Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

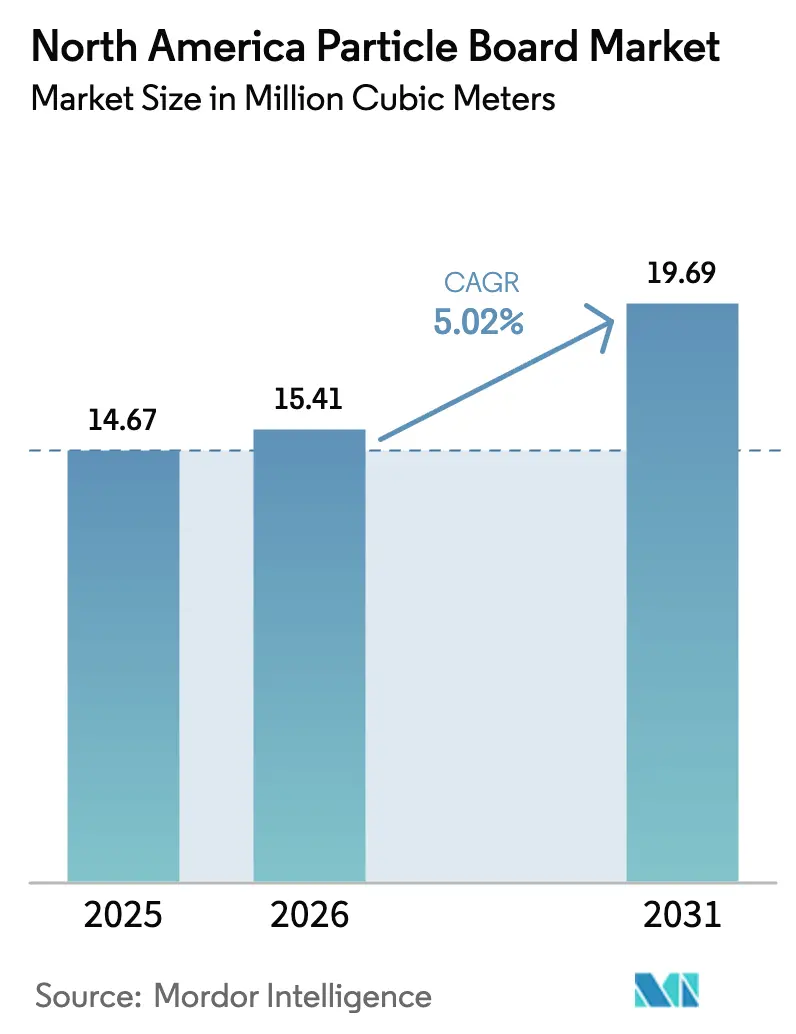

| Base Year Market Size (2025) | 14.67 Million cubic meters |

| Market Volume (2026) | 15.41 Million cubic meters |

| Market Volume (2031) | 19.69 Million cubic meters |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

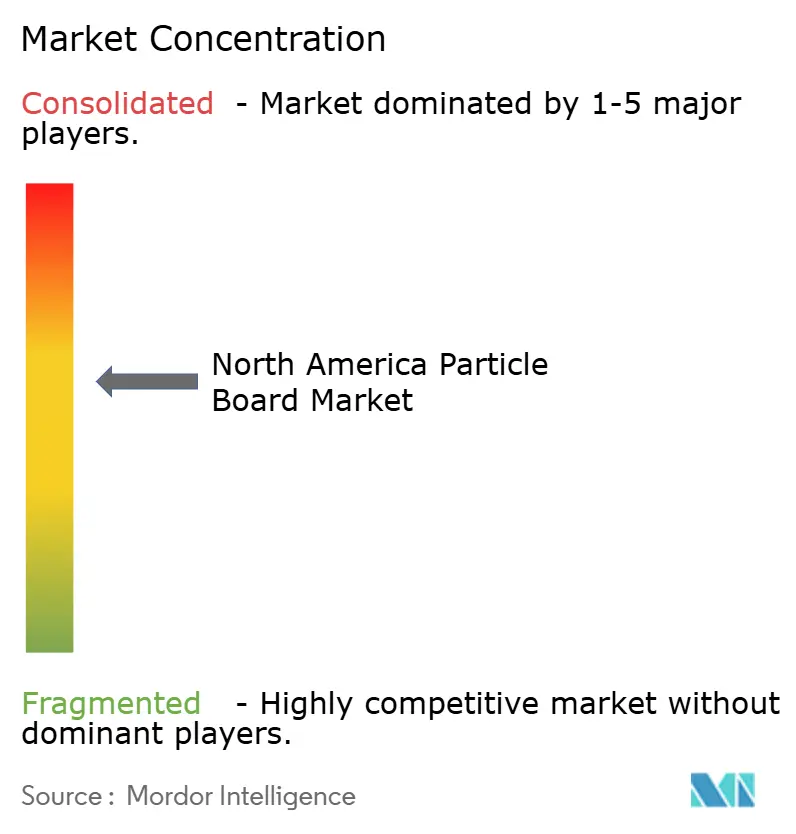

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Particle Board Market Analysis by Mordor Intelligence

North America Particle Board Market size in 2026 is estimated at 15.41 million cubic meters, growing from 2025 value of 14.67 million cubic meters with 2031 projections showing 19.69 million cubic meters, growing at 5.02% CAGR over 2026-2031. This growth trajectory reflects three intersecting forces. First, state-level landfill-diversion mandates are redirecting construction and demolition wood into panel furnish, easing raw-material costs for mills located near urban waste streams. Second, furniture producers are re-engineering product lines around flat-pack formats that prize low weight and tight dimensional tolerances, a design philosophy that dovetails with continuous-press particle board. Third, sugarcane-growing regions in Louisiana are commercializing bagasse as an alternative furnish, helping producers hedge against sawmill-residue volatility. On the demand side, residential remodeling expenditures in the United States are driving cabinet substrates and flooring underlayment volumes upward. Competition is intensifying as continuous-press automation narrows the unit-cost gap between particleboard and medium-density fiberboard, prompting furniture OEMs to reassess their material specifications. Meanwhile, EPA formaldehyde caps have raised the compliance bar, accelerating consolidation and favoring mills that can amortize resin-system upgrades over larger output bases.

Key Report Takeaways

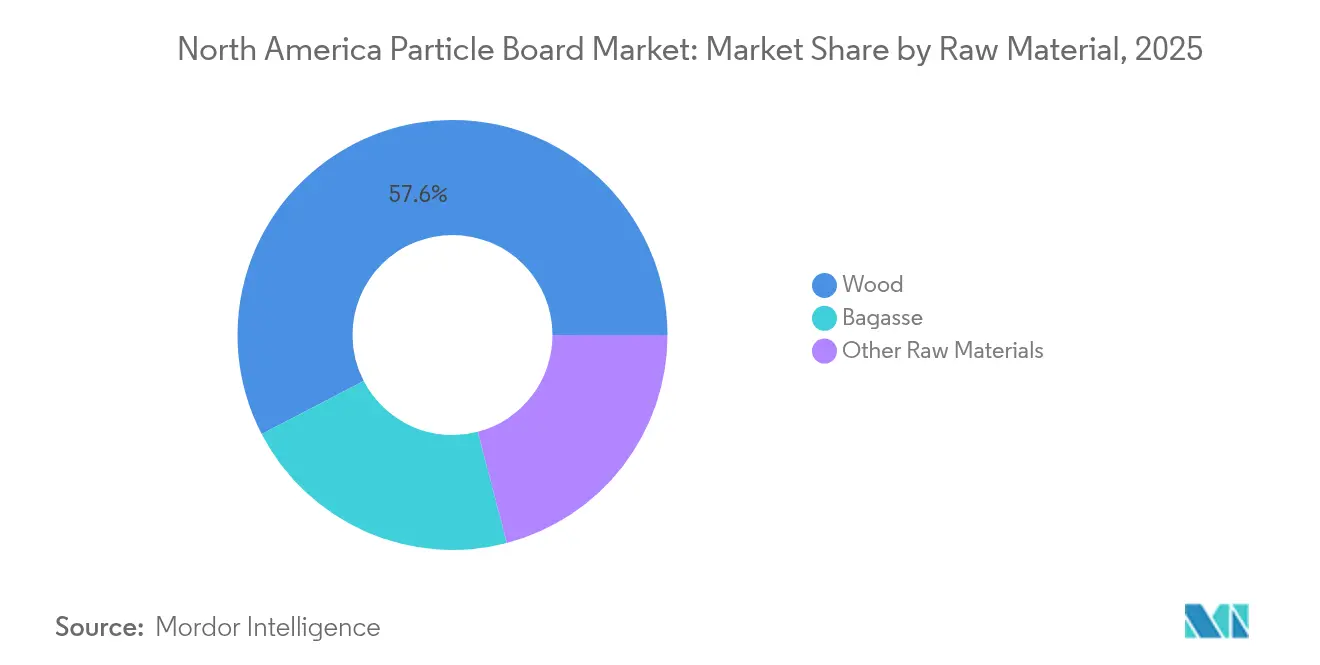

- By raw material, wood residues led with a 57.62% share of the North American particle board market in 2025, while bagasse is projected to expand at a 5.38% CAGR through 2031.

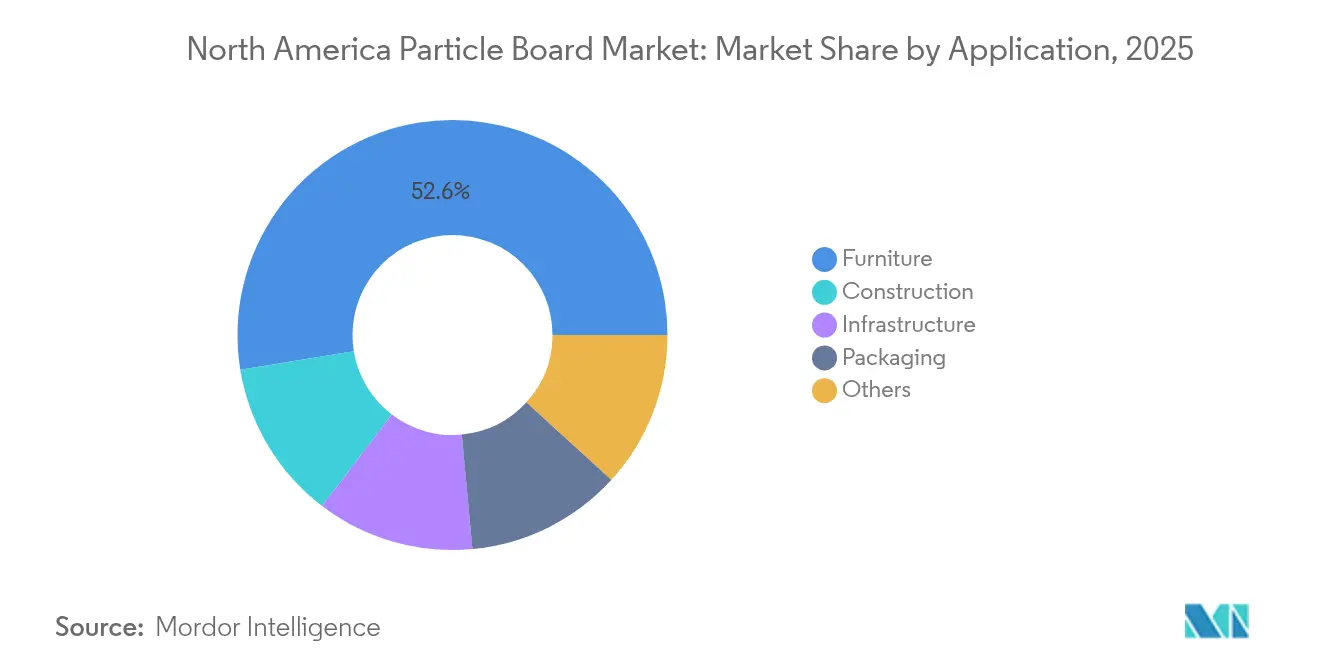

- By application, furniture accounted for 52.58% of the North American particle board market size in 2025 and is projected to advance at a 5.45% CAGR through 2031.

- By geography, the United States captured 66.45% of the North America particle board market share in 2025 and is forecast to grow at a 5.12% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Particle Board Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from the construction industry | +1.2% | United States, Canada | Medium term (2-4 years) |

| Easy availability of regional wood residues | +0.9% | United States (South, Pacific Northwest), Canada (Quebec, Ontario) | Short term (≤ 2 years) |

| Surge in RTA furniture and DIY renovation boom | +1.4% | United States, Canada, with urban concentration | Short term (≤ 2 years) |

| State-level landfill-diversion mandates unlocking recycled feedstock | +0.8% | United States (California, Washington, Oregon) | Medium term (2-4 years) |

| Continuous-press automation cutting unit costs | +0.7% | North America (facilities with capital access) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from the Construction Industry

Residential remodeling spending surpassed expectations in 2024, driving demand for particle board in countertop cores, stair treads, and interior partitions. Single-family housing starts remain comfortably above pre-pandemic baselines, and each new unit incorporates roughly 0.8–1.2 m³ of panel products. Modular construction is scaling in multi-family projects, favoring particle board because the material machines easily and withstands repeated handling during off-site assembly. Canada echoes this pattern, particularly in Ontario and British Columbia, where provincial codes now recognize engineered wood for use in non-load-bearing walls. Infrastructure spending, although a smaller slice of consumption, is lifting particle board volumes in acoustic baffles and temporary formwork used in transit corridors.

Easy Availability of Regional Wood Residues

The 2023 U.S. Department of Energy Billion-Ton Report identified logging residue and unused mill residue as sources of annual waste. Alabama, Georgia, Mississippi, and South Carolina collectively account for significant sawmill by-products each year, prompting mill investment along key rail corridors that connect forests to Gulf Coast ports. Quebec and Ontario enjoy a similar, if colder, dynamic: co-located sawmill and panel operations slash haul distances and stabilize furnish costs. Small-diameter trees harvested through U.S. Forest Service thinning contracts represent an additional source each year, although economics are sensitive to terrain and trucking radius.

Surge in RTA Furniture and DIY Renovation Boom

IKEA North America posted sales in FY 2023, a benchmark that underscores the pull of ready-to-assemble formats on the North America particle board market. E-commerce logistics reward low-bulk packaging, so furniture designers tend to gravitate toward particle board panels that deliver weight savings without compromising fastener-holding capacity. Social-media tutorials have democratized woodworking skills, prompting more homeowners to opt for flat-pack cabinets and laminate flooring underlayment that can be easily installed with basic tools. Millennial and Gen-Z households, typically more mobile than older cohorts, value affordability and quick assembly over heirloom durability. Big-box retailers now bundle particle board shelving and storage kits with step-by-step apps, further normalizing the material for non-structural household upgrades.

State-Level Landfill-Diversion Mandates Unlocking Recycled Feedstock

California’s SB 1383 requires 75% diversion of organic waste by 2025, placing construction and demolition wood squarely within the mandate[1]California Legislature, “SB-1383 Organic Waste Reductions,” leginfo.legislature.ca.gov. Local grinding stations now sell recycled furnish at shadow prices below USD 70 per dry ton, a discount that coastal particle board mills leverage to undercut inland rivals. Washington and Oregon rolled out similar bans, tightening supply for bioenergy plants and reshaping the cost curve for board producers. Public procurement rules in the West favor verified post-consumer content, giving certified panels a competitive edge in school and municipal projects. Mills outside coastal catchment zones must either import recycled furnish, increasing transport costs, or rely more heavily on sawmill residues that face rising competition from the pellet sector.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Threat of MDF and plywood substitutes | -0.6% | North America, with higher impact in premium furniture and cabinetry segments | Medium term (2-4 years) |

| Tightening formaldehyde-emission regulations | -0.4% | United States (EPA jurisdiction), Canada (Health Canada standards) | Short term (≤ 2 years) |

| Bio-energy projects competing for wood residue supply | -0.5% | United States (South, Pacific Northwest), Canada (British Columbia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Threat of MDF and Plywood Substitutes

Medium-density fiberboard commands a price premium but wins market share in painted cabinets because its fine fibers eliminate the need for edge banding. Plywood retains dominance in structural shelving and sub-floor assemblies where particle board’s lower internal bond strength is a disadvantage. Cross-laminated timber is emerging in mid-rise frames and threatens particle board’s foothold in non-structural skirting applications. Consumers in premium brackets often equate MDF or plywood with higher quality, particularly for moisture-prone areas such as kitchens and bathrooms. Producers are trialing melamine-urea-formaldehyde recipes, along with wax additives, to improve moisture resistance; however, these upgrades narrow the cost delta with MDF and curb particle board’s pricing appeal.

Tightening Formaldehyde-Emission Regulations

EPA’s 40 CFR Part 770 caps emissions at 0.09 ppm and mandates third-party certification for interstate commerce[2]U.S. Environmental Protection Agency, “Formaldehyde Standards 40 CFR Part 770,” epa.gov. California’s Air Resources Board enforces a stricter testing cadence, prompting mills to adopt more expensive phenol-formaldehyde or MDI binders. Health Canada has harmonized its thresholds with those of the EPA, removing any compliance arbitrage for exporters. Smaller mills face resin cost increases and must finance new large-chamber test equipment or outsource verification, both of which erode margins. Failure to comply risks recalls, contract loss, and reputational damage, spurring some mid-tier operators to exit or sell capacity to better-capitalized rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Wood Residues Maintain Leadership as Bagasse Gains Traction

Wood residues captured 57.62% of the North America particle board market share in 2025, reflecting entrenched sawmill infrastructure that channels sawdust, shavings, flakes, and chips into continuous-press furnish. Sawdust feeds the surface layer for a smoother finish, while coarser flakes bulk out the core where density drives bending strength. Chips from pulp operations provide a tertiary stream when low-grade roundwood is plentiful, especially in the U.S. South. Bagasse, the fibrous by-product of sugarcane crushing, is forecast to expand at a 5.38% CAGR through 2031, the fastest rate among feedstocks, helped by partnerships between Louisiana sugar mills and panel makers that monetize what was once a disposal cost. Laboratory trials confirm that bagasse boards bonded with MDI resin pass ANSI A208.1 internal-bond benchmarks. Secondary materials such as hemp hurds and cotton stalks remain niche because year-round supply consistency is elusive, a key requirement for continuous-press scheduling.

Continuous refinements in dryer controls and resin sprays are lowering the moisture penalty of recycled demolition lumber, enabling mills to blend reclaimed chips with virgin furnish without exceeding emissions thresholds. Nevertheless, shifting to higher recycled content demands closer contaminant screening because legacy plywood offcuts often carry phenol-based adhesives that skew formaldehyde assays. Large mills with optical sorting lines absorb this complexity more readily, reinforcing the scale advantage that characterizes the North America particle board market.

By Application: Furniture Segment Widens its Lead on DIY Momentum

Furniture accounted for 52.58% of the 2025 volume and is expected to grow at a 5.45% CAGR through 2031, driven by the rapid adoption of ready-to-assemble lines that reduce weight and ship flat. CNC routers cut particle board with minimal tool wear, and edge-banding machines accommodate thickness tolerances as tight as ±0.15 mm on continuous-press output. Construction ranked second, buoyed by remodeling projects that rely on particle board underlayment and stair treads for cost-optimized flooring systems. DIY channels accelerated during the pandemic era and have not receded, as big-box stores continue to stock panelized cabinet kits that reduce skilled-labor spend. Infrastructure and packaging remain smaller niches: transit-station acoustic panels and export crates, respectively, together account for less than one-tenth of aggregate demand. Yet federal domestic-content rules for public projects could stimulate broader use of recycled-content particle board in non-load-bearing partitions.

Retailers are increasingly specifying third-party-certified low-formaldehyde grades, thereby tightening inbound quality checks. This favors mills with on-site emissions testing, further consolidating the customer base around large-scale producers. As a result, furniture OEMs negotiate multi-year contracts tied to methylene-diphenyl-diisocyanate price indices, locking in supply while granting mills a predictable offtake that justifies new line debottlenecking.

Geography Analysis

The United States accounted for 66.45% of North American particle board shipments in 2025, and its output is set to rise at a 5.12% CAGR through 2031. Capacity additions are concentrated in the Southeast, and logistics corridors connect forests with Gulf ports, providing a cost advantage over import-dependent regions. On the West Coast, California’s SB 1383 is unlocking recycled wood flows that coastal mills leverage to underprice their interior competitors, although inland producers remain advantaged in terms of freight for Midwestern customers. The Pacific Northwest continues to contract as log export restrictions, wildfire setbacks, and sawmill closures tighten residue availability, prompting operators like Roseburg to shutter the Missoula line and redeploy capital to higher-yield assets.

Canada ranks second, with integrated facilities in Quebec and Ontario that pipe sawmill shavings directly into continuous press lines. Provincial stumpage policies favor domestic processing; however, rising natural-gas tariffs and competition from pulp mills increase operating costs. Housing starts remain below pre-2008 peaks, limiting growth in construction-linked panel usage. Western Canada sees residue diversion into pellet exports, creating episodic shortages for board producers in British Columbia. Nonetheless, Quebec’s Green Building Program incentivizes low-emission panels in municipal projects, opening a small but lucrative niche for certified particle board.

Mexico holds a modest share but offers white-space potential. Feedstock collection is fragmented, and continuous-press capacity is limited; however, the federal government’s housing-subsidy initiatives indicate a medium-term demand uplift. MASISA’s Terranova facility operates below nameplate capacity due to fuel shortages, yet sugarcane-based bagasse streams in Veracruz could supply future expansion phases if logistics hurdles are overcome. Investors will likely weigh the cost of supply-chain integration—harvesting, chipping, and rail links—against the cost of EPA-equivalent resin systems needed to export to the United States.

Competitive Landscape

The North American particle board market is moderately consolidated. Competitive levers cluster in three areas: furnish security, formaldehyde compliance, and automation maturity. Technologically, the arms race centers on continuous-press retrofits and inline quality control. EPA and CARB emission caps function as quasi-barriers to entry because quarterly testing and certification overhead erode the scale economies of small plants. Furniture OEMs are now writing low-formaldehyde clauses into supplier agreements, effectively blacklisting non-compliant mills. Strategic whitespace is visible in three lanes. First, bagasse-based boards in Louisiana utilize sugar sector residues and benefit from the renewable content marketing appeal. Second, recycled-content panels in California and Washington have reduced disposal fees for municipalities wrestling with SB 1383 compliance. Third, moisture-resistant grades paired with melamine films could claw back kitchen and bathroom share lost to MDF and plywood. Realizing these opportunities will require capital endowments that only larger incumbents or well-funded entrants can marshal.

North America Particle Board Industry Leaders

Roseburg Forest Products

Georgia-Pacific.

Arauco

Kronospan LLC

West Fraser Timber Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Georgia-Pacific confirmed that it will permanently close the Memphis Cellulose mill and the Memphis Technology and Innovation Center, resulting in the elimination of most positions by early December. The closure of the Memphis cellulose mill and technology center is likely to affect particleboard production, as cellulose is a key component in its manufacture.

- May 2024: Kronospan acquired Woodgrain’s particleboard facility in Island City, Oregon, thereby strengthening its North American footprint and advancing its growth strategy.

North America Particle Board Market Report Scope

Particle board, also known as fiberboard, is an engineered product created by combining residual lumber with a binder and applying high pressure and heat. The particle board market is segmented by raw material, application, and geography. By raw material, the market is segmented into wood, bagasse, and other raw materials. By application, the market is segmented into furniture, construction, infrastructure, packaging, and others. By geography, the market is segmented into the United States, Canada, and Mexico. The report covers the market size and forecasts for three countries across the region. For each segment, market sizing and forecasts have been provided based on volume (cubic meters).

By Raw Material

| Wood | Sawdust |

| Shavings | |

| Flakes | |

| Chips | |

| Bagasse | |

| Other Raw Materials |

By Application

| Furniture |

| Construction |

| Infrastructure |

| Packaging |

| Others |

By Geography

| United States |

| Canada |

| Mexico |

| By Raw Material | Wood | Sawdust |

| Shavings | ||

| Flakes | ||

| Chips | ||

| Bagasse | ||

| Other Raw Materials | ||

| By Application | Furniture | |

| Construction | ||

| Infrastructure | ||

| Packaging | ||

| Others | ||

| By Geography | United States | |

| Canada | ||

| Mexico |

Key Questions Answered in the Report

What is the projected volume for particle board demand in North America by 2031?

Consumption is expected to reach 19.69 million m³ by 2031, based on a 5.02% CAGR from 2026.

Which end-use segment will contribute most to incremental growth through 2031?

Furniture applications, driven by ready-to-assemble lines, will add the largest share, growing at a 5.45% CAGR.

How are state landfill-diversion mandates influencing raw-material costs?

Policies such as California’s SB 1383 are channeling demolition wood into furnish streams, reducing delivered costs for mills near urban centers.

Why is bagasse attracting interest from panel producers?

Sugarcane residues can meet ANSI A208.1 strength standards and are forecast as the fastest-growing feedstock at 5.38% CAGR, offering a hedge against sawmill-residue shortages.

How strict are current formaldehyde rules for particle board?

EPA limits emissions to 0.09 ppm and requires third-party certification, with California demanding even tighter testing frequencies.

What is the current value of the North America particle board market?

The North America particle board market size is expected to reach 15.41 million cubic meters by 2026.

Page last updated on: