Market Overview

| Study Period | 2020 - 2031 |

|---|---|

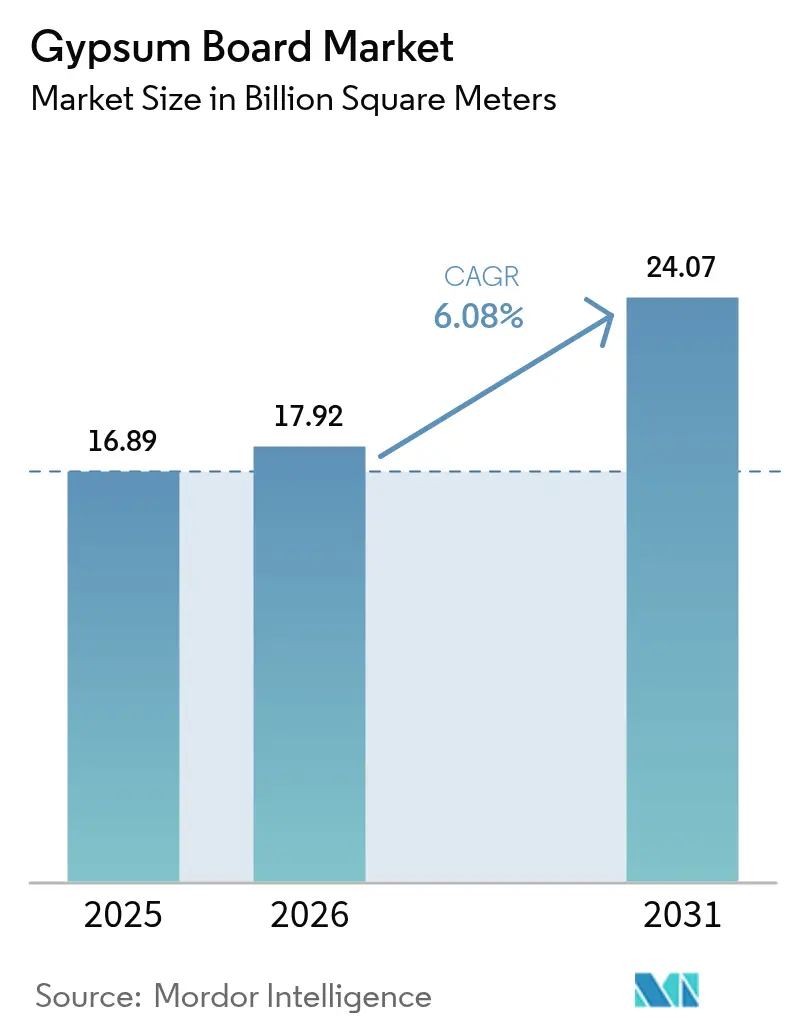

| Market Volume (2026) | 17.92 Billion square meters |

| Market Volume (2031) | 24.07 Billion square meters |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gypsum Board Market Analysis by Mordor Intelligence

Gypsum Board Market size in 2026 is estimated at 17.92 Billion square meters, growing from 2025 value of 16.89 Billion square meters with 2031 projections showing 24.07 Billion square meters, growing at 6.08% CAGR over 2026-2031. Ongoing fire-safety and energy-efficiency mandates anchor demand, while Asia-Pacific’s construction boom, chronic housing shortages in North America, and tightening embodied-carbon rules in Europe shape the competitive field. Capacity expansion projects in Texas and Montreal illustrate how producers balance cost discipline with sustainability investments. Meanwhile, the shift toward lightweight and pre-decorated solutions helps contractors mitigate labor shortages, and recycled or synthetic feedstocks gain strategic importance as coal-powered electricity retires faster than expected. Fiber-cement’s encroachment in wet areas keeps pricing rational, yet broad infrastructure renewal programs continue to backstop volume growth across the gypsum board market.

Key Report Takeaways

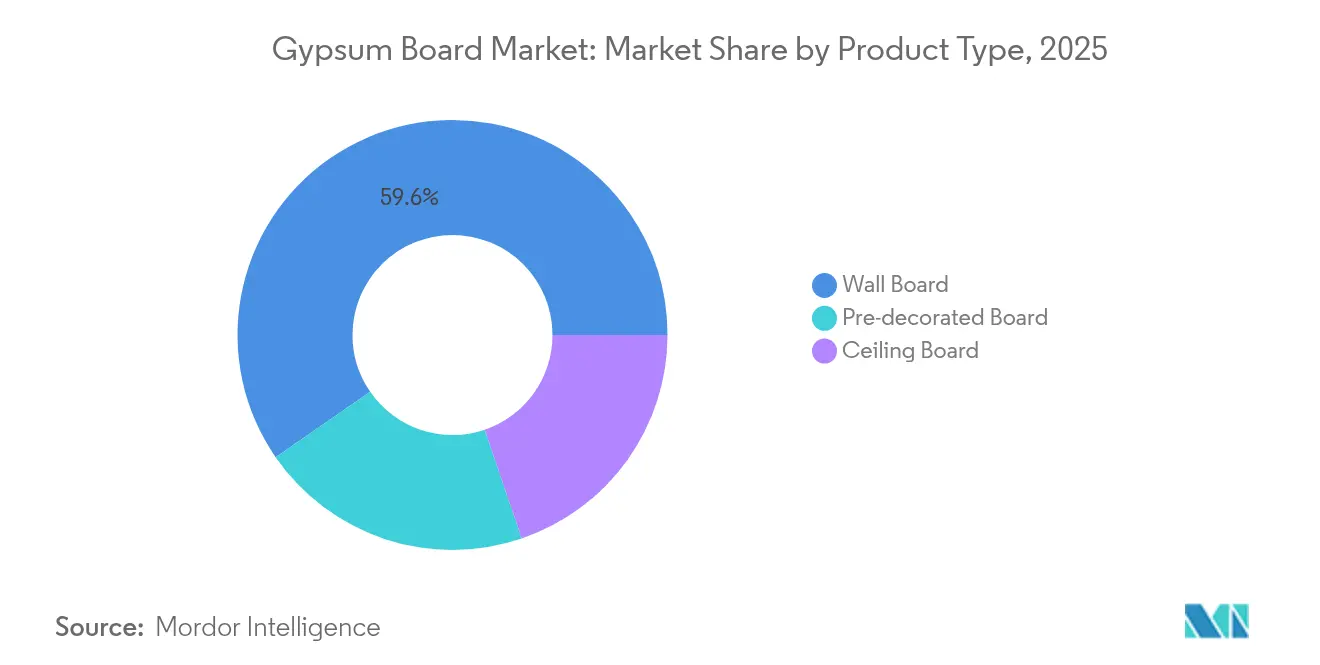

- By product type, wall board led with 59.62% of gypsum board market share in 2025, while pre-decorated board is projected to record a 7.39% CAGR to 2031.

- By raw material, natural gypsum accounted for 69.55% share of the gypsum board market size in 2025, whereas synthetic FGD gypsum is set to expand at 6.78% CAGR through 2031.

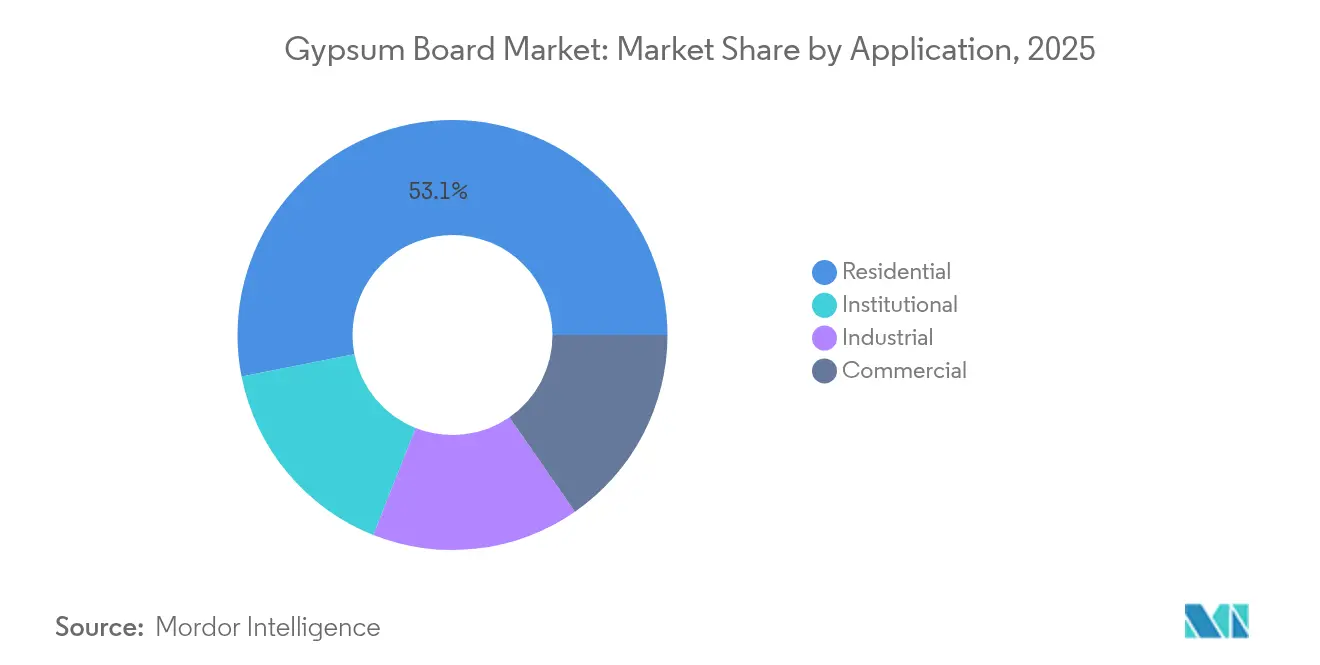

- By application, residential construction captured 53.10% share of the gypsum board market size in 2025; institutional projects are advancing at a 7.08% CAGR between 2026 and 2031.

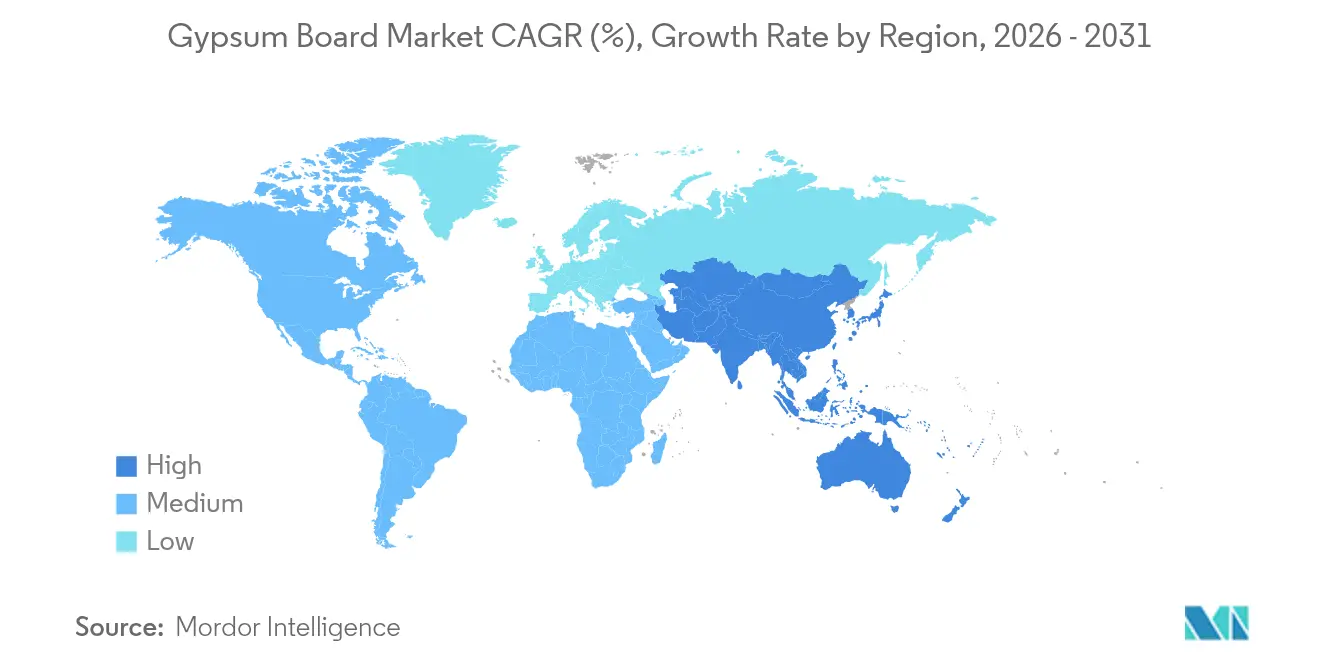

- By geography, Asia-Pacific dominated with 46.10% gypsum board market share in 2025 and is forecast to grow at 7.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gypsum Board Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging residential construction in APAC | +2.1% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Accelerating renovation and remodeling wave in mature markets | +1.8% | North America and Europe | Short term (≤ 2 years) |

| Shift toward lightweight and high-strength drywall solutions | +1.2% | Global | Long term (≥ 4 years) |

| Government incentives for fire-, sound- and energy-efficient buildings | +1.0% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Cost-advantaged synthetic (FGD) gypsum availability | +0.9% | North America core, limited EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Residential Construction in APAC

Rapid urban migration pushes developers toward high-density housing, and gypsum board systems help shorten interior fit-out cycles compared with wet plaster. Although China’s overall cement output fell 10% in 2024, wallboard volumes remained resilient because developers focused on accelerating finishing work to unlock cash flows. India’s government-backed housing schemes add steady baseline demand, while Southeast Asian megaprojects specify gypsum for its proven fire resistance in schools and transit hubs. Labor shortages across the region strengthen the appeal of factory-finished boards that reduce on-site trades.

Accelerating Renovation and Remodeling Wave in Mature Markets

Renovation outlays in the United States climbed to USD 509 billion in 2025, reversing two years of contraction. Forty percent of U.S. dwellings pre-date 1970, so wall replacements align with tighter fire and insulation codes, directly lifting gypsum demand. Homeowners spent an average USD 4,700 on interior upgrades, with mold- and moisture-resistant boards ranking high on shopping lists. Similar retrofit mandates in the EU catalyze orders for high-performance panels that combine thermal and acoustic gains. These dynamics sustain a stable volume base for the gypsum board market during economic slowdowns.

Shift Toward Lightweight and High-Strength Drywall Solutions

Eighty percent of global contractors report skilled-labor gaps, making board weight reduction a productivity lever. New formulations shave 20-30% off panel mass, easing handling while maintaining fire ratings. Glass-fiber-reinforced boards rated for over two-hour exposure extend use cases where Type X products once sufficed. Integration with mass-timber builds also reduces overall embodied carbon by up to 75% compared with conventional concrete toppings[1]USG, “Gypsum Concrete in Mass Timber Construction,” usg.com. Research and development pipelines thus prioritize lighter yet stronger offerings that reposition the gypsum board market for evolving construction techniques.

Government Incentives for Fire, Sound, and Energy-Efficient Buildings

Federal P100 standards dictate stringent interior system performance for all U.S. civilian properties and spur adoption of specialty boards meeting specified fire and acoustic thresholds. California’s AB-2446 targets a 40% cut in building-material carbon intensity by 2035, which encourages low-carbon gypsum innovations. Similar policies in France under RE2020 tighten every three years and further elevate the value proposition for CarbonLow and similar lines. As incentives spread to Asia-Pacific, specification writers increasingly view gypsum as a multipurpose solution, broadening the gypsum board market’s institutional footprint.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural gypsum and energy prices | -1.4% | Global, acute in energy-intensive regions | Short term (≤ 2 years) |

| Rising penetration of fibre-cement and other panel alternatives | -0.8% | North America and APAC, limited EU | Medium term (2-4 years) |

| Carbon-neutral mandates raising embodied-carbon scrutiny | -0.6% | EU core, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural Gypsum and Energy Prices

Mined gypsum output touched 22 million tons in the United States during 2024, but unit costs varied widely by mine depth and haulage distance. Calcination relies heavily on natural gas, making board pricing sensitive to fuel swings. As decommissioning of coal plants removes synthetic supply, mills draw from deposits located farther afield, inflating freight bills and amplifying cost risk[2]U.S. Geological Survey, “Mineral Commodity Summaries 2025: Gypsum,” pubs.usgs.gov. Energy-efficient kilns and regional warehouse hubs partly soften the blow, yet input volatility still trims the gypsum board market growth trajectory in the near term.

Rising Penetration of Fibre-Cement and Other Panel Alternatives

Impact- and water-resistant boards are now marketed with fire ratings comparable to gypsum, eroding one of gypsum’s historic competitive moats. Healthcare and education projects increasingly specify hybrid wall assemblies, prompting gypsum suppliers to accelerate product differentiation strategies. Although substitution remains a minority threat, it nevertheless subtracts from the gypsum board market’s mid-term momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wall Board Dominance Faces Pre-Decorated Disruption

Wall board retained 59.62% gypsum board market share in 2025, sustained by universal acceptance in residential interiors where cost and code compliance drive specification. Pre-decorated panels, however, are forecast to post 7.39% CAGR to 2031, a speed more than one percentage point above the overall gypsum board market.

Premium segments now favor mold-, moisture- or impact-modified boards such as PURPLE XP, priced at a 20-30% uplift over generic Type X, yet often selected for kitchens, baths, and healthcare corridors where downtime is costly. Manufacturers bundle these attributes with factory coatings to seize higher-margin value capture. As contractors increasingly pursue “paint-ready” delivery, pre-decorated formats are poised to widen their share within the gypsum board market.

By Raw Material: Natural Gypsum Leadership Challenged by Synthetic Transition

Natural rock contributed 69.55% of feedstock to the gypsum board market size in 2025, yet reliant producers confront exposure to ore-grade variability and diesel logistics costs. Synthetic FGD gypsum, although set back by coal-plant retirements, is still forecast to grow at 6.78% CAGR as mills retrofit for broader feed compatibility and as regulators recognize its recycling benefits.

Moving forward, blended recipes of mined, synthetic, and recycled fines should stabilize input risk profiles while supporting the gypsum board market’s circular-economy credentials.

By Application: Residential Scale Contrasts with Institutional Growth Dynamics

Residential remodeling and new-home builds absorbed 53.10% of 2025 volume, confirming the segment’s anchor role inside the gypsum board market. Yet institutional buildings, schools, hospitals, and civic centers, are projected to expand fastest at 7.08% CAGR as code writers elevate fire and acoustic baselines for occupant safety.

Institutional specifications increasingly bundle low-embodied carbon with 1- or 2-hour fire separation, steering demand toward specialty boards and thereby lifting average selling prices. Meanwhile, commercial office starts soft-pedal yet data-center and healthcare builds offset much of the slack, maintaining a diverse end-use profile that underpins the gypsum board market during economic cycles.

Geography Analysis

Asia-Pacific claimed 46.10% of 2025 shipments, thanks to China’s massive real-estate backlog and India’s Housing for All program. Regional growth at 7.31% CAGR through 2031 ensures the gypsum board market remains volume-weighted to this geography despite political and credit risk clouds.

North America embodies renovation-driven steadiness. Europe’s pathway is more regulation-led, as RE2020 and similar frameworks reinforce demand for carbon-optimized designs despite slower macro indicators. Together, the three regions shape the competitive map, while South America, and Middle-East and Africa remain opportunity frontiers where lower per-capita penetration leaves headroom for future gypsum board market growth.

Manufacturers differentiate through environmental product declarations, often bundling recycled content to meet tender prerequisites. Although construction output is flatter than Asia-Pacific, premium ESG-minded pricing offsets slower unit growth, safeguarding revenue expansion inside the gypsum board market.

Competitive Landscape

The gypsum board market exhibits high consolidation. Strategic pivots emphasize product differentiation over price cuts. Saint-Gobain markets CarbonLow with up to 60% less embodied carbon, targeting projects subject to green-building credits. Technology uptake extends to logistics and recycling. Automated guided vehicles inside plants cut handling costs, while pilot facilities in Germany and the United States process site scraps into feedstock, reducing landfill fees and supporting ESG disclosures. Competitive intensity thus hinges on who commercializes sustainable solutions at scale fastest, as price wars remain limited by high capital barriers and freight sensitivities that localize supply.

Gypsum Board Industry Leaders

BNBM

Etex Group

Georgia-Pacific Gypsum LLC

Knauf Group

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Saint-Gobain Canada announced CarbonLow, a gypsum wallboard line with up to 60% less embodied carbon, slated for production at North America’s first zero-carbon gypsum facility near Montreal.

- June 2024: USG a subsidiary of Knauf, commenced gypsum production at its new Avery Quarry in Iosco County, Michigan, targeting 550,000 tons in 2025 to offset declining synthetic supply.

Global Gypsum Board Market Report Scope

Gypsum board, also known as drywall or plasterboard, is a building material composed of gypsum core sandwiched between paper facings. It is commonly used for interior wall and ceiling construction in residential, commercial, and institutional buildings. Gypsum boards are available in various thicknesses and sizes to suit different applications and construction requirements. They provide a smooth and durable surface for painting, wallpapering, or decorative finishes.

The gypsum board market is segmented by type, application, and geography. By type, the market is segmented into wallboard, ceiling board, and pre-decorated board. By application, the market is segmented into the residential, institutional, industrial, and commercial sectors. The report also covers the market sizes and forecasts for the gypsum board market in 27 countries across major regions. For each segment, the market sizes and forecasts are provided in terms of volume (million square meters).

By Product Type

| Wall Board |

| Ceiling Board |

| Pre-decorated Board |

By Raw Material

| Natural Gypsum |

| Synthetic (FGD) Gypsum |

| Recycled Gypsum |

By Application

| Residential |

| Commercial |

| Institutional |

| Industrial |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Malaysia | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Qatar | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Wall Board | |

| Ceiling Board | ||

| Pre-decorated Board | ||

| By Raw Material | Natural Gypsum | |

| Synthetic (FGD) Gypsum | ||

| Recycled Gypsum | ||

| By Application | Residential | |

| Commercial | ||

| Institutional | ||

| Industrial | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Malaysia | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Turkey | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Qatar | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the gypsum board market?

The gypsum board market size reached 17.92 billion m² in 2026 and is projected to climb to 24.07 billion m² by 2031.

Which region leads the gypsum board market?

Asia-Pacific dominates with 46.10% share in 2025 and is expected to post the fastest 7.31% CAGR to 2031.

Which product segment is growing fastest?

Pre-decorated gypsum board is forecast to expand at 7.39% CAGR, outpacing traditional wall board growth.

How are sustainability mandates influencing gypsum board demand?

Embodied-carbon regulations such as California’s AB-2446 and France’s RE2020 spur demand for low-carbon boards like Saint-Gobain’s CarbonLow, shifting specifications toward greener products.

What is the biggest restraint on gypsum board market growth?

Volatile energy and raw-gypsum costs reduce producer margins and can slow capacity additions, trimming near-term growth prospects.

Page last updated on: