Dental Sterilization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

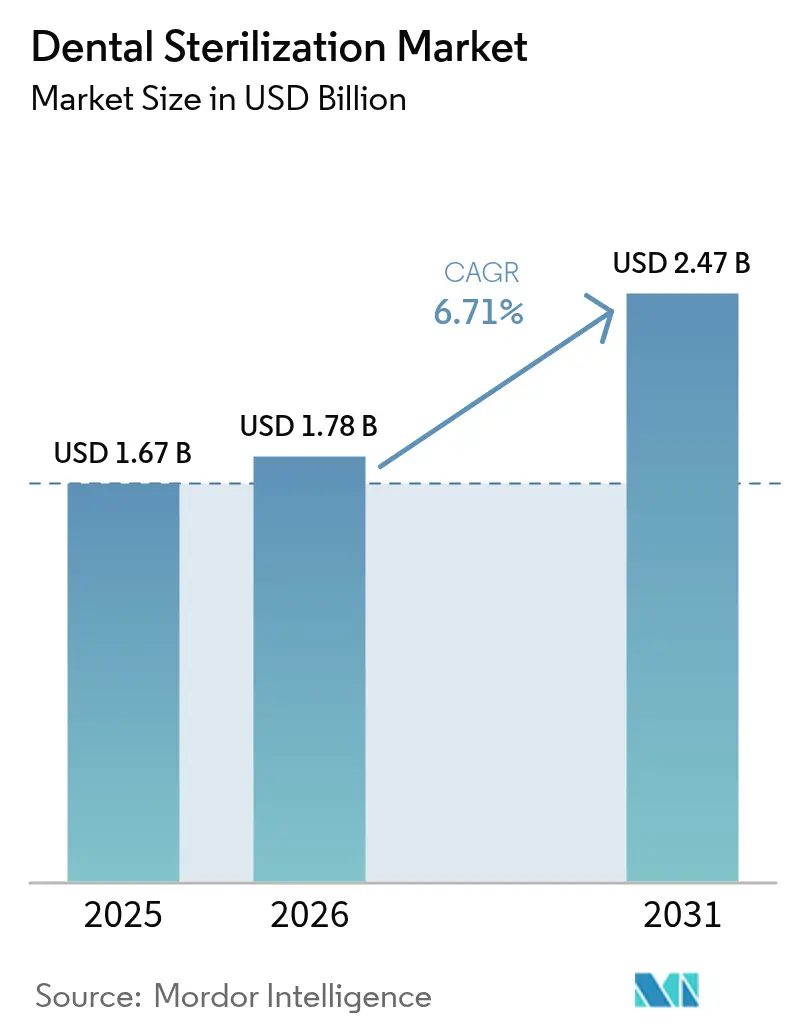

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

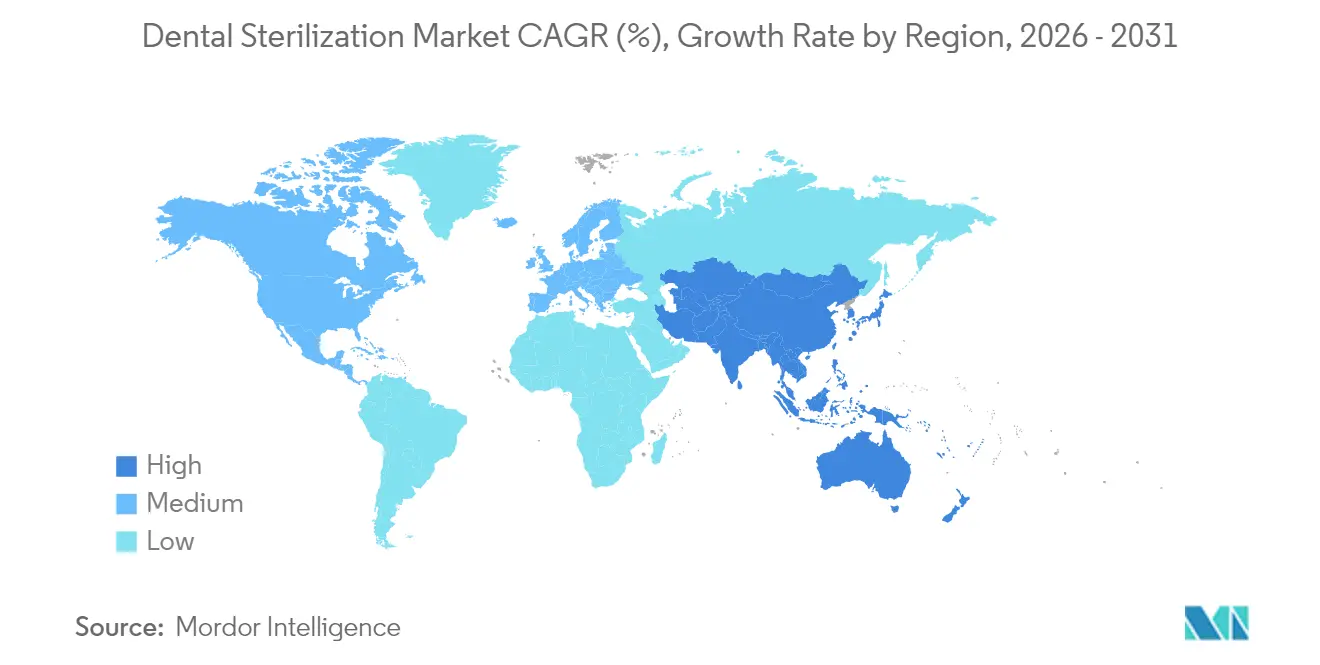

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

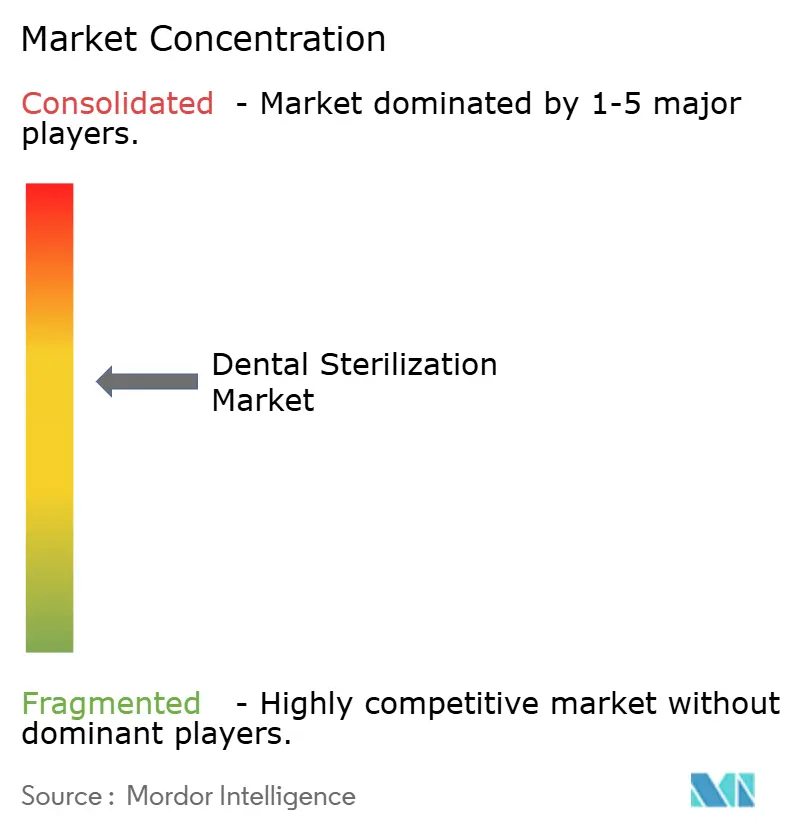

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Sterilization Market Analysis by Mordor Intelligence

Dental Sterilization Market size in 2026 is estimated at USD 1.78 billion, growing from 2025 value of USD 1.67 billion with 2031 projections showing USD 2.47 billion, growing at 6.71% CAGR over 2026-2031. Expansion is propelled by stricter infection-control regulations, widening adoption of digital workflows that raise instrument-turnaround expectations, and steady technology upgrades that align with environmental and staff-safety goals. North America holds 38.16% revenue share in 2024 thanks to well-established reimbursement systems and early uptake of smart autoclaves. Asia-Pacific, advancing at an 8.39% CAGR, is rapidly closing the sterilization-infrastructure gap on the back of aging populations and expanded dental-insurance coverage.[1]Source: Rakhee Patel, Jennifer Gallagher, “Healthy Ageing and Oral Health,” Nature, nature.com Instruments remain the revenue cornerstone, yet rising reliance on single-use consumables and accessories is reshaping purchase patterns and elevating recurring-revenue streams. Hydrogen-peroxide plasma systems are moving from niche to mainstream because they process heat-sensitive devices without ethylene-oxide emissions. Competitive intensity is moderate and fluid; established vendors are pruning portfolios to concentrate on high-margin niches, while mid-tier innovators pursue cloud-connected sterilizers that sync with practice-management platforms.

Key Report Takeaways

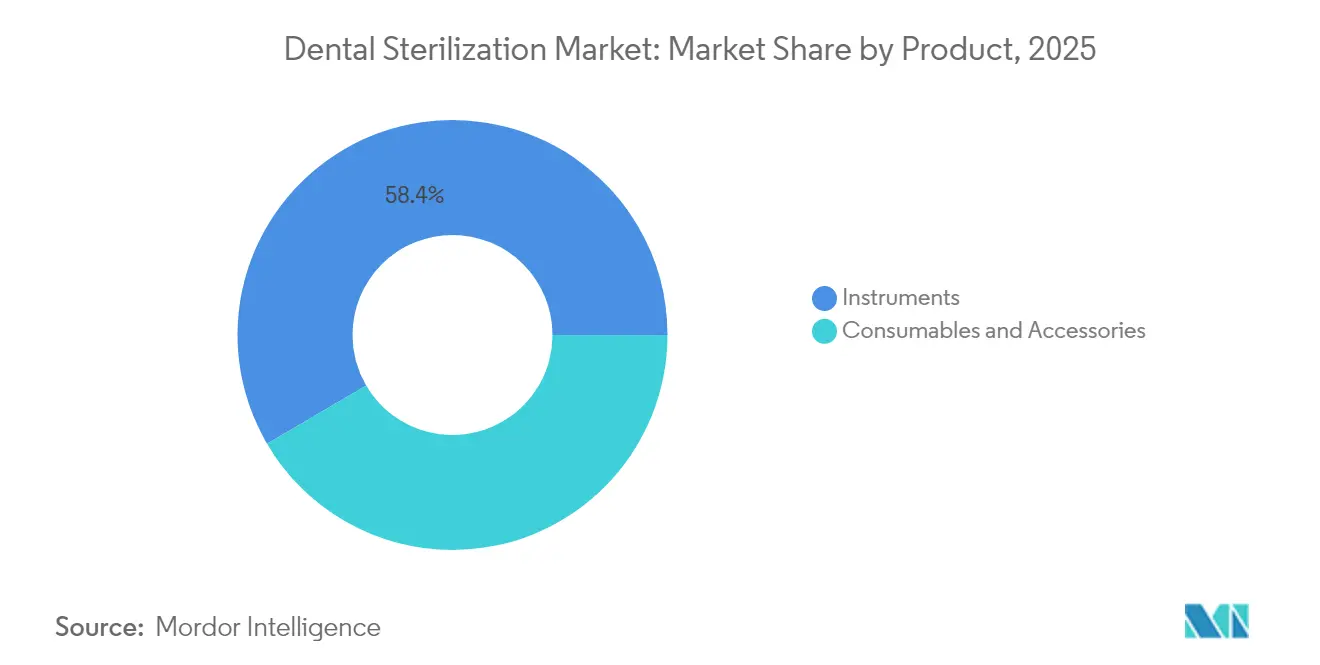

- By product type, instruments accounted for 58.43% of the dental sterilization market share in 2025, whereas consumables and accessories are expanding at a 7.71% CAGR through 2031.

- By sterilization method, heat and steam systems led with 44.75% revenue share in 2025; hydrogen-peroxide plasma units are projected to rise at a 7.62% CAGR between 2026-2031.

- By end user, clinics generated 61.62% of the dental sterilization market size in 2025, while dental laboratories are on track for an 7.94% CAGR to 2031.

- By geography, North America captured 37.88% of global revenue in 2025; Asia-Pacific records the fastest regional CAGR at 8.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Sterilization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Dental Ailments | +1.2% | Global, with higher impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Growth in Cosmetic Dentistry Procedures | +0.8% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increasing Volume of Dental Surgeries | +1.0% | Global, driven by aging population demographics | Long term (≥ 4 years) |

| Stricter Infection-Control Regulations and Guidelines | +1.5% | Global, with immediate impact in developed markets | Short term (≤ 2 years) |

| Chairside CAD/CAM Workflow Creating Rapid Re-Processing Demand | +0.9% | North America & Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Adoption of IoT-Enabled "Smart" Autoclaves by Multi-Clinic Chains | +0.7% | North America & Europe, early adoption in urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Ailments

An estimated 280 million older adults experienced oral disorders in 2024, and the burden is shifting sterilization patterns as clinicians handle complex, multi-visit cases that escalate instrument-turnaround cycles. The World Health Organization’s oral-health strategy elevates infection-prevention obligations, prompting clinics to acquire higher-capacity sterilizers rather than extend cycle times. Emerging Asia-Pacific markets face a dual challenge of rising patient volumes and historically under-funded infection-control infrastructure, spurring fast equipment adoption despite capital constraints. The link between disease prevalence and sterilization demand is non-linear; high-complexity treatments often trigger multiple loads per appointment, stretching existing capacity. Manufacturers that supply modular or stackable autoclave formats are therefore positioned to capitalize on this demographic-driven uptick.

Growth in Cosmetic Dentistry Procedures

Elective aesthetic treatments such as veneers, aligners, and digital smile design rose sharply in 2024, and each procedure involves delicate burs, ceramic presses, and polymerizing tips that cannot tolerate repeated steam exposure.[2]Source: Journal of Esthetic and Restorative Dentistry, “Digital Smile Design and Instrument Preservation,” jerdentistry.com Clinics serving this segment gravitate toward hydrogen-peroxide plasma or ozone-based systems that operate below 60 °C while maintaining sterility assurance levels. Demand concentration remains highest in the United States and Western Europe, yet metropolitan centers in South Korea, Japan, and India now house fast-growing cosmetic practices that replicate Western sterilization standards. Because aesthetic visits often cluster into tightly scheduled sessions, practitioners value rapid-cycle autoclaves that clear instruments in under 20 minutes. Vendors able to embed pre-set parameters for fragile composite instruments on their touchscreens gain a competitive edge.

Increasing Volume of Dental Surgeries

Implant placements, sinus lifts, and periodontal flap surgeries rose in tandem with enhanced life expectancy and a public emphasis on retaining natural dentition. Surgical packs require rigid segregation, ultrasonic cleaning, and validated biological indicator monitoring, elevating the technical bar for in-house processing units. Hospitals traditionally dominated surgical sterilization, but 2025 saw a migration toward advanced private clinics that perform chairside oral-surgery tasks, thereby expanding the installed base of tabletop sterilizers with OR-grade performance. Manufacturers now bundle vacuum-assisted drying, integrated air filters, and automatic documentation to satisfy these quasi-hospital requirements. Growth potential remains robust as emerging regions build implant dentistry programs to meet prosthetic backlog.

Stricter Infection-Control Regulations and Guidelines

Regulatory bodies tightened oversight after the COVID-19 pandemic highlighted cross-contamination risks in aerosols and waterlines. Washington State mandated annual staff competencies and low-speed handpiece motor sterilization in 2024, pushing clinics to reassess cycle repeatability and load validations. The FDA updated its consensus-standards database to include new ethylene-oxide emission thresholds, indirectly steering demand toward low-temperature alternatives. Compliance no longer revolves solely around pass-fail spore tests; digital audits require time-stamped records that cloud-connected autoclaves now generate automatically. Early adopters leverage these capabilities as marketing assets to reassure infection-conscious patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing to Third-Party Reprocessors | -0.8% | North America & Europe, limited impact in Asia-Pacific | Medium term (2-4 years) |

| High Upfront Cost of Advanced Sterilization Equipment | -1.2% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Environmental Scrutiny of Chemical Indicators & Energy Use | -0.6% | Global, with stricter enforcement in developed markets | Long term (≥ 4 years) |

| Supply-Chain Volatility for Critical Heater & Gasket Components | -0.9% | Global, with acute impact during disruption periods | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Outsourcing to Third-Party Reprocessors

Centralized reprocessing hubs promise cost savings for multi-site dentists, but they siphon capital away from in-office equipment purchases, curbing unit shipments.[3]Source: P. Sowa et al., “Disposable vs Reusable Instruments Cost Factors,” communitydentistryjournal.com Outsourced models thrive in North America and parts of Western Europe where logistics infrastructure and regulatory accreditation pathways are mature. However, clinics worry about chain-of-custody gaps and longer instrument unavailability when couriers face delays, limiting widespread take-up. Manufacturers mitigate lost revenue by supplying washer-disinfectors and packaging gear to third-party providers, thus partially offsetting lower sterilizer sales. Over the medium term, hybrid models that mix on-site rapid cycles with outsourced bulk loads could emerge.

High Upfront Cost of Advanced Sterilization Equipment

A hydrogen-peroxide plasma system can cost three times more than a mid-sized steam autoclave, burdening cash-strapped startups and under-funded public clinics. The 2025 United States 10% import tariff further inflated purchase prices, nudging buyers toward refurbished units or extended leasing contracts. Emerging Asian and African markets struggle most with capital access, slowing migration to eco-friendly technologies even as regulations tighten. Manufacturers respond by launching smaller-chamber models, pay-per-cycle billing, and bundled service warranties to dilute initial investment spikes. Nevertheless, the cost hurdle remains the largest single drag on the dental sterilization market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Instruments Anchor Core Spending

Instruments commanded 58.43% of 2025 revenue as they underpin every sterilization workflow, from ultrasonic pre-cleaners to class B vacuum autoclaves. Reusable handpieces, mirrors, and scalers create predictable replacement cycles for chamber seals, filters, and biological indicators, steadying baseline demand. Conversely, consumables and accessories, pouches, wraps, and chemistries, are surging at 7.71% CAGR as clinics prioritize single-use barriers to curb cross-contamination fears. The dental sterilization market size for consumables is predicted to grow in the coming years, reflecting continuous replenishment rather than episodic capital buys. Manufacturers cross-sell packaging supplies through auto-reorder portals embedded in sterilizer software, linking consumables revenue directly to cycle counts and improving margin visibility. Digital traceability initiatives amplify accessory uptake because practices must document every load with lot-specific indicator strips that feed audit logs.

Heat-resistant trays and racks illustrate how instruments and accessories converge; new plasma models require non-metallic tray designs, creating incremental accessory demand that complements core-unit sales. Smart cabinets capable of counting wrapped packs further interlock hardware and consumables as integrated ecosystems. Clinics that adopt chairside CAD/CAM solutions upgrade to specialized ultrasonic units tuned for milling burs, again reinforcing the dominance of instrument-centric expenditure. Although consumables and accessories hold only 41.57% share, their faster CAGR means that by 2031 they will generate comparable gross profit to capital instruments, shifting vendor revenue mixes and aftermarket strategies.

By Sterilization Method: Heat Remains Dominant but Alternatives Accelerate

Heat and steam held 44.75% revenue share in 2025 and remain practice staples because of universal regulatory acceptance and low per-cycle operating cost. Hydrogen-peroxide plasma displays 7.62% CAGR, fueled by its compatibility with fiber-optic handpieces and polymeric implant drivers that warp under high temperatures. Vendors launched sub-10-minute rapid cycles that widen plasma’s appeal beyond niche microsurgery use.

Ethylene-oxide units experience declining installations because the transitional enforcement policy imposes costly emission abatement, prompting hospitals to shrink EO capacity and clinics to bypass it entirely. Ozone and ultraviolet remain emerging modalities; neither is forecast to capture double-digit share before 2031 due to limited load capacity, but they serve as adjuncts for surface disinfection and small plastic parts. Equipment makers hedge by offering multi-modality suites in central-sterile departments, albeit smaller dental environments typically pick one primary modality.

By End User: Clinics Drive Volume; Laboratories Record Fastest CAGR

Clinics produced 61.62% of dental sterilization market size in 2025, a reflection of 1-to-2-chair practices that require compact, countertop autoclaves for daily routine loads. A typical chair generates 15-20 sterilization cycles per day, anchoring consumable turnover and making clinics indispensable volume contributors. Hospitals own higher-value but fewer units dedicated to oral-surgery suites; their demand growth is flat because most hospitals updated equipment after pandemic funding rounds in 2023-2024. Academic institutes remain a niche but stable buyer group, using research-grade validation logs for student equipment.

Dental laboratories clock an 7.94% CAGR because CAD/CAM production elevates cycle frequency and introduces high-value investment casts that mandate gentle plasma or ozone reprocessing. Automated tracking of in-process prosthetics triggers sterilizer cycles more often than clinician demand, driving chamber wear and replacement. Centralized labs that service regional practice networks adopt multi-chamber conveyor autoclaves, raising average selling prices and service contract opportunities.

Geography Analysis

North America retained 37.88% of global revenue in 2025, underpinned by sophisticated insurance systems that reimburse surgical dentistry and by state-level mandates that codify low-speed handpiece sterilization. The United States witnessed a wave of DSO capital investment, directing procurement toward IoT-connected autoclaves that align with enterprise data dashboards. Canada’s provincial infection-control updates boosted demand for class B units with vacuum drying and digital reporting, albeit at a slower pace relative to the U.S., owing to fewer practice counts. Despite saturation, replacement cycles keep North American growth positive because many clinics installed steam units between 2016 and 2018 that approach end-of-life in 2025-2026.

Europe follows with high regulatory cohesion that accelerates eco-friendly technology adoption. The dental sterilization market size in Europe is expected to grow in the coming years, reflecting growing German and French interest in hydrogen-peroxide substitutes for ethylene-oxide. Nordic regions set energy-consumption caps that favor heat-recovery autoclaves, reinforcing vendor differentiation on kilowatt-hour ratings. Southern Europe’s fragmented practitioner base still prefers refurbished equipment, tempering installed-base modernization but opening secondary-market refurbishment opportunities.

Asia-Pacific outruns every other region at an 8.15% CAGR, adding over USD 210 million in incremental revenue through 2031. China’s Healthy China 2030 plan invests in county-level dental clinics that require basic steam units, but Tier-1 cities now order plasma systems for cosmetic dentistry hubs. Japan focuses on aging-society oral surgery, upgrading to larger-capacity class B sterilizers to manage implant kits. India and Southeast Asia accelerate adoption through public-private partnership clinics that benefit from import-duty exemptions on medical devices. The Middle East and Africa post mid-single-digit growth as oil-exporting economies diversify into healthcare, funding multispecialty centers with integrated dental wings. South America shows steady albeit uneven expansion; Brazilian import regulations create periodic bottlenecks, although private insurance growth supports modern clinic builds in São Paulo and Santiago. Currency volatility remains the chief headwind in LATAM, making leasing agreements attractive versus outright capital purchase.

Regulatory Landscape

Dental sterilization equipment and reprocessing practices are shaped by public-health guidance, device regulations, and consensus standards. In the United States, FDA oversight for medical devices and its recognized consensus standards framework increasingly influence expectations for sterilizer validation and documentation, including recognition of updated moist-heat sterilization requirements (ISO 17665:2024). In February 2026, the FDA Quality Management System Regulation (QMSR) became effective, increasing the weight of harmonized, audit-ready quality systems for manufacturers supplying dental sterilization equipment, consumables, and indicators.

Outside the US, the European Union Medical Device Regulation (EU MDR) 2017/745 sets General Safety and Performance Requirements for devices supplied sterile or intended for reprocessing, reinforcing evidence-based validation for packaging and sterilization claims. Regional and state-level rules add operational specificity: Florida Board of Dentistry Rule 64B5-25.003 took effect in May 2025 with mandatory instrument sterilization and disinfection procedures, while NHS Scotland maintains SHTM 01-05 guidance for local decontamination units used in dental settings. In March 2026, ISO 10451:2026 published technical file requirements for dental implant systems, explicitly anchoring sterilization, shelf-life, and packaging documentation in product dossiers that cascade into sterilization process selection and traceability across suppliers.

Value Chain Analysis

The dental sterilization value chain begins with upstream component and material suppliers providing chamber-grade stainless steels, precision pumps and micro-valves, heaters, temperature and pressure sensors, and polymer seals designed for repeated steam and chemical exposure. As clinics and DSOs adopt data-logging and connected sterilizers, the chain becomes more dependent on embedded electronics and software, which increases exposure to shortages in high-reliability sensors and semiconductor components used in control boards and connectivity modules.

Midstream manufacturing typically combines high-skill subsystem fabrication with regulated final assembly, verification, and validation, followed by distribution through direct sales teams, dental distributors, and service networks that install, qualify, and maintain equipment. Downstream, end users (clinics, hospitals, laboratories, and academic sites) consume recurring supplies such as wraps, pouches, indicators, lubricants, and cleaning chemistries, while service partners support preventive maintenance, calibration, and documentation. Standards activity also influences packaging and compliance workflows, including EU updates to harmonized standards for sterile barrier systems and packaging (EN ISO 11607 parts 1 and 2) in March 2024 and ongoing ISO sterilization standardization work that reinforces validated processes and traceable consumables across the chain.

Competitive Landscape

The dental sterilization market exhibits moderate fragmentation. Getinge, and Midmark anchor the premium tier, leveraging robust R&D pipelines and global service networks. In April 2024, STERIS divested its dental segment for USD 787.5 million to sharpen strategic focus on hospital central-sterile operations, signaling a portfolio-optimization trend among incumbents. Getinge countered by acquiring Healthmark Industries for USD 320 million to expand its consumables footprint and strengthen aftermarket revenue. Midmark introduced next-generation M9/M11 steam units featuring touchscreens and integrated cycle-data transfer, defending its clinic stronghold.

Mid-tier challengers, including W&H and SciCan, capitalize on fast iteration cycles to ship Benchtop plasma units that meet tightening footprint constraints in urban practices. Niche innovators develop ozone-based cabinets for small plastics, targeting laboratories and orthodontic offices demanding gentle processing. Software vendors enter the space via partnerships that embed sterilizer status into practice-management dashboards, adding subscription revenue streams.

Price competition remains tempered because regulatory compliance and patient-safety stakes discourage clinics from off-brand imports. Yet in Asia-Pacific, local manufacturers offer steam units at 30% lower price, eroding western vendors’ entry-level share. Market share shifts will likely hinge on bundling: offering sterilizers with washer-disinfectors, packaging, and service contracts that reduce total cost of ownership. Green credentials, measured via energy scores and recyclable indicator programs, are rising differentiators that could redraw vendor rankings by 2030.

Dental Sterilization Industry Leaders

Dentsply Sirona Inc.

Matachana Group

Midmark Corporation

Getinge AB

A-Dec, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is compliance automation and documentation, since audit readiness increasingly depends on time-stamped cycle records, instrument traceability, and validated reprocessing instructions. The CDC infection-control framework, updated in June 2024, continues to emphasize validated sterilization methods and heat-sterilization of dental handpieces between patients using FDA-cleared devices and manufacturer instructions, aligning with sterilizers that embed cycle logging and reduce manual recordkeeping. Midmark reinforced this direction in February 2026 with commercial availability of its next-generation M9 and M11 steam sterilizers, featuring automated cycle recordkeeping and a redesigned chamber rated for 25,000 cycles, which supports clinics that need higher throughput and standardized reporting across multi-site operations.

Workflow consolidation and capacity-per-footprint improvements also create room for vendors, especially for practices dealing with staff constraints and rapid instrument turnaround from digital dentistry. Getinge highlighted this throughput theme in April 2026 by expanding validated load capacity on its GSS67N steam sterilizer platform (up to 24 trays and 600 lbs within the installed footprint), signaling that vendors are productizing higher validated loads rather than depending on larger rooms. At the same time, low-temperature approaches that avoid ethylene oxide emissions and protect heat-sensitive devices continue moving into mainstream dental settings, creating space for suppliers that can bundle sterilizers with compatible packaging, indicators, and service programs to simplify end-to-end reprocessing and reduce operator touchpoints.

Recent Industry Developments

- March 2026: Midmark announced a 2026 Sterilizer Trade-In Promotion that offered rebates for eligible sterilizer trade-ins through October 30, 2026. The program was positioned to accelerate replacement of older installed units with newer models that support tighter documentation and workflow needs, while also defending share by giving clinics a structured upgrade path.

- February 2026: Midmark launched its next-generation M9 and M11 steam sterilizers with automated cycle recordkeeping, a 5-inch touchscreen, and a redesigned chamber architecture rated for 25,000 cycles. The release reinforced the shift toward audit-ready, digitally documented sterilization in dental clinics and supported higher utilization with durability-oriented design changes.

- July 2024: Midmark launched the next-generation M9 and M11 steam sterilizers, emphasizing integrated data-logging and durability upgrades for dental practices. The update supported clinics that need consistent cycle traceability and reduced downtime as infection-control scrutiny and instrument-turnaround expectations increase.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the products and solutions used in dental care settings to clean, disinfect, and sterilize instruments and related items so they can be safely reused between patients. The market is measured in value terms in USD.

Scope exclusions: Dentistry devices used for treatment (such as imaging systems, CAD/CAM, handpieces, and implants) and general hospital sterile processing that is not linked to dental care are excluded.

Segmentation Overview

- By Product

- Instruments

- High-temperature sterilizers (autoclaves)

- Low-temperature sterilizers

- Cleaning & disinfection equipment

- Packaging equipment

- Consumables & Accessories

- Sterilization packaging & wraps

- Instrument disinfectants

- Surface disinfectants

- Sterilization indicators

- Lubricants & cleaning solutions

- Instruments

- By Sterilization Method

- Heat / Steam (≥121 °C)

- Hydrogen-Peroxide Plasma

- Ethylene Oxide

- Ozone

- Ultraviolet & Gamma Radiation

- Chemical Immersion (glutaraldehyde, peracetic)

- By End User

- Hospitals

- Clinics

- Dental Laboratories

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the starting data layer, we reviewed public sources that explain dental procedure volumes, infection prevention expectations, and device adoption patterns across regions. Helpful references included sources such as CDC infection prevention guidance, FDA device and safety communications, World Health Organization publications, OECD health statistics, and national health ministries that publish oral health indicators.

Along with these, we also used company annual reports, investor presentations, product catalogs, and trusted press coverage to understand portfolio mix, pricing ranges, and distribution routes. Patent database searches were used to track where sterilization technologies are evolving and where product cycles are active. For financial cross-checks, we used paid subscriptions for company financials and news screening, and we also referenced tender and contracts databases where public procurement signals were available. The desk sources listed here are illustrative, and additional public materials were also reviewed to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary inputs came from interviews and structured surveys with dental clinic operators, hospital dental departments, dental labs, sterilization workflow leads, and distribution-side specialists. When field observations did not align with initial assumptions, we ran follow-up contacts to tighten the estimates. Because this is a global market, coverage was balanced across major demand centers so pricing behavior, replacement cycles, and compliance practices could be checked region by region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 38% | EMEA: 36% |

| Smaller Players: 17% | Managers: 46% | Americas: 20% |

Market-Sizing & Forecasting

The core model starts from a top-down build where dental care activity and infection-control usage are translated into a demand pool, and then converted into value through typical unit needs and price ranges. In practice, procedure volumes, the number of active dental chairs and clinics, instrument turnaround intensity, and the expected frequency of sterilization cycles were used as key demand anchors. These were then mapped to sterilization equipment needs and recurring consumables.

To keep the totals realistic, results were corroborated with selective bottom-up approximations, such as sampled price points for autoclaves and related equipment, channel checks on consumables run rates, and supplier-side capacity and sales signals where they were publicly visible. When gaps appeared, especially around replacement cycles, service attachments, and emerging low-temperature use cases, assumptions were tightened using interview feedback and simple sensitivity checks. For forecasting, scenario analysis was applied around variables such as dental visit recovery, clinic expansions, compliance tightening, and equipment replacement timing. The final path was then aligned with what most primary experts considered the base case.

Data Validation & Update Cycle

Before finalizing, outputs are triangulated against independent signals such as dental procedure activity trends, regulatory and guidance changes, and supplier commentary on demand and pricing movement. Variance checks are run by region and by major product group, and any sharp jumps trigger a deeper review of unit assumptions, currency treatment, and inflation inputs. When needed, we re-validated with a small set of primary contacts.

The work is reviewed in multiple steps so the logic, math, and narrative stay aligned, and then it is signed off after anomalies are resolved. Reports are refreshed annually, with interim updates when material events occur that can move demand or pricing. Right before delivery, a final pass is completed so clients receive the most current and consistent view.

Mordor Intelligence's Dental Sterilization Market Size Compared Against Other Published Estimates

Published market sizes for dental sterilization do not always match because the counted items and the timing of the data can shift from one study to another, even when the same end market is being discussed. Differences also come from how firms treat recurring consumables versus equipment, and whether they anchor demand on dental activity signals or on supplier-side revenue splits.

Dental infection control categories that are not specific to sterilization, such as broad barrier products and general dental disposables, sit outside Mordor Intelligence's scope. This narrows the model to sterilization-led equipment and related workflow needs and reduces double counting. Other estimates may use a faster price escalation assumption for consumables, apply different currency conversion timing, or project aggressive adoption of advanced low-temperature systems without validating replacement cycles through clinic-side checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.78 B (2026) | |

| Industry Publisher A | USD 1.63 B (2024) | Uses an earlier base year and may blend adjacent dental infection control categories into the same total, which can compress or expand the apparent sterilization value depending on what is counted as sterilization-specific. |

| Global Publisher B | USD 1.68 B (2025) | Starts from a different base year and can apply broader product baskets and longer forecast windows, which changes how replacement cycles, service add-ons, and price movement are reflected in the starting market value. |

Across the three figures, the spread is mainly explained by what is included in the product basket and how the base year is set. That then affects how prices and replacement timing carry through the model. By keeping the demand build tied to observable dental activity and by stress-testing key assumptions with field feedback, the resulting number stays traceable to clear inputs that can be repeated and updated with each refresh.

Key Questions Answered in the Report

What is the projected value of the dental sterilization market by 2031?

The market is expected to reach USD 2.47 billion by 2031 based on a 6.71% CAGR during 2026-2031.

Which region is the fastest-growing in dental sterilization equipment demand?

Asia-Pacific leads growth with an 8.15% CAGR through 2031, driven by aging populations and expanding dental-insurance coverage.

Why are hydrogen-peroxide plasma sterilizers gaining popularity?

They process heat-sensitive instruments at low temperatures and avoid ethylene-oxide emissions, aligning with tighter environmental guidelines.

Which product segment currently holds the largest revenue share?

Instruments dominate with 58.43% of 2025 revenue because every practice relies on reusable tool reprocessing.

How are stricter regulations influencing purchasing decisions?

New guidelines mandate documented, fail-safe sterilization processes, pushing clinics toward smart autoclaves that automatically record cycle data for compliance audits.

What is driving the rapid growth of the dental laboratory segment?

The integration of CAD/CAM workflows demands quick instrument turnarounds and precise low-temperature sterilization, leading to an 7.94% CAGR for laboratories.

Page last updated on: