Cement Board Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

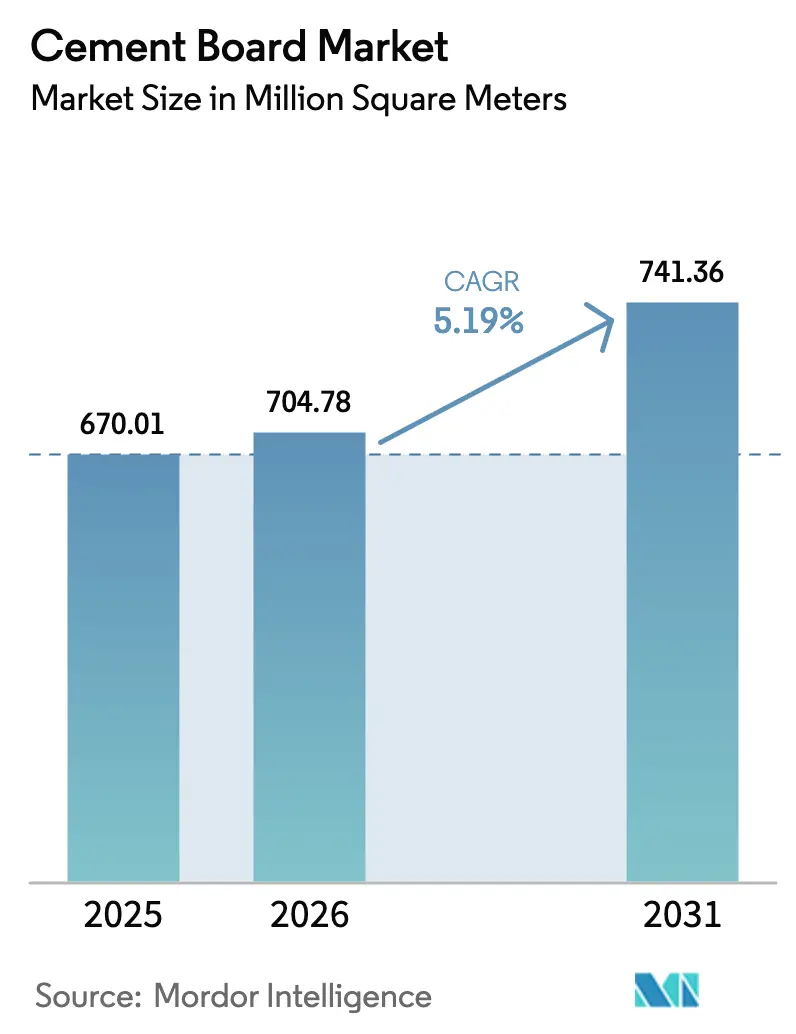

| Market Volume (2026) | 704.78 Million square meters |

| Market Volume (2031) | 741.36 Million square meters |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

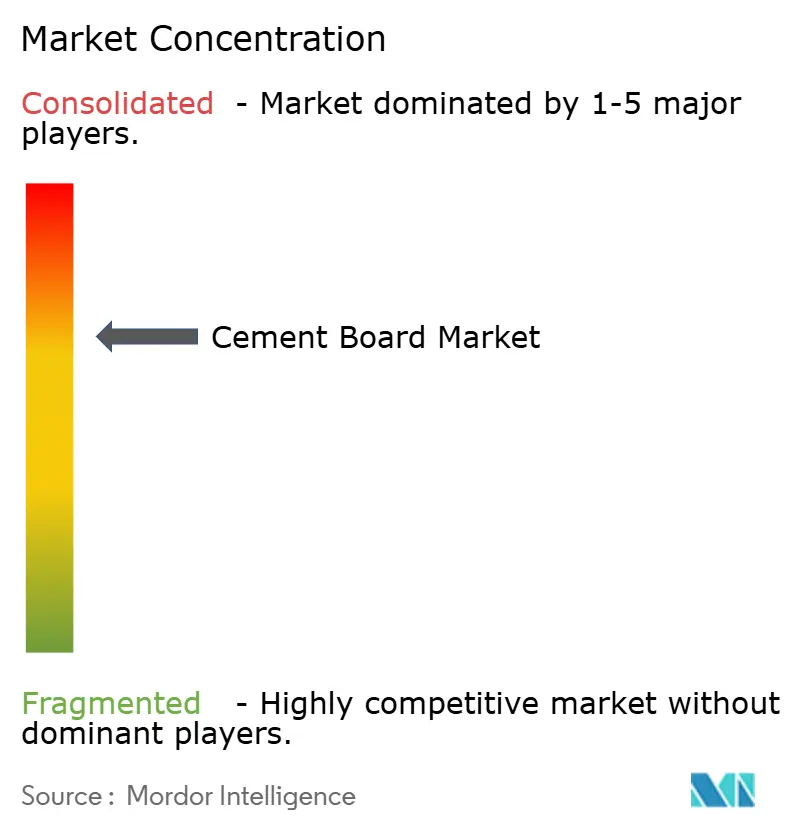

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cement Board Market Analysis by Mordor Intelligence

The Cement Board Market size is projected to expand from 670.01 Million square meters in 2025 and 704.78 Million square meters in 2026 to 741.36 Million square meters by 2031, registering a CAGR of 5.19% between 2026 to 2031. This growth reflects rising demand for non-combustible, moisture-resistant panels that comply with ever-stricter fire-safety and environmental rules. Developers are adopting factory-cut boards that speed installation, curb labor hours, and reduce embodied carbon. Insurance incentives in wildfire-prone regions, stricter bans on asbestos, and rapid uptake of modular building systems reinforce long-term volume expansion. Leading suppliers continue to refine autoclaving, blended-cement binders, and digital process controls to offset energy inflation and carbon levies while protecting margins.

Key Report Takeaways

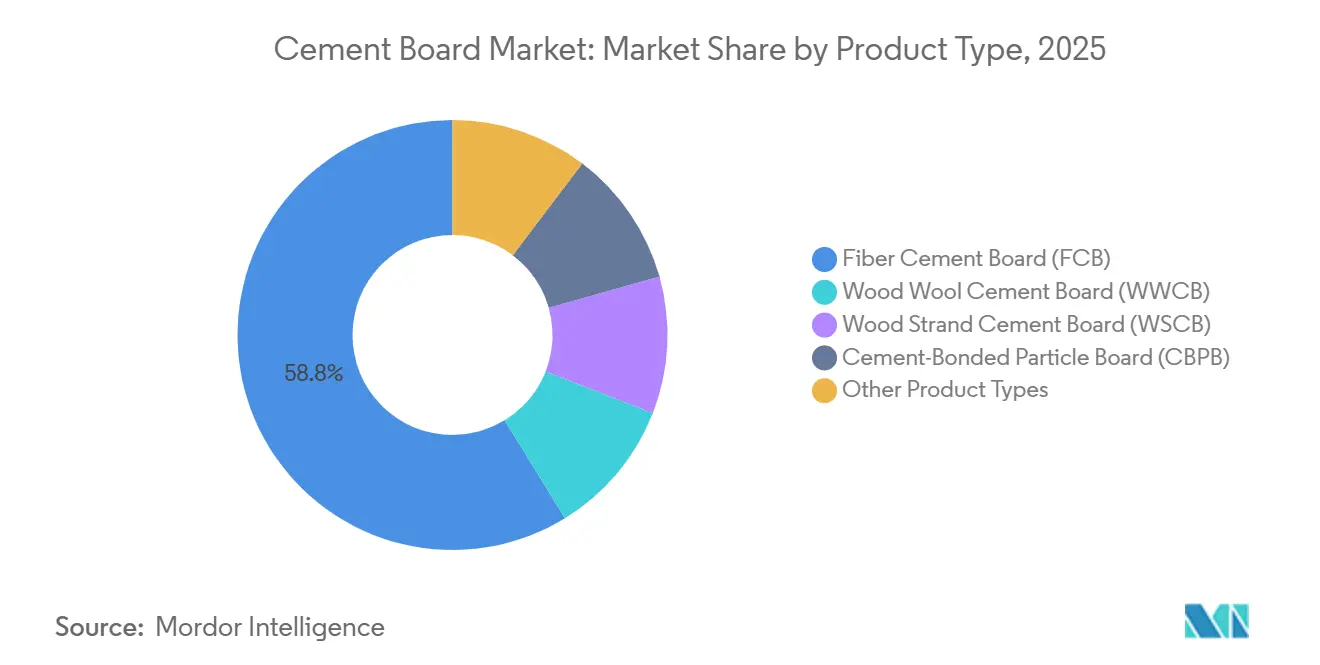

- By product type, Fiber Cement Board commanded 58.76% of the cement board market share in 2025. Other product types, such as Magnesium Oxide Cement Board (MOCB) and Rice Husk Cement Board, are forecast to advance at a 5.56% CAGR through 2031.

- By application, exterior and partition walls held 37.10% of the cement board market size in 2025; other applications, such as prefabricated and fire-resistant assemblies, are set to grow at a 5.79% CAGR to 2031.

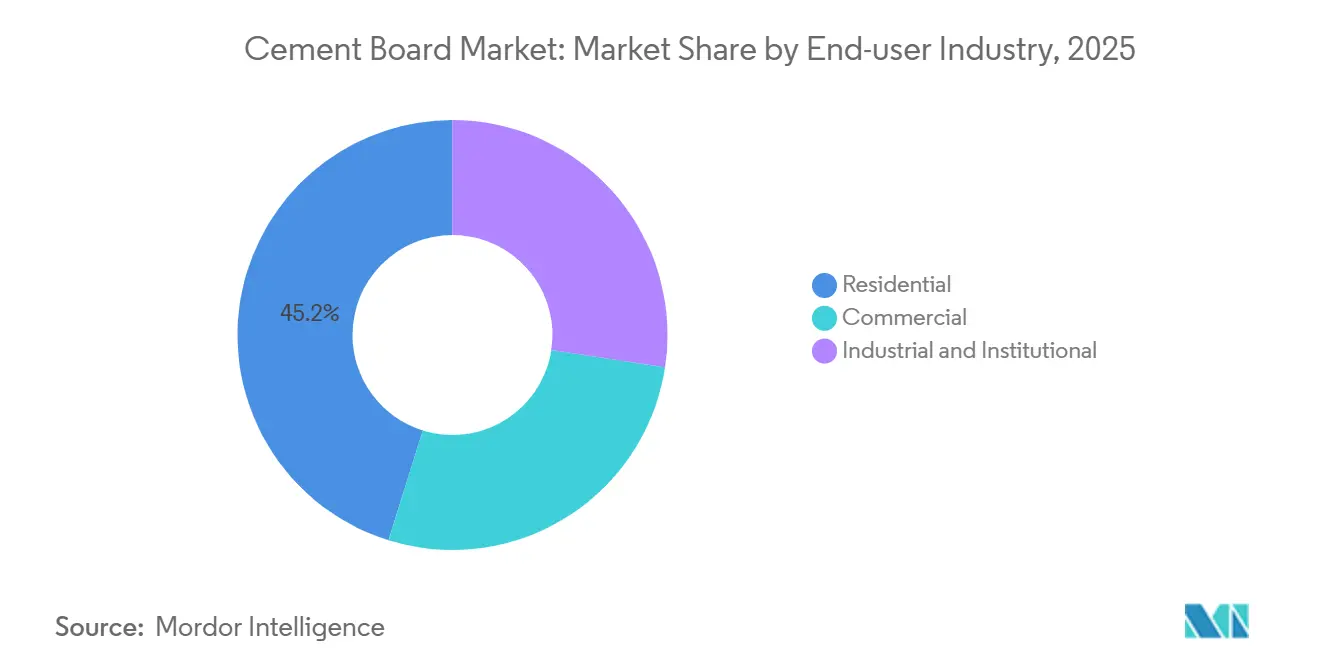

- By end-user, residential projects represented 45.19% of 2025 consumption, while industrial and institutional segments are expected to post a 5.66% CAGR through 2031.

- By geography, Asia-Pacific accounted for 44.07% of the 2025 volume, with regional demand expanding at a 5.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cement Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption in residential and commercial construction | +1.4% | Global, high in Asia-Pacific & North America | Medium term (2-4 years) |

| Mandatory green-building codes favoring non-asbestos boards | +1.2% | North America, EU, Australia, select APAC cities | Long term (≥4 years) |

| Demand for durable, impact-resistant interior panels | +0.9% | Global, especially high-rise & institutional | Medium term (2-4 years) |

| Uptake in off-site volumetric modular buildings | +0.8% | North America, Northern Europe, Japan | Medium term (2-4 years) |

| Wildfire insurance discounts for fire-rated cladding | +0.6% | California, Australia, Mediterranean Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption in Residential and Commercial Construction

Tighter building codes and labor shortages make cement board a preferred substrate in both housing and non-residential work. California’s 2024 CALGreen update requires Environmental Product Declarations for exterior cladding, disqualifying vinyl options and pushing contractors toward fiber cement[1]California Building Standards Commission, “CALGreen Code 2024,” cbsc.ca.gov. India added 450 million ft² of residential floor area in 2025, much of it using cement board soffits and stairwell liners to meet 90-minute fire-rating rules. Commercial retrofits in Singapore and Hong Kong now swap gypsum for 12 mm boards to achieve Green Mark Platinum impact-resistance targets. On-site crews can fasten pre-scored panels 40% faster than wet plaster, trimming mid-rise schedules by two to three weeks.

Mandatory Green-Building Codes Favoring Non-Asbestos Boards

The European Union’s 2024 revision to the Construction Products Regulation mandates a Declaration of Performance confirming zero asbestos content, accelerating fiber cement uptake. Australia’s 2025 National Construction Code closed import loopholes that once allowed uncertified boards. New York City’s Local Law 97 caps façade embodied carbon, prompting developers to replace aluminum composites with cement board for a 35% footprint cut. Manufacturers holding ready EPD libraries and ISO 8336 fire-test data reach the market six to nine months sooner than new entrants.

Demand for Durable, Impact-Resistant Interior Panels

Hospitals in the United States now specify 9 mm boards for corridors because they resist gurney impacts and cut 10-year repair labor by USD 1,200 per 1,000 ft²[2]U.S. Geological Survey, “Mineral Commodity Summary: Gypsum 2026,” usgs.gov. Flexural strength of 12-18 MPa allows slimmer walls that reclaim floor area in towers. Cold-storage plants in Europe favor cement board to meet HACCP hygiene goals, since the material stays mold-free through freeze-thaw cycles. Data-center insurers limit premium surcharges to 5% when non-combustible partitions, such as fiber cement, protect cable trays.

Uptake in Off-Site Volumetric Modular Buildings

Factories in Pennsylvania and Ontario integrate 12 mm panels as both exterior sheathing and bathroom backer within one line, cutting on-site trades and logistics. Japan’s prefab leaders install ductile boards that withstand 0.4 g seismic loads under the Building Standard Law. United Kingdom guidance released in 2025 names fiber cement as preferred fire-safe cladding for new modular homes. Nested shipping of pre-cut boards lowers freight costs by 12% and reduces in-transit breakage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost versus gypsum and OSB | -0.7% | Global, price-sensitive housing | Short term (≤2 years) |

| Volatile cement & cellulose fiber prices / CO₂ levies | -0.5% | EU & North America | Medium term (2-4 years) |

| Limited end-of-life recycling infrastructure | -0.3% | EU, California, selected APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Initial Cost Versus Gypsum and OSB

Fiber cement panels retail at USD 18–24 in North America, 40-60% above Type X gypsum. The price gap widened after Portland-cement increases of 12% in 2025, whereas gypsum stayed flat. Labor adds cost because carbide blades and pre-drilling extend crew hours by 10-15%. Affordable-housing budgets in India and Southeast Asia often cap material spend, limiting near-term penetration despite lower life-cycle outlays.

Volatile Cement and Cellulose Fiber Prices / CO₂ Levies

Portland-cement spot prices swung 18-22% in 2025 as energy markets tightened. Softwood pulp, the chief cellulose input, spiked 18% after Canadian supply cuts. The EU’s Carbon Border Adjustment Mechanism adds EUR 80-100 per metric ton of embedded CO₂, inflating landed costs by up to 12%. California’s allowance price rose to USD 38 per ton in late 2025, adding USD 4-6 per m³ to in-state production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: FCB Maintains Lead as Autoclaving Scales

Fiber Cement Board captured 58.76% of 2025 volume, locking in its position through mature ASTM C1186-compliant lines. James Hardie’s autoclaved boards post 18-22 MPa flexural strength and ±0.3% dimensional tolerance, satisfying both cladding and structural-sheathing roles. Other product types, such as magnesium oxide and rice-husk variants, while costlier, are expanding at a 5.56% CAGR on superior chloride resistance that suits coastal builds. Within this mix, the cement board market size for high-performance FCB is projected to widen fastest in code-driven regions such as North America and the EU. Niche formats, wood wool, and strand boards serve acoustic ceilings, offering NRC values up to 0.75. Producers in India and Vietnam now substitute up to 40% cellulose with rice-husk fiber, lowering raw costs by USD 5 /m² without sacrificing Class A fire ratings.

Rice-husk and magnesium boards are poised to erode small shares from FCB in price-sensitive and specialty markets. However, the cement board market share of autoclaved FCB will remain dominant where seismic, fire, and warranty criteria override first-cost differences. Saudi Arabian marine projects, Japanese multifamily towers, and U.S. data centers all specify FCB for its verified performance envelope. Momentum also rests on well-documented EPD libraries that help builders meet embodied-carbon targets.

By Application: Prefabrication and Fire Assemblies Accelerate

Exterior and partition walls held 37.10% of application volume in 2025, reflecting decades of code compliance. Yet the cement board market size tied to prefabricated modules and fire-resistant enclosures is forecast to climb 5.79% annually. Factory assembly lines in North America mount 12 mm panels as both diaphragm and wet-area liner, trimming per-module material costs by USD 200. Data centers and pharmaceutical cleanrooms specify non-combustible skins that stay intact for 120 minutes under ISO 834 curves, an advantage that gypsum cannot match.

Floor-underlayment demand is climbing in commercial retrofits that lay large-format tile. Roofing use is a niche but expanding across Indonesia and the Philippines, where fiber cement’s thermal insulation curbs urban heat. Cladding finishes now mimic timber grain or stone, broadening aesthetic appeal for mid-rise façades. Overall, prefabrication’s time-saving economics and fire-safety needs help diversify the cement board market.

By End-User Industry: Institutional Projects Lead Growth

Residential builders consumed 45.19% of boards in 2025, but industrial and institutional buyers will log a 5.66% CAGR to 2031. A 10 MW data-center shell typically installs up to 12,000 m² of panels to satisfy insurer demands for non-combustible envelopes. Cold-storage warehouses and HACCP-regulated food plants favor cement board for moisture resistance and microbial neutrality. School districts and hospitals select the material for corridors where impact damage is common, reducing lifetime maintenance.

Commercial office retrofits adopt 12 mm panels to meet the International Building Code’s 90-minute corridor rating in Type IIB structures. Southeast Asian hotels clad kitchen and bath walls with fiber cement to qualify for local fire rules within 3 m of cooking appliances. Collectively, these specification-driven segments underpin the cement board market as regulations tighten and life-cycle cost takes precedence over upfront price.

Geography Analysis

Asia-Pacific dominated the cement board market with 44.07% of 2025 volume and is poised for a 5.42% CAGR. India’s PMAY program alone generated 18 million m² of demand in 2025 by mandating cyclone-resistant cladding in coastal states. Vietnam’s USD 36 billion FDI inflow into electronics parks drove penetration from 12% in 2023 to 22% in 2025. Japan’s prefab sector continues to install ductile fiber cement that withstands 0.4 g lateral loads.

In North America, California’s WUI code requires Class A cladding in hazard zones, adding 6 million m² of annual demand. HUD guidance in 2025 promoted fiber cement for modular affordable housing, boosting orders from Pennsylvania and Ontario plants. Canada’s 2025 code tightened moisture-management rules in cold climates, favoring boards over OSB.

Europe’s market volume is shaped by post-Grenfell fire statutes and the Energy Performance of Buildings Directive. Germany’s Building Energy Act credits high-thermal-mass partitions that stabilize indoor temperature swings. The UK replaced combustible façades on 2,500 buildings after 2024, converting to fiber cement. Nordic prefab ventures specify airtight boards to meet Passive House targets, while southern Europe deploys them as wildfire defenses.

In South America and the Middle East & Africa region, Brazil’s relaunched Minha Casa program in 2024 mandated termite-resistant cladding, adding 3 million m² in 2025. Saudi Arabia’s Vision 2030 hospitality builds use cement board to tolerate 50°C temperature swings. UAE green-building schemes under Estidama and Al Sa'fat grant credits for EPD-certified boards, nudging suppliers with transparent carbon data.

Competitive Landscape

The Cement Board market is moderately consolidated. James Hardie is investing USD 450 million in a Philippines plant that will cut Southeast Asian freight costs by 30% once operational in 2027. Etex acquired a Brazilian producer in 2025 to secure eucalyptus pulp, trimming fiber costs by 10-15%. Saint-Gobain’s digital twin platform reduced scrap 12% and energy 8% across European lines. End-of-life recycling remains white space. Pilot projects in the Netherlands and Japan test thermal decomposition to reclaim cement fines, but the energy use of 1.2-1.5 MWh/t is still prohibitive.

Cement Board Industry Leaders

James Hardie Industries Plc.

Etex Group

Saint-Gobain

Siam Cement Public Company Limited

ELEMENTIA MATERIALES, S.A.B. DE C.V

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Building materials and home solutions company, BirlaNu, announced plans to set up a greenfield fibre cement board plant in the Nellore district of Andhra Pradesh, India. The facility will utilise fly ash from coal-based thermal power plants as a key input, reducing industrial waste and boosting circular-economy practices.

- June 2025: IME Group, Nepal's inaugural producer of fiber cement boards, officially launched operations at its facility. This fully-automated plant boasts a daily production capacity of 75,000 sq. ft. The boards, measuring 4 ft by 8 ft and available in thicknesses from 4mm to 30mm, are not only fire-resistant and weatherproof but also flexible, durable, and eco-friendly.

Global Cement Board Market Report Scope

Cement boards serve as versatile building materials, finding applications in construction, renovation, and decoration. Composed of a blend of cement, water, and aggregates (like sand or silica), these boards are molded into sheets. Unlike traditional wood-based materials, cement boards exhibit reduced shrinkage and expansion, making them particularly suited for regions experiencing significant temperature and humidity variations.

The cement board market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into fiber cement board, wood wool cement board, wood strand cement board, and cement bonded particle board. By application, the market is segmented into flooring, exterior and partition walls, roofing, columns and beams, facades, weatherboard, and cladding, acoustic and thermal insulation, and other applications (prefabricated houses, permanent shuttering, fire-resistant construction, etc.). By end-user industry, the market is segmented into residential, commercial, and industrial and institutional. The report also covers the sizes and forecasts for the cement board market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (square meters).

| Fiber Cement Board (FCB) |

| Wood Wool Cement Board (WWCB) |

| Wood Strand Cement Board (WSCB) |

| Cement-Bonded Particle Board (CBPB) |

| Other Product Types (Magnesium Oxide Cement Board (MOCB), Rice Husk Cement Board) |

| Flooring |

| Exterior and Partition Walls |

| Roofing |

| Columns and Beams |

| Facades, Weatherboard and Cladding |

| Acoustic and Thermal Insulation |

| Other Applications (Prefabricated and Fire-resistant Construction) |

| Residential |

| Commercial |

| Industrial and Institutional |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| Vietnam | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Turkey | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Qatar | |

| Nigeria | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Fiber Cement Board (FCB) | |

| Wood Wool Cement Board (WWCB) | ||

| Wood Strand Cement Board (WSCB) | ||

| Cement-Bonded Particle Board (CBPB) | ||

| Other Product Types (Magnesium Oxide Cement Board (MOCB), Rice Husk Cement Board) | ||

| By Application | Flooring | |

| Exterior and Partition Walls | ||

| Roofing | ||

| Columns and Beams | ||

| Facades, Weatherboard and Cladding | ||

| Acoustic and Thermal Insulation | ||

| Other Applications (Prefabricated and Fire-resistant Construction) | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial and Institutional | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| Vietnam | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Turkey | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Qatar | ||

| Nigeria | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the cement board market in 2026?

It reached 704.78 million m² in 2026 and is projected to post a 5.19% CAGR through 2031.

Which product type holds the biggest share?

Fiber Cement Board led with 58.76% of 2025 volume thanks to its autoclaved strength and fire performance.

Which region is growing fastest?

Asia-Pacific is forecast to expand at 5.42% annually, lifted by India’s PMAY and Vietnam’s industrial parks.

What drives adoption in wildfire zones?

Class A fire ratings earn homeowners 10-20% insurance discounts in California and Australia, spurring retrofits.

Why do industrial users choose cement board?

Data centers, cleanrooms, and cold-storage sites value the material’s non-combustibility, impact strength, and moisture resistance, lowering long-term maintenance.

Page last updated on: