Endotracheal Tube Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

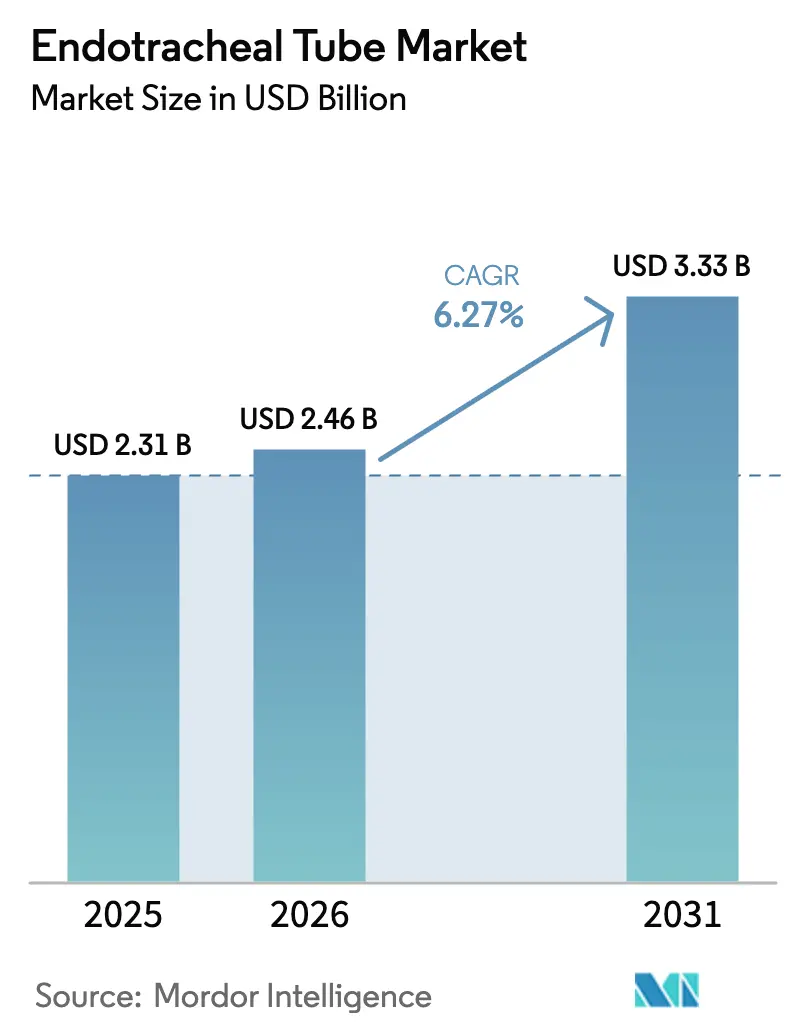

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 3.33 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

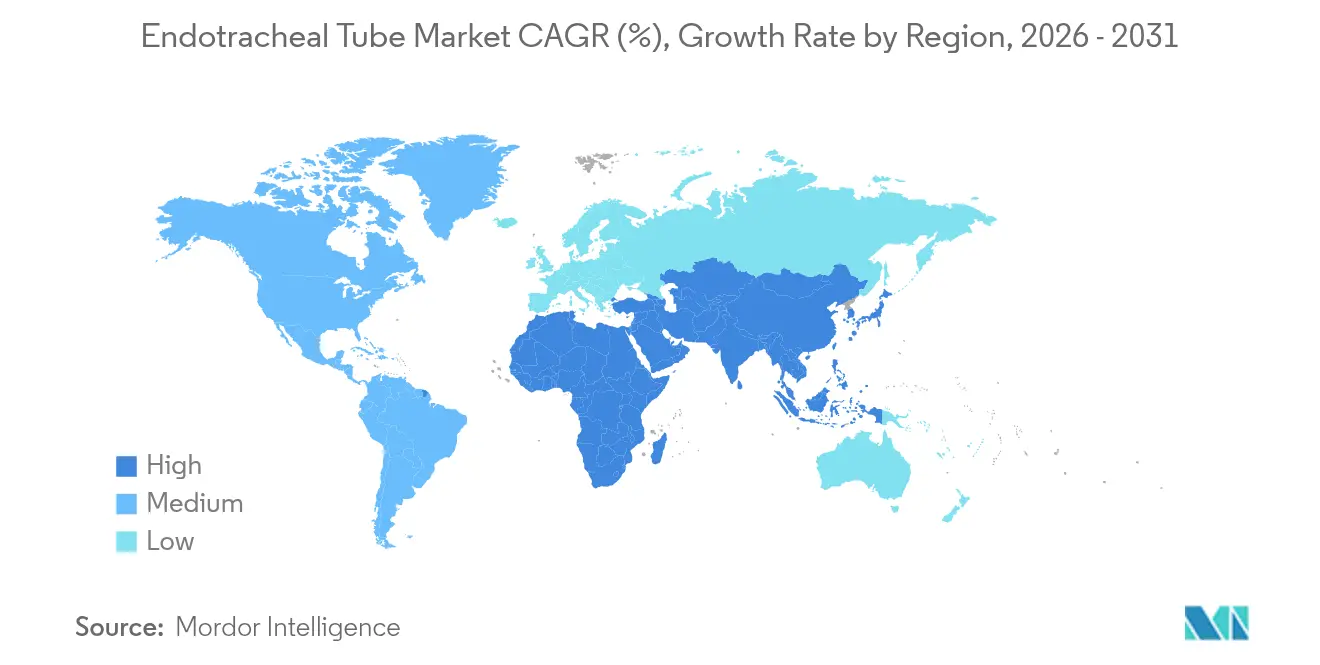

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endotracheal Tube Market Analysis by Mordor Intelligence

The endotracheal tube market size is expected to grow from USD 2.31 billion in 2025 to USD 2.46 billion in 2026 and is forecast to reach USD 3.33 billion by 2031 at 6.27% CAGR over 2026-2031. Growth stems from surging surgical volumes, rising chronic disease burden that lengthens ventilation time, and quick uptake of video-enabled intubation systems that improve first-pass success rates.[1]Geraghty E., “Video versus Direct Laryngoscopy for Urgent Intubation,” New England Journal of Medicine, nejm.org Infection-prevention protocols push demand for antimicrobial coatings, while sustainability rules in Europe spur experimentation with bio-based polyurethanes that meet clinical and environmental standards. Supply-chain fragility remains a headline risk after pediatric device shortages led the FDA to monitor production bottlenecks and encourage hospitals to diversify suppliers.[2]Center for Devices and Radiological Health, “Medical Device Supply Chain Vulnerabilities,” fda.gov Competitive positioning revolves around technology rather than price, so manufacturers that bundle tubes with imaging or smart monitoring gain an edge in hospital tenders.

Key Report Takeaways

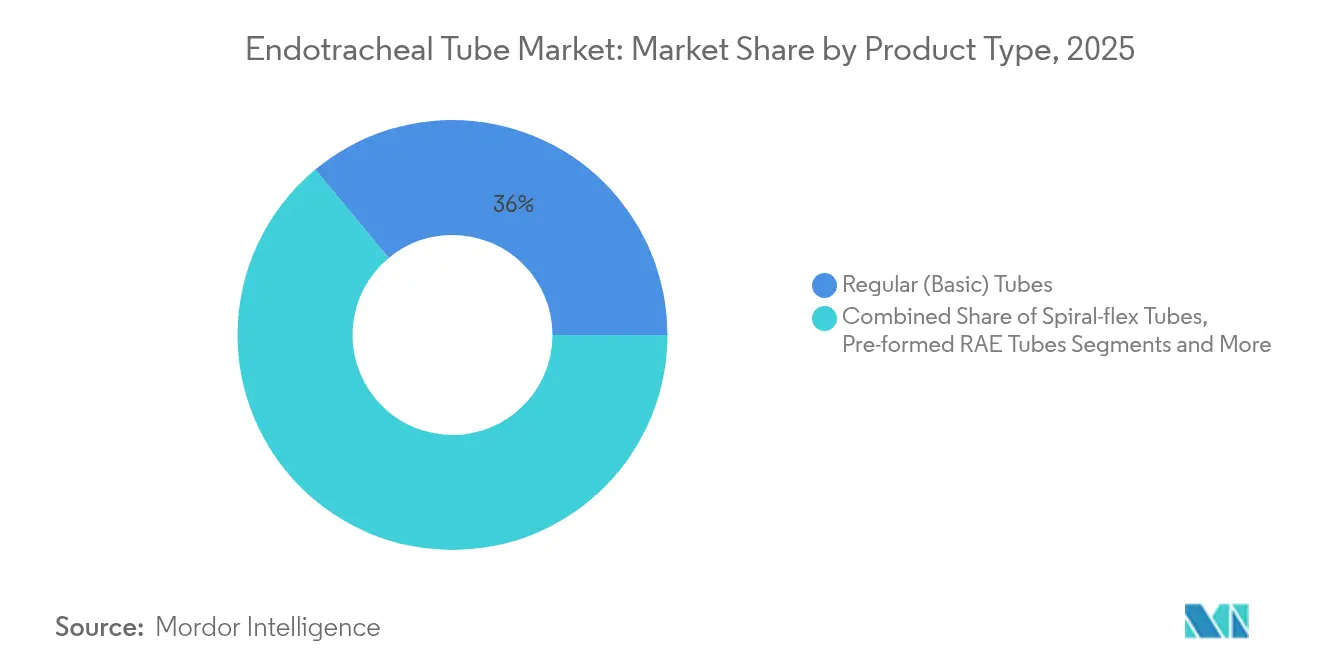

- By product type, regular basic tubes accounted for 36.02% of the endotracheal tube market share in 2025, whereas video-enabled tubes are projected to grow at a 10.12% CAGR through 2031.

- By route, orotracheal intubation held 68.25% of the endotracheal tube market share in 2025, while nasotracheal applications are set to expand at an 8.67% CAGR.

- By end user, hospitals commanded 58.89% share of the endotracheal tube market size in 2025, and pre-hospital emergency medical services are advancing at a 9.02% CAGR to 2031.

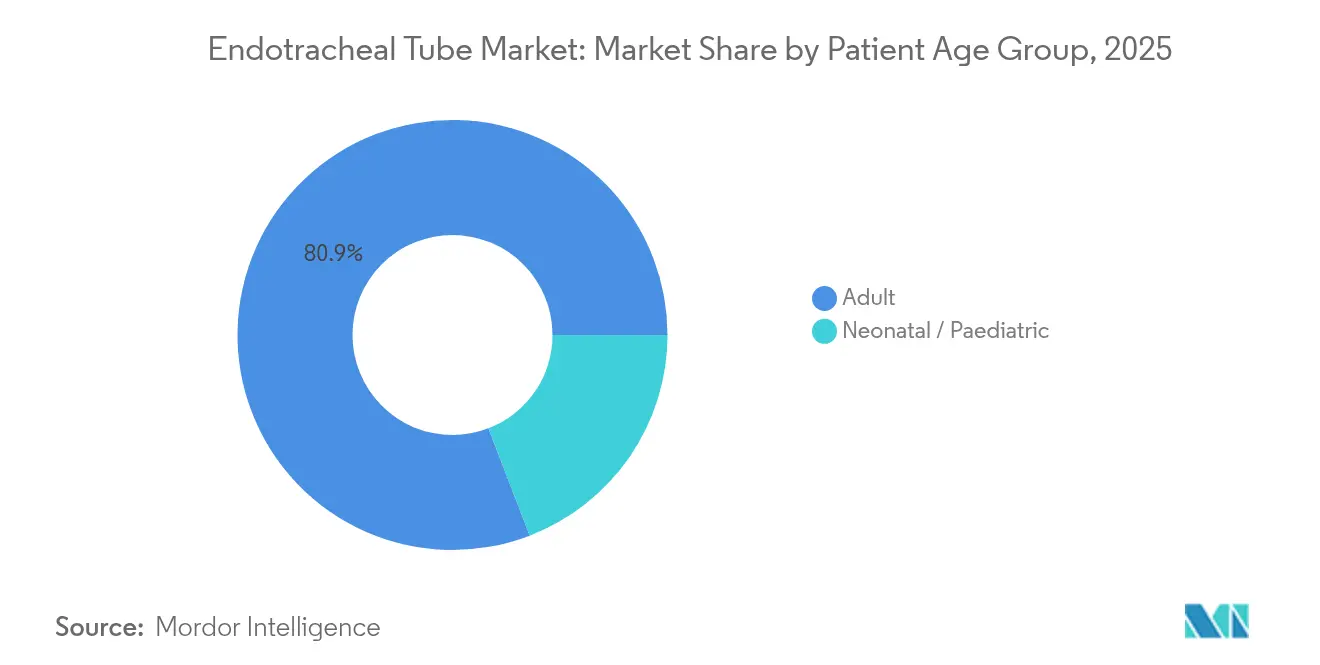

- By patient age group, adults represented 80.85% share, whereas neonatal and pediatric demand is rising at a 6.97% CAGR.

- By material, PVC dominated with 65.92% share, but polyurethane and other alternatives are forecast to increase at an 8.01% CAGR.

- By geography, North America led with 31.88% revenue share in 2025; Asia Pacific is the fastest-growing region at an 8.16% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Endotracheal Tube Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Incidence Of Chronic Diseases | +1.2% | Global, with concentration in aging populations of North America & Europe | Long term (≥ 4 years) |

| Rising Number Of Surgical Procedures | +1.8% | Global, led by APAC expansion and North American volume growth | Medium term (2-4 years) |

| Technological Advancements In Tube Design & Materials | +1.1% | North America & EU leading innovation, APAC adoption following | Medium term (2-4 years) |

| AI-Enabled Cuff Pressure Monitoring Gaining Reimbursement | +0.7% | North America primarily, with EU regulatory alignment | Short term (≤ 2 years) |

| Demand For Antimicrobial & Sub-Glottic Suction Tubes To Curb VAP | +0.9% | Global ICU settings, strongest in developed markets | Medium term (2-4 years) |

| Growth In Single-Use Video-Integrated Tubes For Difficult Airway | +0.6% | North America & EU early adoption, APAC emerging | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing incidence of chronic diseases

Greater prevalence of respiratory, cardiovascular, and neurologic illnesses lengthens ventilation duration and lifts tube consumption. Aging populations intensify these needs, prompting hospitals to expand ICU capacity and adopt tubes with antimicrobial coatings that cut ventilator-associated pneumonia, which affects roughly 30% of ventilated patients.[3]Li W. et al., “Incidence and risk factors of ventilator-associated pneumonia,” Journal of Thoracic Disease, jtd.amegroups.org The link between chronic disease and airway demand is strongest in North America and Europe, where comorbidities complicate surgical recovery.

Rising number of surgical procedures

Every general anesthesia case requires a secure airway, so escalating surgical volume directly boosts demand. Asia Pacific is adding operating rooms fastest, while North America maintains high volume. Complex thoracic and trauma procedures favor double-lumen or reinforced tubes, and emergency cases amplify the call for antimicrobial options that limit infection risk. Hospitals therefore juggle inventory across multiple specialized SKUs to stay prepared.

Technological advances in tube design and materials

Thermally softened polyurethane tubes lower postoperative sore throat prevalence and vocal cord injury, especially in double-lumen use. European rules effective 2026 curtail single-use plastics, pushing manufacturers toward recyclable or bio-based polymers that satisfy both clinicians and regulators. R&D therefore focuses on balancing flexibility, biocompatibility, and sustainability.

AI-enabled cuff pressure monitoring gaining reimbursement

Continuous monitoring keeps cuff pressure within target ranges more consistently than manual checks, cutting aspiration risk. CMS reimbursement decisions in 2025 remove cost barriers, so hospitals can deploy automated systems that ease nursing workload and potentially lower VAP incidence. Early adopters in the United States influence practice guidelines that spread to Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability Of Alternate Supraglottic Airway Devices | -0.8% | Global, with higher adoption in emergency medicine settings | Medium term (2-4 years) |

| High Frequency Of Product Recalls & Related Litigations | -1.1% | North America & EU primarily, due to stringent regulatory oversight | Short term (≤ 2 years) |

| Medical-Grade PVC & Silicone Supply Constraints | -0.7% | Global supply chain impact, concentrated in Asia manufacturing hubs | Medium term (2-4 years) |

| EU Sustainability Rules Discouraging Single-Use Plastics | -0.4% | EU primarily, with spillover effects in export markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of alternate supraglottic airway devices

Paramedics favor supraglottic devices for speed during out-of-hospital cardiac arrest, where survival hinges on quick oxygenation. Studies show higher 72-hour survival than with endotracheal intubation in some protocols, although immediate survival favors tubes. This creates substitution risk for short-duration or prehospital scenarios.

High frequency of product recalls and related litigations

Design flaws have triggered class I recalls, such as Medtronic’s withdrawal of reinforced EMG tubes for airway-obstruction risk. Hospitals react by vetting suppliers more rigorously and diversifying vendors, which slows decision cycles and adds compliance costs for manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Video technology drives premium growth

The endotracheal tube market size for video-integrated models is set to expand at a 10.12% CAGR, well above the overall trajectory. Regular basic tubes remain the volume anchor with 36.02% of the endotracheal tube market share in 2025. Hospitals accept the higher upfront price for Ambu VivaSight 2 DLT after cost-benefit reviews showed USD 47.65 savings per thoracic case thanks to faster positioning and fewer replacements. Reinforced spiral-flex tubes serve prolonged surgeries that risk kinking, while antimicrobial and sub-glottic suction designs migrate from tertiary ICUs into secondary-level hospitals as infection control audits tighten.

Procurement patterns confirm that specialty devices move the category away from commodity status. OEMs pitch outcome data to justify premiums and bundle training modules that shorten learning curves. Demand for double-lumen tubes stays resilient in thoracic and cardiac suites, and R&D continues to miniaturize integrated optics to fit smaller diameters for pediatric use.

By Route: Nasotracheal applications gain momentum

Orotracheal placement continues as the clinical default, carrying 68.25% share in 2025. Nasotracheal procedures, however, will grow 8.67% annually through 2031 as maxillofacial and dental surgeries rise and as trauma cases where the oral path is not viable gain attention. Video laryngoscopes equalize success rates across both routes, with neonatology data showing marked improvement in first-pass outcomes when visual guidance is used.

Training curricula increasingly teach route selection based on anatomy and scenario rather than habit, resulting in more nuanced practice. Manufacturers respond with route-specific curvature and smaller proximal connectors that accommodate concurrent surgical access, thereby enriching the portfolio and boosting cross-selling opportunities.

By End User: Emergency services drive expansion

Hospitals purchase in bulk and held 58.89% of volume in 2025, but the fastest line item belongs to pre-hospital emergency medical services at a 9.02% CAGR. National programs that certify paramedics in advanced airway skills have lifted adoption of compact, single-use tubes with integrated stylets. EMS teams value light weight, pre-loaded designs that speed deployment, and reimbursement policies now recognize these disposables as lifesaving essentials.

Ambulatory surgical centers and outpatient clinics also raise baseline demand as day-case volumes climb. Procurement splits into high-volume, low-complexity tubes for routine sedation and premium specialized designs for longer cases, prompting distributors to widen catalog breadth.

By Patient Age Group: Neonatal specialization creates value

Adults still dominate volumes, capturing 80.85% share in 2025, yet neonatal and pediatric requirements show the clearest room for technology-led differentiation. That segment is projected to grow 6.97% per year, underpinned by evidence that video laryngoscopy lifts neonatal first-pass success and that standardized insertion depth protocols cut malposition rates to 25% from previous norms.

Smaller tubes impose tight tolerances on wall thickness and cuff integrity, driving investment in precision extrusion and laser welding. Hospitals are willing to pay premiums for correctly sized neonatal sets, since failed placement risks hypoxia and elevates ICU stay costs.

By Material: Sustainability drives innovation

PVC continues as the workhorse polymer, supported by installed sterilization infrastructure and clinician familiarity, giving it 65.92% share in 2025. Polyurethane lines, including bio-based formulations, will grow 8.01% yearly. Early adopters praise their flexibility and reduced need for phthalate plasticizers, which regulators sometimes scrutinize. Silicone remains an option for electromyography tubes needing electrical neutrality, though supply tightness and cost restrain broader uptake.

EU mandates push the entire supply chain to redesign packaging and seek recyclability certifications. Several producers pilot biodegradable thermoplastic polyurethanes derived from castor oil, aiming to secure regulatory approvals before the 2026 enforcement date.

Geography Analysis

North America maintains leadership with 31.88% of the endotracheal tube market in 2025, thanks to entrenched surgical capacity and early adoption of video guidance and AI monitoring. The region also confronts supply shortages that disproportionately hit pediatric units, prompting the FDA to manage real-time shortage lists and advise on alternative suppliers. Reimbursement support for smart cuff monitoring accelerates hospital purchases, reinforcing premium-skewed demand.

Europe pursues sustainability and infection control in tandem. The upcoming Packaging and Packaging Waste Regulation compels suppliers to pivot toward recyclable materials and drop single-use plastics, increasing compliance costs yet opening new niches for eco-designed offerings. Hospitals lean on antimicrobial and sub-glottic suction tubes to curb ventilator-associated pneumonia rates, particularly in ICUs with strict quality metrics.

Asia Pacific is the growth engine with an 8.16% CAGR through 2031. China’s doctor headcount is projected to reach 5.93 million by 2025, and India’s investment in trauma centers raises demand for reliable airway tools. In many facilities, ventilation costs already exceed USD 15,000 per ICU patient, so administrators pay closer attention to tubes that shorten weaning and prevent complications. Procurement still favors cost-effective PVC models, yet premium segments scale quickly once reimbursement frameworks mature.

Competitive Landscape

The endotracheal tube industry shows moderate consolidation. Top players pursue differentiation via integrated imaging, antimicrobial coatings, and smart monitoring rather than aggressive discounting. BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care group broadens its connected-care platform. Medtronic acquired Aircraft Medical for video laryngoscopes to complement its tube portfolio, while Teleflex plans a corporate split to sharpen focus on high-growth airway products.

White-space remains in neonatal and EMS sub-markets where specialized sizing and portability requirements erect entry barriers. Manufacturers that bundle tubes with compatible laryngoscopes and monitoring apps create ecosystems that lock in customers. Smaller innovators often license antimicrobial coatings or biodegradable polymers to incumbents that can scale production and navigate global regulatory pathways.

Strategic moves highlight the premium on technological proof. Ambu publishes cost-saving data for its VivaSight line, Medtronic emphasizes AI cuff monitoring outcomes, and PVC incumbents accelerate R&D on bio-based substitutes to retain European contracts. Litigation and recalls add reputational stakes; firms with robust quality systems gain trust and purchasing preference.

Endotracheal Tube Industry Leaders

Medtronic

ICU Medical

Becton, Dickinson and Company

Angiplast Pvt Ltd

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Smiths Medical, now part of ICU Medical, issued an urgent correction for multiple ORAL/NASAL endotracheal tube sizes cited by the FDA.

- June 2024: Medline Industries recalled Sub-G Endotracheal Tubes with sub-glottic suction because inflation tube detachment could obstruct the airway.

Global Endotracheal Tube Market Report Scope

As per the scope of the report, an endotracheal tube is a medical device used to secure the airway in patients who require mechanical ventilation or have compromised breathing. It is a flexible plastic tube that is inserted through the nose into the trachea to ensure that air can flow into and out of the lungs.

The endotracheal tubes market is segmented by product type, route, end user, and geography. By product type, the market is segmented into regular endotracheal tubes, reinforced endotracheal tubes, preformed endotracheal tubes, and double-lumen endotracheal tubes. By route, the market is segmented into orotracheal and nasotracheal. By end user, the market is segmented into hospitals, clinics, ambulatory surgical centers, and other end users. The other end users segment includes homecare settings and emergency medical services. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecast have been done based on value (USD).

| Regular (Basic) Tubes |

| Reinforced / Spiral-flex Tubes |

| Pre-formed RAE Tubes (Oral & Nasal) |

| Double-lumen / Endobronchial Tubes |

| Video-enabled / Camera-integrated Tubes |

| Anti-microbial / Drug-coated Tubes |

| Sub-glottic Suction (VAP-prevention) Tubes |

| Orotracheal |

| Nasotracheal |

| Hospitals |

| Ambulatory Surgical Centres |

| Clinics & Physician Offices |

| Pre-hospital / EMS |

| Neonatal / Paediatric |

| Adult |

| PVC |

| Silicone |

| Polyurethane & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Regular (Basic) Tubes | |

| Reinforced / Spiral-flex Tubes | ||

| Pre-formed RAE Tubes (Oral & Nasal) | ||

| Double-lumen / Endobronchial Tubes | ||

| Video-enabled / Camera-integrated Tubes | ||

| Anti-microbial / Drug-coated Tubes | ||

| Sub-glottic Suction (VAP-prevention) Tubes | ||

| By Route | Orotracheal | |

| Nasotracheal | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Clinics & Physician Offices | ||

| Pre-hospital / EMS | ||

| By Patient Age Group | Neonatal / Paediatric | |

| Adult | ||

| By Material | PVC | |

| Silicone | ||

| Polyurethane & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the endotracheal tube market?

The endotracheal tube market is valued at USD 2.46 billion in 2026.

How fast is the endotracheal tube market expected to grow?

Market value is projected to rise to USD 3.33 billion by 2031 at a 6.27% CAGR.

Which product segment is growing fastest?

Video-integrated tubes are forecast to expand at a 10.12% CAGR due to their superior first-pass success rates.

Why is Asia Pacific the fastest-growing region?

Infrastructure investments, rising surgical volumes, and improved trauma care training lift Asia Pacific growth to an 8.16% CAGR.

How are sustainability regulations affecting material choices?

EU rules that restrict single-use plastics encourage a shift from PVC toward recyclable or bio-based polyurethanes, driving material innovation.

Page last updated on: