Transfection Reagents And Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

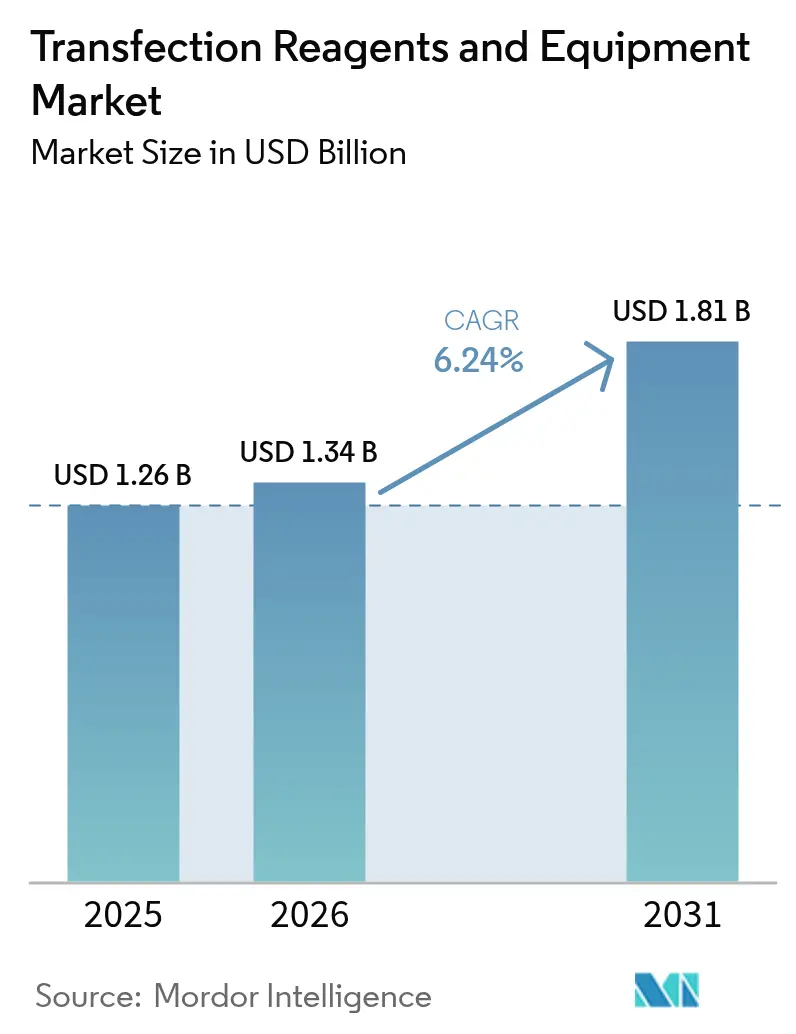

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

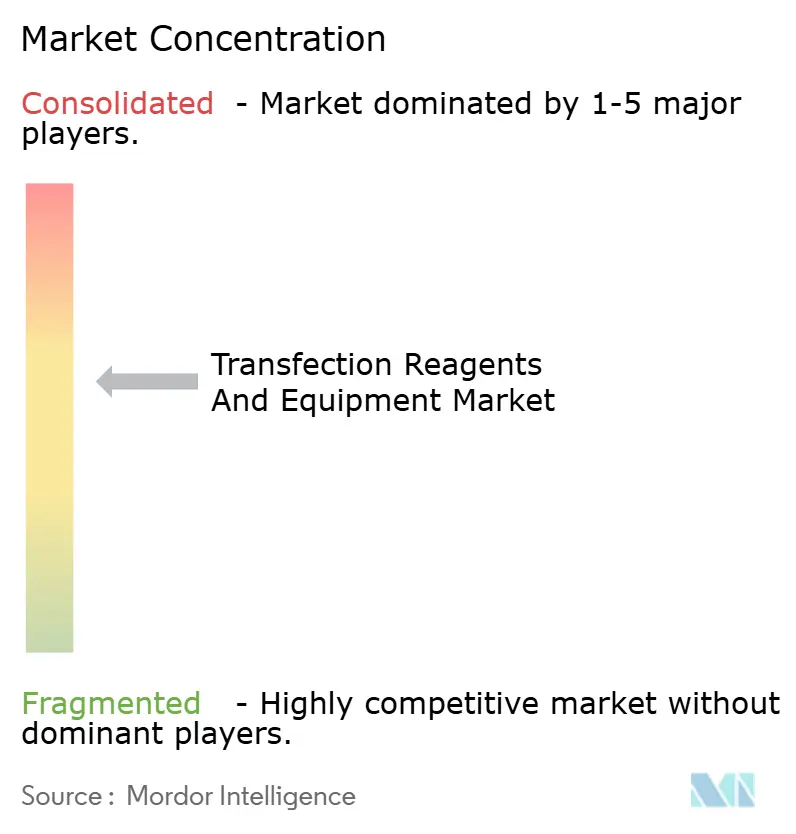

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transfection Reagents And Equipment Market Analysis by Mordor Intelligence

The transfection reagents and equipment market size was valued at USD 1.26 billion in 2025 and estimated to grow from USD 1.34 billion in 2026 to reach USD 1.81 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031). This steady expansion is propelled by regulatory momentum in cell and gene therapies, sustained R&D spending by pharmaceutical manufacturers, and rapid method-level innovation that improves scalability for commercial production. Consolidation among suppliers, the emergence of AI-guided reagent design, and heightened outsourcing to contract development and manufacturing organizations (CDMOs) are reinforcing competitive barriers while widening end-user options. Asia-Pacific’s double-digit growth, Europe’s regulatory harmonization around advanced therapies, and North America’s established manufacturing base collectively intensify global demand for GMP-grade transfection solutions. Equipment revenues are rising faster than reagents as laboratories replace manual protocols with high-throughput electroporation, microfluidic, and nanoparticle platforms optimized for consistency, traceability, and automated parameter control. Together, these factors confirm a durable expansion cycle for the transfection reagents and equipment market through 2030.

Key Report Takeaways

- By product category, reagents retained 73.62% of the transfection reagents and equipment market share in 2025, while the equipment segment is accelerating at a 12.64% CAGR through 2031.

- By method, viral techniques occupied 42.68% of the transfection reagents and equipment market size in 2025; physical methods post the fastest growth at 14.45% CAGR through 2031.

- By application, protein production accounted for 30.21% of the transfection reagents and equipment market size in 2025, whereas cell and gene therapy manufacturing is advancing at a 14.98% CAGR to 2031.

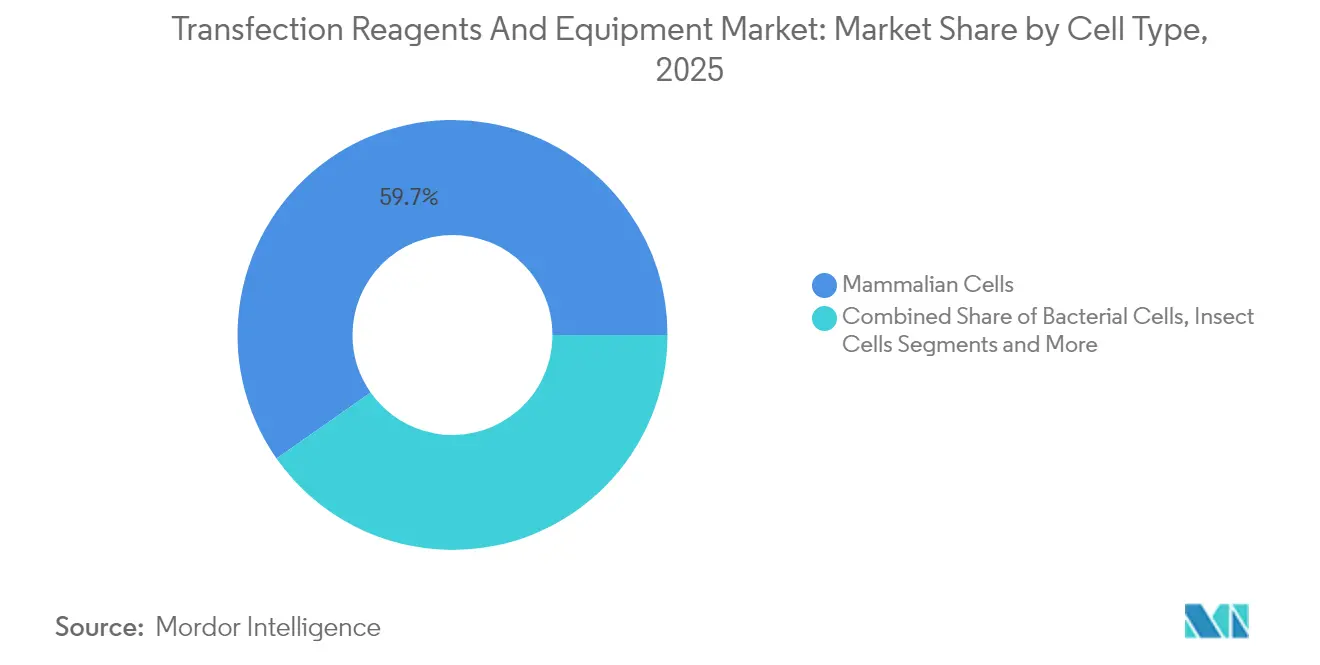

- By cell type, mammalian cells led with 59.74% of transfection reagents and equipment market share in 2025; insect cells register the highest projected CAGR at 11.39% through 2031.

- By end user, pharmaceutical and biotechnology companies controlled 62.94% of the transfection reagents and equipment market size in 2025, while CROs and CMOs are expanding at a 12.01% CAGR through 2031.

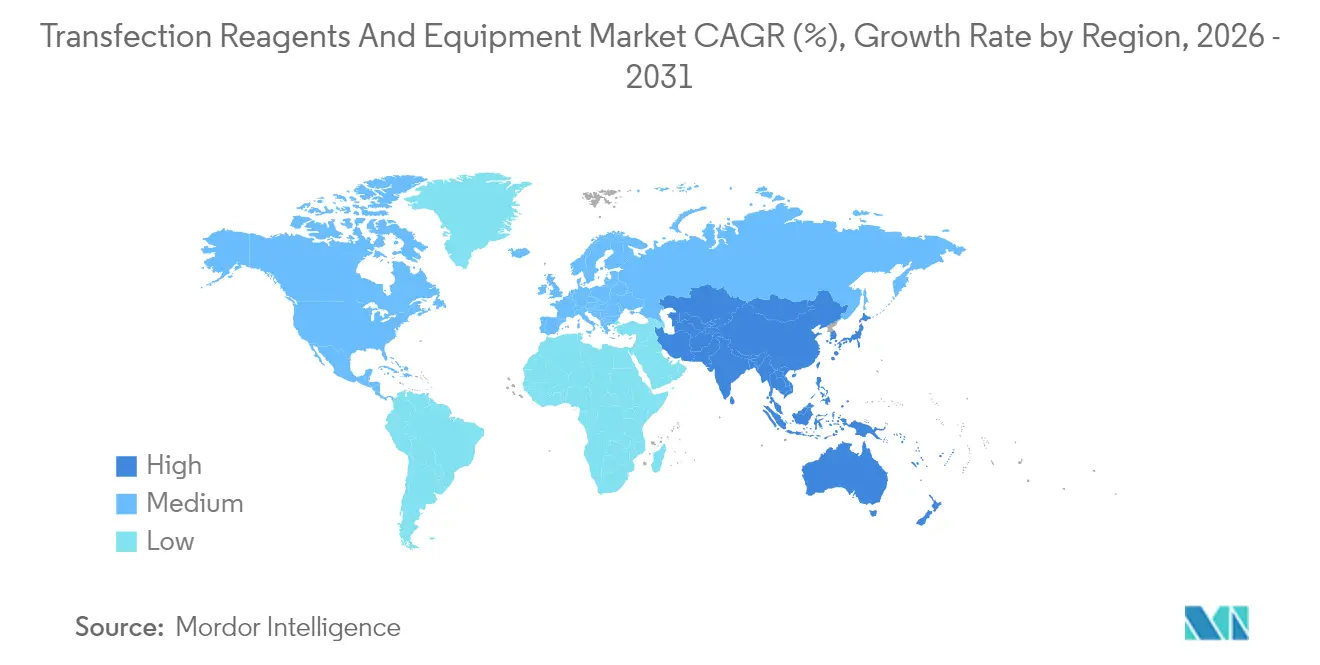

- By geography, North America led with 37.66% market share in 2025, whereas Asia-Pacific is expected to register a 10.14% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Transfection Reagents And Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in non-viral transfection chemistries | +1.8% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Growing R&D spend by pharma & biotech firms | +1.5% | North America & Asia-Pacific | Short term (≤ 2 years) |

| Surge in synthetic gene & mRNA demand | +2.1% | North America & European Union | Short term (≤ 2 years) |

| Expansion of cell & gene-therapy clinical pipelines | +1.9% | Global, North America leading | Medium term (2-4 years) |

| AI-driven reagent-formulation optimization | +0.8% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Microfluidic high-throughput transfection platforms | +0.7% | North America & Europe, APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Non-Viral Transfection Chemistries

Multiple research groups are engineering ionizable cationic lipids with biodegradable cores that remove cholesterol and phospholipids while maintaining high transfection efficiency, lowering toxicity and enabling organ-targeted delivery[1]Yizhou Dong, “Reformulating Lipid Nanoparticles for Organ-Targeted mRNA Accumulation and Translation,” Nature Communications, nature.com. Polyplus supplemented this progress with FectoVIR-AAV, a reagent calibrated for industrial AAV production that boosts viral titers in GMP environments. The expansion of polymer-based and hybrid nanotube carriers furthers non-viral uptake, mitigating batch variability and reducing viral safety concerns. Manufacturers now embed predictive algorithms that adjust reagent ratios in real time, assuring consistent performance across different cell lines and reducing development timelines. As non-viral efficiencies approach viral benchmarks, the technology becomes integral to large-scale therapeutic manufacturing, driving consumption of high-performance reagents.

Growing R&D Spend by Pharma & Biotech Firms

Despite broader cost pressures, leading life-science companies preserve or raise gene-therapy budgets to secure premium assets that command higher pricing in specialty indications. Roche deployed EUR 90 million in a German gene-therapy center, while AstraZeneca invested USD 300 million in a U.S. cell-therapy plant, both requiring high-capacity transfection lines. These projects expand demand for platform reagents that adhere to data-rich quality-by-design protocols. Generative AI further accelerates screening cycles, mandating automated equipment that can execute tens of thousands of optimized transfections each week. This capex shift cascades down the supply chain, widening the installed base of high-throughput devices and recurring reagent sales.

Surge in Synthetic Gene & mRNA Demand

Five LNP-enabled therapeutics have secured either FDA or EMA approval, affirming lipid nanoparticles as an accepted carrier for mRNA payloads. Emerging plasmid alternatives such as dbDNA and rapid-assembly circular DNA aim to sidestep bacterial contaminants and shorten production cycles, but they still require specialized transfection chemistries. Regulatory authorities are crafting LNP-specific guidelines that tighten characterization requirements, increasing reliance on well-documented GMP reagents. Suppliers now bundle validated documents, sterility reports, and endotoxin profiles within each reagent lot, helping sponsors meet accelerated review timelines. The race to commercialize mRNA therapeutics thus translates directly into volume gains for transfection consumables tailored to nucleic-acid payload diversity.

Expansion of Cell & Gene-Therapy Clinical Pipelines

The global pipeline includes more than 3,900 gene-therapy trials either completed, ongoing, or approved, indicating unparalleled clinical activity. Regulatory designations such as the FDA’s regenerative medicine advanced therapy pathway expedite approvals but also heighten expectations for batch-to-batch consistency. iPSC-derived therapies entering Phase I require electroporation platforms capable of processing hundreds of millions of cells without compromising viability, galvanizing equipment demand. As indications move from rare to prevalent diseases, commercial batch sizes grow exponentially, extending reagent consumption lifecycles and locking in predictable long-term revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced reagents & instruments | -1.2% | Global, steeper in emerging economies | Short term (≤ 2 years) |

| Limited cell-type specificity / cytotoxicity | -0.9% | Global, cross-application | Medium term (2-4 years) |

| GMP-grade plasmid supply bottlenecks | -0.8% | North America & Europe | Short term (≤ 2 years) |

| Scale-up challenges for commercial manufacturing | -1.1% | Mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Reagents & Instruments

GMP-compliant reagents ship at premium price points, and clinical-grade electroporation devices can exceed USD 300,000, deterring start-ups and academic labs[2]Noah Maloney, “Electroporators Cost for Leasing & Financing,” Excedr, excedr.com. Equipment leasing and reagent subscription models are emerging to soften upfront burdens, yet many emerging-market firms still defer procurement or rely on lower-spec alternatives that hinder scalability. Facility divestitures—such as UniQure’s sale of a production plant—highlight the operational cost strain on mid-tier innovators. Suppliers with global service footprints and financing programs gain a competitive edge by democratizing access to premium platforms.

Limited Cell-Type Specificity / Cytotoxicity Issues

Primary T-cells, mesenchymal stem cells, and other difficult-to-transfect lines often exhibit sub-optimal uptake that limits therapeutic efficacy, even with optimized protocols. Acoustic and acoustothermal techniques are improving viability metrics, but commercial readiness remains several years away. To bridge performance gaps, vendors release cell-type-tailored chemistries such as jetOPTIMUS, though universal compatibility remains elusive. Persistent inefficiencies lengthen development timelines and inflate consumable costs, narrowing margins for both innovators and service providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Reagents Dominate Despite Equipment Acceleration

Reagents represented 73.62% of the transfection reagents and equipment market in 2025, reflecting steady demand from repeat consumables required for each experiment or production batch. This dominance translated into more than USD 927 million in reagent revenues within the transfection reagents and equipment market size, while equipment contributed the balance. Lipid-based chemistries remain the largest subset due to established safety profiles; polymer and hybrid lipid-polymer systems gain share in applications that benefit from reduced immunogenicity. The reagents category also benefits from shorter innovation cycles, with suppliers introducing formulations engineered for mRNA, CRISPR guides, or AAV production every 12–18 months.

Equipment revenues, though smaller in absolute terms, are increasing at 12.64% CAGR as manufacturers replace manual or low-throughput methods. Electroporation platforms account for the largest share of equipment sales; recent models include cartridge-based disposables that minimize cross-contamination risk. Microinjection systems remain essential for embryonic stem-cell applications despite labor-intensive workflows, whereas microfluidic devices offer automated throughput for early-stage screens. AI-enabled electroporation chambers that adjust field strength and pulse duration in real time address long-standing variability challenges. As CDMOs and large biologics producers expand capacity, equipment backlogs support robust forward demand.

By Method: Viral Methods Lead While Physical Methods Surge

Viral approaches held 42.68% market share in 2025 within the transfection reagents and equipment market. Sponsors rely on AAV and lentiviral delivery for their high integration efficiency, critical in ex vivo therapies such as CAR-T. The regulatory familiarity of viral systems and the availability of readymade vector platforms reduce development risk. However, concerns around immunogenicity and insertional mutagenesis motivate exploration of alternative techniques.

Physical methods are realizing 14.45% CAGR propelled by potent electroporation and sonoporation technologies that reach efficiencies above 90% without viral proteins. These systems support closed-system manufacturing, aligning with GMP expectations by minimizing contamination risk. Sonoporation further extends applicability to hard-to-transfect tissues via ultrasound-mediated membrane permeabilization, a feature attractive in in vivo gene therapies. Although biochemical methods like calcium-phosphate precipitation persist in basic research, their market share is gradually declining as next-generation modalities scale throughput and reduce cytotoxicity.

By Application: Therapeutic Manufacturing Drives Growth

Despite protein production maintaining 30.21% share, the cell and gene therapy manufacturing application is experiencing the fastest expansion at 14.98% CAGR in the transfection reagents and equipment market. The arrival of commercial-scale CAR-T, CRISPR-edited hemoglobinopathy treatments, and iPSC-derived therapy pipelines demands GMP-grade transfection reagents, supporting premium pricing tiers. Manufacturers integrate electronic batch records and AI-based release testing, driving demand for compliant digital interfaces on electroporation devices.

Protein production applications remain essential for monoclonal antibodies and receptor-fusion proteins, reinforced by continuous-processing initiatives that raise yield per liter. Drug discovery labs rely on transient transfection for high-throughput screening, sustaining reagent volumes despite relatively low premiums. Academic and cancer research units develop novel intracellular delivery platforms, such as foam-based carriers that have demonstrated up to 384-fold efficiency improvements, expanding niche applications and potentially seeding future commercial products.

By Cell Type: Mammalian Dominance Faces Emerging Alternatives

Mammalian systems captured 59.74% of the transfection reagents and equipment market in 2025, supported by validated CHO and HEK293 lines widely accepted by regulators. Workflow familiarity and predictable post-translational modifications make mammalian transfection the default for therapeutic proteins. Innovation focuses on editing cell-death pathways and metabolic rewiring to elevate productivity, thereby raising reagent usage per batch.

Insect cells deliver an 11.39% CAGR because baculovirus systems offer high volumetric yields and rapid scaling, suiting vaccine production where speed is paramount. Yeast and fungi address glyco-engineering needs, whereas plant-based expression gains attention for oral or thermostable biologics. Each alternative demands custom-tailored transfection chemistries, often at lower ionic strengths or different pH optima, expanding supplier portfolios and R&D services.

By End User: CROs Challenge Pharma Dominance

Pharmaceutical and biotechnology companies held a 62.94% stake in the transfection reagents and equipment market size in 2025, sustaining large internal footprints for proprietary IP protection and process control. They increasingly purchase full-suite platforms—reagents, instruments, software—to retain data integrity across discovery to commercial phases. However, CROs and CMOs are expanding 12.01% CAGR as sponsors outsource specialized projects or surge needs, especially in regions where real estate or headcount constraints limit internal capacity. Academic centers remain vital incubators of innovation but often lack budgets for premium electroporators, relying on grant-supported shared facilities or cost-sharing agreements with industry partners.

Geography Analysis

North America held 37.66% market share in 2025, underpinned by FDA leadership and robust venture funding. The region hosts large-scale facilities like AstraZeneca’s new USD 300 million cell-therapy site, reinforcing domestic demand for production-scale reagents and electroporation equipment. Integer capacity constraints and rising operating expenses nevertheless motivate select companies to explore CDMO partnerships in lower-cost jurisdictions.

Asia-Pacific records the highest regional CAGR at 10.14%, energized by China’s 228 drug approvals in 2024 and regulatory reforms that target full convergence with ICH guidelines by 2027. Domestic suppliers scale up GMP-grade vector and reagent production, while multinational CDMOs expand footprint to serve both local and export pipelines. Japan and South Korea are codifying dedicated advanced-therapy frameworks, streamlining clinical entry for allogeneic products. Southeast Asian governments are offering tax incentives and greenfield bioparks, positioning the sub-region as a future transfection manufacturing hub.

Europe benefits from harmonized ATMP guidelines and proactive EMA approvals such as the CRISPR-based CASGEVY therapy, sustaining demand for end-to-end transfection solutions. Roche’s EUR 90 million gene-therapy center exemplifies how global incumbents anchor production within the EU, leveraging workforce expertise and streamlined release testing. Environmental compliance initiatives spur innovation in biodegradable lipid formulations, while supply-chain traceability regulations encourage digitalization of equipment platforms.

Competitive Landscape

The transfection reagents and equipment industry is moderately concentrated, with integrated giants Thermo Fisher Scientific, Merck, and Lonza leveraging vertical breadth and M&A to secure end-to-end capability. Thermo Fisher’s planned USD 40–50 billion acquisition budget and its USD 4.1 billion purification business purchase illustrate continued scale building. Merck’s USD 600 million Mirus Bio acquisition expanded its viral-vector know-how, strengthening its reagent lineup. Lonza’s manufacturing contract for CASGEVY underlines its stature as a preferred large-scale partner.

Challenger firms carve out niches through technological differentiation. MaxCyte’s Flow Electroporation supports 29 strategic licenses and underpins the first CRISPR therapy approval, demonstrating the commercial relevance of high-viability non-viral platforms. The company’s 2025 acquisition of SeQure Dx extends its analytics into off-target editing characterization. Polyplus focuses on reagent optimization, leveraging AI design to rapidly customize formulations for specific cell types and payloads. White-space opportunities persist in ultralow-cost, high-yield reagents for emerging markets and in turnkey microfluidic platforms that merge real-time analytics with cloud-based control.

Transfection Reagents And Equipment Industry Leaders

Bio-Rad Laboratories

Polyplus-transfection SA

Promega Corporation

Qiagen N.V.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EMBLEM Technology Transfer GmbH licensed patented technology to CHO Plus for transfecting cells to produce therapeutic agents.

- July 2024: STEMCELL Technologies launched the CellPore Transfection System, a technology aimed at advancing cell-engineering research and novel cell-therapy development.

Global Transfection Reagents And Equipment Market Report Scope

As per the scope of the report, transfection refers to the process of artificially introducing nucleic acids (DNA or RNA) into eukaryotic cells. Such introductions of foreign nucleic acid using various chemical, biological, or physical methods can result in changing the properties of the cell, allowing the study of gene function and protein expression in the context of the cell. The reagents and equipment used in this procedure are referred to as transfection reagents and equipment. The transfection reagents and equipment market is segmented by product (reagents and equipment), by method (biochemical method, physical methods, and viral methods), by end-user (pharmaceutical and biotechnology companies, and academics and research institutes, and others), and by geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Reagents | Lipid-based |

| Polymer-based | |

| Protein-based | |

| Equipment | Electroporation Systems |

| Microinjection Systems | |

| Nanoparticle-mediated Systems |

| Biochemical Methods | Lipofection |

| Calcium-Phosphate | |

| Physical Methods | Electroporation |

| Microinjection | |

| Sonoporation | |

| Viral Methods | Retroviral |

| Lentiviral | |

| AAV |

| Protein Production |

| Gene & mRNA Expression Studies |

| Cell & Gene Therapy Manufacturing |

| Cancer Research |

| Drug Discovery & Screening |

| Mammalian Cells |

| Bacterial Cells |

| Yeast & Fungi |

| Insect Cells |

| Plant Cells |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| CROs & CMOs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Reagents | Lipid-based |

| Polymer-based | ||

| Protein-based | ||

| Equipment | Electroporation Systems | |

| Microinjection Systems | ||

| Nanoparticle-mediated Systems | ||

| By Method | Biochemical Methods | Lipofection |

| Calcium-Phosphate | ||

| Physical Methods | Electroporation | |

| Microinjection | ||

| Sonoporation | ||

| Viral Methods | Retroviral | |

| Lentiviral | ||

| AAV | ||

| By Application | Protein Production | |

| Gene & mRNA Expression Studies | ||

| Cell & Gene Therapy Manufacturing | ||

| Cancer Research | ||

| Drug Discovery & Screening | ||

| By Cell Type | Mammalian Cells | |

| Bacterial Cells | ||

| Yeast & Fungi | ||

| Insect Cells | ||

| Plant Cells | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| CROs & CMOs | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the transfection reagents and equipment market?

The transfection reagents and equipment market size stood at USD 1.34 billion in 2026 and is projected to reach USD 1.81 billion by 2031 at a 6.24% CAGR.

Which product segment generates the highest revenue?

Reagents dominate, holding 73.62% market share in 2025 due to their recurring consumable nature.

Why are physical transfection methods growing rapidly?

Physical techniques like electroporation achieve high efficiency without viral vectors, driving a 14.45% CAGR as safety and scalability demands rise.

Which region is expanding fastest in this market?

Asia-Pacific records the highest CAGR at 10.14%, driven by China’s regulatory reforms and manufacturing scale-up.

How are AI technologies influencing this industry?

AI optimizes reagent formulations and transfection parameters, reducing failure rates and shortening development timelines, particularly in North American and European facilities.

Page last updated on: