Pediatric Perfusion Products Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

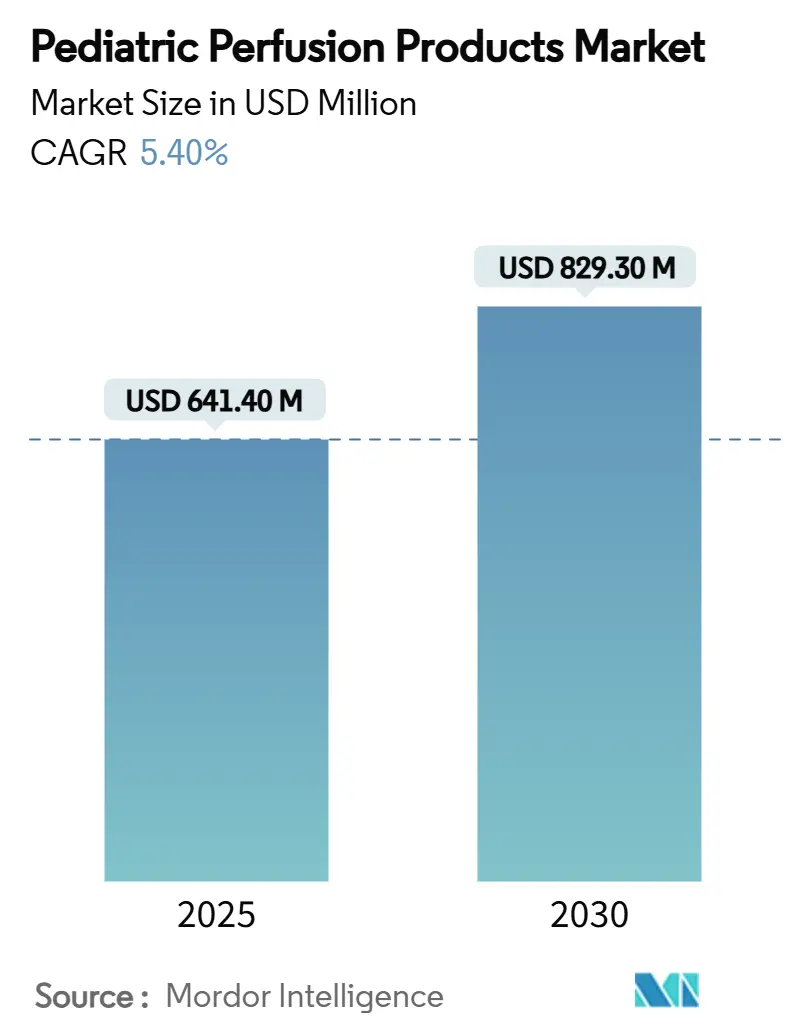

| Market Size (2025) | USD 641.40 Million |

| Market Size (2030) | USD 829.30 Million |

| Growth Rate (2025 - 2030) | 5.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Perfusion Products Market Analysis by Mordor Intelligence

The paediatric perfusion products market size stands at USD 641.4 million in 2025 and is forecast to reach USD 829.3 million by 2030, reflecting a 5.4% CAGR. Widening clinical use in cardiothoracic surgery, neonatal respiratory support, and emergency extracorporeal resuscitation underpins steady demand. At the same time, hospitals increasingly favour purpose-built devices over miniaturized adult circuits to improve outcomes and cut transfusion needs. Technological advances—especially low-priming-volume oxygenators, non-heparin coatings, and compact pumps—have reduced inflammatory sequelae, shortened ICU stays, and enabled in-hospital mobility during support. Regulatory tailwinds are visible in the United States, where the FDA expanded mechanical circulatory support indications for children ≥30 kg in late 2024, signaling a more predictable approval environment. Capacity building across Asia Pacific is accelerating; several new centres of excellence in Vietnam, India, and China are narrowing access gaps and fueling equipment tenders. At the same time, supply-chain fragility and a tightening perfusionist labour pool temper growth prospects, pressing manufacturers to localize component sourcing and automate routine workflow steps.

Key Report Takeaways

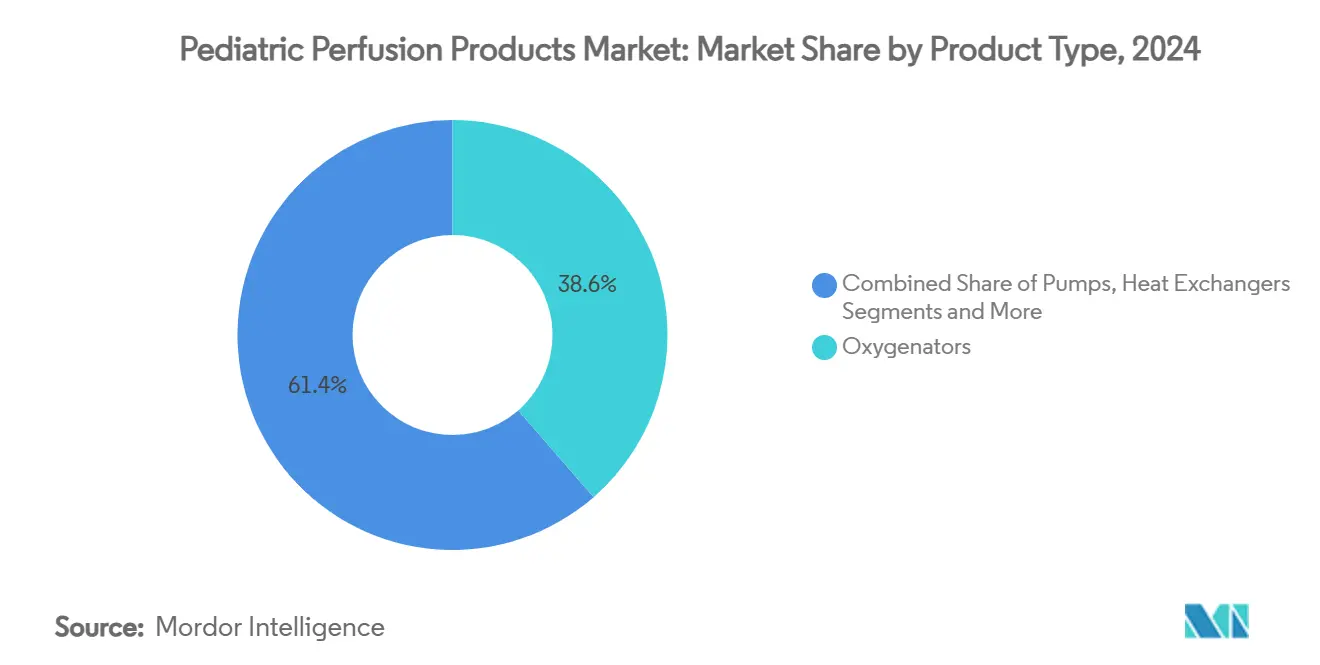

- By product type, oxygenators captured a 38.6% revenue share in 2024, while tubing and cannulae are poised for a 6.4% CAGR to 2030.

- By patient age group, neonates commanded 46.2% of paediatric perfusion systems market share in 2024; ECMO technology is projected to expand at a 5.9% CAGR through 2030.

- By perfusion technology, cardiopulmonary bypass held a 54.1% share of the paediatric perfusion systems market in 2024, and ECMO is advancing at a 5.9% CAGR through 2030.

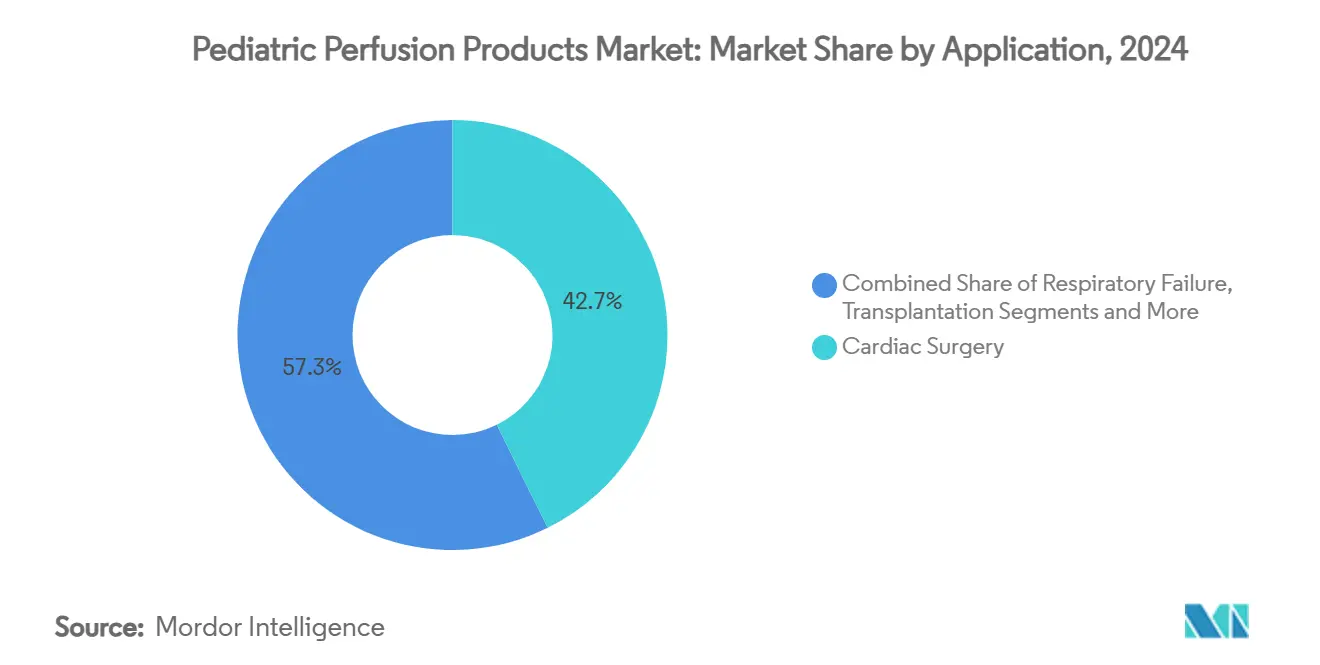

- By application, cardiac surgery accounted for a 42.7% slice of the paediatric perfusion systems market size in 2024, and respiratory failure support is set for a 6.3% CAGR through 2030.

- By end user, paediatric cardiac centres represented 37.4% of the revenue share in 2024, whereas ambulatory surgical centres are forecast to log a 5.1% CAGR to 2030.

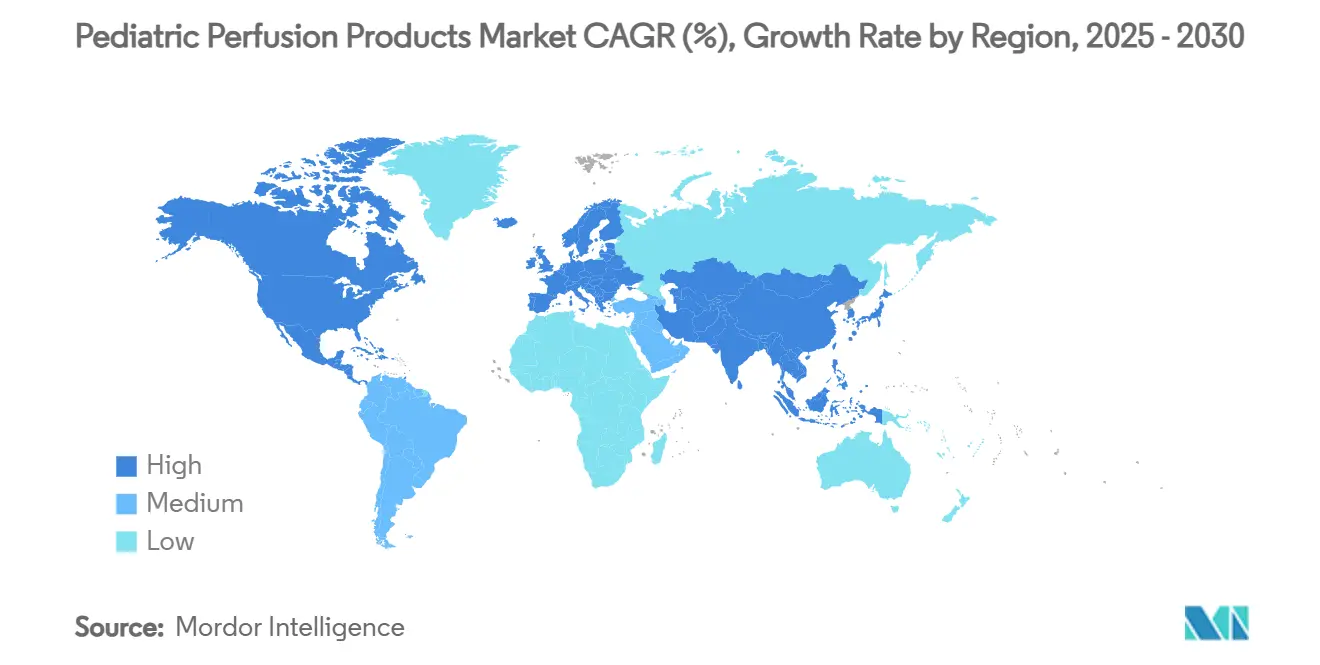

- By geography, North America led with 40.3% paediatric perfusion systems market share in 2024; Asia Pacific is on track for the fastest 7.3% CAGR to 2030.

Global Pediatric Perfusion Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in congenital heart defect (CHD) procedures | +1.20% | Global; high intensity in Asia Pacific | Medium term (2-4 years) |

| Miniaturised oxygenator & circuit innovations | +0.90% | North America, EU; rapid uptake in Asia Pacific | Short term (≤ 2 years) |

| Expansion of paediatric cardiac centres in EMs | +1.10% | Asia Pacific core; spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Goal-directed perfusion protocols boost disposables | +0.70% | Global; early use in developed markets | Medium term (2-4 years) |

| Rise of ECMO retrieval teams for neonatal transport | +0.80% | North America & EU; expanding in emerging metros | Short term (≤ 2 years) |

| Philanthropy-backed outcome-based funding in LMICs | +0.60% | Sub-Saharan Africa, South-East Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Congenital Heart Defect (CHD) Procedures

Improved prenatal screening and AI-enabled echocardiography drive earlier CHD detection, pushing surgical volumes higher even in low-resource settings. A multicountry study involving 3,068,075 children reported 0.130% CHD prevalence and revealed a negative correlation with local GDP, underscoring demand in poorer regions.[1]Honglin Song et al., “Early Diagnosis and Treatment of Asymptomatic CHD,” doi.org Early correction improves growth indices, encouraging policymakers to prioritise timely surgery budgets. In parallel, hybrid cath-lab–operating-room techniques require perfusion consoles that switch seamlessly between partial and full bypass. These combined forces amplify the need for adaptable, paediatric-specific circuits.

Miniaturized Oxygenator & Circuit Innovations

Cutting priming volume from conventional 213 ml to 102 ml curbs haemodilution, lowers transfusion exposure and shortens ICU recovery. Microfluidic multilayer oxygenators sustaining 480 ml/min blood flow show superior gas transfer and smoother shear profiles. Real-world data indicate that 49% of 5–20 kg children avoid transfusion when such circuits are used, anchoring miniaturization as a primary differentiator. Antithrombogenic polymers that obviate heparin further shrink complication risk and align with supply-chain resilience strategies amid global heparin volatility.

Expansion of Paediatric Cardiac Centres in EMs

Government grants and philanthropic support are multiplying specialist hubs in Vietnam, India, and other emerging markets, thereby localizing treatment for an estimated 240,000 Indian neonates born with CHD each year.[2]Children’s HeartLink, “2023 Annual Report,” childrensheartlink.org Australia’s USD 50 million Artificial Heart Frontiers Program shows advanced economies also backing paediatric-focused R&D that will cascade into export markets.[3]Mark Butler, “$50 million to develop world-leading artificial heart,” Australian Government, health.gov.au . . . . . . . New Research Tele-mentoring and VR surgical training bolster workforce readiness, while public-private financing spreads acquisition costs across multiyear outcome-based contracts.

Goal-Directed Perfusion Protocols Boost Disposables

FDA-cleared monitoring systems such as CDI OneView present 22 live parameters—including oxygen extraction ratio—allowing clinicians to individualize flows and hematocrit targets in real time [TERUMO.COM]. Continuous blood-gas-monitored pumps that meet CLIA standards demonstrate tighter pH and lactate control versus intermittent sampling. As centres embed these protocols in quality dashboards, demand rises for single-use oxygenators, precision tubing, and inline sensors certified for extended runtime, reinforcing consumable revenue visibility.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of paediatric perfusion systems | -0.80% | Global; most acute in smaller and emerging centres | Medium term (2-4 years) |

| Limited reimbursement for neonatal ECMO | -0.60% | North America & EU; knock-on globally | Long term (≥ 4 years) |

| Global heparin supply volatility | -0.40% | Worldwide; Asia Pacific production concentration | Short term (≤ 2 years) |

| Post-COVID perfusionist workforce attrition | -0.70% | North America & EU; signs of spread to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Paediatric Perfusion Systems

Advanced neonatal ECMO consoles often exceed USD 300,000, a figure beyond many district hospitals, especially where annual CHD caseloads are under 100 procedures. Higher unit costs stem from limited production runs, paediatric-specific R&D and stringent validation protocols. In addition, service contracts and mandatory disposables elevate total cost of ownership. Manufacturers are reacting by offering lease-to-own schemes and introducing modular designs that share pumps or monitors across circuits, but affordability remains a gating factor for smaller buyers.

Limited Reimbursement for Neonatal ECMO

Payment frameworks lag clinical practice in several high-income markets. In the United States, 78% of ECMO claims still funnel through peripheral-support MS-DRG codes that do not fully capture resource utilization. While the FDA’s Transitional Coverage pathway for breakthrough paediatric devices promises earlier coverage, evidence thresholds and lengthy rule-making dilute near-term impact. The resulting financial uncertainty discourages hospitals from adding capacity despite proven survival gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oxygenators Anchor Revenue

Oxygenators retained a 38.6% revenue lead in 2024 as gas exchange efficiency remains the prime determinant of circuit safety and efficacy. By virtue of continuous innovation—biomimetic hollow fibres, microfluidic layers, and ultra-low priming reservoirs—vendors drive down transfusion dependence and inflammatory markers. Growth is further propelled by the inclusion of pre-installed coatings that reduce systemic heparin dose, a critical advantage amid anticoagulant shortages. The tubing & cannulae category is forecast for 6.4% CAGR to 2030 on the back of minimally invasive paediatric cannulation and widespread ECMO transport teams demanding flexible yet kink-resistant lines. Reservoirs, pumps, and heat exchangers, though slower growing, benefit from an industry pivot to integrated modules that allow rapid set-up on limited OR footprints.

Second-generation devices increasingly embed RFID tracking for disposables, improving inventory audits and supporting outcome-based contracts. As real-time analytics gain currency, manufacturers bundle disposable oxygenators with cloud-enabled dashboards, locking in recurring revenue from data subscriptions. With most high-volume cardiac centres averaging 350–400 paediatric cases yearly, consumables represent a predictable annuity stream, cushioning capital-equipment cyclicality.

By Perfusion Technology: ECMO Outpaces Conventional Bypass

Cardiopulmonary bypass continued to account for 54.1% of procedures in 2024, underscoring its entrenched role in open-heart repair. Nonetheless, ECMO utilization is climbing at a 5.9% CAGR as indications broaden to respiratory failure, bridge-to-transplant, and extracorporeal CPR. Portable systems weighing under 10 kg enable intra-hospital transfers without circuit disconnection, thus widening eligibility to centres lacking fixed OR-adjacent pump rooms. In addition, the FDA’s December 2024 clearance of paediatric Impella pumps signals expanding hybrid support strategies combining short-term ventricular unloading with oxygenation.

Ventricular assist devices, while niche, fill a gap for chronic heart-failure patients awaiting donor organs. Novel isolated-organ perfusion platforms, primarily used in research, are being evaluated for metabolic support in sepsis and traumatic injury. Collectively, these advances diversify the perfusion toolbox, compelling hospitals to maintain multipurpose consoles capable of switching between modalities with minimal hardware swaps.

By Application: Respiratory Failure Segment Gains Traction

Cardiac surgery remains the backbone application at 42.7% of 2024 volumes, reflecting persistent CHD prevalence and complexity. Yet neonatal respiratory distress and acute lung injury cases are accelerating, pushing respiratory-failure support toward a 6.3% CAGR as clinicians embrace ECMO to reduce ventilator-induced lung damage. The paediatric perfusion systems market size for respiratory care is projected to cross USD 260 million by 2030, reflecting the modality’s growing footprint inside NICUs. Transplantation support stays steady, aided by the FDA-approved Organ Care System that recorded 94% six-month survival in paediatric recipients.

Trauma and emergency departments are piloting extracorporeal CPR after paediatric cardiac surgery, with American Heart Association registry data showing superior survival to conventional measures. Broader clinical adoption depends on protocol standardization and rapid-deployment training, but could unlock significant incremental circuit sales.

By End User: Ambulatory Streams Gather Momentum

Paediatric cardiac centres handled 37.4% of global cases in 2024, leveraging concentrated expertise and multipronged funding to replace legacy heart-lung machines with miniaturized platforms—such centres also pioneer outcome-linked procurement, embedding performance clauses that reward reduced transfusion and shorter ICU stay. Children’s hospitals maintain a sizeable share owing to integrated NICUs and PICUs, but ambulatory surgical centres are advancing at a 5.1% CAGR as procedure complexity falls for select repairs and catheter-based interventions. These facilities need compact, quick-priming circuits and user-friendly controls to manage mixed-skill staffing.

Academic institutes contribute to early-stage testing of smart algorithms and fill workforce gaps through fellowship programs. Registry initiatives like PediPERFORM document best practices, accelerate knowledge diffusion, and influence capital procurement criteria.

Geography Analysis

North America commanded 40.3% of paediatric perfusion systems market share in 2024, benefiting from dense tertiary cardiac centres, robust private insurance and rapid regulatory approvals. Continued growth hinges on mitigating perfusionist shortages through advanced training and partial automation. Consolidation among group purchasing organizations is fostering bulk-buy contracts that favour vendors with broad portfolios but exacting service-level guarantees.

Asia Pacific will post the fastest 7.3% CAGR through 2030 as China scales paediatric surgery capacity and India tackles its annual birth cohort of 240,000 CHD infants. Public tenders increasingly specify local-content thresholds, prompting multinationals to expand regional assembly. Philanthropy-funded hubs in Vietnam exemplify sustainable mixed-financial models that pair technology donations with local skills transfer.

Europe maintains steady mid-single-digit growth driven by well-funded national health services and cohesive MDR/IVDR compliance pathways. Middle East & Africa and South America together represent a double-digit unmet need. International NGOs are piloting outcome-based reimbursement and cross-border referral networks to bridge capacity deficits. Global cardiac-surgical targets of 4.0 procedures per 100,000 population for LMICs underscore long-run upside if financing and workforce hurdles are resolved.

Competitive Landscape

The paediatric perfusion systems industry remains moderately fragmented; the top five players control roughly significant global revenue. Medtronic leads in ECMO and disposable oxygenators, reinforced by the 2024 VitalFlow launch featuring biocompatible, non-heparin coatings. Terumo leverages CDI OneView integration to differentiate with data analytics, while Getinge’s 2024 exit from surgical perfusion opens white space for niche manufacturers to gain share.

LivaNova’s withdrawal from circulatory support highlights profitability challenges in low-volume, high-complexity paediatric segments but frees investment for more scalable neuro-modulation lines. Strategic acquisitions continue: Bridge to Life bought VitaSmart in December 2024 to add a compact console aimed at European ambulatory centres.

Vendors are also embedding AI-driven flow optimization and predictive alarm systems to win value-based contracts that tie reimbursements to complication rates and ICU length-of-stay metrics. Overall, competition is shifting from hardware specification wars toward holistic outcome packages combining disposables, software, and remote clinical support.

Pediatric Perfusion Products Industry Leaders

Medtronic

Terumo Corporation

Getinge AB

LivaNova

Fresenius SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Johnson & Johnson MedTech gained FDA approval to extend Impella 5.5 and Impella CP use to children with cardiogenic shock, broadening short-term ventricular support options.

- December 2024: Bridge to Life closed its acquisition of Medica SpA’s VitaSmart perfusion system, expanding its European footprint.

- September 2024: Medtronic unveiled the VitalFlow ECMO system with a non-heparin surface and mobility features for intra-hospital transport

Global Pediatric Perfusion Products Market Report Scope

| Oxygenators |

| Pumps |

| Heat Exchangers |

| Tubing & Cannulae |

| Reservoirs & Accessories |

| Cardiopulmonary Bypass (CPB) |

| Extracorporeal Membrane Oxygenation (ECMO) |

| Ventricular Assist Devices (VADs) |

| Isolated Organ Perfusion |

| Others |

| Cardiac Surgery |

| Respiratory Failure |

| Transplantation Support |

| Sepsis & Severe Infection |

| Trauma & Emergency |

| Paediatric Cardiac Centres |

| Children's Hospitals |

| Ambulatory Surgical Centres |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Oxygenators | |

| Pumps | ||

| Heat Exchangers | ||

| Tubing & Cannulae | ||

| Reservoirs & Accessories | ||

| By Perfusion Technology | Cardiopulmonary Bypass (CPB) | |

| Extracorporeal Membrane Oxygenation (ECMO) | ||

| Ventricular Assist Devices (VADs) | ||

| Isolated Organ Perfusion | ||

| Others | ||

| By Application | Cardiac Surgery | |

| Respiratory Failure | ||

| Transplantation Support | ||

| Sepsis & Severe Infection | ||

| Trauma & Emergency | ||

| By End User | Paediatric Cardiac Centres | |

| Children's Hospitals | ||

| Ambulatory Surgical Centres | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected global demand for paediatric perfusion consoles by 2030?

Installations are expected to support a paediatric perfusion systems market size of USD 829.3 million by 2030, reflecting a 5.4% CAGR.

Which geographic region is poised for the fastest expansion?

Asia Pacific will grow at 7.3% CAGR, driven by large CHD caseloads and new centres of excellence.

Why are miniaturised oxygenators considered critical for neonates?

Low-priming-volume designs cut haemodilution, reduce transfusions and improve postoperative recovery.

How is regulatory policy influencing adoption in the United States?

Recent FDA clearances, including expanded Impella indications and new ECMO systems, provide clearer approval pathways and reimbursement prospects.

What challenge does the workforce shortage pose to providers?

A 12% reduction in certified perfusionists since 2020 is delaying surgeries and pushing hospitals toward semi-automated monitoring solutions.

Which product category holds the largest revenue share?

Oxygenators remain the top-selling component, accounting for 38.6% of 2024 revenue due to continuous gas-exchange innovation.

Page last updated on: