Philippines Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

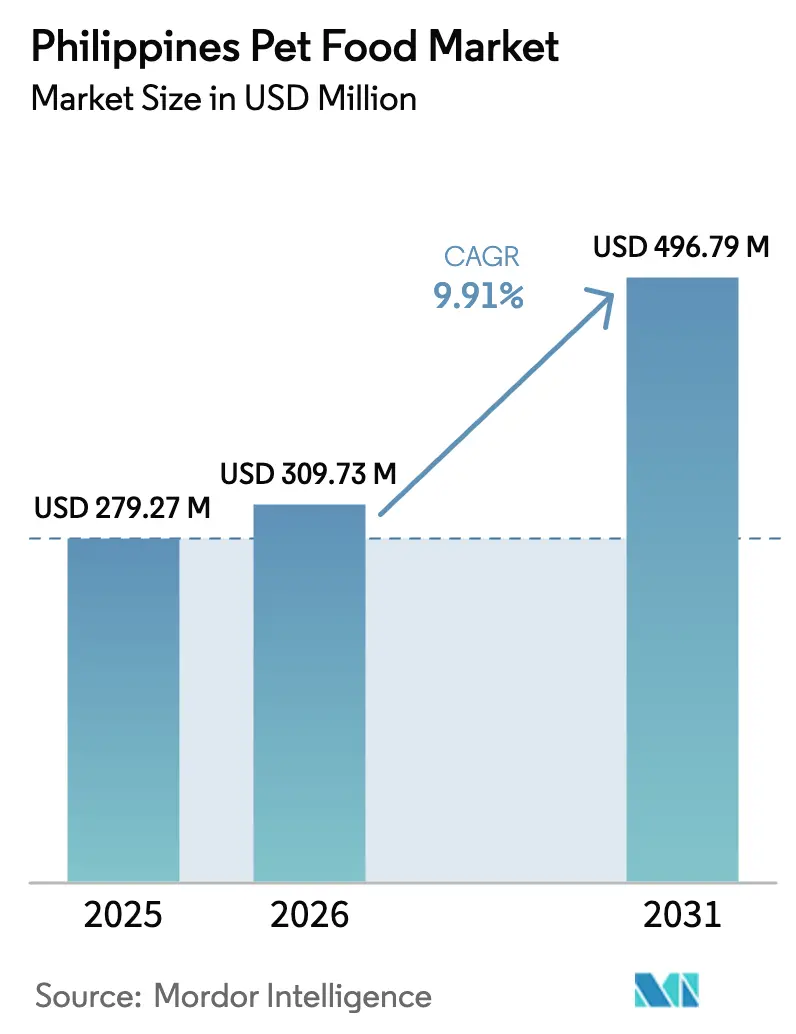

| Base Year Market Size (2025) | USD 279.27 Million |

| Market Size (2026) | USD 309.73 Million |

| Market Size (2031) | USD 496.79 Million |

| Growth Rate (2026 - 2031) | 9.91% CAGR |

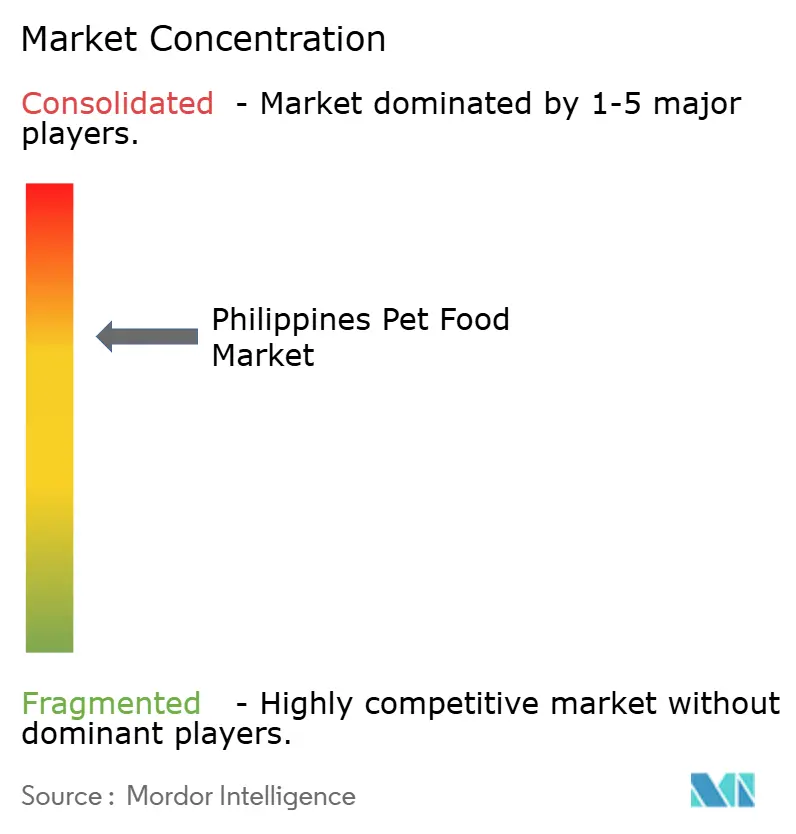

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Philippines Pet Food Market Analysis by Mordor Intelligence

The Philippines pet food market size is projected to expand from USD 279.27 million in 2025 and USD 309.73 million in 2026 to USD 496.79 million by 2031, registering a 9.91% CAGR between 2026 to 2031. Pet humanization, a large dog population, and the rapid spread of modern retail underpin solid volume gains, while government crackdowns on unregistered imports help credible brands reclaim share. Feed-millers reallocating idle extrusion lines, combined with incentives under the Animal Industry Development and Competitiveness Act, are broadening local supply and lowering ingredient costs. E-commerce platforms, led by Shopee, Lazada, and TikTok Shop, deepen reach into secondary cities despite stronger surveillance of gray-market listings. Nevertheless, the Philippines' pet food market continues to wrestle with high price sensitivity, table-scrap feeding habits, and slow Bureau of Animal Industry (BAI) approvals that stretch product launch windows by as much as a year. These cross-currents leave ample headroom for veterinary telehealth, subscription services, and functional treats that translate human wellness trends into pet nutrition.

Key Report Takeaways

- By pet food product, food commanded 55.6% of the Philippines pet food market share in 2025 and is on track to grow at an 11.7% CAGR through 2031, easily outpacing treats and supplements.

- By pets, dogs held 61.8% of the Philippines pet food market size in 2025, and are set to advance at an 11.8% CAGR to 2031, reinforcing their dominance in Filipino households.

- By distribution channel, supermarkets and hypermarkets led with 37.2% revenue share in 2025, and the online channel will grow the fastest at an 11.6% CAGR through 2031 on the back of free shipping promotions and rising digital adoption.

- The market is moderately concentrated, with Mars, Incorporated, Charoen Pokphand Foods Public Company Limited (Perfect Companion Group Co., Ltd.), Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.), General Mills, Inc. (Blue Buffalo Pet Products, Inc.), and Nestlé Purina PetCare collectively accounting for a significant share of the Philippines pet food market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and premium-nutrition spend | +1.9% | National, strongest in Metro Manila, Cebu, and Davao | Medium term (2–4 years) |

| Expansion of modern retail and e-commerce | +1.7% | Nationwide, early gains in Metro Manila, Calabarzon, and Central Luzon | Short term (≤ 2 years) |

| Growing dog and cat population | +1.0% | Nationwide | Long term (≥ 4 years) |

| Feed-millers converting idle capacity into pet-food lines | +0.9% | Manufacturing hubs in Luzon and Mindanao | Medium term (2–4 years) |

| Surge in veterinary tele-health and pet insurance | +0.7% | Metro Manila, Cebu, and Davao with spillover into provinces | Medium term (2–4 years) |

| Government incentive program for domestic meat by-product rendering | +0.5% | Nationwide, key plants in Luzon and Mindanao | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Premium-Nutrition Spend

Filipino pet owners increasingly regard their pets as family members, demonstrating a strong preference for pampering them and prioritizing products that improve their pets' health and hygiene. This trend is particularly evident in the dog food segment, where significant growth in health-focused product offerings is anticipated during the forecast period. According to Agriculture and Agri-Food Canada (AAFC), the pet population in the Philippines grew from 56.3 million in 2020 to 65.9 million in 2024. In 2024, cats and dogs accounted for 35.0% of the total pet population, while other pets made up 65.0%. By 2029, the cat and dog populations are projected to reach 3.2 million and 24.3 million, respectively[1]Source: Agriculture and Agri-Food Canada, "Sector Trend Analysis – Pet food in the Philippines," agriculture.canada.ca. The development of pet food is anticipated to mirror trends in human food, with a growing interest in vegan diets for pets emerging in the local market. Additionally, veterinary diets targeting renal, digestive, and weight management issues are following a similar premiumization trend. This sustained growth reflects the positive outlook for the Philippine pet food market, supported by rising disposable incomes.

Expansion of Modern Retail and E-Commerce

The expansion of supermarkets and hypermarkets has reduced the prominence of traditional wet markets, which primarily sold bulk rice and table scraps, thereby providing packaged brands with significant shelf space. In 2021, the Philippines' eCommerce market sales for all product categories reached USD 17 billion, driven by 73 million active online users[2]Source: International Trade Administration, "Philippines Country Commercial Guide," trade.gov . This growth continued despite regulatory warnings from the Bureau of Animal Industry (BAI) and other authorities about counterfeit products, which remained a significant concern for consumers. Pilmico Foods reported year-over-year sales growth in 2022 following the online-exclusive launch of Maxime dog food, highlighting the benefits of digital channels. Additionally, subscription models like McDuffy’s fresh-meal plan cater to affluent pet owners who prioritize convenience and ingredient transparency.

Growing Dog and Cat Population

With one of the highest dog and cat ownership rates in Asia, the Philippines offers significant growth opportunities for the pet food market. As pets have become increasingly popular household companions, particularly during the pandemic, pet ownership and pet food sales have grown significantly over the past five years. The number of households owning cats rose from 1.7 million in 2020 to 2.0 million in 2024, reflecting an increase in the percentage of households owning cats from 6.5% to 7.0% during the same period[3]Source: Agriculture and Agri-Food Canada, "Sector Trend Analysis – Pet food in the Philippines," agriculture.canada.ca. Ongoing rabies vaccination drives by the Department of Health have formalized and encouraged pet owners to visit veterinary clinics, thereby driving demand for commercial pet nutrition. Additionally, trap-neuter-return programs for stray animals have expanded the consumer base by introducing newly adopted pets, even though initial purchases often focus on entry-level price points.

Surge in Veterinary Tele-Health and Pet Insurance

Pet insurance penetration in the Philippines remains minimal, with only a small percentage of pet owners opting for coverage. Over the years, several financial institutions have introduced policies at varying price points to cater to different customer needs. Life by Petto offers a subscription service that includes unlimited teleconsultations, emphasizing premium diet formulas through tailored dietary recommendations. Virtual consultations make professional advice more affordable, providing it in rural areas where the availability of veterinarians is significantly lower than in urban centers like Metro Manila. This increased accessibility is encouraging more pet owners to adopt therapeutic and functional diets, thereby supporting the overall growth of the pet food market in the Philippines.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity and table-scrap feeding | −1.6% | Nationwide, acute in rural Luzon, Visayas, and Mindanao | Long term (≥ 4 years) |

| Lengthy Bureau of Animal Industry (BAI) product registration | −0.8% | Nationwide | Medium term (2–4 years) |

| Counterfeit and gray-market products eroding trust | −0.6% | Metro Manila, Calabarzon, and nationwide online channels | Short term (≤ 2 years) |

| Low veterinarian density in Visayas and Mindanao | −0.4% | Visayas and Mindanao | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Bureau of Animal Industry (BAI) Product Registration

Each new stock-keeping unit requires a Certificate of Feed Product Registration (CFPR), along with individual product clearance, a process that takes 6 to 12 months and incurs annual fees[4]Source: Bureau of Animal Industry, “Feed Regulations and Product Registration Requirements,” bai.gov.ph. Importers are also required to provide certificates of free sale, good manufacturing practice documentation, and veterinary health assurances. These regulatory measures are intended to ensure consumer safety and maintain product quality. However, they significantly delay innovation pipelines for global companies such as Nestlé Purina PetCare, limiting their ability to introduce new products to the market efficiently. At the same time, non-compliant sellers introduce products into online marketplaces without obtaining the necessary approvals, creating unfair competition and hindering the advancement of the pet food market in the Philippines. This dual challenge of stringent regulations and non-compliance disrupts the market's growth trajectory and slows industry modernization.

Counterfeit and Gray-Market Products Eroding Trust

The Bureau of Animal Industry (BAI) issued an advisory highlighting the presence of multiple unregistered pet food products on platforms such as Shopee, Lazada, and TikTok Shop. These products often feature fraudulent labels that conceal substandard protein sources or expired stock, posing risks to animal health. With fewer than 50 inspectors overseeing thousands of outlets, enforcement efforts remain insufficient, making it challenging to ensure compliance across the market. Although premium brands have begun incorporating QR codes for authentication to enhance product credibility, consumer awareness of these measures remains limited. This lack of trust significantly impacts the Philippines pet food market's fastest-growing channel, online retail, where consumer confidence is essential for premium-priced transactions. The growing prevalence of unregistered products underscores the need for stricter regulatory measures and increased consumer education to safeguard animal health and foster trust in the online retail space.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Food Product: Food Segment Anchors Growth Amid Premiumization

Food is the largest pet food product segment, accounting for 55.6% of the Philippines pet food market share in 2025, and is growing fastest at an 11.7% CAGR through 2031. Dry kibble dominates because its shelf life aligns with the tropical climate, and its price fits middle-income budgets. Wet formats stay niche, given the higher cost per calorie and limited cold-chain capacity outside the top three cities. Nestlé Purina PetCare’s ongoing PHP 6 billion (USD 107 million) capacity expansion in 2026 underscores confidence that premium dry offerings will continue to drive overall market value upward.

Treats and functional supplements benefit from increased training activities and the use of human-grade ingredients. Although supplements account for a smaller share of spending, probiotic powders and omega-3 chews are expanding briskly among urban millennials. Pet veterinary diets, prescribed for conditions such as diabetes, renal disease, urinary tract disease, obesity, and dermatological issues, encounter adoption challenges due to high costs and a low density of veterinarians in Visayas and Mindanao, which limits access to prescription recommendations.

By Pets: Dogs Continue to Lead While Cats Gain Momentum

Dogs are the largest pet segment and generated 61.8% of the Philippines pet food market share in 2025, and are growing fastest at an 11.8% CAGR through 2031, testifying to their deep cultural and security roles. The dog population is primarily located in urban and peri-urban areas, where increasing pet humanization is fueling demand for premium kibble, functional treats, and veterinary diets.

Cats, though fewer in number, remain underserved, with cat food sales facing limited competition from local manufacturers who prioritize dog nutrition due to higher sales volumes. Increasing awareness about feline care is expanding the cat segment within the Philippines pet food market and is projected to support future growth as dog ownership approaches saturation. Other pets, such as birds, rabbits, and small mammals, currently represent a minimal share of the market but are gaining attention from specialty retailers like Pet Warehouse, which offers food products tailored to niche dietary requirements.

By Distribution Channel: Supermarkets/Hypermarkets Sustain Lead as Online Scales Quickly

Supermarkets and hypermarkets are the largest distribution channel, accounting for 37.2% of the Philippines pet food market size in 2025, reflecting their national footprint and aggressive loyalty programs. Chains such as SM Supermarket allocate multiple aisles to pet nutrition, giving mass brands consistent exposure. The Philippines pet food market size within brick-and-mortar formats, therefore, retains inertia despite digital advances.

Conversely, the online channel registers the fastest growth, with a 11.6% CAGR through 2031. Free shipping thresholds and cash-on-delivery options lure provincial consumers who lack specialty stores. Yet regulatory advisories about counterfeit items pressure platforms to vet sellers more rigorously. Compliance enhancements will determine how swiftly e-commerce’s contribution to the Philippines pet food market. Veterinary clinics and pet grooming salons also distribute prescription diets and therapeutic formulas. These channels attract customers who prioritize veterinarian recommendations over retail shelf options, as they often provide expert advice and tailored solutions for specific pet health needs.

Geography Analysis

Metro Manila, Calabarzon, and Central Luzon are anticipated to contribute a major portion of the overall revenue during the projected period. The capital region is known for its extensive network of veterinarians who often recommend high-quality, specialized diets for pets. This has led to a significant increase in average monthly pet care expenditures. Additionally, Nestlé Purina PetCare's (Nestlé S.A.) Cabuyao facility's local manufacturing operations play a crucial role in ensuring a consistent and reliable supply chain. This strategic advantage further establishes Luzon as a significant export hub catering to countries across Southeast Asia.

Visayas and Mindanao trail because logistics markups push shelf prices higher than in Luzon. The proposed Universal Robina plant in Mindanao tackles that handicap by slashing freight costs and creating a supply base closer to Davao and Cagayan de Oro. Cebu emerges as the central archipelago’s retail hub, where specialty chains and telehealth start-ups increasingly converge, laying the groundwork for premium growth.

Rural municipalities across all island groups remain largely underdeveloped, with commercial penetration at a minimal level. A substantial fund has been allocated to upgrade rendering capabilities, aiming to enhance ingredient self-sufficiency. This initiative aims to enable producers to offer starter kibble at more affordable prices in local sari-sari stores. Successfully addressing these areas is anticipated to significantly expand the pet food market in the Philippines while addressing and reducing disparities in regional consumption patterns.

Competitive Landscape

The market shows moderate concentration. Mars, Incorporated, Charoen Pokphand Foods Public Company Limited (Perfect Companion Group Co., Ltd.), Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.), General Mills, Inc. (Blue Buffalo Pet Products, Inc.), and Nestlé Purina PetCare collectively controlled a significant market share in 2025. Intensified price competition in the mass market segment has prompted incumbents to offer bundled loyalty points, larger bag formats, and additional promotional incentives. These strategies aim to retain customer loyalty, attract price-sensitive consumers, and strengthen their competitive position.

Investment activity remains lively. Nestlé Purina PetCare’s PHP 6 billion (USD 107 million) plant expansion in 2025 boosts local extrusion and shortens lead times, sharpening its edge against import-reliant rivals. Universal Robina Corporation (JG Summit Holdings, Inc.) and San Miguel Foods, Inc. retrofit feed-mill lines rather than erect entirely new facilities, trimming capital outlays and speeding time-to-market. E-commerce exclusive partnerships, such as Pilmico’s Maxime line on Shopee, sidestep shelf wars and tap digital demographics newly comfortable with cashless payments.

Innovation in the pet food market focuses on credibility and convenience. Brands are incorporating QR codes to ensure authenticity, demonstrating their commitment to combating counterfeiting. Fresh-meal start-ups, such as McDuffy, offer human-grade pet food on a subscription basis, catering to pet owners seeking premium, tailored nutrition. Similarly, Life by Petto integrates teleconsultations with diet plans, providing personalized dietary solutions and enhancing customer engagement by combining services with product offerings. As a result, the pet food market in the Philippines is transitioning from a basic commodity segment to a multifaceted ecosystem of products, platforms, and related services, reflecting a growing emphasis on quality, customization, and added value.

Philippines Pet Food Industry Leaders

-

Mars, Incorporated

-

Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

-

Charoen Pokphand Foods Public Company Limited (Perfect Companion Group Co., Ltd.)

-

General Mills, Inc. (Blue Buffalo Pet Products, Inc.)

-

Nestlé Purina PetCare (Nestlé S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Aboitiz Foods, a subsidiary of Philippines-based Aboitiz Equity Ventures Inc., acquired Singapore-based Diasham Resources Pte. Ltd., enhancing its pet food and animal nutrition business. This acquisition enables Aboitiz to improve its pet food product lines, including Maxime, Tommy, and Woofy, by incorporating Diasham's specialized additives.

- November 2025: Real Pet Food Company (RPF) has introduced Fresh(labs), the first research and development initiative in the Asia-Pacific region, including the Philippines, focused on fresh pet nutrition. This multi-million-dollar investment is designed to enhance the science, education, and innovation in pet food.

- January 2025: Nestlé Purina PetCare has committed PHP 6 billion (approximately USD 107 million) to enhance its local operations in the Philippines through 2027. This investment focuses on expanding factory capacity, upgrading technology, and improving manufacturing efficiency across its five production facilities, including Cabuyao, Laguna, Batangas, and Cagayan de Oro.

Philippines Pet Food Market Report Scope

Pet food refers to animal feed specifically designed, formulated, and manufactured for domestic pets, primarily dogs and cats. It is intended to provide complete and balanced nutrition, including proteins, fats, vitamins, and minerals, or to serve as treats.

The Philippines pet food market report provides a comprehensive analysis across key segments of the industry. The market is categorized by pet food product into food, pet nutraceuticals or supplements, pet treats, and pet veterinary diets. It is further segmented by pet type into cats, dogs, and other pets, and by distribution channel into convenience stores, online platforms, specialty stores, supermarkets and hypermarkets, and other channels. Market estimates and forecasts are presented in terms of value expressed in USD and volume measured in metric tons.

| Food | By Sub-Product | Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||

| Wet Pet Food | |||

| Pet Nutraceuticals/Supplements | By Sub-Product | Milk Bioactives | |

| Omega-3 Fatty Acids | |||

| Probiotics | |||

| Proteins and Peptides | |||

| Vitamins and Minerals | |||

| Other Nutraceuticals | |||

| Pet Treats | By Sub-Product | Crunchy Treats | |

| Dental Treats | |||

| Freeze-dried and Jerky Treats | |||

| Soft and Chewy Treats | |||

| Other Treats | |||

| Pet Veterinary Diets | By Sub-Product | Diabetes | |

| Digestive Sensitivity | |||

| Oral Care Diets | |||

| Renal | |||

| Urinary Tract Disease | |||

| Obesity Diets | |||

| Derma Diets | |||

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Pet Food Product | Food | By Sub-Product | Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub-Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub-Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft and Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub-Product | Diabetes | ||

| Digestive Sensitivity | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary Tract Disease | ||||

| Obesity Diets | ||||

| Derma Diets | ||||

| Other Veterinary Diets | ||||

| By Pets | Cats | |||

| Dogs | ||||

| Other Pets | ||||

| By Distribution Channel | Convenience Stores | |||

| Online Channel | ||||

| Specialty Stores | ||||

| Supermarkets/Hypermarkets | ||||

| Other Channels | ||||

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms