Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

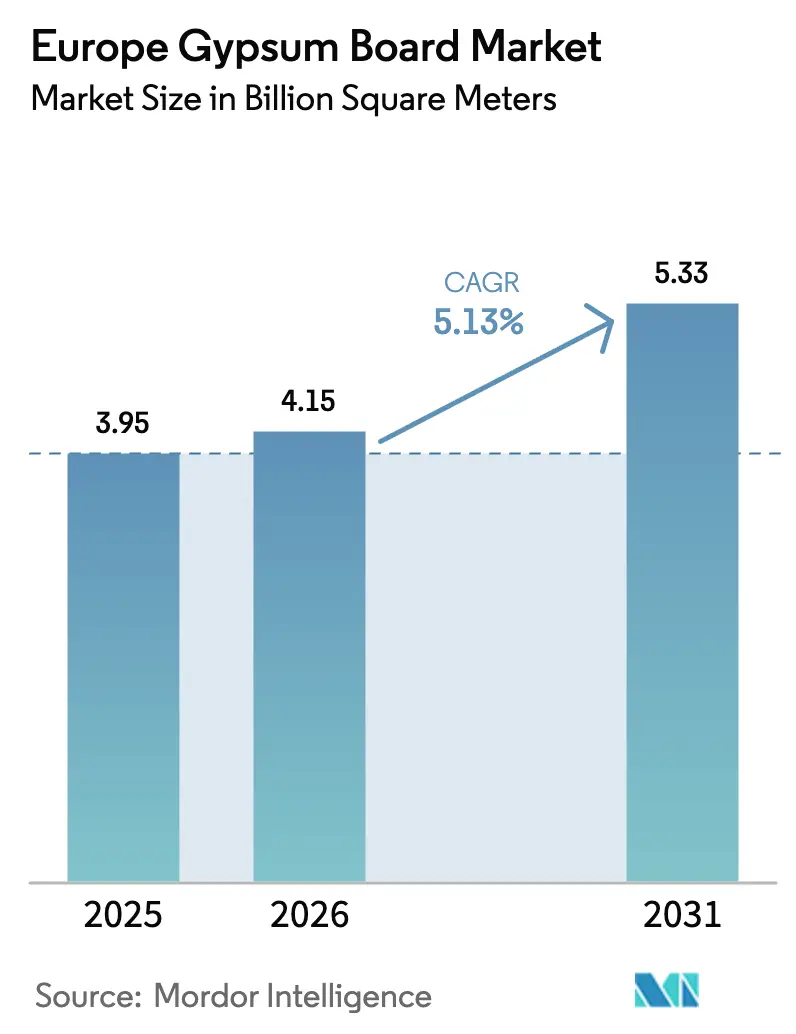

| Base Year Market Size (2025) | 3.95 Billion square meters |

| Market Volume (2026) | 4.15 Billion square meters |

| Market Volume (2031) | 5.33 Billion square meters |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

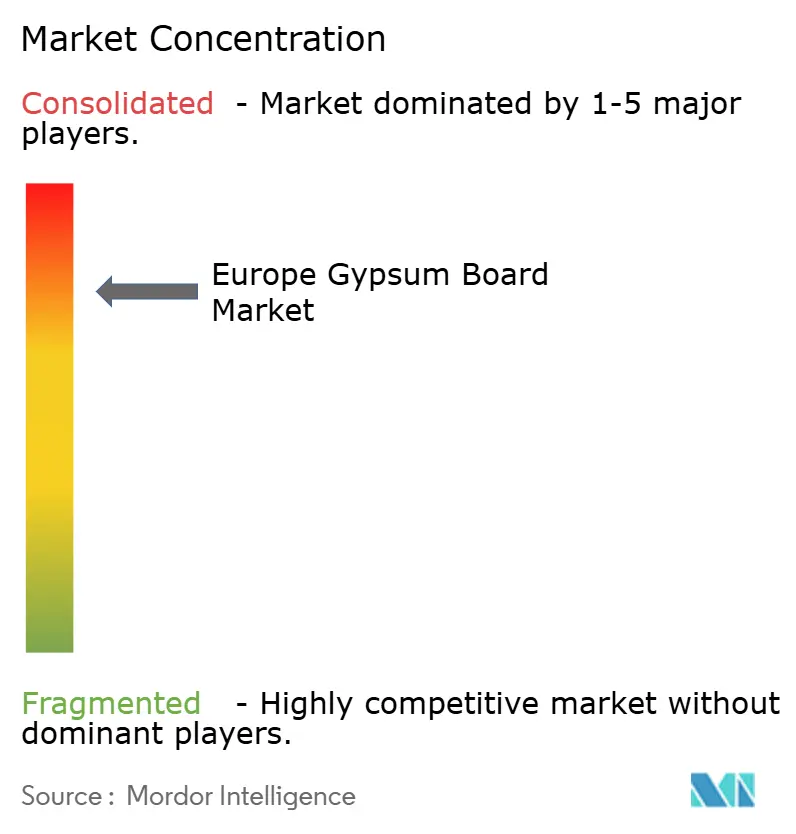

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Gypsum Board Market Analysis by Mordor Intelligence

The European Gypsum Board Market size is projected to be 3.95 billion square meters in 2025, 4.15 billion square meters in 2026, and reach 5.33 billion square meters by 2031, growing at a CAGR of 5.13% from 2026 to 2031. A measured rebound in renovation spending, the roll-out of national building‐renovation plans, and easing interest-rate pressures underpin the recovery after 2024’s construction slump. Regulatory compliance rather than speculative housebuilding is the prime demand trigger because the revised Energy Performance of Buildings Directive links renovation subsidies to mandatory life-cycle global-warming-potential disclosure. Deep energy retrofits that layer insulated plasterboard over existing substrates, rapid adoption of prefabricated interior systems, and stricter fire-plus-acoustic codes are pivoting volume toward high-performance wall boards. Competitive intensity is rising as multinationals accelerate recycled-content launches and expand regional footprints while cost-optimized local producers defend share in price‐sensitive Mediterranean markets.

Key Report Takeaways

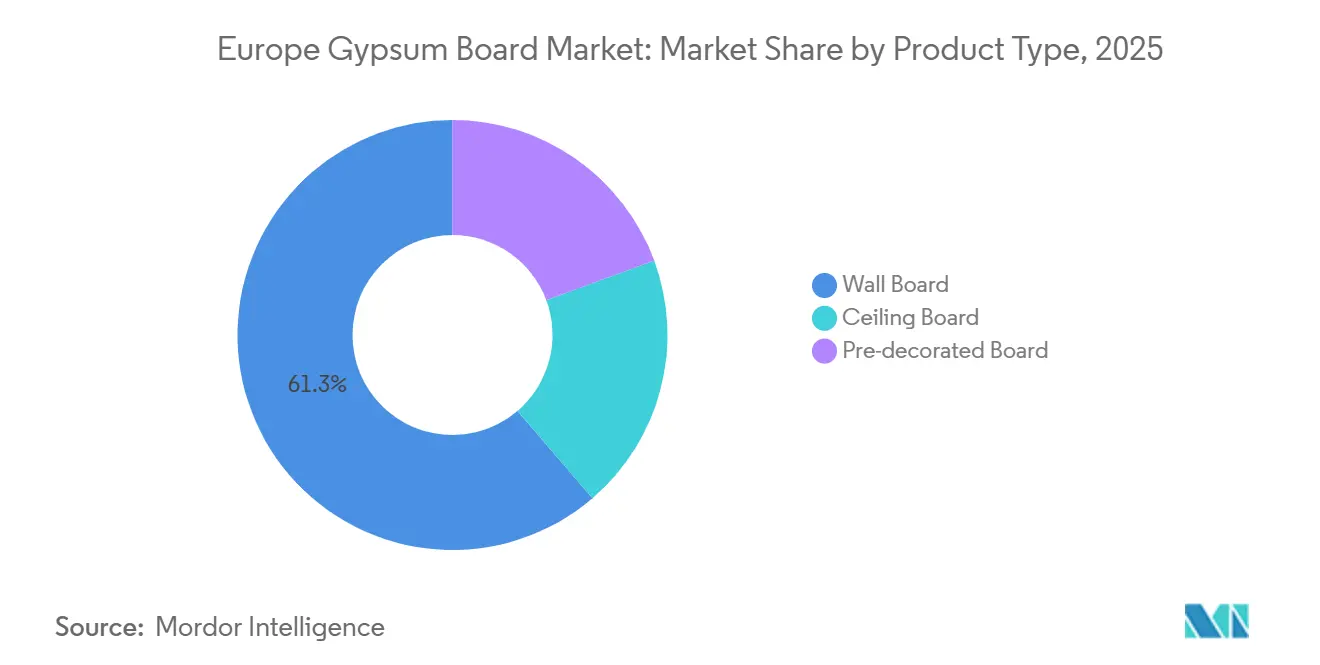

- By product type, wall board captured 61.28% of Europe gypsum board market share in 2025 and is advancing at a 7.85% CAGR through 2031.

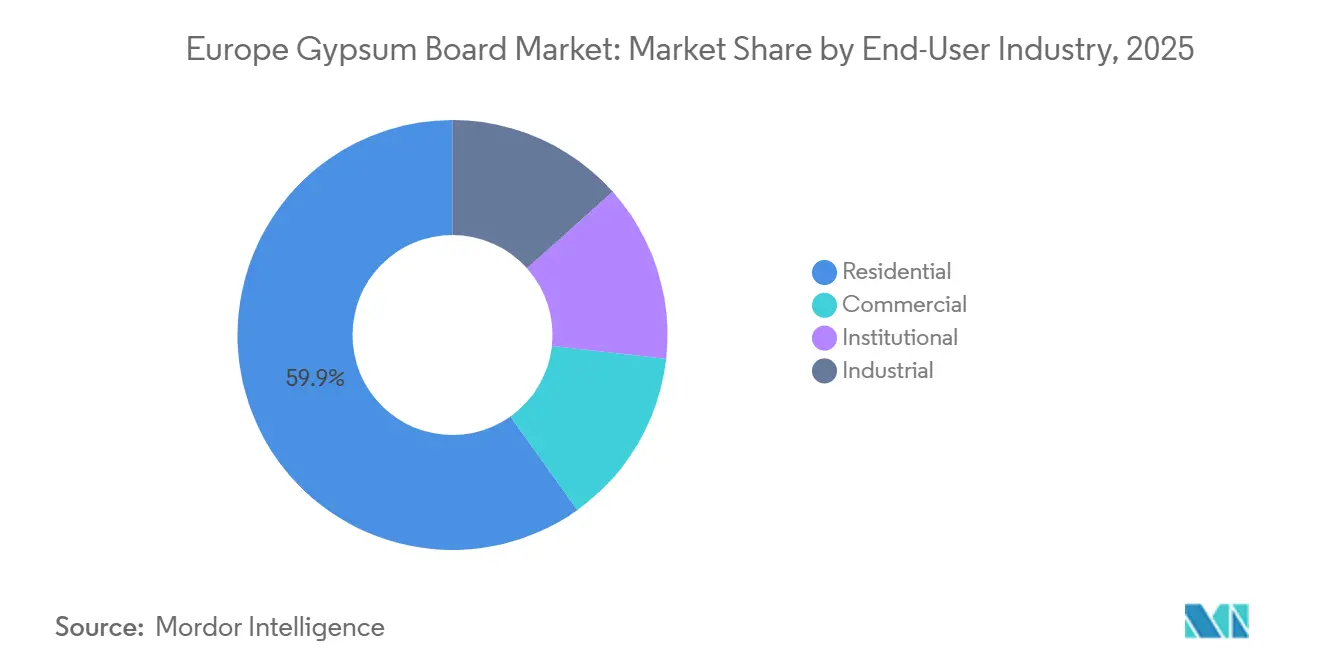

- By end-user industry, residential commanded 59.87% share of the Europe gypsum board market size in 2025, while commercial demand is growing at 7.90% CAGR to 2031.

- By geography, Germany led with 37.12% of Europe gypsum board market share in 2025; the NORDIC countries are expanding fastest at 6.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Gypsum Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green-Deal Backed Renovation Incentives | +1.8% | EU-wide, strongest in Germany, France, Italy, Spain | Medium term (2-4 years) |

| Stricter EU Fire and Acoustic Codes for Lightweight Partitions | +0.9% | EU-wide, particularly NORDIC countries, Germany, UK | Long term (≥ 4 years) |

| Rapid Uptake of Prefabricated Interior Systems | +1.2% | Germany, NORDIC countries, Netherlands, Austria | Medium term (2-4 years) |

| Growing Adoption of Moisture- and Mold-Resistant Boards in Coastal Areas | +0.5% | Mediterranean (Spain, Italy, Greece), Atlantic (UK, France) | Long term (≥ 4 years) |

| Hybrid-Work Boosts Demand for Demountable Walls | +0.7% | Western Europe (UK, Germany, France, Benelux), NORDIC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Green-Deal Backed Renovation Incentives

The Renovation Wave aims to upgrade 35 million buildings by 2030, with Member States obliged to submit final National Building Renovation Plans by December 2026[1]European Commission, “Renovation Wave Strategy,” ec.europa.eu . Tying subsidies to life-cycle global-warming-potential limits pulls retrofit demand forward as owners pre-empt future penalties. Germany’s EUR 500 billion Climate and Transformation Fund illustrates the scale of public capital, yet its 18.9% drop in building permits through November 2024 shows that finance alone cannot lift private housing starts. Transaction-cost reductions—one-stop shops and technical-assistance centers—due in 2026 are expected to unlock small-owner projects where gypsum board dominates internal upgrades. Spain’s Recovery Fund outlays already lifted construction output 9.8% year-on-year by November 2024, reinforcing the renovation-first dynamic. Romania’s 21% jump in construction investment in 2025 underlines how EU funding determines country-level growth trajectories.

Stricter EU Fire and Acoustic Codes for Lightweight Partitions

The EPBD recast requires Member States to reference Euroclass fire ratings and ISO 717 acoustic thresholds when partitions are replaced, embedding performance mandates into every retrofit. Several countries already compel whole-building life-cycle assessments, and Iceland targets 43% emissions cut by 2030, making lightweight A2-rated gypsum systems the baseline. Achieving similar fire and acoustic performance with timber panels needs thicker assemblies that raise upfront cost and embodied carbon. Knauf’s multi-attribute GB-WRTX board epitomizes the product drift toward bundled compliance, though each added certification inflates testing overheads that regional producers struggle to absorb.

Rapid Uptake of Prefabricated Interior Systems

Labor shortages trimmed EU construction payrolls 5% below 2019 levels in 2024, intensifying interest in factory-made wall modules that slash on-site hours. Knauf’s EUR 80 million Fos-sur-Mer plant, opened March 2024, outputs gypsum boards pre-integrated with insulation, vapor barriers and conduits, cutting installation times 40%. Horizon 2020’s ELISSA project proved a 25% heating-energy saving using prefabricated gypsum façades embedded with phase-change materials, though scale-up remains limited by fragmented supply chains. Adoption is highest in high-wage Germany and NORDICs where labor economics favor factory assembly over wet trades.

Growing Adoption of Moisture- and Mold-Resistant Boards in Coastal Areas

Climate-driven humidity spikes are lifting failure rates of standard boards whose water uptake exceeds 10%, leading to premature mold and replacement cycles. Moisture-resistant H1 boards carry a 15–20% premium, curbing penetration to less than 25% of coastal installations in 2025. Insurance exclusions are now nudging UK specifiers toward H1 products after moisture-related claims jumped 12% in 2024. Etex recycled 590,000 tonnes of gypsum waste in 2024—much from damaged boards—highlighting the circular-economy upside of initial moisture protection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Standard Boards' Water Vulnerability in High-Humidity Zones | -0.6% | Coastal Mediterranean, Atlantic regions, Baltic | Medium term (2-4 years) |

| Volatility in Gypsum and Liner-Paper Prices | -0.8% | EU-wide, acute in import-dependent markets (UK, Benelux) | Short term (≤ 2 years) |

| Emerging Bio-Based Wall Panels Stealing Sustainability Mindshare | -0.4% | NORDIC countries, Germany, Austria, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Standard Boards’ Water Vulnerability in High-Humidity Zones

Standard boards absorb more than 10% water by weight, causing swelling and mold within three years in coastal bathrooms and basements. Codes in Spain, Italy and Greece still lack mandatory H1 specifications, limiting moisture-resistant uptake to below 25% despite rising insurance exclusions. Etex’s 2024 waste data show moisture failures drive substantial replacement tonnage, undercutting circularity goals. While the issue is geographically limited, reputational spillover challenges gypsum’s suitability in any damp location.

Volatility in Gypsum and Liner-Paper Prices

Declining coal generation slashed synthetic gypsum supply, forcing greater reliance on natural gypsum or imports. Germany’s FGD gypsum output fell to 6.99 million t in 2019 from 11.25 million t in 2008 and is still dropping[2]USGS, “Gypsum Annual Report,” usgs.gov . Spot liner-paper prices swung 25–30% during 2023–2024; vertically integrated producers recouped margin faster than converters buying on the open market. UK and Benelux plants, importing up to 40% of feedstock, face the sharpest cost swings, influencing new-plant location choices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wall Board Dominates Volume and Growth

Wall board accounted for 61.28% of deliveries in 2025 and is forecast to grow 7.85% annually to 2031, keeping the Europe gypsum board market size expansion solidly tilted toward retrofit-friendly formats. Ceiling board trails because office new-build remains muted, while pre-decorated board stays niche outside high-wage Scandinavia and Germany. Manufacturers increasingly favor insulated wall boards that combine thermal, fire and acoustic performance in one sheet, aligning with EPBD thresholds. Knauf’s Fos-sur-Mer line produces 85% wall board, underscoring the segment’s pull.

Despite maturity, wall board remains the innovation hub of the Europe gypsum board market. Prefabricated wall modules reduce on-site labor by 40%, critical where wage rates exceed EUR 40 hourly. Digital passports embedded in wall boards support EPBD logbook requirements, facilitating recycling at end-of-life. Ceiling board upgrades focus mainly on acoustic tuning for hybrid offices, yet delayed tenant decisions cap growth. Pre-decorated boards gain traction where construction programs demand single-trade interior packages to compress schedules.

By End-User Industry: Residential Leads, Commercial Accelerates

Residential industry consumed 59.87% of boards in 2025, reflecting the stock of legacy dwellings that require energy upgrades to meet 2030 targets. The Europe gypsum board market share of commercial industry is expanding fastest, achieving a 7.90% CAGR through 2031 as corporates reconfigure space for hybrid work. Institutional demand adds stability because healthcare and education facilities must hit zero-emission status by 2028, two years ahead of private buildings.

Renovation incentives shift residential consumption toward laminated insulation boards, softening the link with new housing starts. Spain’s residential expansion, buoyed by Recovery Fund inflows, illustrates how EU transfers offset local mortgage constraints. Commercial uptake is concentrated in technology and finance tenants that value demountability to avoid relocation costs. Industrial users curb demand as logistics developers pivot to prefabricated metal panels with lower gypsum intensity. Across all segments, recycled-content specifications are tightening, aligning procurement with circular-economy criteria.

Geography Analysis

Germany dominated with 37.12% of shipments in 2025, yet its housing permits fell 18.9% year-on-year through November 2024 and residential output slid 4.9% in 2024 before a muted 1.1% rebound in 2025. Compliance-driven retrofits partly cushion demand, but the dwindling pipeline of new apartments constrains upside. Manufacturers respond by promoting prefabricated wall modules that compress labor overheads in Germany’s tight job market.

The NORDIC countries—Sweden, Norway, Denmark, Finland and Iceland—are the fastest-growing segment at 6.20% CAGR to 2031, driven by mandatory life-cycle assessment regimes and 43% carbon-reduction pledges that position low-embodied-carbon wall systems as default. Public procurement often requires Environmental Product Declarations and minimum recycled-content thresholds, pushing producers to route high-recycled-gypsum boards toward these markets. High labor costs also accelerate adoption of factory-finished wall panels, reinforcing volume growth.

Southern Europe shows a mixed picture. Spain’s construction activity rose 9.8% year-on-year by November 2024, primed by Recovery Fund grants, while Italy and France’s construction activity contracted 5.3% and 3.9% respectively in 2024. Cost-sensitive buyers in the Mediterranean still prioritize low-priced standard boards, dampening rapid uptake of recycled-content options. Central-Eastern Europe is volatile: Romania’s construction activity surged 21% in 2025 on EU-co-financed projects, but Bulgaria’s construction activity swings from 13.9% growth in 2024 to a 1.4% dip in 2025. Manufacturers therefore tailor product mixes: premium boards with high recycled content flow north, while leaner specifications defend share in the south.

Competitive Landscape

Highly concentrated yet fiercely contested, the European gypsum board market sees the top five—Knauf, Saint-Gobain, Etex, Holcim, and James Hardie—control roughly 80% of volumes. Demand drops of up to 40% in selected markets during 2024 compressed margins, prompting cost-cutting and targeted capacity additions. Etex opened its Bristol plant, the group’s most efficient plasterboard line, to position for the next upcycle, while Knauf invested EUR 80 million in Fos-sur-Mer to serve the prefabrication boom.

Strategic moves extend beyond gypsum. Holcim’s pending acquisition of Xella signals convergence between insulation, AAC blocks, and gypsum boards into integrated walling solutions worth EUR 12 billion annually. James Hardie, best known for fiber-cement siding, is leveraging its fire-resistant credentials to penetrate European interior partitions, heightening competition for incumbents in high-performance niches.

Europe Gypsum Board Industry Leaders

Etex Group

Saint-Gobain

Knauf Group

Holcim

James Hardie Europe GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Saint-Gobain introduced Gyproc SoundBloc Infinaé 100, the first 100% recycled gypsum board in the UK. This product utilizes recycled gypsum from construction waste to produce a high-quality, sustainable solution, aiming to minimize environmental impact and support circularity within the industry.

- October 2024: Knauf Group commissioned the Fos-sur-Mer gypsum board plant in France, adding 30 million square meters of annual capacity dedicated to prefabricated modules. The company invested EUR 80 million in the eight-hectare site for the manufacturing plant.

Europe Gypsum Board Market Report Scope

Gypsum boards are a common building material used for partitions and lining walls, roofs, ceilings, and floors. These boards are constructed of a set gypsum core surfaced with specially created paper firmly adhered to the core. Gypsum board is also known as drywall, plasterboard, and wallboard.

The Europe gypsum board market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into wallboard, ceiling board, and pre-decorated board. By end-user industry, the market is segmented into the residential, commercial, institutional, and industrial. The report also covers the market sizes and forecasts for the gypsum board market in 5 countries across the Europe. For each segment, the market sizing and forecasts have been done on the basis of volume (square meters).

By Product Type

| Wall Board |

| Ceiling Board |

| Pre-decorated Board |

By End-User Industry

| Residential |

| Commercial |

| Institutional |

| Industrial |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Rest of Europe |

| By Product Type | Wall Board |

| Ceiling Board | |

| Pre-decorated Board | |

| By End-User Industry | Residential |

| Commercial | |

| Institutional | |

| Industrial | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe gypsum board market in 2026?

Volume reached 4.15 billion square meters in 2026 and is forecast to climb to 5.33 billion square meters by 2031.

What is the expected CAGR for gypsum board demand in Europe?

The market is projected to post a 5.13% CAGR between 2026 and 2031.

Which product type leads regional consumption?

Wall board dominates with 61.28% share in 2025 and is also the fastest-growing segment with a 7.85% CAGR from 2026 to 2031.

Why are NORDIC countries the fastest-growing sub-region?

Mandatory life-cycle assessment rules and ambitious carbon targets are driving 6.20% CAGR demand through 2031.

Page last updated on: