Pipettes, Pipettors, and Accessories Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

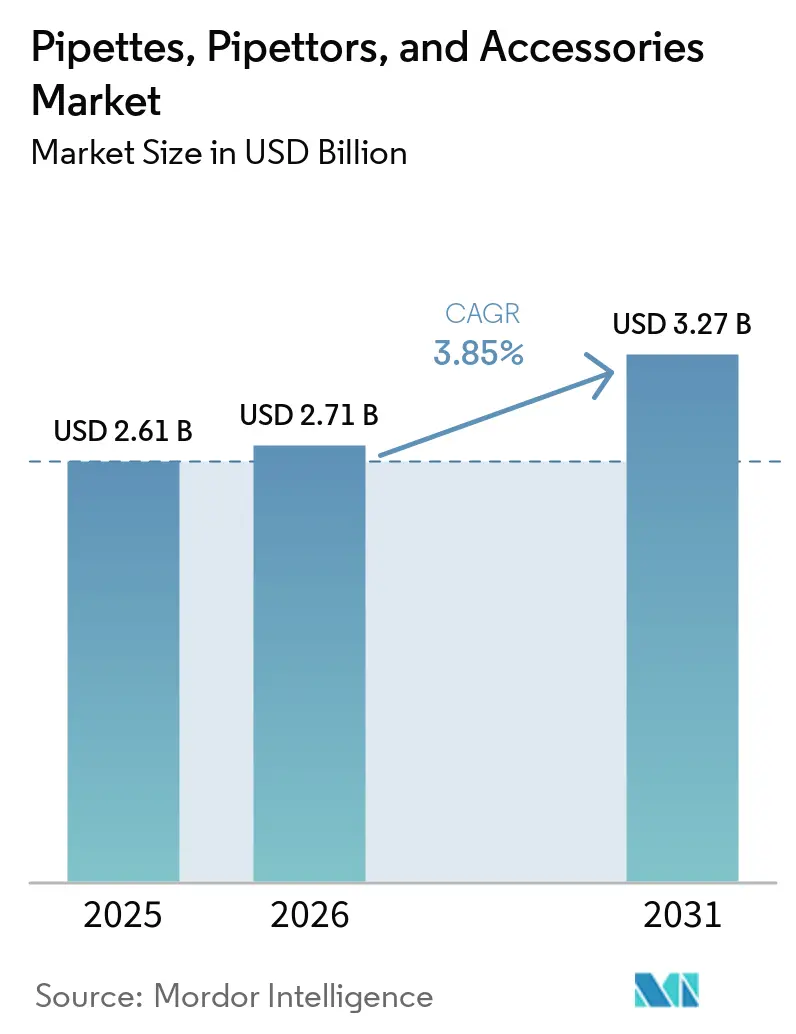

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

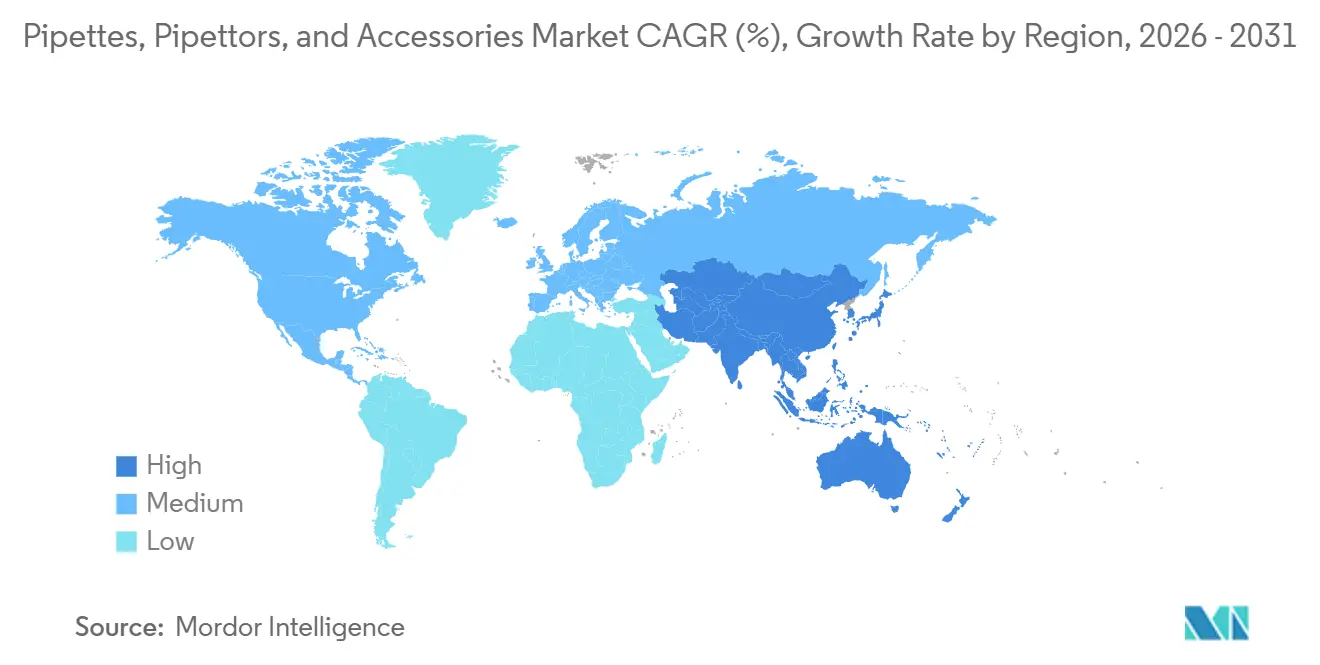

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pipettes, Pipettors, and Accessories Market Analysis by Mordor Intelligence

The Pipettes, Pipettors, And Accessories Market size is projected to be USD 2.61 billion in 2025, USD 2.71 billion in 2026, and reach USD 3.27 billion by 2031, growing at a CAGR of 3.85% from 2026 to 2031.

The market is growing because laboratories in drug discovery, genomics, and cell-based manufacturing need tighter liquid handling accuracy, stronger process control, and better documentation across routine workflows. Demand is also shifting toward products that stay embedded in daily lab operations, which raises the value of accessories, calibration systems, and software-linked tools alongside core instruments. The pipettes, pipettors, and accessories market is also being shaped by a clear move away from competition based only on mechanical precision, because buyers now look more closely at digital traceability, workflow integration, and repeatability across multi-user environments. Regional demand remains uneven, with North America holding the largest revenue base while Asia-Pacific expands faster as laboratory capacity grows across several state-backed and private life sciences programs. Competitive positioning in the pipettes, pipettors, and accessories market therefore depends on a vendor’s ability to support regulated quality requirements, recurring consumable demand, and evolving sustainability preferences without losing relevance in price-sensitive institutional channels.

Key Report Takeaways

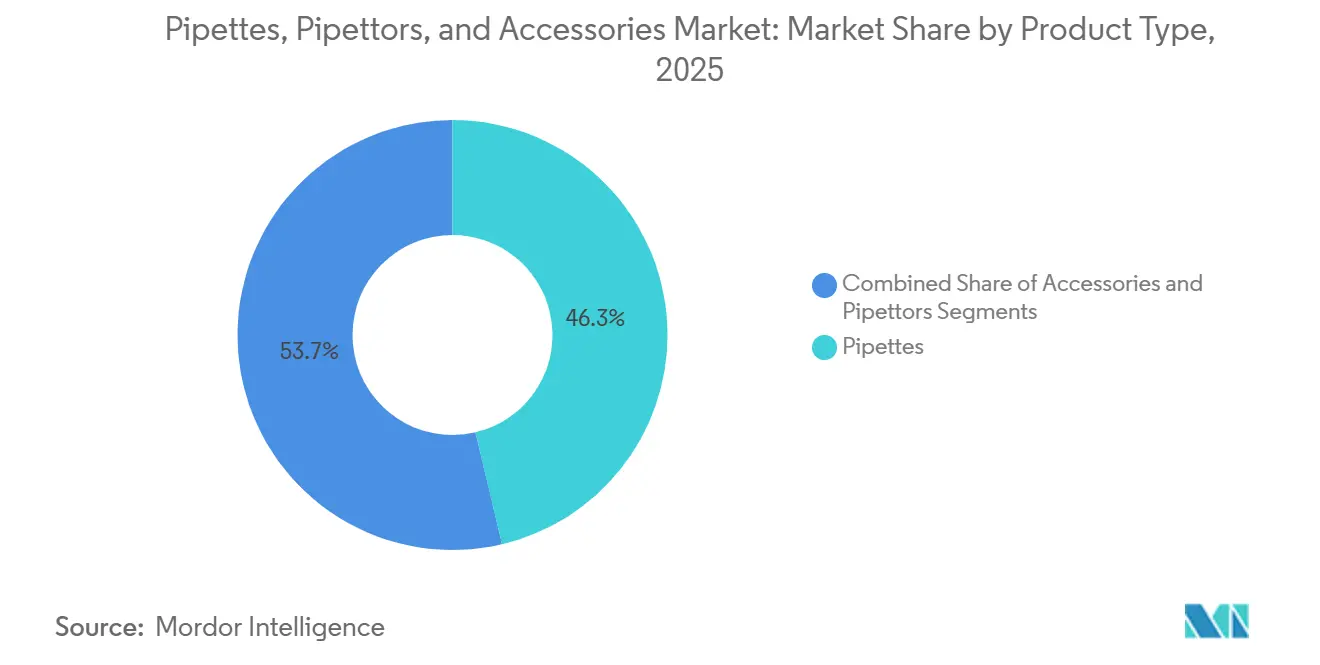

- By product type, Pipettes held 46.31% revenue share in 2025, while Accessories are forecast to expand at a 4.38% CAGR through 2031.

- By material, Glass accounted for 45.24% of revenue in 2025, while Plastic is projected to record the highest 5.52% CAGR through 2031.

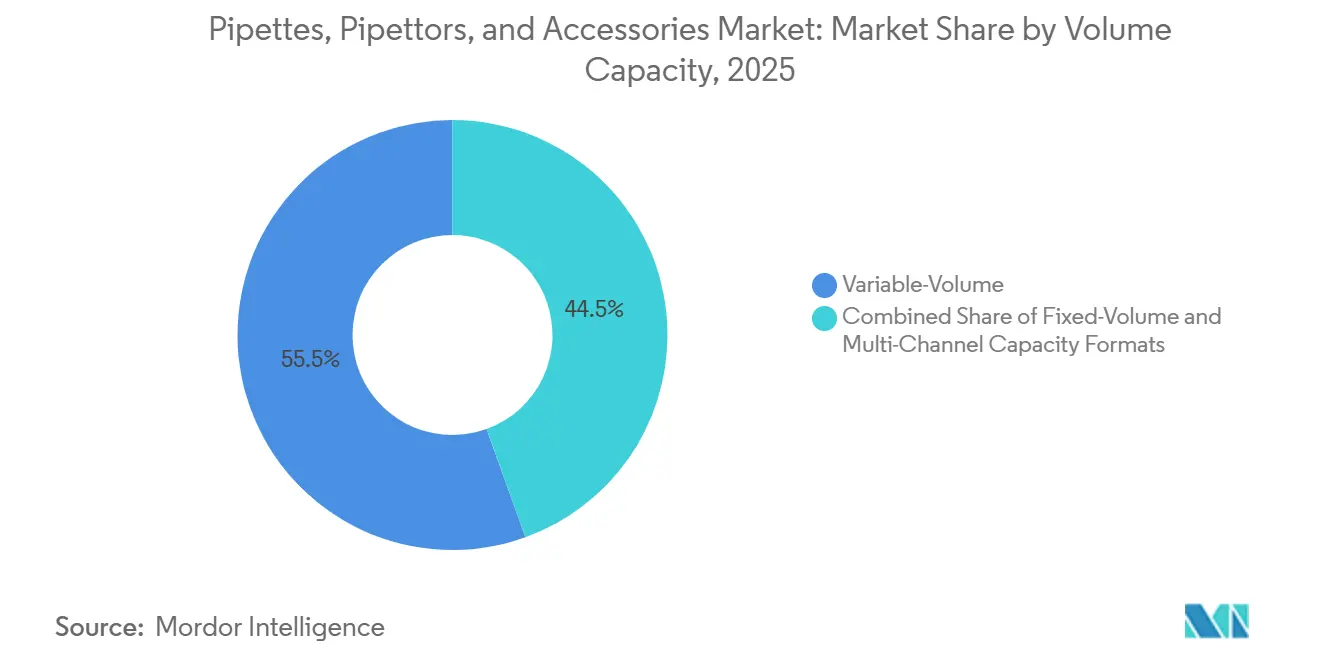

- By volume capacity, Variable-Volume formats captured 55.52% of the pipettes, pipettors, and accessories market share in 2025 and are projected to grow at a 4.25% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 38.52% of revenue in 2025, while Laboratories are forecast to grow at a 5.25% CAGR through 2031.

- By geography, North America represented 42.22% of global revenue in 2025, while Asia-Pacific is projected to expand at a 5.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pipettes, Pipettors, and Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Throughput Liquid Handling in Life Sciences | +1.0% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Expansion of Biotech, Genomics, and Cell Therapy Workflows | +0.8% | North America and EU, APAC core including China, South Korea, and Japan | Medium term (2-4 years) |

| Automation-Ready Pipettors Supporting Lab Digitization | +0.7% | North America and EU, with spillover to APAC | Medium term (2-4 years) |

| Growth in Specialized Calibration, Traceability, and Compliance Needs | +0.4% | Global, with regulatory lead in EU and North America | Short term (≤ 2 years) |

| Rising Replacement Cycle for Ergonomic and Electronic Pipettes | +0.3% | Global, with highest churn in pharmaceutical and CRO labs | Short term (≤ 2 years) |

| Sustainability Shift Toward Reusable and Lower-Waste Accessories | +0.2% | Europe first, followed by North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Throughput Liquid Handling in Life Sciences

The pipettes, pipettors, and accessories market is benefiting from the fact that modern drug discovery, genomic screening, and clinical sample processing now run at sample volumes that manual single-channel work cannot support with stable error control. Laboratories that process hundreds or thousands of samples in one run need multi-channel and electronic systems that can maintain tight consistency across repeated transfers, because even small deviations create downstream data quality issues. In this setting, buyers compare vendors less on basic advertised accuracy and more on repeatability under real operating pressure, especially in oncology biomarker work and ADMET screening programs. The pipettes, pipettors, and accessories market is therefore moving toward routine use of multi-channel electronic tools in facilities that once treated them as premium purchases reserved for only the busiest workflows. This change supports demand across both advanced automated platforms and mid-range instruments that fit existing benches without major infrastructure changes. It also makes installed workflow fit more important than standalone instrument specifications, since throughput needs now shape procurement much earlier in laboratory planning.

Expansion of Biotech, Genomics, and Cell Therapy Workflows

The pipettes, pipettors, and accessories market is seeing stronger demand from next-generation sequencing, single-cell analysis, and cell therapy workflows that require very tight liquid volume control across repeated transfer steps. In cell therapy manufacturing, a transfer error carries greater operational weight because it can affect sterile closed-system processing and, in clinical-stage settings, broader quality expectations tied to patient-facing production. Cellares had secured USD 327 million in Series D financing by June 2026 to expand automated IDMO Smart Factory capacity across South San Francisco, Bridgewater, Leiden, and Japan, and those facilities require validated liquid handling infrastructure that fits GMP expectations. Element Biosciences also announced a USD 175 million investment in June 2026 to accelerate growth across genomic, multiomic, and clinical research solutions, which supports continued upstream demand for precision liquid handling tools used in sequencing and related workflows. As a result, the pipettes, pipettors, and accessories market is tilting toward vendors that can show validated workflow fit in genomics and cell therapy rather than relying only on broad general-purpose product portfolios. That preference becomes more visible during facility buildouts, where qualification risk often matters more than price.

Automation-Ready Pipettors Supporting Lab Digitization

The pipettes, pipettors, and accessories market is also being pushed by a procurement shift toward electronic pipettors that can support digital records, user controls, and better process standardization in shared laboratory settings. Procurement decisions increasingly reflect downstream needs such as laboratory information management integration, data governance, and traceable operating histories, which means the tool is now assessed as part of a wider workflow system. This has lengthened evaluation cycles in some accounts, but it has also raised switching friction after a digital format becomes part of validated operating procedures. The pipettes, pipettors, and accessories market is therefore moving away from purely hardware-led buying patterns and toward a model in which electronic pipettors help anchor compliance and operating consistency. That shift is especially relevant in laboratories where manual documentation creates too much administrative burden for busy teams running repeated assays. Once that threshold is reached, the total cost of staying with manual processes often becomes harder to justify than upgrading to connected electronic alternatives.

Growth in Specialized Calibration, Traceability, and Compliance Needs

The pipettes, pipettors, and accessories market is gaining from tighter calibration and traceability expectations, because compliance standards are pulling laboratories toward more structured monitoring routines and better documented volumetric control. ISO 8655-7:2022 Amendment 1, published in February 2024, introduced stricter requirements around calibration test volumes, balance readability, and alternative measurement procedures, which raised the technical bar for calibration programs. This change expands demand beyond annual certification alone, because laboratories now place greater value on continuous monitoring support, calibration accessories, and software-backed recordkeeping. Sartorius launched the Cubis II Single Channel Pipette Calibration System in September 2025 to streamline ISO-compliant calibration for pipettes from 2 to 5,000 µL, which directly addresses the operational complexity of managing larger multi-volume fleets[1]Sartorius AG, “Introducing the Cubis II Pipette Calibration System, A Complete Game-Changer for Fast, ISO-Compliant Calibration of Single Channel Pipettes,” Sartorius Newsroom, sartorius.com. In practice, stricter compliance rules often pull through demand for multiple products at once, since a laboratory replacing non-traceable instruments usually also needs compatible calibration support. The pipettes, pipettors, and accessories market therefore benefits not only from fresh instrument sales but also from recurring service and workflow revenue linked to regulatory discipline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity in Academic and Public Laboratories | -0.3% | Global, highest in developing markets and public-sector labs | Short term (≤ 2 years) |

| Calibration Burden and Downtime in Regulated Workflows | -0.2% | EU and North America in GMP-regulated facilities | Medium term (2-4 years) |

| Consumable Compatibility Lock-In and Vendor Switching Friction | -0.3% | Global | Long term (≥ 4 years) |

| Counterfeit and Low-Quality Tip Supply in Cost-Driven Channels | -0.2% | APAC, South America, and MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity In Academic And Public Laboratories

The pipettes, pipettors, and accessories market faces a clear revenue limit in academic and publicly funded laboratories, because many of these buyers work within fixed annual budgets that constrain adoption of higher-priced electronic instruments. In many emerging-market institutions, glass pipettes remain the default option because unit cost still drives procurement more strongly than long-term operating efficiency. That pattern helps lower-cost manufacturers from India and China win entry-level demand, especially where purchase reviews focus more on list price than on calibration intervals, ergonomic effects, or total ownership cost. Budget pressure also slows the transition to connectivity-enabled systems even when performance gains are clear and well understood by technical staff. The pipettes, pipettors, and accessories market therefore sees value growth pulled more heavily toward pharmaceutical, biotechnology, and commercial laboratory accounts where spending can support better specifications. Academic demand remains meaningful in unit terms, but it grows more slowly in value because purchasing skews toward basic formats.

Calibration Burden And Downtime In Regulated Workflows

The pipettes, pipettors, and accessories market also faces slower upgrade cycles in GMP-regulated settings because calibration is not just a technical event, but a broader documentation and scheduling burden across large installed fleets. When a single instrument falls out of compliance, the operational consequences can extend into batch review, protocol scrutiny, and extra quality oversight, which makes downtime a serious purchasing concern. The updated ISO framework has intensified this burden by requiring more structured calibration practices, which raises labor and recordkeeping needs for facilities without dedicated internal calibration resources. Smaller CROs and mid-size pharmaceutical manufacturers are affected more sharply because they must spread that compliance cost across a smaller fleet base. This slows replacement timing even where electronic systems could improve long-term traceability and workflow control. Vendors that can reduce downtime through integrated calibration solutions are better placed to turn this restraint into a practical commercial advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accessories Segment Extends Instrument Revenue Lifecycle

Pipettes held 46.31% of product type revenue in 2025, giving them the leading position in the pipettes, pipettors, and accessories market share across this segmentation. Their lead reflects the fact that they remain the basic liquid transfer tool across research, testing, manufacturing, and clinical laboratory settings. Pipettors form the middle layer of the product mix, spanning single-channel, multi-channel, and electronic formats that serve increasingly differentiated workflow needs. Within that group, electronic variants are gaining internal weight as digital traceability and repeatable operating controls become more important in GMP and ISO-accredited environments. Eppendorf launched the Research 3 neo in September 2025 with accuracy that exceeds ISO 8655 requirements and a dual-speed volume setting mechanism, which shows how established suppliers are repositioning the core pipette as a configurable platform rather than a simple commodity device[2]Eppendorf SE, “Eppendorf Unveils Next-Generation Pipettes Delivering Enhanced Adaptability, Precision, and Comfort,” Eppendorf Newsroom, eppendorf.com.

Accessories are forecast to expand at a 4.38% CAGR from 2026 to 2031, which makes them the fastest-growing product category in the pipettes, pipettors, and accessories market. Their growth reflects the commercial value of recurring consumables, calibration support items, and other workflow-linked products that remain in use long after the original instrument sale. Once a laboratory adopts a proprietary tip format or accessory ecosystem, that choice often remains in place across several refresh cycles, which strengthens retention more than single instrument purchases do. Sustainability preferences are also feeding accessory demand, since buyers increasingly review refill systems, lower-waste packaging, and alternative materials during routine procurement. This means the revenue relationship between supplier and customer is being shaped less by one-time instrument replacement and more by the daily operating products that surround that installed base.

By Material: Plastic Gains Ground On Sustainability And Automation Compatibility

Glass accounted for 45.24% of revenue in 2025, making it the largest material category in the pipettes, pipettors, and accessories market size by share for that year. Its position remained strongest in volumetric measurement, serological pipettes, and settings where solvent resistance and proven lab familiarity still shape specifications. Stainless steel continued to serve smaller specialized applications such as dispensing needles, cannula formats, and other accessory types where repeated autoclaving or chemical exposure limits polymer use. Even so, material choice is no longer guided only by chemical performance, because automation readiness and procurement policy are changing the basis of comparison. Laboratories are looking more closely at dimensional consistency, operational waste, and the ability of a material system to support high-throughput robotic or semi-automated handling.

Plastic is forecast to grow at a 5.52% CAGR from 2026 to 2031, which makes it the fastest-expanding material segment within the pipettes, pipettors, and accessories market. This growth is linked to both sustainability programs and the spread of automated workflows that depend on consistent polymer tips and accessory formats. Hamilton’s GreenLine CO-RE II tips are manufactured from 65% to 75% ISCC PLUS-certified bio-circular polypropylene, and the company states that the raw material carbon footprint is nearly 111% lower than fossil-grade alternatives. The move away from glass is progressing faster in cost-sensitive and logistics-sensitive markets, while European institutions are balancing recyclability and compliance concerns more gradually. Glass will retain a place in applications where precision measurement and solvent resistance remain decisive, but plastic is gaining where scale, automation fit, and procurement criteria increasingly converge.

By Volume Capacity: Variable-Volume Formats Dominate Versatility-Driven Procurement

Variable-Volume formats held 55.52% of global revenue in 2025 and are forecast to grow at a 4.25% CAGR through 2031, which keeps them in the leading position within the pipettes, pipettors, and accessories market. Their strength comes from broad protocol flexibility, because one instrument can handle a wider range of assay volumes across mixed laboratory workloads. This matters in settings where staff move between different sample types and plate formats during the same work cycle. Fixed-Volume pipettes continue to serve standardized high-throughput processes where eliminating operator adjustment helps reduce one source of human error. They also retain value in regulated workflows where a specific fixed setting can support control discipline and repeatability across repeated protocol steps.

Multi-channel capacity formats are gaining momentum inside this segmentation because plate-based genomics, immunoassay, and screening workflows need simultaneous dispensing that single-channel methods cannot match at scale. The operational appeal of this format lies in faster cycle times, less repetitive handling, and more stable cross-well consistency during routine processing. Adjustable tip-spacing tools extend that same logic further by helping users transfer between different labware footprints without breaking the process into multiple manual steps. That design is especially relevant in research environments where sample containers and target formats vary throughout an experiment. As a result, leadership in this segment will depend increasingly on how well suppliers serve multi-format workflow reality rather than on whether they optimize for only one standard plate configuration.

By End User: Pharmaceutical And Biotechnology Companies Set The Quality Baseline

Pharmaceutical and biotechnology companies accounted for 38.52% of global revenue in 2025, which made them the largest end-user group in the pipettes, pipettors, and accessories market. Their procurement behavior differs from that of many other buyers because vendor approval, regulatory documentation, and validated compatibility tables often shape the purchase more than list price does. This concentrates spending among suppliers that can meet qualification standards consistently across instruments, consumables, and traceability requirements. In these accounts, the cost of failure or non-compliance is far greater than the cost difference between a premium and a basic pipetting system. That dynamic helps explain why higher-value demand remains concentrated in regulated commercial life sciences environments.

Laboratories, including CROs, CDMOs, and independent testing facilities, are forecast to grow at a 5.25% CAGR from 2026 to 2031, making them the fastest-growing end-user category in the pipettes, pipettors, and accessories industry. Their growth reflects both expansion at existing outsourced service providers and new capacity coming online in regions where pharmaceutical companies continue to rely on external research and testing support. Hospitals remain a smaller but stable source of demand, mainly in clinical chemistry, hematology, and molecular diagnostics workflows where transfer accuracy affects patient result validity. Academic and research institutes still buy meaningful volumes, especially in manual and glass-based formats, but budget pressure limits their value growth. Other end users such as food safety, environmental testing, and forensic laboratories are also adding steady demand as testing standards become more formal and quality expectations move closer to life sciences practice.

Geography Analysis

North America accounted for 42.22% of global revenue in 2025, which gave the region the largest position in the pipettes, pipettors, and accessories market share by geography. Its lead reflects the concentration of large biopharma research campuses, federally funded genomics activity, and a deep CRO base that supports outsourced pharmaceutical work. The region also favors premium specifications, because regulated buyers place strong emphasis on validated performance, documentation, and digital audit readiness. That mix keeps revenue per unit above many other regions and supports replacement demand for older manual fleets as laboratories move toward more traceable electronic formats.

Europe remained the second-largest regional market and carried a particularly strong manufacturing base for precision liquid handling products, especially in Germany, Switzerland, and Denmark. Demand in the region is supported by strict compliance frameworks, a dense installed base of quality-focused laboratories, and procurement processes that reward calibration readiness and documented performance. Sartorius strengthened that position in September 2025 with the launch of the Cubis II Single Channel Pipette Calibration System, which supports faster ISO-compliant calibration and reinforces the company’s broader software-linked quality offering. Sustainability is also more visible in European vendor selection than in many other regions, which gives suppliers with certified lower-waste accessories an early advantage.

Asia-Pacific is forecast to grow at a 5.15% CAGR from 2026 to 2031, making it the fastest-growing regional component of the pipettes, pipettors, and accessories market. China continues to build capacity in oncology, genomics, and precision medicine, which supports expanding need for dependable liquid handling tools across research and development settings. Japan remains an important market for precision instruments with clinical laboratory and pharmaceutical quality testing as stable demand anchors. India is becoming more specification-conscious as production-linked incentives and broader healthcare infrastructure investment reshape procurement priorities beyond basic price considerations. South America and the Middle East and Africa remain smaller in scale, but both are adding incremental demand through growth in clinical diagnostics, pharmaceutical quality control, and more formal laboratory operating standards.

Competitive Landscape

The pipettes, pipettors, and accessories market remains moderately fragmented, with a cluster of established European and American suppliers holding stronger positions in premium electronic and multi-channel formats while many regional and mid-tier players compete in manual tools and standard accessories. This structure means competitive advantage is built not only on precision, but also on installed base depth, consumable retention, compliance support, and the ability to fit into validated workflows. The recurring revenue model matters greatly, because tip replenishment, accessory replacement, and calibration services often create more durable value than one-time instrument sales. The pipettes, pipettors, and accessories market therefore rewards suppliers that can keep customers inside a wider operating ecosystem rather than winning only the initial equipment order.

Product strategy is moving toward platform thinking rather than single-device selling. Eppendorf’s September 2025 launch of the Research 3 neo reflected that shift by emphasizing higher adaptability, comfort, and ISO-exceeding accuracy in a format designed to stay relevant across varied workflows. Sartorius followed a different but related path with the Cubis II Single Channel Pipette Calibration System, using calibration workflow simplification to deepen quality-system relevance beyond the pipette itself. These examples show that leading companies are competing by widening the operational role of their offering, not by relying only on base instrument precision.

Accessories are becoming a stronger area of rivalry because proprietary tip compatibility still helps protect recurring revenue, yet sustainability expectations are opening the door for material innovation and alternative procurement criteria. Hamilton’s GreenLine consumables illustrate this direction, since the company is linking accessory design to formal sustainability goals through bio-circular polypropylene inputs[3]Hamilton Company, “GreenLine Tip, Sustainable Automated Pipette Tip,” Hamilton Company Official Website, hamiltoncompany.com. This matters because many institutional buyers now review waste, traceability, and carbon disclosures alongside performance and price. Mid-tier suppliers from India, Denmark, Switzerland, Japan, and China remain relevant by focusing on application-specific designs, quicker customization, and lower upfront cost in accounts where top-tier premium pricing is harder to justify. The pipettes, pipettors, and accessories market is unlikely to consolidate into a highly concentrated structure soon, but competitive pressure will keep increasing as digital fit, regulatory support, and consumable strategy become more closely linked.

Pipettes, Pipettors, and Accessories Industry Leaders

Thermo Fisher Scientific Inc.

Eppendorf SE

Sartorius AG

Mettler-Toledo International Inc.

Hamilton Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DeNovix Inc. launched the Squid Full Range Pipette, covering a wide 1 – 1000 µL volume range. It replaced three to five traditional pipettes, streamlining workflows by removing the need to switch devices during experiments.

- March 2026: Thermo Fisher Scientific introduced the Fluid Ease Pro ClipTip electronic pipette with a 2.0-inch color touchscreen, Bluetooth 5.0, USB-C charging, support for five user profiles, and custom calibration. It ensures consistent pipetting in shared lab environments.

Global Pipettes, Pipettors, and Accessories Market Report Scope

As per the scope of the report, pipettes and pipettors are precision tools used to measure and transfer specific liquid volumes in laboratories. Accessories include tips, stands, and calibration tools that support proper pipetting.

The segmentation for the pipettes, pipettors, and accessories market is categorized by product type, material, volume capacity, end user, and geography. By product type, the market includes pipettes (air displacement pipettes, positive displacement pipettes, micro-pipettes, manual pipettes, and digital pipettes), pipettors (single-channel pipettors, multi-channel pipettors, and electronic pipettors), and accessories. By material, the market is segmented into glass, plastic, and stainless steel. By volume capacity, it is divided into fixed-volume, variable-volume, and multi-channel formats. By end user, the market is segmented into hospitals, laboratories, academic and research institutes, pharmaceutical and biotechnology companies, and other users. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Pipettes | Air Displacement Pipettes |

| Positive Displacement Pipettes | |

| Micro-Pipettes | |

| Manual Pipettes | |

| Digital Pipettes | |

| Pipettors | Single-Channel Pipettors |

| Multi-Channel Pipettors | |

| Electronic Pipettors | |

| Accessories |

| Glass |

| Plastic |

| Stainless Steel |

| Fixed-Volume |

| Variable-Volume |

| Multi-Channel Capacity Formats |

| Hospitals |

| Laboratories |

| Academic and Research Institutes |

| Pharmaceutical and Biotechnology Companies |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Pipettes | Air Displacement Pipettes |

| Positive Displacement Pipettes | ||

| Micro-Pipettes | ||

| Manual Pipettes | ||

| Digital Pipettes | ||

| Pipettors | Single-Channel Pipettors | |

| Multi-Channel Pipettors | ||

| Electronic Pipettors | ||

| Accessories | ||

| By Material | Glass | |

| Plastic | ||

| Stainless Steel | ||

| By Volume Capacity | Fixed-Volume | |

| Variable-Volume | ||

| Multi-Channel Capacity Formats | ||

| By End User | Hospitals | |

| Laboratories | ||

| Academic and Research Institutes | ||

| Pharmaceutical and Biotechnology Companies | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for pipettes, pipettors, and accessories through 2031?

The sector was valued at USD 2.61 billion in 2025, reaches USD 2.71 billion in 2026, and is forecast to reach USD 3.27 billion by 2031 at a 3.85% CAGR.

Which product area is expanding the fastest?

Accessories are projected to grow at a 4.38% CAGR through 2031, helped by recurring consumables demand, calibration needs, and stronger customer retention around installed instrument bases.

Why do pharmaceutical and biotechnology companies lead demand?

They held 38.52% of revenue in 2025 because procurement in regulated settings depends on validated performance, documentation, and approved compatibility standards rather than price alone.

Which material category has the strongest growth outlook?

Plastic is expected to post the fastest 5.52% CAGR through 2031, supported by automation compatibility and rising interest in certified lower-impact materials.

Which region offers the best growth prospects?

Asia-Pacific is forecast to grow at a 5.15% CAGR through 2031 as research, testing, and manufacturing capacity expands across major life sciences markets.

What is shaping competition most strongly now?

Competition is moving toward digital traceability, calibration support, recurring consumables strategy, and sustainability-linked accessory portfolios rather than mechanical precision alone.

Page last updated on: