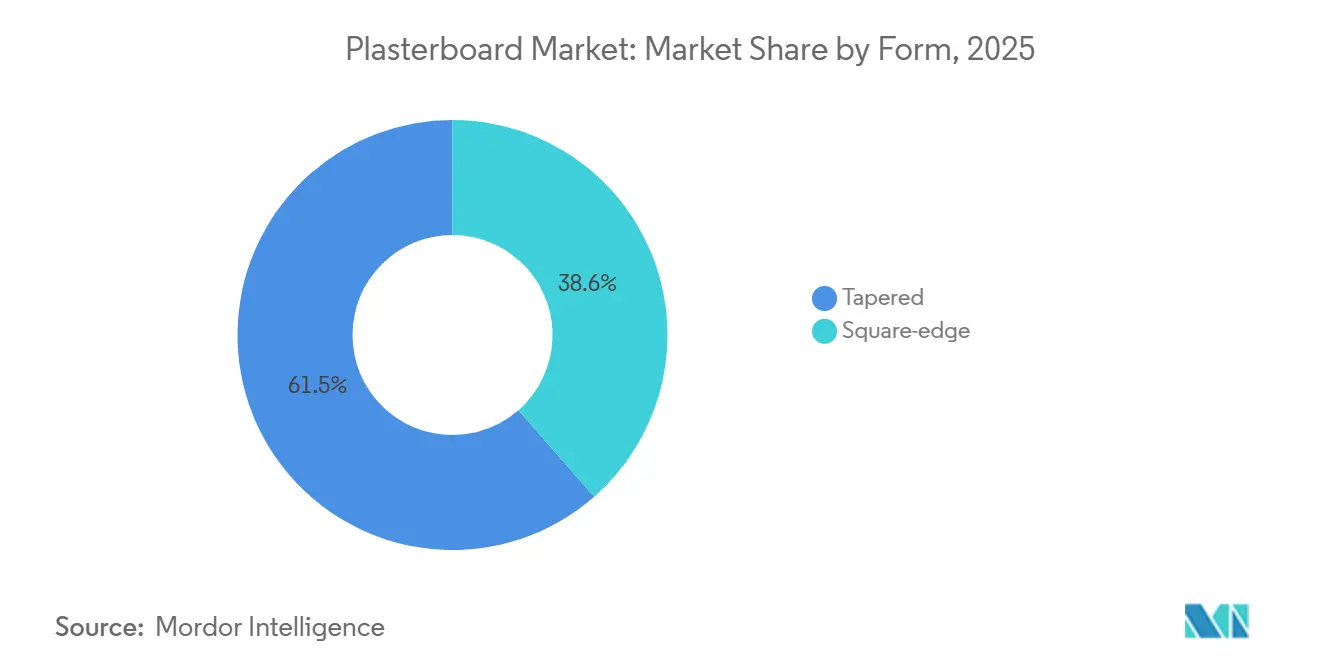

- By form, tapered-edge boards led the Plasterboard market with a 61.45% share in 2025, whereas square-edge variants are growing at a 5.12% CAGR during the forecast period (2026-2031).

- By type, standard boards accounted for 55.12% of the Plasterboard market size in 2025, while moisture-resistant grades posted the highest 5.57% CAGR during the forecast period (2026-2031).

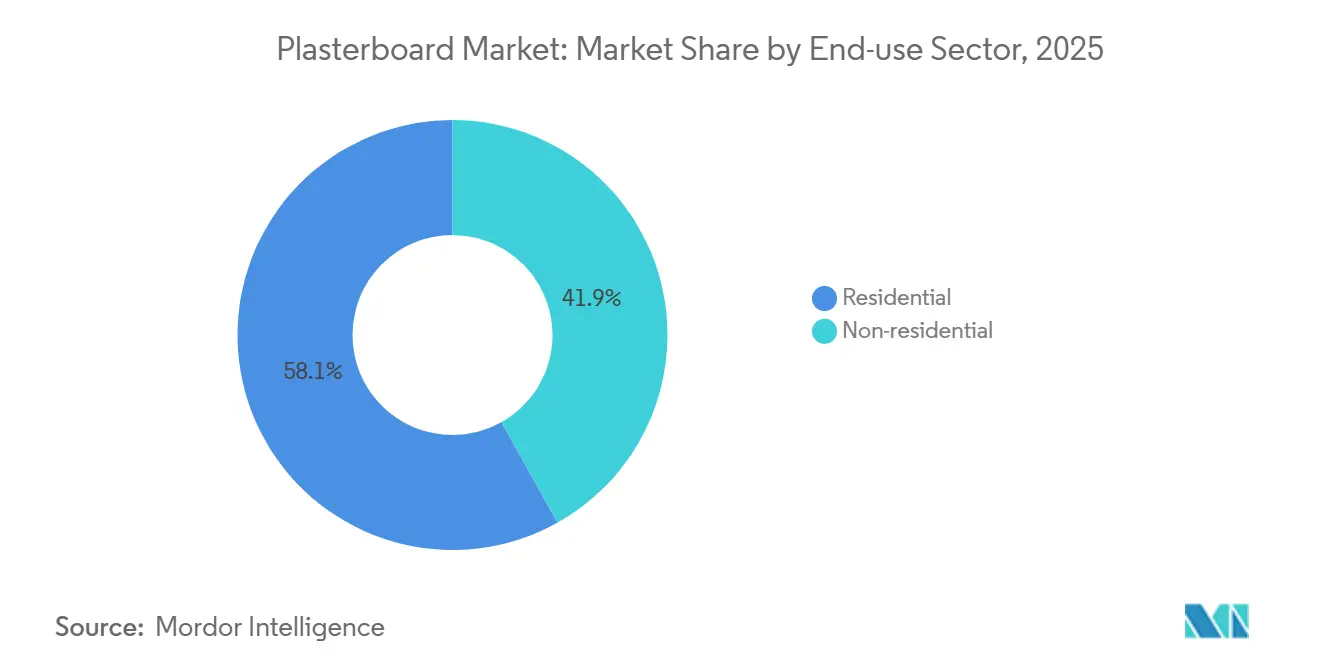

- By end-use sector, residential construction accounted for 58.13% of the 2025 volume, while non-residential projects registered the fastest growth rate of 5.41% during the forecast period (2026-2031).

- By geography, the Asia-Pacific region captured 46.11% of the global volume in 2025; the Middle East and Africa region is expected to expand at a 5.27% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plasterboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift toward dry-construction techniques | +1.2% | Global | Long term (≥ 4 years) |

| Asia and GCC residential mega-projects pipeline | +1.0% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Tightening green-building VOC/recycled-content rules | +0.8% | Global, with early enforcement in EU & California | Medium term (2-4 years) |

| Low-cost synthetic-gypsum supply in emerging markets | +0.6% | APAC, South America, MEA | Short term (≤ 2 years) |

| AI-enabled job-site layout tools boost installer productivity | +0.5% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Dry-Construction Techniques

Dry assemblies replace labor-intensive wet masonry in markets where builder penalties for late delivery outweigh material premiums. Prefabricated wall systems and modular frames cut on-site schedules by up to 40%, driving contractors to specify multi-performance plasterboard combinations, fire, sound, and moisture resistance, in a single envelope. Industry surveys show Building Information Modeling adoption reached 73% among Tier-1 general contractors in North America during 2025, enabling off-site panel fabrication that reduces rework. China’s 14th Five-Year Plan and India’s Smart Cities Mission explicitly encourage industrialized construction, shifting demand toward high-rise mixed-use towers that require large quantities of tapered-edge and specialty boards[1]State Council of the People’s Republic of China, “Outline of the 14th Five-Year Plan,” gov.cn. The trend progressively migrates into mature European and United States renovation cycles, where labor scarcity and high wage rates make speed paramount.

Asia and GCC Residential Mega-Projects Pipeline

Saudi Arabia’s NEOM targets 80,000 residential units and 9,000 hotel rooms in its first phase, while The Red Sea Project, Qiddiya, and New Murabba together add another 7 million m² of built-up area, committing over USD 1 trillion of capex through 2030. Simultaneously, India delivered 29 million homes under PMAY (Pradhan Mantri Awas Yojana) by 2024, and Indonesia’s greenfield Nusantara capital has mobilized 200,000 construction workers. These pipelines demand tapered-edge boards for seamless interiors and moisture-resistant variants suitable for coastal humidity, giving an advantage to producers with plants inside the Gulf Cooperation Council customs union or within India’s GST (Goods and Services Tax) corridor. Local capacity sidesteps freight surcharges that can add 15% to landed cost, making proximity a decisive competitive factor.

Tightening Green-Building VOC/Recycled-Content Rules

California’s Title 24 and the European Union Construction Products Regulation (CPR-2024) now cap interior-finish VOCs (Volatile Organic Compounds) at 0.5 ppm (parts per million), disqualifying legacy high-binder formulas. LEED (Leadership in Energy and Environmental Design) v5 adds credits for 20% post-consumer recycled content, steering procurement toward synthetic-gypsum and reclaimed demolition materials. Knauf’s Fiberock Aqua-Tough (95% recycled content) and CertainTeed’s Extreme with M2Tech technology exemplify compliant, low-VOC launches. Reformulation cycles cost 18-24 months and require ISO 14001 certification, but compliance opens doors to government tenders in the European Union and United States public-schools programs that collectively place over USD 150 billion of new building materials annually.

Low-Cost Synthetic-Gypsum Supply in Emerging Markets

Flue-gas desulfurization (FGD) gypsum accounted for 35% of global feedstock in 2025, with unit costs of USD 15-20 per tonne, about half the landed price of mined gypsum in land-locked regions[2]U.S. Geological Survey, “Gypsum Statistics and Information,” usgs.gov. China, India, and Southeast Asia generate 80% of that synthetic output, letting regional producers undercut imports by 20-25%. The model faces headwinds in North America and Europe as coal retirements choke supply, but newly commissioned scrubber plants across ASEAN and South Asia will offset declines elsewhere through 2030. Western producers respond by signing long-term offtake contracts or investing in closed-loop recycling mandated under California’s AB 1220, effective 2024, which bans landfilling of gypsum waste.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile gypsum and energy prices | -0.7% | Global | Short term (≤ 2 years) |

| Land-fill bans raise gypsum-waste disposal cost | -0.4% | EU & North America, early adoption in APAC urban centers | Medium term (2-4 years) |

| PFAS content scrutiny limits some fire-resistant boards | -0.3% | North America, with EU regulatory review underway | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Gypsum and Energy Prices

Natural gypsum spot prices climbed from USD 287 per ton in 2020 to USD 430 per ton in 2024 after mine closures in Spain and Mexico collided with freight cost spikes. Power and kiln fuel account for up to 25% of conversion cost; European natural gas averaged EUR 45/MWh in 202, double its 2020 level, forcing capacity curtailments. North American wallboard makers scrambled for dwindling FGD (Flue Gas Desulfurization) gypsum as 12 GW of coal generation retired in 2024, triggering bidding contests and temporary plant outages. Vertically integrated miners absorbed shocks better, but merchant buyers saw gross-margin erosion exceeding 300 basis points.

Land-Fill Bans Raise Gypsum-Waste Disposal Cost

California’s AB 1220 prohibits landfilling plasterboard and lifts tipping fees to USD 80 per ton for mixed loads; the European Union Waste Framework Directive introduces similar diversion targets, pushing United Kingdom disposal costs to GBP 98.60 (USD 132.12) per ton. Contractors must segregate scraps and route them to certified recyclers, raising logistics complexity and overhead on tight-margin renovation jobs. Large producers like Saint-Gobain operate 15 North American take-back hubs reclaiming 200,000 tons annually, while smaller firms struggle to fund equivalent loops.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Square-Edge Boards Pick Up Renovation Momentum

Tapered-edge boards kept a dominant 61.45% volume, sustained by new-build apartments and office interiors that prioritize seamless walls. North America and Western Europe, where wages top USD 40 per hour, will likely see square-edge share exceeding 45% by 2031, while Asia-Pacific sticks to tapered-edge for a premium finish at lower labor rates. Square-edge panels are set to grow at a 5.12% CAGR during the forecast period (2026-2031), outperforming the aggregate plasterboard market. Renovation crews favor the profile because butt-joint finishing shortens labor by roughly 18% on small projects, holding down overall installed cost.

Manufacturers are blurring lines: CertainTeed’s 2026 micro-bevel launch bridges aesthetics and speed, offering a near-tapered finish without compound feathering. National Gypsum’s lightweight EVOLVE range, introduced in 2025, comes in both edge types, signaling supplier hedging rather than wagering on a single winner. The plasterboard market share of hybrid edges is expected to rise, particularly in hospitality refurbishments, where schedule, weight limits, and appearance all matter.

By Type: Moisture-Resistant Boards Drive Specialty Upside

Standard panels retained 55.12% of 2025 volume, yet moisture-resistant grades are climbing 5.57% CAGR to 2031, the fastest among six product categories, fueled by hyperscale data centers, coastal housing, and healthcare facilities requiring mold-proof interiors. Fire-resistant boards remain compliance essentials for egress corridors but face PFAS-related recertification holdups, tempering their advance. Sound-attenuating, impact-resistant, and thermal-insulated panels collectively earn margins above commodity boards, making them attractive pockets even at modest tonnage.

Price gaps narrow as technology evolves: CertainTeed’s Extreme line carries a 12% premium versus commodity drywall yet scores 10 on ASTM D3273. British Gypsum’s dual-performance FireLine MR merges moisture and 60-minute fire resistance, shrinking SKU counts for builders. These multi-attribute products are set to push the moisture-resistant plasterboard market share, reshaping the mix and raising average selling prices.

By End-Use Sector: Non-Residential Accelerates Ahead of Housing Starts

Residential held 58.13% of global demand in 2025, buoyed by Asia’s affordable-housing drives, but non-residential demand is pacing faster at 5.41% CAGR during the forecast period (2026-2031). Data centers alone added roughly 2.5 GW of IT load in 2025, consuming 8-10 million m² of specialty boards for fire and moisture protection. Healthcare expansions across OECD (Organisation for Economic Co-operation and Development) economies prefer impact- and sound-resistant drywall for patient safety, supplying another high-margin outlet. Logistics warehouses specify mainly standard boards for office cores, yet their sheer square footage supports e-commerce growth, making them a large incremental sink. Residential volume leadership continues, but its growth skews toward emerging markets and high-end custom builds in mature economies, where multi-performance wallboard justifies premium pricing.

Geography Analysis

Asia-Pacific anchored 46.11% of the Plasterboard market in 2025, yet its growth rate cools as China’s developers deleverage and renovation supplants greenfield starts. India’s Smart Cities and industrial corridors still lift regional volumes, and Indonesia’s Nusantara project keeps ASEAN demand buoyant. Japan and South Korea maintain steady replacement demand driven by seismic retrofits and aging infrastructure that increasingly mandates fire-resistant and lightweight panels.

The Middle East and Africa lead regional growth at 5.27% CAGR to 2031 on the back of Saudi Vision 2030, the United Arab Emirates's Expo City expansion, and Egypt’s New Administrative Capital. Harmonized ASTM (American Society for Testing and Materials) and British Standards simplify cross-border board trade, enabling Riyadh, Doha, and Dubai plants to serve neighbors within a 500 km trucking radius. Regional specifications highlight moisture-resistant and tapered-edge boards suitable for coastal humidity and high-rise towers.

North America remains the second-largest region as data-center construction in Virginia and Texas offsets cooler single-family starts hurt by mortgage rates above 6%. California’s landfill ban accelerates gypsum-recycling mandates, pushing suppliers to incorporate take-back logistics. Europe, holding roughly one-quarter of global volume, is shaped by Construction Products Regulation (CPR)-2024 and the Energy Performance of Buildings Directive. Germany, the United Kingdom, and France focus on low-VOC recycled-content drywall, while Nordic countries over-index on thermal-insulated boards for energy-efficient envelopes. South America’s recovery is driven by Brazil’s Minha Casa Minha Vida II and Argentina’s infrastructure push, although currency volatility favors locally mined gypsum over imports.

Competitive Landscape

The Plasterboard market is moderately fragmented. Asian challengers exploit synthetic-gypsum feedstock from coal scrubbers to undercut pricing by 20–25% in Southeast Asia and the Gulf. Patent filings cluster around lightweight cores, recycled cellulose facings, and PFAS (per- and polyfluoroalkyl substances)-free fire retardants. Smaller regional firms lag due to capital constraints, creating acquisition opportunities for majors seeking ESG (Environmental, Social, and Governance)-compliant growth.

Plasterboard Industry Leaders

Etex Group

Saint-Gobain

Georgia-Pacific

USG Corporation

Knauf Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Saint-Gobain unveiled its CertainTeed plasterboard facility in Sainte-Catherine, Canada. This plant, now entirely electrified, draws its power from hydroelectric sources and stands as North America's inaugural zero-carbon (encompassing scope 1 and 2) plasterboard facility.

- March 2025: The Deputy Minister of Economy and Commerce of the Kyrgyz Republic inaugurated the construction of new production facilities for Mega Union Industry LLC, specializing in gypsum and gypsum plasterboard sheets.

Global Plasterboard Market Report Scope

Plasterboard is basically a layer of gypsum between two layers of lining paper. The gypsum layer can have different additives added to it, and the lining paper can have different additives, weight, and strength.

The Plasterboard market is segmented into form, type, end-use sector, and geography. By form, the market is divided into square-edged and tapered. By type, the market is divided into fire-resistant, impact-resistant, thermal-insulated, moisture-resistant, sound-resistant, and standard. By end-use sector, the market is divided into residential and non-residential. The report also covers the Plasterboard market size and forecasts for the plasterboard market in 15 countries across major regions. Market sizing and forecasting for each segment have been done based on volume (square meters).

| Square-edge |

| Tapered |

| Standard |

| Fire-resistant |

| Thermal-insulated |

| Moisture-resistant |

| Sound-resistant |

| Impact-resistant |

| Residential |

| Non-residential |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Square-edge | |

| Tapered | ||

| By Type | Standard | |

| Fire-resistant | ||

| Thermal-insulated | ||

| Moisture-resistant | ||

| Sound-resistant | ||

| Impact-resistant | ||

| By End-use Sector | Residential | |

| Non-residential | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global demand for plasterboard by 2031?

Demand is forecast to reach 16.81 million square meters by 2031, growing at a 4.96% CAGR from 2026 to 2031.

Which region is expected to grow fastest in plasterboard consumption through 2031?

The Middle East and Africa are set to expand at a 5.27% CAGR, led by Saudi Arabia’s NEOM and other Gulf mega-projects.

Why are moisture-resistant boards gaining share?

Data centers, healthcare facilities, and coastal housing require mold-proof interiors, pushing moisture-resistant volumes to a projected 25-30% share by 2031.

How are landfill bans affecting plasterboard disposal costs?

California and the EU now levy fees up to USD 80-100 per tonne on mixed gypsum waste, making recycling programs economically attractive.

What strategic moves are market leaders making to secure raw materials?

Majors such as Saint-Gobain and Knauf are integrating into gypsum mining and locking long-term synthetic-gypsum offtake contracts to hedge price volatility.

Page last updated on: