Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.72 Billion |

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 9.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Particle Board Market Analysis by Mordor Intelligence

The India Particle Board Market size was valued at USD 0.72 billion in 2025 and estimated to grow from USD 0.79 billion in 2026 to reach USD 1.27 billion by 2031, at a CAGR of 9.98% during the forecast period (2026-2031). Current demand growth stems from urban housing starts, organized furniture retail, and export compliance pressures that reward quality upgrades. Regulatory milestones such as the February 2025 Bureau of Indian Standards (BIS) Quality Control Orders are accelerating the shift from a fragmented, price-sensitive supply base toward a consolidated, technology-driven ecosystem[1]Bureau of Indian Standards, “Quality Control Orders for Wood-Based Boards,” dpiit.gov.in . Government incentives, including the Production Linked Incentive (PLI) scheme for furniture components, reinforce capital spending on capacity additions that embed AI-enabled automation and emission-controlled resin technologies. Large producers are front-loading investments to pre-empt the BIS deadline, while medium-scale firms are pivoting to waste-based feedstocks to protect margins from imported log price swings. Export opportunities tied to CARB Phase 2 and EN 120 formaldehyde limits have created a dual-market strategy.

Key Report Takeaways

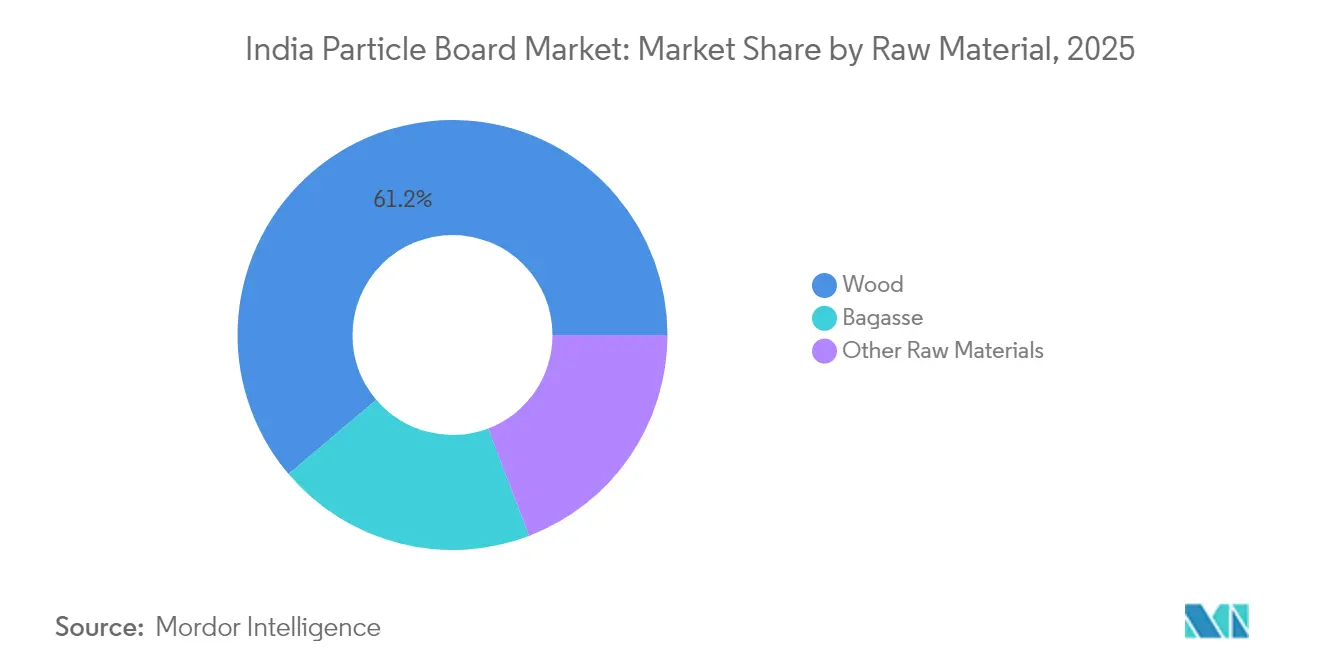

- By raw material, wood commanded 61.20% of India particle board market share in 2025, whereas bagasse is forecast to accelerate at a 12.32% CAGR through 2031.

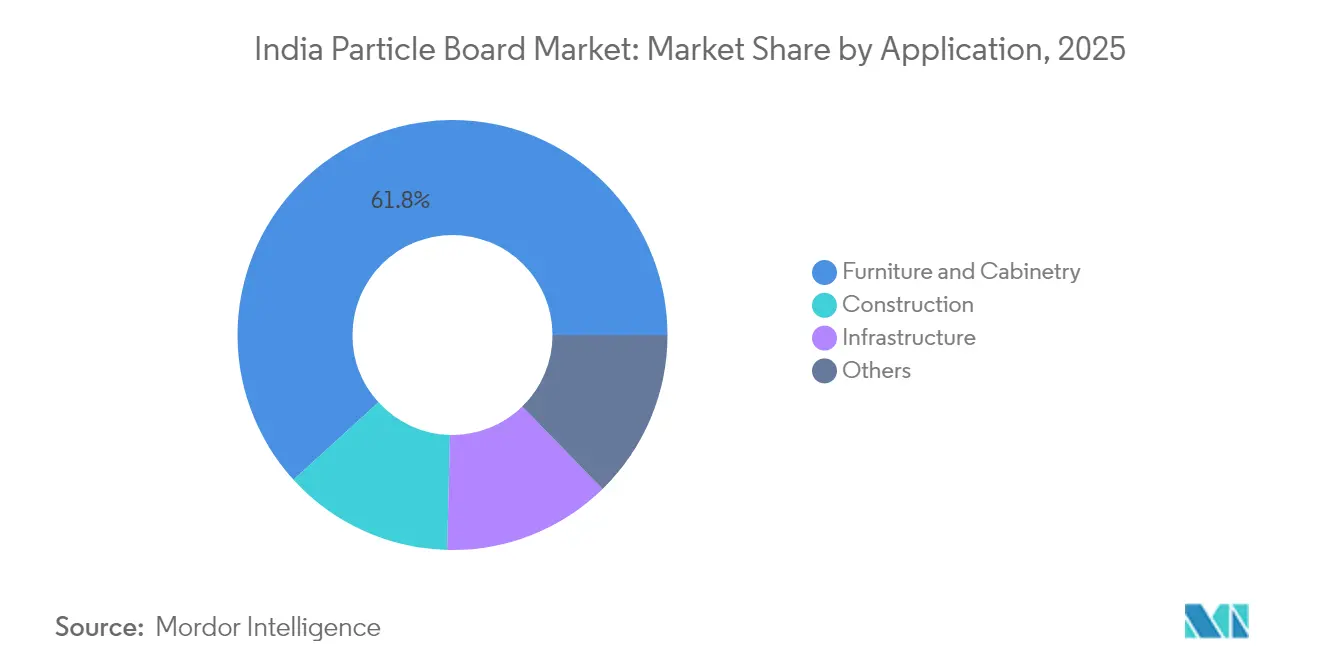

- By application, furniture and cabinetry accounted for 61.75% of the India particle board market size in 2025 and is expected to expand at an 11.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Particle Board Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising office, hospitality and retail furniture demand | +2.8% | National, with concentration in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Urban-housing push and smart-city projects | +2.1% | 100 smart cities and major urban agglomerations | Long term (≥ 4 years) |

| Government PLI incentives for furniture components | +1.9% | Manufacturing clusters in Gujarat, Maharashtra, Tamil Nadu | Short term (≤ 2 years) |

| EU/US low-emission export opportunity | +1.7% | Export-oriented manufacturing hubs | Medium term (2-4 years) |

| AI-enabled panel-line automation cuts unit cost | +1.2% | Large-scale manufacturing facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Office, Hospitality, and Retail Furniture Demand

Commercial refurbishment cycles have shortened as enterprises adopt modular workstations that rely on standardized board dimensions, ensuring steady call-offs from panel suppliers. Hospitality chains replacing custom millwork with easily replaceable particle board (chip board) fixtures now place multi-year blanket orders that stabilize factory throughput. Organized retail is scaling ready-to-assemble furniture lines whose flat-pack logistics favor particle board over plywood because of weight and cost advantages. E-commerce sellers bundle fittings and fasteners with pre-laminated panels to serve budget-conscious consumers, deepening consumption in Tier-2 growth corridors. Corporate occupiers migrating to secondary cities extend this driver beyond traditional metropolitan catchments.

Urban-Housing Push and Smart-City Projects

Smart-city spending packages interior fit-outs for public transit stations, administrative offices, and community centers into the civil works budget, adding a non-cyclical layer of demand for certified boards. Affordable-housing schemes under PMAY integrate modular kitchens that specify E1-grade particle board, linking social policy with industrial growth. Industrial corridor nodes blend residential and commercial real-estate approvals, creating contiguous demand pools for board-based cabinetry. Green-building scorecards increasingly reward low-emission engineered wood, allowing compliant producers to bid at premium prices. The pipeline of 12 new industrial nodes sustains long-range order visibility that justifies new continuous-press lines.

Government PLI Incentives for Furniture Components

PLI rebates covering up to 8% of incremental sales encourage furniture exporters to lock in domestic panel suppliers that satisfy ISO and FSC chain-of-custody requirements, thereby reducing reliance on Southeast Asian imports. Long-term offtake contracts arising from PLI awards have shortened payback periods for new presses to under four years, catalyzing green-field plants in Tamil Nadu and Maharashtra. Board makers are collaborating with downstream assemblers to co-design low-waste panel sizes. Regional governments layer additional land and power subsidies, concentrating capacities in designated clusters where logistics infrastructure already exists. This confluence of fiscal incentives and guaranteed demand expedites the scaling of export-grade production lots.

EU/US Low-Emission Export Opportunity

Formaldehyde emission caps of 0.05 ppm under CARB Phase 2 align with India’s limits, enabling dual-certified plants to serve domestic and overseas buyers without parallel SKUs. Export premiums shield margins from domestic price volatility and finance the installation of melamine-urea-formaldehyde blends that cut emissions by 40%. U.S. home-improvement chains source private-label particle board furniture exclusively from compliant facilities, opening multi-container monthly lanes for qualified Indian producers. European distributors require third-party audits, compelling suppliers to digitize traceability all the way to plantation forests, which in turn raises the entry bar for non-compliant mills. As emission ceilings in key markets tighten, early movers could lock in share before late adopters upgrade equipment.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MDF cannibalisation in premium cabinets | -1.8% | Urban markets with higher disposable income | Medium term (2-4 years) |

| Volatile imported log and resin prices | -2.3% | National, affecting import-dependent manufacturers | Short term (≤ 2 years) |

| Tightening global formaldehyde limits | -1.1% | Export-oriented and premium domestic segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MDF Cannibalisation in Premium Cabinets

MDF’s finer fiber matrix yields crisper routed edges that premium kitchen makers prefer for shaker-style doors, leading to a share shift at the cabinetry market's upper end. Urban consumers tolerate a 15-20% price uplift when the perceived quality jump aligns with rising disposable incomes. Particle board suppliers respond with higher-density grades and improved surface sanding to shrink the aesthetic gap, while staying 8-10% below MDF on delivered cost. Moisture-prone zones such as under-sink panels remain MDF strongholds, but board makers accelerate research and development on hydrophobic additives to claw back share. Cannibalisation, therefore, remains contained to premium SKUs rather than mass-market furniture.

Volatile Imported Log and Resin Prices

Hardwood log imports priced in EUR expose mills to currency swings that can inflate landed cost by up to 12% within a quarter. Resin inputs linked to global crude benchmarks push glue cost swings onto margins that smaller mills cannot hedge. CITES restrictions on specific hardwood species force abrupt sourcing shifts that disrupt chip geometry and press calibrations. Some producers offset volatility by ramping bagasse content, yet seasonal availability necessitates inventory buffers that tie up working capital. Larger producers negotiate annual resin contracts and diversify feedstock through recycled wood streams, but smaller units face squeeze-outs during price spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Wood Dominance Faces Sustainability Pressure

Wood-based feedstocks retained 61.20% of India particle board market share in 2025, anchoring process yields through centuries-old sawmill linkages that guarantee chip consistency. However, climate commitments and biomass incentives propel bagasse to a 12.32% CAGR, outpacing all other materials and narrowing wood’s hegemony each successive year. The India particle board market size attributable to bagasse could grow purely on the back of sugar-mill waste monetization once planned storage silos and dryers come online. Simultaneously, recycled wood chips from construction debris enter the mix, providing feedstock hedges against imported log shortages.

Bagasse-centric plants compile carbon-credit dossiers to monetize greenhouse-gas offsets, adding a supplementary revenue stream that cushions price cycles. University trials demonstrate comparable rupture and internal-bond strength modulus between bagasse and eucalyptus boards when press parameters are optimized, nullifying earlier quality concerns. Several western-India mills have committed capex for dedicated depithing and cleaning units, anticipating preferential procurement from green-label furniture exporters. As BIS audit teams expand post-2025, feedstock traceability standards will favor mills with digitized bagasse procurement records.

By Application: Furniture Leadership Drives Market Evolution

Furniture and cabinetry absorbed 61.75% of the India particle board market in 2025, driven by organized retail and e-commerce bundles that embed ready-to-assemble concepts into urban lifestyles. This application segment is forecast to grow at a 11.52% CAGR through 2031. Construction fix-outs, such as drywall backing and mezzanine flooring, deliver year-round offtake that stabilizes mill utilization when furniture orders dip seasonally. Infrastructure interiors for rail terminals and civic buildings represent a pipeline that widens geographic penetration beyond major metros.

Furniture makers increasingly demand pre-laminated E1-grade panels that speed assembly and reduce downstream lamination labor, compelling board suppliers to integrate short-cycle press lines. Online brands co-design knock-down formats with panel producers to minimize waste across the nesting layout. Though price sensitive, construction panels offer lower defect tolerances, pushing mills to install in-line sanding and defect-mapping scanners that simultaneously raise overall plant yields. As smart-city tenders stipulate low-formaldehyde surfaces, infrastructure applications will effectively mirror the quality threshold set by export furniture.

Geography Analysis

Western and southern clusters anchor most of India's particle board market output. Tamil Nadu’s share is rising after a USD 662 million integrated complex came online, adding 320,000 m³ of annual capacity and reinforcing the state’s position as a gateway for export consignments moving through Chennai and Tuticorin ports. Maharashtra plants leverage Mumbai’s port to access imported pine logs while maintaining just-in-time deliveries to Pune’s fast-growing modular kitchen assemblers.

Northern units around Haryana and Punjab draw on poplar plantations and recycled demolition wood, catering to Delhi-NCR’s refurb market and supplying decorative pre-lam boards to local OEMs. These plants often serve as feeders to export container consolidation yards in Nhava Sheva, ensuring backward integration with laminated surface printers. Eastern and northeastern states present untapped bamboo and agro-waste reserves, yet infrastructure gaps limit scale efficiencies; pilot lines funded under viability-gap grants aim to address this over the next two years. Therefore, the India particle board (chip board) market is evolving toward a multi-hub configuration that balances raw-material concentration with end-use proximity.

The government’s industrial corridor program will add 12 new nodes, unlocking land parcels with pre-approved environmental clearances that cut permitting times to under six months. Mills sited in these nodes can co-locate with furniture exporters, reducing freight cost and turnaround, thereby positioning themselves for PLI incentives. State-level power subsidies differ widely, giving plants in renewable-rich Gujarat and Tamil Nadu a 50-70 basis-point energy-cost edge over coal-dependent regions. As BIS inspectors scale operations, compliance scores skew higher in established hubs, making location choice a strategic bet on future regulatory enforcement intensity.

Competitive Landscape

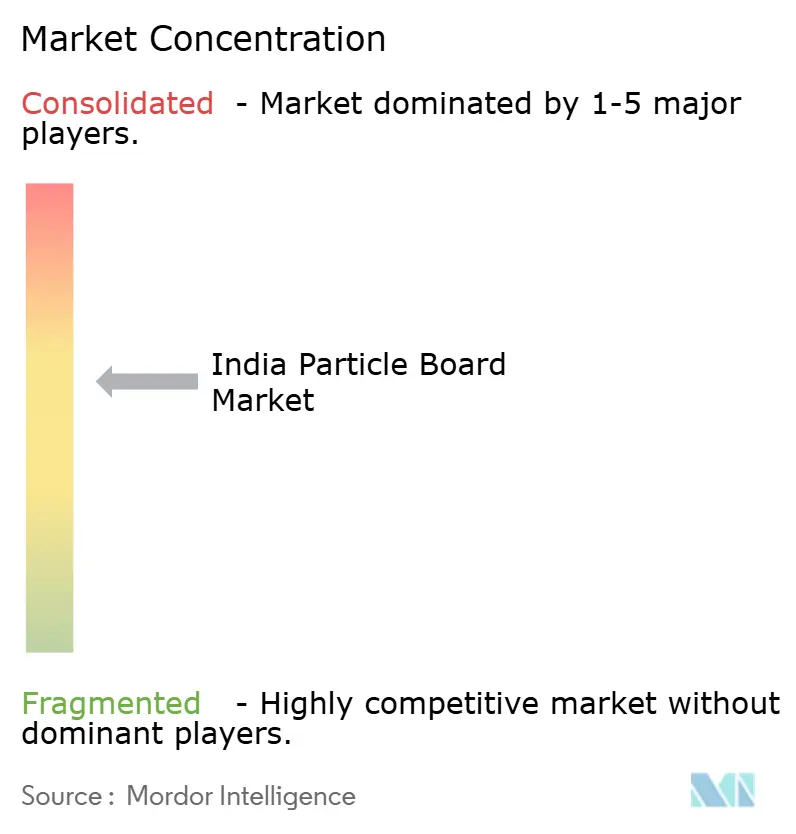

The India Particle Board Market is moderately consolidated. Strategic capex trends reveal a pivot toward integrated complexes combining MDF and particle board under one roof, allowing feedstock flexibility depending on market spreads. Sustainability certifications—from FSC chain-of-custody to EPD declarations—serve as differentiators in export tenders, prompting midsize firms to invest in audit readiness. Meanwhile, niche entrants target moisture-resistant and fire-retardant grades where regulatory mandates create protected segments. Competition is shifting from price wars to compliance, service reliability, and innovation in low-emission chemistries.

India Particle Board Industry Leaders

CenturyPly (Century Prowud)

Shirdi Panel Industries Ltd.(ASIS)

Action TESA

Merino Industries

Associate Décor Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CenturyPly commissioned a particle board manufacturing plant at Therovy Kandigai near Chennai, Tamil Nadu, with a daily capacity of 800 cubic meters. This facility is designed to meet rising domestic and export demand for engineered wood panels.

- May 2024: Action TESA launched MOIST-MASTER, a high moisture-resistant particle board designed for durability in humid and coastal environments. With a density of more than 700, it offers borer and termite resistance and low formaldehyde emissions.

India Particle Board Market Report Scope

Particle board, also known as fiberboard, is an engineered material made of separate fibers. Fiberboards are generally made of engineered wood, either hard or softwood. The wood is mixed with wax and resin binders by applying high pressure and temperature. The Indian particle board market is segmented by raw materials and applications. By raw material, the market is segmented into wood, bagasse, and other raw materials. By applications, the market is segmented into construction, furniture, infrastructure, and other applications. For each segment, the market sizing and forecasts have been done based on value (USD million).

By Raw Material

| Wood | Sawdust |

| Shavings | |

| Flakes | |

| Chips | |

| Bagasse | |

| Other Raw Materials |

By Application

| Furniture and Cabinetry |

| Construction |

| Infrastructure |

| Others |

| By Raw Material | Wood | Sawdust |

| Shavings | ||

| Flakes | ||

| Chips | ||

| Bagasse | ||

| Other Raw Materials | ||

| By Application | Furniture and Cabinetry | |

| Construction | ||

| Infrastructure | ||

| Others |

Key Questions Answered in the Report

What is the current value of the India particle board market?

The India particle board market reached USD 0.79 billion in 2026 and is projected to reach USD 1.27 billion by 2031.

How fast is demand expected to grow over the forecast horizon?

The market is forecast to post a 9.98% CAGR from 2026-2031, driven by urban housing, organized furniture retail, and export compliance premiums.

Which raw material segment is expanding the quickest?

Bagasse-based boards are growing at a 12.32% CAGR as sugar-mill waste monetization and sustainability incentives gain traction.

Why are BIS Quality Control Orders significant for manufacturers?

The February 2025 BIS mandate requires compliance licenses, effectively phasing out non-compliant mills and accelerating industry consolidation.

How do export regulations influence domestic production standards?

Alignment with CARB Phase 2 and EN 120 formaldehyde limits enables dual-compliant plants to earn 25-30% price premiums in EU and U.S. markets, prompting industry-wide upgrades.

Which regions dominate manufacturing capacity?

Gujarat, Maharashtra, and Tamil Nadu collectively host more than 70% of capacity owing to raw-material proximity, port access, and supportive state policies.

Page last updated on: